What Is a Real Estate Power of Attorney?

A real estate power of attorney is a specialized form of limited POA that authorizes one person — the agent or attorney-in-fact — to act on the principal's behalf in a specific real estate transaction or series of transactions. The authority is usually narrowly scoped to one property, identified by legal description, and to a particular type of transaction: sale, purchase, refinance, lease, or management. The document is designed to satisfy the specific requirements of title insurers, lenders (including Fannie Mae, Freddie Mac, FHA, and VA), and county recorders — all of whom have strict and sometimes idiosyncratic rules about what a POA must say before they will accept it at closing.

The real estate POA exists because real estate transactions are unlike most other legal matters. Every closing creates a chain of title that will be examined by future title companies and purchasers, and every deed becomes part of a public record. If the agent's authority is unclear, the title becomes defective, and any future sale of the property can be delayed or derailed. To prevent these problems, title insurers developed a practice of requiring real estate POAs to be drafted with surgical precision, recorded in the county land records, and, in many cases, signed fresh for each transaction. Our templates incorporate decades of title-industry best practice so the document will survive title examination.

The most common use of a real estate POA is absence at closing: a buyer or seller who cannot physically attend the closing because they are out of state, overseas, deployed, hospitalized, or otherwise unavailable, authorizes a trusted person — often a spouse, relative, real estate attorney, or closing agent — to sign the deed, mortgage, and settlement paperwork on their behalf. A less common but important use is property management, where an out-of-town owner authorizes a local agent to lease, collect rent, and handle repairs on rental property.

Real estate POAs are recorded in the county recorder's or register of deeds' office where the property sits. Recording creates constructive notice to the world that the agent had authority, which is essential for the title insurer underwriting the transaction. Each county has its own recording formalities — margin sizes, cover page requirements, return-to addresses, recording fees — that our templates comply with automatically.

Even after the transaction closes, a well-drafted real estate POA either terminates automatically by its own terms or is revoked and the revocation recorded in the same county. This keeps the chain of title clean and forecloses any possibility that the document could be misused in a future transaction. Careful real estate attorneys treat recording and revocation as standard closing practice.

Transaction-Specific

Narrowly scoped to one property and one transaction.

Recorded in County Records

Becomes part of the public chain of title.

Lender-Compliant

Satisfies FNMA, Freddie Mac, FHA, and VA requirements.

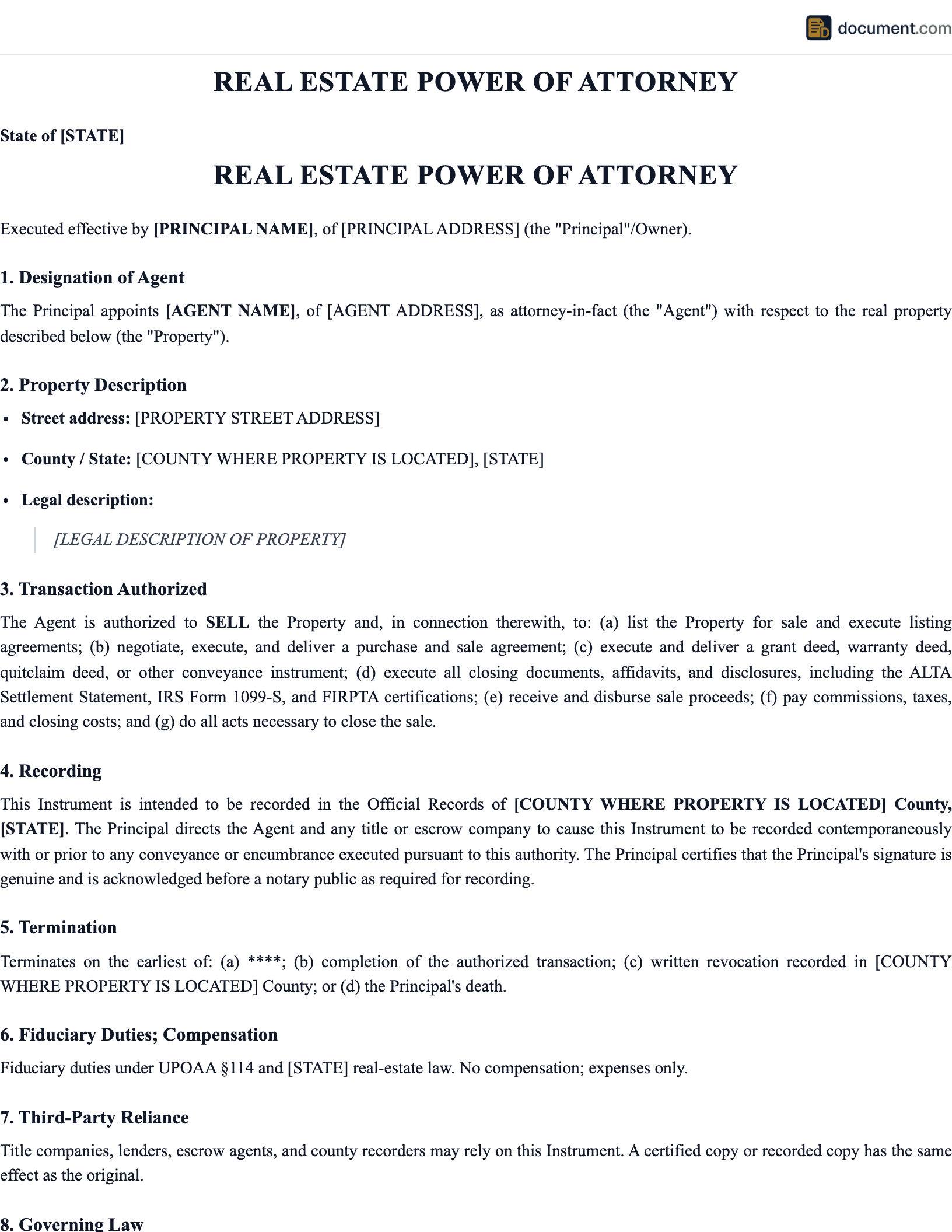

Real Estate POA Form Preview

Below is a structural preview of our real estate POA template. Notice the detailed property description, transaction identification, and recording formalities.

Real Estate Power of Attorney

Property Transaction Authorization

1. Principal

2. Agent (Attorney-in-Fact)

3. Property

4. Transaction Authorized

5. Specific Authority

- Execute deed, settlement statement, and closing documents

- Negotiate minor adjustments within $5,000 of purchase price

- Sign lender disclosures and required affidavits

- Endorse proceeds checks for direct deposit to Principal's account

- Take any other action reasonably necessary to complete closing

6. Recording & Execution

Principal Signature

Notary & Recording Stamp

Common Uses for a Real Estate POA

Real estate POAs solve a narrow but important set of problems centered on transactions that cannot wait for the principal to be physically present.

Out-of-State Closings

A seller who relocated before listing, or a buyer purchasing a vacation home from across the country, authorizes a local agent to attend and sign at closing.

Refinance Signings

A homeowner deployed overseas or hospitalized authorizes a spouse to sign the refinance documents to secure lower rates before closing.

Estate Administration

An elderly or incapacitated property owner authorizes an adult child to sell a long-held family home as part of downsizing or estate planning.

Property Management

An out-of-state landlord authorizes a local property manager to lease, collect rent, and handle repairs for rental property.

Commercial Transactions

A business owner authorizes a commercial real estate attorney to close a commercial lease or purchase while the owner attends to other business matters.

Military Deployment

A servicemember closing on a home before or during deployment relies on a spouse or family member to sign at closing and handle follow-up paperwork.

Real Estate POA vs Other Documents

Real estate POAs are closely related to other delegation documents, but the differences matter when title insurance and lender acceptance are on the line.

Real Estate POA vs Limited POA

Real Estate POA

- - Specialized for property transactions

- - Includes legal description & parcel ID

- - Complies with recording formalities

- - Designed to satisfy lenders and title

Generic Limited POA

- - Generic single-purpose delegation

- - May lack real estate-specific language

- - Often rejected at closing

- - Best for non-real-estate tasks

Real Estate POA vs General POA

Real Estate POA

- - Transaction-specific and narrow

- - Higher acceptance at closings

- - Easier for title underwriting

General POA

- - Broad ongoing authority

- - Title companies may demand specific language

- - Useful when agent manages multiple assets

How to Create a Real Estate POA

Real estate POAs reward preparation. The more precisely the document is drafted and the more closely it aligns with lender and title requirements, the less friction you will face at closing.

Identify the Property Precisely

Gather the full street address, city, county, parcel ID, and the legal description exactly as it appears on the current deed. The legal description is the most important piece — without it, title companies will reject the POA.

Identify the Transaction

Specify whether the agent is authorized to sell, purchase, refinance, lease, or manage. For purchases and refinances, include the expected closing date, loan amount, and lender name. For sales, include the buyer's name and purchase price.

Choose Your Agent

Pick a spouse, adult child, real estate attorney, or closing agent who will be physically present at closing and can handle the paperwork. Notify the title company and lender of the agent's identity before closing.

Confirm Lender Acceptance Early

Ask the lender whether they will accept a POA, what specific language they require, and whether the POA must be dated before or after the loan application. FHA, VA, and conventional loans all have different rules.

Include Specific Authority Language

List exactly what the agent may do: sign the deed, execute the settlement statement, sign mortgage documents, endorse proceeds checks, negotiate minor adjustments within a specified dollar range. Vague language risks rejection.

Use the Right Execution Formalities

Every state requires notarization for a real estate POA, and most require that the notarization use acknowledgment language suitable for recording. Some states also require witnesses. Sign in the presence of the notary.

Record the POA in the Property's County

File the original notarized POA with the county recorder or register of deeds where the property sits. Recording creates constructive notice and satisfies title underwriting.

Deliver the Original to the Closing Agent

The closing agent or title company needs the original recorded POA (or a certified copy) at the closing table. A copy from email is rarely sufficient.

Revoke After the Transaction Closes

Sign a written revocation and record it in the same county to remove the POA from the chain of title. This is standard best practice for careful real estate attorneys.

Key Components of a Real Estate POA

Every effective real estate POA contains the following elements. Missing any of them creates risk of rejection at closing.

Principal Identification

Full legal name and current mailing address of the property owner.

Agent Identification

Full legal name, address, and relationship of the attorney-in-fact.

Property Description

Street address, parcel ID, and full legal description as recorded.

Transaction Type

Sale, purchase, refinance, lease, or management.

Specific Authority

Exact actions the agent may take at closing.

Lender-Compliant Language

FNMA, Freddie Mac, FHA, or VA-required provisions.

Notarization & Recording

Acknowledgment language and county recording formalities.

Expiration or Termination

Transaction completion or specific calendar date.

Recording & Lender Rules

Real estate POAs sit at the intersection of state recording law, federal mortgage underwriting rules, and title insurance underwriting. Each layer has independent requirements, and all must be satisfied for the POA to be usable at closing.

State recording lawdictates the formalities required to record a document in county land records: margin size (typically 3 inches at top, 1 inch elsewhere), return-to address, document title, notary acknowledgment form, and recording fees. Our templates apply the formalities required in the property's county.

Lender rulesvary by loan type. Fannie Mae's Selling Guide B8-5-05 allows POAs for purchase and limited cash-out refinance transactions with specific restrictions. Freddie Mac's Seller/Servicer Guide has similar rules. FHA (HUD Handbook 4000.1) imposes additional restrictions, especially for cash-out refinances and reverse mortgages. VA loans (Pamphlet 26-7) allow POAs with specific veteran-acknowledgment language. Cash transactions have no lender rules but still must satisfy the title insurer.

Title insurancerequirements depend on the underwriter. All major title insurers require the original (or certified) POA, proof of recording, and sometimes an agent's affidavit confirming the POA is still in effect. Some underwriters require the POA to be dated within a specific window before the closing date.

Because these rules change periodically, always confirm current requirements with the lender and title company well before the closing date. Our templates include the most commonly accepted language, but no template can replace a direct conversation with the institutions involved in your specific transaction.

Real Estate POA Requirements by State

Each state has its own recording formalities, acknowledgment language, and witness requirements for real estate POAs. The list below shows the 50 states for which our templates apply state-specific rules.

Sample Real Estate POA

Below is a condensed preview of our real estate POA template drafted for a residential sale.

REAL ESTATE POWER OF ATTORNEY

Property Transaction Authorization

I, [Principal], owner of the real property described below, do hereby appoint[Agent] as my Attorney-in-Fact for the limited purpose of completing the transaction identified herein.

1. PROPERTY

Street Address: [Street, City, State ZIP]

Parcel ID: [Parcel ID]

Legal Description: [Legal Description]

2. TRANSACTION

Transaction Type: [Sale]

Purchase Price: $[Amount]

Buyer: [Buyer Name]

Expected Closing Date: [Date]

3. AUTHORITY GRANTED

My Agent is authorized to execute the deed conveying the Property to the Buyer, to sign the settlement statement and any closing disclosures, to execute all documents required by the lender and title company, to endorse any checks or drafts payable to me for the proceeds of sale, and to take any other action reasonably necessary to complete the Transaction.

4. TERMINATION

This Power of Attorney terminates upon the earlier of: (a) completion of the Transaction; or (b) [Expiration Date].

5. RECORDING

This instrument is intended to be recorded in the land records of[County] County,[State].

Frequently Asked Questions

Common questions about real estate powers of attorney, closings, recording, lender acceptance, title insurance, and multi-state property.

Official Resources

Authoritative resources on real estate POAs, mortgage underwriting, recording, and title insurance.

Fannie Mae Selling Guide

Section B8-5-05 covers POAs in purchase and refinance transactions.

Freddie Mac Seller/Servicer Guide

Freddie Mac requirements for attorney-in-fact signings.

HUD Handbook 4000.1 (FHA)

FHA Single Family Housing Policy Handbook — POA provisions.

VA Lender Handbook (Pamphlet 26-7)

VA loan program rules including POA requirements for veterans.

American Land Title Association

Industry resources on POAs at closing and title insurance underwriting.

HUD - RESPA

Real Estate Settlement Procedures Act overview.

CFPB - About POAs

Consumer Financial Protection Bureau guide to powers of attorney.

ABA Real Property Section

American Bar Association resources on real estate practice.

Create your Real Estate Power of Attorney in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.