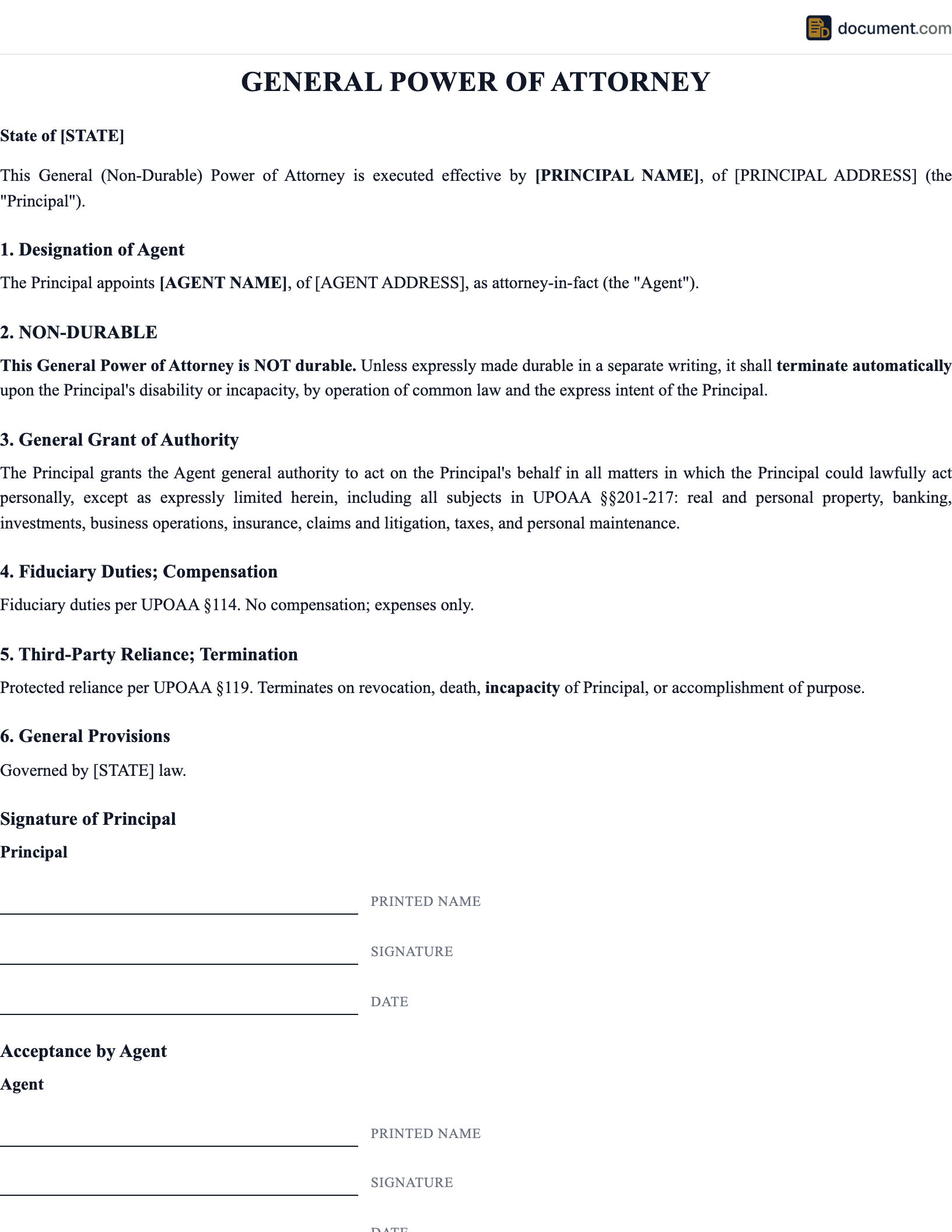

What Is a Power of Attorney?

A power of attorney is a written instrument by which one person (the principal) authorizes another (the agent, also called the attorney-in-fact) to act in legal, financial, medical, or other specified matters as if the principal were acting personally. The agent's acts bind the principal to the same extent as if the principal had taken them directly. The scope can be unlimited (a general POA), limited to specified categories (financial only, medical only, real estate only), or limited to a single transaction (closing on a specific property, signing one contract). The legal authority traces back to common-law agency: a principal may delegate by writing any act the principal could lawfully do, with limited exceptions for acts requiring the principal's personal performance (voting, executing a will, swearing an oath).

Twenty-eight states have adopted the Uniform Power of Attorney Act of 2006 in whole or substantial part: Alabama, Arkansas, Colorado, Connecticut, Georgia, Hawaii, Idaho, Iowa, Maine, Maryland, Michigan, Minnesota, Montana, Nebraska, Nevada, New Hampshire, New Mexico, North Carolina, Ohio, Oklahoma, Pennsylvania, South Carolina, Texas, Utah, Vermont, Virginia, Washington, West Virginia, and Wisconsin. The remaining states operate under state-specific statutes, with the most heavily customized regimes in California (Cal. Prob. Code § 4000 et seq.), New York (N.Y. Gen. Oblig. Law § 5-1501 et seq.), Florida (Fla. Stat. § 709.2101 et seq.), and Illinois (755 ILCS 45). The UPOAA reverses the common-law default by making every POA durable unless the document specifies otherwise. Most non-UPOAA states still require express durability language to keep the POA in effect after the principal becomes incapacitated.

Durable vs springing

Two structural choices affect when the agent's authority begins and whether it survives the principal's incapacity. A durable POA continues in force after the principal becomes incapacitated; a non-durable POA terminates by operation of law at that moment. Durability is created by statutory magic words. UPOAA § 104 calls for "this power of attorney is not affected by my subsequent incapacity" or substantially similar language. California Prob. Code § 4124 uses identical phrasing. A springing POA defers the agent's authority until a triggering event, almost always incapacity certified in writing by one or two physicians. The springing model adds a verification step at every transaction (the bank or title company wants to see the physician letters), which slows things down and gives third parties an excuse to refuse acceptance. Most estate planning attorneys recommend an immediately effective, durable POA held by counsel or a successor agent until needed, eliminating the trigger-proof problem while preserving the principal's control.

Witness and notarization rules by state

Notarization is required in nearly every state for the POA to be effective against third parties. UPOAA § 105 requires acknowledgment before a notary. California (Cal. Prob. Code § 4121), Texas (Tex. Est. Code § 751.0021), and Florida (Fla. Stat. § 709.2105) require notarization independently. Witness requirements are layered on top in several states. Florida requires two adult witnesses plus a notary for any POA. Pennsylvania requires two witnesses (20 Pa. C.S. § 5601(b)). Most healthcare POAs require two adult witnesses regardless of state, with restrictions: the witnesses generally cannot be the named agent, healthcare providers, or employees of the principal's care facility. New York's General Obligations Law § 5-1501B requires the principal's signature to be witnessed by two adults, neither of whom is the agent. Remote online notarization is permitted in 45 states under statutes adopted from 2019 to 2023, typically requiring knowledge-based identity authentication and a recorded audio-visual session retained for five to ten years.

Termination by death, revocation, and other events

A POA terminates by operation of law on the principal's death (every state, every type of POA). The agent's continued action post-death exposes the agent to personal liability. Other automatic terminations under UPOAA § 110 include: revocation by the principal in writing, termination of the agent's authority for any reason (resignation, death, removal), and dissolution of the principal's marriage if the spouse was the agent (in 28 states this is automatic, in others it requires express revocation). Court orders can terminate a POA. The court may also limit or remove the agent on petition by the principal, a relative, or any interested person if the agent has breached fiduciary duty or the principal lacked capacity at execution. Time-limited POAs terminate on the stated end date. Limited POAs terminate when the specified task completes. Knowing which terminations are automatic and which require notice prevents both inadvertent acts beyond authority and inadvertent reliance on a stale document.

Legal Authority

Authorize a trusted agent to act on your behalf in financial, legal, or medical matters

Incapacity Planning

Ensure your affairs are managed seamlessly if you become unable to act for yourself

Court Avoidance

Avoid the costly, time-consuming conservatorship or guardianship court process

Power of Attorney Form Preview

Below is a visual preview of the sections and fields included in a standard power of attorney form. This mockup illustrates the structure and level of detail our templates provide. Your completed document will be fully formatted, professionally styled, and customized for your specific POA type and state requirements.

Durable Power of Attorney

For Financial and Legal Matters

Section 1: Principal (Person Granting Authority)

Section 2: Agent (Attorney-in-Fact)

Primary Agent

Successor Agent

Section 3: Powers Granted

Section 4: Durability & Effective Date

Section 5: Limitations & Special Instructions

Section 6: Execution

Principal Signature

Notary Public

Witness 1 Signature

Witness 2 Signature

Types of Power of Attorney

There are several types of power of attorney, each designed for different situations and levels of authority. The right type depends on whether you need broad or limited authority, whether the POA should survive incapacity, and what specific matters the agent will handle. Select the type that best fits your needs to get a state-specific template with the proper legal language and provisions.

General Power of Attorney

Broad authority over financial and legal matters on behalf of the principal

Durable Power of Attorney

Remains valid even if the principal becomes incapacitated or mentally incompetent

Limited/Special Power of Attorney

Restricted to specific tasks, transactions, or a defined timeframe

Medical/Healthcare Power of Attorney

Authorizes healthcare decisions when the principal is unable to communicate

Financial Power of Attorney

Specifically for financial transactions, banking, investments, and tax matters

Springing Power of Attorney

Only activates upon a specific triggering event such as incapacitation

Minor Child Power of Attorney

Grants temporary guardianship authority over children to a designated caregiver

Real Estate Power of Attorney

Authorizes property transactions including buying, selling, and managing real estate

Vehicle Power of Attorney

Authorizes DMV transactions, vehicle registration, titling, and sales on behalf of the principal

Agent Authorization Letter

Short-form authorization letting an agent act on a principal's behalf for limited specific tasks

IRS Power Of Attorney Form 2848

IRS Form 2848 authorizing a CPA or attorney to represent you before the IRS on tax matters

Military

Military power of attorney for service members deploying or on active duty to authorize an agent

Revocation

Formally revokes a previously granted power of attorney and terminates the agent's authority

State Tax

Authorizes a representative to handle state tax matters and correspondence with state revenue agencies

Choosing the Right Power of Attorney

With nine different types of power of attorney available, selecting the right one can feel overwhelming. The decision depends on your specific situation, the scope of authority you want to grant, and when you need the POA to take effect. Use the guide below to identify which type, or combination of types, is right for you.

"I want someone to manage ALL of my financial and legal affairs."

You need a General Power of Attorney if you are competent and want immediate authority, or a Durable Power of Attorney if you want the authority to continue if you become incapacitated. For most estate planning purposes, a durable POA is the better choice because it provides protection precisely when you need it most.

"I only need someone to handle ONE specific task or transaction."

You need a Limited/Special Power of Attorney. This is ideal for situations like authorizing someone to close a real estate deal while you are out of the country, sign specific documents on your behalf, or handle a single financial transaction. The POA clearly defines the specific task and typically includes an expiration date.

Limited/Special POA"I want someone to make medical decisions if I cannot speak for myself."

You need a Medical/Healthcare Power of Attorney (also called a healthcare proxy in some states). This authorizes your agent to make medical decisions (including treatment options, surgeries, medication, and end-of-life care) when you are unable to communicate your wishes. Consider pairing this with a living will for comprehensive healthcare planning.

Medical/Healthcare POA"I only want the POA to activate if something happens to me."

You need a Springing Power of Attorney. Unlike an immediately effective POA, a springing POA lies dormant until a specified triggering event, typically the principal's incapacitation as certified by one or two physicians. Note that some states have limited or eliminated springing POAs, and third parties may be reluctant to accept them due to uncertainty about when the trigger occurred.

Springing POA"I need someone to care for my children while I am away."

You need a Minor Child Power of Attorney. This grants temporary guardianship authority to a designated caregiver, allowing them to make educational, medical, and daily care decisions for your children. It is commonly used for military deployment, extended travel, medical treatment, or temporary caregiving arrangements.

Minor Child POA"I need someone to handle a property transaction or DMV paperwork."

You need a Real Estate Power of Attorney for property transactions (buying, selling, refinancing, or managing real estate) or a Vehicle Power of Attorney for DMV transactions (title transfers, registration, or selling a vehicle on your behalf). These specialized POAs include the specific language required by recording offices and motor vehicle departments.

Tip: Many people create multiple POAs. For example, a durable financial POA and a separate medical POA, each with a different agent. This allows you to choose the best person for each role and prevents any single person from having authority over both your finances and your healthcare.

POA vs Other Documents

A power of attorney is often confused with other legal documents that deal with incapacity planning, healthcare decisions, and estate management. Understanding the differences is critical for choosing the right document, or combination of documents, for your situation.

Power of Attorney vs Guardianship/Conservatorship

Power of Attorney

- - Created voluntarily by the principal

- - Principal chooses their own agent

- - No court involvement or oversight required

- - Inexpensive to create (under $100)

- - Private document, not part of public record

- - Terminates upon death of principal

Guardianship/Conservatorship

- - Imposed by a court when person is incapacitated

- - Court selects the guardian/conservator

- - Requires court petition, hearing, and ongoing oversight

- - Expensive ($3,000-$10,000+ in legal fees)

- - Public court proceeding, part of public record

- - May be temporary or permanent

Key takeaway: A durable power of attorney is one of the most effective ways to avoid guardianship or conservatorship. By designating your agent in advance, you eliminate the need for your family to go through a costly, time-consuming, and public court process if you become incapacitated.

Power of Attorney vs Living Will / Advance Directive

Healthcare Power of Attorney

- - Appoints a person to make medical decisions

- - Agent uses judgment based on your preferences

- - Covers all medical decisions, not just end-of-life

- - Flexible: agent can respond to unforeseen situations

- - Requires a willing, available agent

Living Will / Advance Directive

- - Directly states your treatment preferences

- - No agent needed; the document speaks for you

- - Typically limited to end-of-life situations

- - Less flexible; cannot address every scenario

- - Provides clear guidance for specific situations

Best practice:Estate planning attorneys recommend having both a healthcare POA and a living will. The healthcare POA handles day-to-day medical decisions, while the living will provides specific direction for end-of-life care. Some states offer a combined "advance directive" form that includes both.

Power of Attorney vs Healthcare Proxy

Medical Power of Attorney

- - Term used in most states

- - Grants broad healthcare decision-making authority

- - May include specific powers and limitations

- - Often part of a broader POA document

Healthcare Proxy

- - Term used in certain states (NY, MA, etc.)

- - Functionally identical to medical POA

- - May be a state-specific statutory form

- - Usually a standalone healthcare document

In practice:These documents serve the same purpose: appointing someone to make healthcare decisions on your behalf. The name varies by state. In Massachusetts and New York, the document is called a "healthcare proxy." In most other states, it is called a "medical power of attorney" or "healthcare power of attorney." Our templates use the correct terminology for your state.

Power of Attorney vs Trust

Power of Attorney

- - Agent acts on behalf of the principal

- - Covers assets in the principal's name

- - Terminates upon principal's death

- - Does not avoid probate

- - Simpler and less expensive to create

Revocable Living Trust

- - Trustee manages assets held in the trust

- - Only covers assets transferred into the trust

- - Continues after the grantor's death

- - Avoids probate for trust assets

- - More complex and expensive to establish

When to use both:A trust and a POA serve complementary roles. The trust manages assets that have been transferred into it, while the POA handles assets and matters that remain in the principal's individual name. Most comprehensive estate plans include both a revocable living trust and a durable power of attorney to ensure complete coverage.

How to Create a Power of Attorney: A 10-Step Guide

A POA has ten working parts, in order: type, agent, scope, durability, limitations, compensation, HIPAA authorization (if healthcare), execution formalities, distribution, and a calendar for review. The order matters because each step constrains the next. The type drives which statutory form applies. The agent choice determines what limitations are appropriate. The scope determines whether HIPAA is needed. Execution formalities differ by state in ways that can void the document if missed. A POA that fails any step is worse than no POA at all because the family relies on it until it is rejected, then has to seek court appointment of a conservator from a starting position of urgency.

Two drafting choices carry the most weight. The durability decision determines whether the POA survives incapacity, which is the entire point of estate planning use. Without durability language tracking the state's statutory wording (UPOAA § 104, Cal. Prob. Code § 4124, Tex. Est. Code § 751.0021, etc.), the agency relationship terminates by operation of law at the moment the principal needs it most. The hot-powers decision determines whether the agent can make gifts, change beneficiary designations, create or amend trusts, or delegate authority. Under UPOAA § 201, these powers are not granted by a general grant of authority; they must be expressly enumerated. Twenty-eight states follow that rule. Texas Est. Code § 751.031 requires initial-by-initial authorization for hot powers on the statutory form. Treat a general grant of authority as silence on hot powers.

Capacity at the time of execution must be confirmed. The standard for testamentary capacity (used for POAs in most jurisdictions) requires that the principal understand what a POA is, what authority they are granting, who the agent is, and that the document can be revoked. A physician's contemporaneous capacity assessment is the cheapest insurance against later challenges and costs $200 to $500 in most markets. For elderly principals or principals with diagnosed cognitive issues, document capacity in the medical record before execution.

Determine the Type of POA You Need

Start by identifying why you need a power of attorney and what authority you want to grant. Do you need someone to manage all of your financial affairs (general or durable POA), handle a specific transaction (limited POA), make medical decisions (healthcare POA), or care for your children (minor child POA)? Your answer determines which type of POA is appropriate.

Consider whether you want the POA to take effect immediately or only upon a triggering event (springing POA). For estate planning purposes, most attorneys recommend a durable POA that takes effect immediately, because springing POAs can create complications when the agent needs to prove the triggering event has occurred. If you are uncomfortable with your agent having immediate authority, you can sign the POA and have your attorney hold it in escrow until it is needed.

Choose Your Agent Carefully

Your agent will have significant authority over your affairs, so choose someone you trust completely. The ideal agent is trustworthy, financially responsible, organized, available when needed, and willing to serve. Most people choose a spouse, adult child, sibling, or close friend. You may also appoint a professional fiduciary, such as an attorney or financial institution, particularly for complex financial matters.

Always name at least one successor agent who can step in if your primary agent is unable or unwilling to serve. Consider whether you want co-agents who must act jointly (providing checks and balances but potentially slowing decision-making) or agents who can act independently (more convenient but less oversight). Discuss your expectations with your chosen agent before finalizing the document.

Tip: Your agent does not have to live in the same state as you, but geographic proximity can make it easier for them to handle in-person tasks like banking, real estate transactions, and medical advocacy.

Define the Scope of Authority

Specify exactly what powers you are granting to your agent. A general or durable POA typically grants broad authority over financial matters including banking, real estate, investments, taxes, insurance, government benefits, and legal proceedings. A limited POA restricts authority to specific tasks or transactions. Be as specific as possible to prevent both overreach and gaps in authority.

Consider whether to grant your agent the power to make gifts (important for tax planning but susceptible to abuse), change beneficiary designations, create or amend trusts, or delegate authority to others. These "hot powers" carry additional risk and are subject to stricter scrutiny in many states. If you do not explicitly grant a power, most states presume the agent does not have it.

Include Durability Language

If you want the POA to remain effective if you become incapacitated, you must include specific durability language. The exact wording varies by state, but it generally states: "This power of attorney shall not be affected by my subsequent disability or incapacity" or "This power of attorney shall become effective upon my disability or incapacity." Without this language, the POA automatically terminates if you become incapacitated, which is often precisely when you need it most.

Warning: A POA without durability language is virtually useless for estate planning and incapacity planning. If you become incapacitated and your POA is not durable, your family will need to seek a court-appointed conservator or guardian, the exact situation the POA was supposed to prevent.

Set Limitations and Special Instructions

Even with a broad power of attorney, you can include specific limitations on the agent's authority. Common limitations include caps on gift-giving amounts, restrictions on self-dealing (the agent cannot benefit themselves), prohibitions on changing beneficiary designations, and requirements for the agent to obtain a second opinion before making major financial decisions.

You can also include special instructions such as requiring the agent to maintain detailed records, provide periodic accountings to a trusted third party, follow specific investment strategies, or consult with particular advisors before making significant decisions. These instructions provide guardrails that protect you while still giving your agent the flexibility to act on your behalf.

Address Agent Compensation and Expenses

Specify whether your agent will be compensated for their services and how expenses will be handled. Many family members serve as agents without compensation, but the agent should be entitled to reimbursement for reasonable out-of-pocket expenses incurred in carrying out their duties. If you are appointing a professional fiduciary, specify the compensation rate or formula (such as a percentage of assets managed or an hourly rate) to avoid disputes.

Include HIPAA Authorization (Healthcare POA)

If you are creating a healthcare or medical power of attorney, include a HIPAA authorization that allows your agent to access your protected health information. Without this authorization, healthcare providers may be legally prohibited from sharing your medical records with your agent under the Health Insurance Portability and Accountability Act (HIPAA). The authorization should name your agent specifically and describe the scope of health information they may access.

Consider also including a HIPAA authorization in your financial POA, as your agent may need to access medical information to manage health insurance claims, apply for disability benefits, or evaluate long-term care options.

Execute the Document Properly

Proper execution is critical. A POA that is not properly signed, notarized, or witnessed according to your state's laws may be rejected by the institutions you need it to work with. Most states require the principal to sign the POA in the presence of a notary public. Many states also require one or two witnesses who are not named as agents in the document. Some states have specific statutory forms that must be used.

The principal must be mentally competent at the time of signing. They must understand what a POA is, what powers they are granting, and the consequences of granting those powers. If there is any question about the principal's competency, consider having a physician provide a capacity assessment before execution.

Best practice: Have the agent sign an acknowledgment of their fiduciary duties on the POA itself. This is required in some states and serves as evidence that the agent understands their obligations.

Distribute Copies to Relevant Parties

Once the POA is properly executed, provide certified copies to your agent, successor agent, and any institutions where the agent may need to act on your behalf, including banks, investment firms, insurance companies, and (for real estate POAs) the county recorder's office where property is located. Many financial institutions prefer to have a copy on file in advance so they can review it before the agent needs to use it.

Keep the original in a secure but accessible location, such as a fireproof safe at home, and tell your agent and successor agent where it is stored. Do not put the only copy in a safe deposit box that only you can access, as your agent may need the document precisely when you cannot open the box.

Review and Update Regularly

A power of attorney should be reviewed and potentially updated every 3 to 5 years, or whenever there is a significant life event such as a marriage, divorce, death of the agent, move to a new state, major change in financial circumstances, or change in your relationship with the agent. Some financial institutions are more likely to accept a recently executed POA, as they may be concerned about the validity of a document that is many years old.

If you move to a new state, have your POA reviewed to ensure it complies with the new state's laws. While most states will honor a POA validly executed in another state, having a POA that conforms to your current state's statutory form will minimize the risk of rejection by local institutions.

Key Components of a Power of Attorney

A comprehensive power of attorney addresses every aspect of the agent's authority and the principal's wishes. Missing critical components can render the document unenforceable, create gaps in authority, or leave the principal vulnerable to abuse. The table below outlines the essential elements every power of attorney should include.

| Component | Description |

|---|---|

| Principal Identification | Full legal name, date of birth, address, and Social Security number (last 4) of the person granting authority |

| Agent Designation | Full legal name, address, and contact information of the primary agent (attorney-in-fact) |

| Successor Agent | Alternate agent who steps in if the primary agent is unable or unwilling to serve |

| Grant of Authority | Specific powers granted to the agent: financial, legal, healthcare, real estate, business, or personal |

| Durability Clause | Language specifying whether the POA survives the principal's incapacity (durable vs non-durable) |

| Effective Date | When the POA takes effect: immediately upon execution or upon a triggering event (springing) |

| Expiration / Termination | Conditions under which the POA terminates: specific date, completion of task, revocation, or death |

| Limitations on Authority | Specific restrictions on the agent's powers: gift-giving limits, self-dealing prohibitions, excluded actions |

| Special Instructions | Specific directions to the agent regarding record-keeping, reporting, investment preferences, or care wishes |

| Fiduciary Duties | Statement of the agent's legal obligations: duty of loyalty, care, accounting, and good faith |

| Agent Compensation | Whether the agent is entitled to compensation and/or reimbursement for reasonable expenses |

| Co-Agent Provisions | If multiple agents, whether they act jointly (together), severally (independently), or jointly and severally |

| Third-Party Reliance | Language protecting third parties who rely on the POA in good faith from liability |

| Revocation Clause | Statement that the principal may revoke the POA at any time by written notice to the agent |

| HIPAA Authorization | For healthcare POAs, authorization for the agent to access the principal's protected health information |

| Governing Law | The state whose laws govern the interpretation and enforcement of the POA |

| Execution / Signatures | Principal's signature, notarization, witness signatures, and agent acknowledgment as required by state law |

Powers You Can Grant Under a Power of Attorney

A power of attorney can authorize your agent to handle a wide range of matters on your behalf. The specific powers you include depend on the type of POA and your individual needs. Below are the major categories of powers that can be granted, along with examples of what each includes.

Financial Powers

- - Banking transactions (deposits, withdrawals, transfers)

- - Bill payment and debt management

- - Investment and retirement account management

- - Tax return preparation and filing

- - Insurance claims and policy management

- - Government benefit applications (Social Security, VA)

- - Safe deposit box access

Healthcare Powers

- - Consent to or refuse medical treatment

- - Choose doctors and healthcare facilities

- - Access medical records (HIPAA authorization)

- - Make end-of-life care decisions

- - Authorize surgeries and procedures

- - Arrange long-term care and assisted living

- - Manage organ donation and autopsy decisions

Real Estate Powers

- - Buy, sell, or lease real property

- - Refinance or obtain mortgages

- - Manage rental properties and collect rent

- - Negotiate and execute real estate contracts

- - Handle property tax payments and appeals

- - Authorize repairs and improvements

- - Grant easements and resolve boundary disputes

Business Powers

- - Operate and manage business entities

- - Sign contracts and agreements on behalf of business

- - Hire and terminate employees

- - Make business banking transactions

- - Buy, sell, or pledge business assets

- - File business tax returns

- - Participate in partnership or LLC decisions

Legal Powers

- - Initiate or defend legal proceedings

- - Hire attorneys and legal counsel

- - Settle claims and disputes

- - Sign legal documents and contracts

- - Handle arbitration and mediation

- - Manage legal correspondence

- - File court documents on principal's behalf

Personal Care Powers

- - Determine living arrangements

- - Arrange transportation and travel

- - Manage household staff and services

- - Handle mail and personal correspondence

- - Make decisions about social activities

- - Manage personal property and belongings

- - Arrange caregiving and support services

Digital Asset Powers

An increasingly important category of powers relates to digital assets. Many states now allow POAs to address digital property under the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA). Digital asset powers may include:

- - Access to email accounts and social media

- - Management of cryptocurrency and digital wallets

- - Online banking and payment platforms

- - Cloud storage and digital files

- - Domain names and websites

- - Digital subscriptions and memberships

- - Online business accounts and marketplaces

- - Intellectual property held digitally

Revoking a Power of Attorney

A competent principal can revoke a POA at any time. The revocation right cannot be waived in the document; any clause purporting to make a POA irrevocable is void as against public policy in every state. Capacity at the time of revocation is required and is judged at the moment of revocation, not at execution. A principal who has lost testamentary capacity cannot revoke; the family must seek court-appointed conservatorship to remove the agent. Five steps make revocation effective in practice.

First, prepare a written revocation that identifies the original POA by date and the agent's name, states the principal's intent to revoke all authority, and is signed and dated by the principal. Second, notarize the revocation; in every state that required notarization for execution, notarization is required for revocation. Third, deliver actual notice to the agent and any successor agents by certified mail with return receipt or by personal service; UPOAA § 110(c) shields an agent who acts without actual knowledge of revocation, so the proof of delivery is what cuts off the agent's authority. Fourth, send copies to every third party that holds the POA: banks, brokerages, insurance companies, healthcare providers, the IRS (if Form 2848 was filed), the Social Security Administration, and the VA. Fifth, if the POA was recorded for real estate purposes (most states permit recording, several require it for real estate POAs), record the revocation with the same county recorder's office. Destroying the original alone does not work because outstanding copies remain operative until each holder receives notice.

Revocation procedure under UPOAA § 110

Under UPOAA § 110, the principal can revoke by signed writing or by physical destruction of the original with intent to revoke. The simpler practice is the signed writing because it provides documentary evidence the principal can mail to third parties. Section 110(c) shields the agent from liability for acts taken in good faith without actual knowledge of revocation, which makes prompt notice critical. A revocation that revokes only the agent's authority but preserves a successor agent's authority is permitted; a revocation that revokes all authority terminates the document entirely. Spouse-agent terminations occur automatically on dissolution of marriage in 28 states under UPOAA § 110(b)(3); in non-UPOAA states, divorce does not automatically terminate the POA and an express revocation is required (a common oversight in divorce practice).

How to Revoke a Power of Attorney

Create a Written Revocation

Draft a written document clearly stating that you revoke the power of attorney, identifying the original POA by date and the name of the agent. Sign and date the revocation, and have it notarized (required in some states, recommended in all).

Notify the Agent

Deliver a copy of the revocation to the agent and any successor agents in writing. Send via certified mail with return receipt requested to create proof of delivery.

Notify Third Parties

Send copies of the revocation to all institutions and individuals that received copies of the original POA, including banks, financial institutions, healthcare providers, insurance companies, and the IRS if the agent filed taxes on your behalf.

Record the Revocation (if applicable)

If the original POA was recorded with a county recorder's office (common for real estate POAs), record the revocation with the same office to put the public on notice that the POA is no longer valid.

Retrieve and Destroy Copies

Request the return of all copies of the original POA from the agent and third parties. While you cannot guarantee all copies are recovered, the written revocation and notice supersede any outstanding copies.

When a POA Automatically Terminates

Death of the Principal

All POAs terminate immediately when the principal dies, regardless of type

Incapacity (Non-Durable POA)

A non-durable POA terminates if the principal becomes incapacitated

Expiration Date

If the POA includes an expiration date, it terminates on that date

Task Completion (Limited POA)

A limited POA terminates when the specified task or transaction is completed

Court Order

A court may revoke a POA if the agent is acting improperly or the POA was obtained through fraud

Divorce (Spousal Agent)

In many states, divorce automatically revokes a POA if the spouse was named as agent

Legal Requirements for Powers of Attorney

POAs are creatures of state law. The requirements for valid execution, the default rules for agent authority, and the mechanisms for third-party acceptance vary in ways that determine whether the document works in practice. Three sources of authority operate simultaneously: state POA statutes (most based on the UPOAA), state-specific durability and witness rules, and federal overlays for healthcare (HIPAA), Social Security (SSA-1696 for representative payees), Veterans benefits (VA Form 21-22), and tax matters (IRS Form 2848). A POA that satisfies state law is still rejected by the IRS unless Form 2848 is filed because federal agencies require their own forms.

The Uniform Power of Attorney Act of 2006 has been adopted in 28 states. UPOAA reverses the historical default by treating every POA as durable unless the document specifies otherwise (§ 104), reverses the gift-giving default by requiring express enumeration of hot powers (§ 201), imposes mandatory acceptance with statutory penalties for unreasonable refusal (§ 120), and codifies the agent's fiduciary duties (§ 114). The 22 non-UPOAA states keep some or all of the historical defaults, which makes drafting in those states more deliberate. A general grant of authority means more in California or New York than it does in a UPOAA state, and the same general grant means very little in either jurisdiction for hot powers.

Uniform Power of Attorney Act (UPOAA)

Drafted by the Uniform Law Commission in 2006 and adopted in 28 states as of 2025. The UPOAA codifies durable-by-default treatment (§ 104), enumerates hot powers requiring express grant (§ 201, covering gifts, beneficiary changes, trust creation and amendment, rights of survivorship, delegation, and disclaimers), imposes acceptance obligations on third parties with seven business days to accept or reject and statutory damages for unreasonable refusal (§ 120), defines the agent's fiduciary duties (§ 114, including loyalty, care, accounting, and cooperation with healthcare agents), and creates a statutory short form (§ 301) that satisfies execution requirements when used.

Notarization requirements

Notarization is required by 49 states for the POA to be effective against third parties; only Utah permits a non-notarized POA in limited circumstances. UPOAA § 105 requires the principal's signature to be acknowledged before a notary or other authorized officer. State-specific statutes follow the same rule: California Prob. Code § 4121 (signature in the presence of a notary or two adult witnesses), Texas Est. Code § 751.0021 (notarization required), Florida Stat. § 709.2105 (notarization plus two witnesses), New York Gen. Oblig. Law § 5-1501B (notarization plus two witnesses). Remote online notarization is permitted in 45 states under post-2019 statutes (Virginia was first in 2011, with most states following 2019 to 2023). RON statutes typically require knowledge-based authentication using public records, credential analysis of a government ID, audio-visual recording retained for five to ten years, and use of an approved RON platform.

Witness requirements by state

Twenty-three states require witnesses in addition to notarization for a financial POA. Florida and South Carolina require two adult witnesses. Pennsylvania requires two witnesses (20 Pa. C.S. § 5601(b)). Vermont requires one witness. California permits either notarization or two witnesses (Cal. Prob. Code § 4121). New York requires two witnesses plus notarization. The remaining 27 states accept notarization alone. Healthcare POAs almost always require two adult witnesses regardless of the financial-POA rule, with restrictions: the witnesses generally cannot be the named agent, blood relatives or heirs of the principal, healthcare providers treating the principal, or owners or employees of the principal's care facility. Texas Health and Safety Code § 166.154 lists these disqualifications explicitly. Disqualified-witness signatures void the POA, not just the signature, in most jurisdictions.

Recording for Real Estate POAs

If a power of attorney will be used for real estate transactions, many states require or recommend that the POA be recorded with the county recorder's office in the county where the property is located. Recording puts the public on notice that the agent has authority to act on behalf of the principal in property matters. Title companies and closing agents will typically require a recorded POA before allowing the agent to sign real estate documents. The POA must usually be notarized before it can be recorded, and some states have specific formatting requirements (margins, font size, etc.) for recorded documents.

State-Specific Variations

- Statutory Forms: Some states (including California, New York, Illinois, and Texas) have specific statutory POA forms. While not always mandatory, using the statutory form increases the likelihood that third parties will accept the POA without question. Our templates conform to state statutory forms where they exist.

- Agent Acknowledgment: Several states (including Colorado, Idaho, and Maine under the UPOAA) require the agent to sign an acknowledgment of their fiduciary duties before exercising authority. This serves as evidence that the agent understands their legal obligations to the principal.

- Third-Party Acceptance: Many states have enacted laws requiring banks and financial institutions to accept validly executed POAs and imposing liability for unreasonable refusal. The UPOAA includes provisions giving third parties a reasonable time (typically 7 business days) to accept or reject a POA, and requiring them to provide written reasons for any rejection.

- Springing POA Restrictions: Some states have limited or eliminated springing powers of attorney due to the practical difficulties of determining when the triggering event has occurred. In these states, the POA must take effect immediately upon execution.

- Gift-Giving Authority: Under the UPOAA and in many states, the authority to make gifts must be specifically and expressly granted in the POA. It is not included in a general grant of authority. This is an important safeguard against financial abuse. Annual gift-giving authority is often limited to the IRS annual gift tax exclusion amount ($18,000 per recipient in 2024, $19,000 in 2025).

Power of Attorney by State

Each state has different requirements for powers of attorney, including notarization rules, witness requirements, statutory form preferences, agent acknowledgment requirements, and acceptance obligations for financial institutions. Select your state below for a POA form customized to your jurisdiction's specific laws.

Sample Power of Attorney

Below is a condensed preview of our durable power of attorney template. This sample shows the structure, language, and sections included in our attorney-reviewed documents. Your completed POA will be fully customized for your specific type, state, powers granted, and agent designations.

DURABLE POWER OF ATTORNEY

For Financial and Legal Matters

I, [Principal Full Legal Name], of [Address, City, State, ZIP], born on [Date of Birth], do hereby appoint:

PRIMARY AGENT:

Name: [Agent Full Legal Name]

Address: [Agent Mailing Address]

Relationship: [Relationship]Phone: [Phone]

SUCCESSOR AGENT:

Name: [Successor Agent Name]

Address: [Successor Agent Address]

Relationship: [Relationship]Phone: [Phone]

1. GRANT OF AUTHORITY

I grant my Agent full power and authority to act on my behalf in all financial and legal matters, including but not limited to the following:

- Banking and financial transactions

- Real estate transactions (buy, sell, lease, mortgage, manage)

- Investment and retirement account management

- Tax return preparation and filing with the IRS and state agencies

- Insurance claims and policy management

- Government benefits and entitlements

- Business operations and management

- Legal proceedings and claims

2. DURABILITY

This Power of Attorney shall not be affected by my subsequent disability or incapacity. This Power of Attorney shall remain in full force and effect unless and until I revoke it in writing, or until my death.

3. EFFECTIVE DATE

This Power of Attorney shall take effect immediately upon my execution of this document and shall remain in effect until revoked by me in writing, or until my death.

4. LIMITATIONS

My Agent shall NOT have the authority to: (a) make gifts of my property exceeding $[Amount]per recipient per calendar year; (b) change beneficiary designations on life insurance policies or retirement accounts; (c) create, amend, or revoke my will or trust; (d) exercise any powers I may hold as trustee of another person's trust...

5. AGENT'S DUTIES

My Agent accepts this appointment and agrees to act in my best interest, to avoid conflicts of interest, to keep my property separate from the Agent's property, to maintain complete records of all transactions conducted on my behalf, and to exercise the powers granted herein with the care, competence, and diligence of a prudent person dealing with the property of another...

6. COMPENSATION

My Agent shall be entitled to reimbursement for all reasonable expenses incurred in connection with performing duties under this Power of Attorney. My Agent[shall/shall not]be entitled to reasonable compensation for services rendered.

7. THIRD-PARTY RELIANCE

Any third party who receives a copy of this Power of Attorney may rely upon it and act in accordance with its terms. Any third party may rely upon the representations of my Agent regarding all matters relating to any power granted to my Agent...

8. REVOCATION

I reserve the right to revoke this Power of Attorney at any time by delivering a written notice of revocation to my Agent and to any third parties who have received copies of this document. Revocation shall be effective upon receipt of written notice...

Frequently Asked Questions

Find answers to common questions about powers of attorney, agent duties, execution requirements, and how POAs work in practice.

Official Resources

For additional information on power of attorney requirements, elder law, estate planning, and agent responsibilities, consult these official and reputable resources.

AARP - Power of Attorney Guide

Comprehensive guide to understanding and creating a power of attorney

ABA - Power of Attorney Resources

American Bar Association resources on POA law and elder law issues

ULC - Uniform Power of Attorney Act

Uniform Law Commission information on the UPOAA and state adoption status

NAELA - Elder Law Attorneys

National Academy of Elder Law Attorneys: find an elder law attorney near you

CFPB - Managing Someone Else's Money

Consumer Financial Protection Bureau guides for agents and fiduciaries

NIA - Advance Care Planning

National Institute on Aging guide to healthcare POA and advance directives

Nolo - POA Legal Encyclopedia

Free legal information on all types of power of attorney

HHS - HIPAA for Individuals

U.S. Department of Health and Human Services HIPAA authorization guidance

Create your Power of Attorney in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.