What Is a Revocable Living Trust?

A revocable living trust is a fiduciary instrument created during the grantor's lifetime that separates legal title from equitable title. The grantor (also called the settlor or trustor) transfers legal title to a trustee, who holds the property under a written trust agreement for the benefit of beneficiaries named in the document. Because the grantor retains the power to amend or revoke the trust at any time during life, the IRS treats the structure as a grantor trust under IRC §§ 671-679. Trust income flows to the grantor's individual Form 1040 using the grantor's Social Security number, and no Form 1041 fiduciary return is required while the grantor is alive and competent.

Trust law in the United States is largely a creature of state statute. The Uniform Trust Code (UTC), promulgated by the Uniform Law Commission in 2000 and updated through the 2018 amendments, has been enacted in 36 jurisdictions including Florida, Tennessee, Pennsylvania, Virginia, Massachusetts, and the District of Columbia. UTC §§ 401-409 govern trust creation, requiring intent to create a trust, a definite beneficiary (or a charitable purpose), trust property, and a trustee with active duties. States that have not adopted the UTC (notably California, New York, Texas, and Illinois) follow common law trust principles modified by their own probate or trust codes. California Probate Code §§ 15200 and following, the New York Estates, Powers and Trusts Law (EPTL), and the Texas Trust Code each reach the same core requirements through different statutory language.

Revocable vs irrevocable

Revocability is the central design choice. A revocable trust under UTC § 602 stays subject to amendment, restatement, and revocation by the grantor for as long as the grantor has capacity, which is what makes the trust a planning tool rather than a transfer of wealth. The trade-off is that IRC § 2038 pulls every asset in a revocable trust back into the grantor's gross estate at death, and every state treats those assets as reachable by the grantor's creditors during life. An irrevocable trust permanently transfers ownership. The grantor cannot retrieve the assets, which removes them from the gross estate (IRC § 2036) and starts the IRC § 2503(b) annual gift tax calculation at funding. Irrevocable trusts also unlock spendthrift protection under UTC § 502, the domestic asset protection trust laws in 19 states (Alaska, Delaware, Nevada, South Dakota, Tennessee, Wyoming, and others), and the long-term planning structures used for special needs beneficiaries, generation-skipping transfers, and life insurance ownership through an ILIT.

Funding the trust (titling assets)

A trust that is signed but not funded provides nothing. Funding means retitling each asset into the trustee's name. Real estate is transferred by quitclaim or grant deed naming the trustee in fiduciary capacity (for example, “Catherine M. Whitfield, Trustee of the Catherine M. Whitfield Revocable Living Trust dated March 12, 2025”), executed before a notary, and recorded with the county recorder where the property sits. The federal Garn-St. Germain Act (12 U.S.C. § 1701j-3(d)) bars lenders from invoking due-on-sale clauses for transfers to a revocable trust where the grantor remains a beneficiary and continues to occupy the property. Bank and brokerage accounts are retitled through the institution's trust certification process, almost always relying on a Certificate of Trust under UTC § 1013. Vehicles can be retitled in a trust's name in roughly 35 states; the rest (including Texas) require a beneficiary designation or post-death affidavit instead. Tangible personal property is transferred by an Assignment of Personal Property executed at the same time as the trust agreement.

Pour-over will mechanic

Even a diligent grantor will leave some assets in individual name at death: an account opened after funding, a refund check, a vehicle in a non-trust-titling state, an inheritance received during illness. A pour-over will, recognized in every state under the Uniform Testamentary Additions to Trusts Act or comparable provisions (California Probate Code § 6300, New York EPTL § 3-3.7), directs the residuary of the probate estate to the trustee of the existing trust. The will itself is admitted to probate, but the trust then governs the ultimate disposition. The pour-over will is also the only instrument that can nominate a guardian for minor children under state probate code (for example, California Probate Code § 1500), which is one reason a will-plus-trust pairing remains the standard estate plan even when the trust holds nearly everything.

Trustee duties under the UTC

A trustee holds fiduciary duties that cannot be waived by drafting (UTC § 105). Core duties include the duty of loyalty (UTC § 802), which prohibits self-dealing absent informed consent or court approval; the duty of impartiality (UTC § 803) when there is more than one beneficiary; the duty of prudent administration (UTC § 804), measured by the Uniform Prudent Investor Act standard adopted in nearly all states; the duty to keep adequate records and account to beneficiaries (UTC § 813), generally requiring annual reports; and the duty to inform beneficiaries of the trust's existence and material terms within 60 days of accepting trusteeship or learning that the trust has become irrevocable. Breach of these duties exposes the trustee to surcharge for losses, removal, and in some cases personal liability for taxes the trust failed to pay.

Spendthrift provisions

A spendthrift clause restricts both voluntary alienation by the beneficiary (selling or pledging the trust interest) and involuntary attachment by the beneficiary's creditors. UTC § 502 makes a spendthrift restriction enforceable so long as it limits both transfer types. The clause does not protect against four classes of claim under UTC § 503: a child or former spouse with a support judgment, a judgment creditor who provided services for protection of the beneficiary's interest, the federal government for tax debts, and a state for support claims. A spendthrift clause in a self-settled revocable trust does not protect the grantor from the grantor's own creditors in any state outside the 19 domestic asset protection trust jurisdictions, where the trust must be irrevocable and survive a state-specific look-back period (4 years in Nevada and Delaware, 2 years in Wyoming) before the protection takes effect.

Probate Avoidance

Trust assets pass directly to beneficiaries without court involvement, saving time and money

Privacy Protection

Trust terms, asset details, and beneficiary information remain private and never appear on the court docket

Incapacity Planning

Successor trustee manages assets immediately on the grantor's incapacity, with no conservatorship petition required

Revocable Living Trust Form Preview

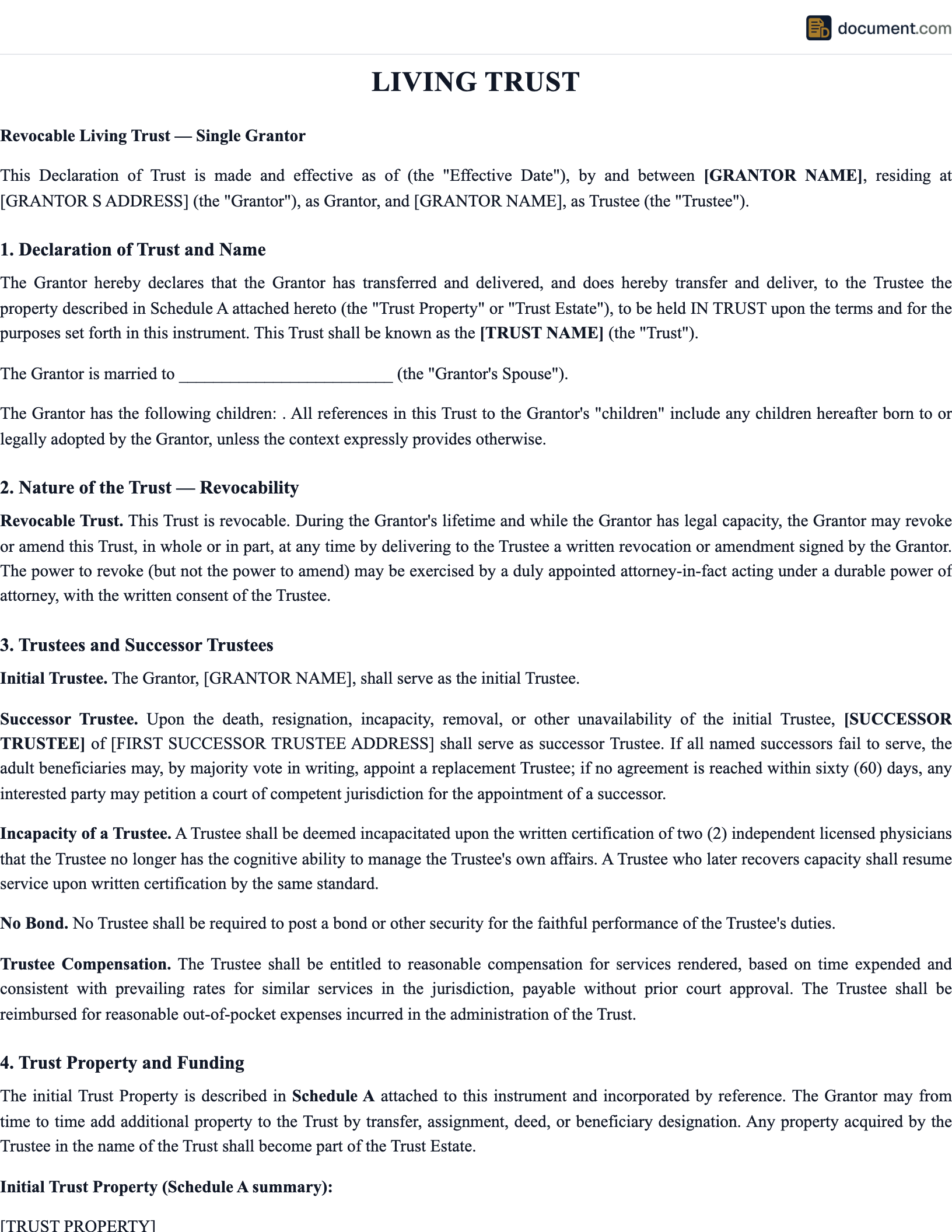

A complete revocable living trust agreement runs 15 to 25 pages and addresses creation, trustee succession, lifetime distributions, incapacity standards, post-death distribution, sub-trust funding, spendthrift protection, trustee powers, accounting duties, and execution formalities. The preview below shows the four anchoring sections that any review of a trust starts with: the identity of the parties, the trust property schedule, the beneficiary designations, and the notarized signature block. Your completed agreement is customized to the controlling state law (UTC, California Probate Code, New York EPTL, Texas Trust Code, or Florida Trust Code).

Revocable Living Trust Agreement

The Catherine M. Whitfield Revocable Living Trust

Article I: Trust Creation & Identity

Article II: Trust Property (Schedule A)

Article III: Beneficiary Designations

Primary Beneficiaries

Execution

Grantor/Trustee Signature

Notary Public

Types of Trusts

The revocable living trust is the standard estate-planning vehicle, but several specialized trust forms address goals the basic revocable trust cannot reach. Irrevocable trusts remove assets from the grantor's gross estate under IRC § 2036 and provide creditor protection unavailable in any revocable structure. Special needs trusts under 42 U.S.C. § 1396p(d)(4)(A) preserve a beneficiary's eligibility for SSI and Medicaid. Charitable remainder trusts (IRC § 664) and charitable lead trusts (IRC § 170(f)) split benefits between charity and family while generating income tax deductions and removing appreciated property from the taxable estate.

Living Trust vs Other Estate Planning Tools

A trust is one of several mechanisms that move property at death. The others (a will admitted to probate, transfer-on-death (TOD) and payable-on-death (POD) beneficiary designations under the Uniform Transfer on Death Security Registration Act, joint tenancy with right of survivorship, community-property-with-right-of-survivorship in nine community property states, and TOD deeds available in 31 jurisdictions) each have distinct strengths and failure modes. The right plan uses the trust for assets that benefit from probate avoidance, ongoing management, and creditor protection, and uses the lighter mechanisms for assets where probate is acceptable or beneficiary designations are easier to maintain.

Living Trust vs Last Will and Testament

Revocable Living Trust

- - Avoids probate for trust assets

- - Operates during life and after death

- - Remains completely private

- - Provides incapacity management

- - Cannot name guardians for children

- - More expensive to create and maintain

Last Will and Testament

- - Requires probate for enforcement

- - Takes effect only at death

- - Becomes public record during probate

- - No incapacity provisions

- - Only way to name child guardians

- - Simpler and less expensive to create

Best practice: Use both. The trust holds the bulk of your assets and avoids probate. A pour-over will catches anything not transferred to the trust and names guardians for minor children.

Living Trust vs Transfer-on-Death Designations

Revocable Living Trust

- - Centralized management of all assets

- - Can impose conditions on distributions

- - Provides incapacity management

- - Requires funding (transferring assets)

- - More complex to establish

TOD/POD Designations

- - Simple beneficiary designation on accounts

- - Outright distribution only, no conditions or staging

- - No incapacity provisions

- - No setup required beyond completing a form

- - Free through your financial institution

When to use which: TOD and POD designations are useful for simple situations with competent adult beneficiaries. A trust is better when you need conditions on distributions, have minor or special needs beneficiaries, or want coordinated management of multiple assets.

How to Create a Revocable Living Trust: A 7-Step Guide

A living trust takes effect through two coordinated acts: execution of the trust agreement and funding of the trust corpus. Skip funding and the document is a nullity. Skip notarization in a state that requires it and the trust may be voidable. Work through the steps in order, document each asset transfer, and store the executed agreement, the deeds of conveyance, and the assignments of personal property as a single package the successor trustee can act on without searching.

Inventory Your Assets

Build a schedule of every asset you hold: real property by parcel and APN, bank and brokerage accounts by institution and last four digits, retirement accounts (IRA, 401(k), 403(b)) with current beneficiary designations, life insurance face value and beneficiary, vehicles by VIN, closely held business interests with operating-agreement transfer restrictions noted, and tangible personal property of material value. Identify titling form for each: sole, joint tenancy with right of survivorship, tenancy by the entirety (available in 25 states for spouses), or community property (in nine community-property states). Joint-tenancy and beneficiary-designated assets generally bypass probate already and do not need retitling. The inventory determines which assets must be moved into the trust and which already pass outside of probate by operation of law.

Choose Your Successor Trustee

The successor trustee assumes legal title and fiduciary control on the grantor's incapacity (defined in the trust by reference to written certification by one or two licensed physicians, or by a designated trust protector) or death. The role carries the duty of loyalty under UTC § 802, the duty of prudent administration under UTC § 804 measured by the Uniform Prudent Investor Act standard, and the duty to account to beneficiaries under UTC § 813. Name at least one alternate. Spouses commonly serve as co-trustees with an adult child or corporate trustee as successor. Corporate trustees (bank trust departments, trust companies) charge roughly 0.5 to 1.5 percent of assets under management annually and bring institutional record-keeping that an individual trustee often cannot match. Avoid naming a beneficiary as sole trustee of a sub-trust where the beneficiary holds discretion over distributions to themselves; that arrangement defeats spendthrift protection and exposes the trust to creditor reach under UTC § 504.

Define Distribution Terms

State the dispositive plan with precision. Outright distribution at the grantor's death works for adult competent beneficiaries with no creditor exposure. Staged distributions (a common structure: one-third at 25, one-third at 30, balance at 35) require sub-trusts that survive past the grantor and need their own trustee, accounting, and EIN. Special-needs beneficiaries should receive their share through a third-party special needs trust drafted to preserve eligibility for SSI and Medicaid under 42 U.S.C. § 1396p(d)(4)(A) (first-party d(4)(A) trust) or § 1396p(d)(4)(C) (pooled trust). Specify per stirpes versus per capita distribution if a beneficiary predeceases the grantor; the default rule under the Uniform Probate Code § 2-709 is per capita at each generation, which differs from common-law per stirpes. Address the contingency of all named beneficiaries predeceasing through a residual clause naming a charity or class of relatives.

Draft and Sign the Trust Agreement

The trust agreement must identify the grantor, the initial trustee, the successor trustees in order, the beneficiaries, the trust property (typically by Schedule A reference), the dispositive terms during life and at death, the trustee powers (UTC § 815 default powers can be incorporated by reference or expanded), administrative provisions (governing law, situs, spendthrift clause, no-contest clause), and the grantor's express reservation of the power to amend or revoke. Notarization is required in 47 states and recommended even where not required because financial institutions generally refuse to honor a trust certification without a notarized signature page. Florida (Fla. Stat. § 736.0403) and Louisiana (La. Rev. Stat. § 9:1751) require two witnesses in addition to the notary. Trusts are not filed with the court; they remain private documents. Keep the original in a fireproof location and give the successor trustee a complete copy.

Fund the Trust

Funding is a separate act for each asset class. Real estate requires a quitclaim or grant deed from the grantor to the trustee, executed before a notary, and recorded with the county recorder. The Garn-St. Germain Act (12 U.S.C. § 1701j-3(d)) protects the transfer from due-on-sale acceleration. California (Proposition 13), Texas, and most other states do not reassess property tax for a transfer to the grantor's revocable trust. Bank and brokerage accounts are retitled by submitting a Certificate of Trust under UTC § 1013 (or state equivalent like California Probate Code § 18100.5). Retirement accounts are generally handled by beneficiary designation rather than ownership transfer; the SECURE Act of 2019 imposed a 10-year payout rule on most non-spousal beneficiaries that affects whether a conduit or accumulation trust is the right structure. Tangible personal property is transferred by an Assignment of Personal Property attached as Schedule B.

Critical: An unfunded trust provides nothing. Assets still in your individual name at death go through probate under the will or, in default of a will, under the state intestacy statute, regardless of the existence of the trust.

Create a Pour-Over Will

A pour-over will is the safety net for assets that escape funding. The Uniform Testamentary Additions to Trusts Act, codified in every state (California Probate Code § 6300, New York EPTL § 3-3.7, Florida Statute § 732.513), permits a will to dispose of property to the trustee of a trust identified by date and grantor, even if the trust is amended after the will is executed. The will is admitted to probate, the residue is paid to the trustee, and the trust then governs distribution. The pour-over will is also the only instrument that nominates a guardian for minor children (California Probate Code § 1500, New York SCPA § 1726), which keeps the will in the estate plan even when the trust holds nearly all the assets.

Review and Update Periodically

Review the trust on a fixed cycle (every 3 to 5 years) and on every triggering event: marriage, divorce, birth or adoption, death of a beneficiary or trustee, sale or acquisition of real property, relocation to a new state, sale of a business interest, or material change in federal tax law. The federal estate tax exemption is $13.99 million per individual in 2025 and is scheduled to revert to roughly $7 million on January 1, 2026 unless Congress extends the higher amount, which will materially change A/B trust funding and disclaimer planning. Minor edits go through a trust amendment; cumulative or substantive edits warrant a complete restatement, which preserves the original trust date and avoids re-funding. Audit the funding schedule each review and confirm new assets carry the trustee title.

Key Components of a Revocable Living Trust

A complete trust agreement contains nine working parts. Each maps to a specific UTC article or state-code section and answers a question the successor trustee will face. The declaration establishes the trust's identity and governing law (UTC § 107). The trustee provisions name initial and successor trustees and define removal authority (UTC §§ 704-706). The trust property schedule lists what is funded. The lifetime provisions define the grantor's reserved powers (UTC § 602). The incapacity provisions trigger successor authority. The distribution plan governs the dispositive scheme. The spendthrift clause anchors creditor protection (UTC § 502). The tax provisions accommodate IRC § 671-679 grantor-trust treatment and any A/B split. The execution block carries the formalities. Omitting any one creates a gap the successor trustee will have to fill through court petition.

| Component | Description |

|---|---|

| Trust Declaration | Trust name, date of creation, grantor identification, statement of revocability, and governing state law |

| Trustee Provisions | Initial trustee, successor trustee, co-trustee provisions, trustee powers, compensation, and removal procedures |

| Trust Property (Schedule A) | Description of all assets transferred to the trust, updated as assets are added or removed |

| Lifetime Provisions | Grantor's rights during lifetime: income distributions, principal access, amendment, and revocation rights |

| Incapacity Provisions | Definition of incapacity, process for determining incapacity, and successor trustee's authority during incapacity |

| Distribution Plan | Specific and residuary distributions after death, including sub-trust provisions for minors and conditional distributions |

| Spendthrift Clause | Protects trust assets from beneficiaries' creditors and prevents assignment of trust interests |

| Tax Provisions | A/B trust splitting for married couples, generation-skipping transfer tax provisions, and income tax reporting instructions |

Funding Your Living Trust

Funding is the act of retitling each asset from the grantor's individual name into the trustee's fiduciary capacity. A trust without funded assets is a legal shell with nothing to administer; the assets pass through probate at death just as if no trust existed. Each asset class uses a different transfer instrument and different recording or notification rules. Track each transfer in writing and update Schedule A whenever the asset roster changes.

Real Estate

Execute a new deed (quitclaim or grant deed) from your name to yourself as trustee. Record the deed with the county recorder. Notify your insurance company and mortgage lender. Property tax reassessment exemptions apply in most states for transfers to revocable trusts.

Bank & Investment Accounts

Contact each institution and request to retitle the account in the trust's name. You will typically need a copy of the trust or a certificate of trust. The process usually takes 1 to 2 weeks per institution.

Retirement Accounts & Life Insurance

Name the trust as beneficiary, not as owner. The SECURE Act of 2019 imposed a 10-year payout rule on most non-spousal beneficiaries (29 U.S.C. § 1056), and naming an accumulation trust rather than a conduit trust changes how distributions are taxed. Confirm the trust qualifies as a designated beneficiary under Treas. Reg. § 1.401(a)(9)-4 before making the designation.

Personal Property

Execute an Assignment of Personal Property transferring tangible items (furniture, jewelry, art, collectibles) to the trustee, attached as Schedule B. Roughly 35 states accept vehicle titling in a trust's name; states that do not (including Texas) require a transfer-on-death designation or post-death affidavit instead.

Legal Requirements for Living Trusts

Trust law operates at three levels. Federal tax law (IRC §§ 671-679 for grantor trust treatment, IRC §§ 2036-2042 for estate-tax inclusion, IRC §§ 2501-2524 for gift tax) determines how the trust is taxed. State trust law (the Uniform Trust Code in 36 jurisdictions, the California Probate Code, the New York EPTL, the Texas Trust Code) determines validity, trustee duties, and beneficiary rights. State property and recording law determines how each asset is conveyed to the trustee and how creditor claims attach. A trust that satisfies one layer but fails another produces unintended results that no later amendment can fully cure.

Uniform Trust Code (UTC)

The UTC has been enacted in 36 jurisdictions, including Florida, Pennsylvania, Tennessee, Virginia, Massachusetts, Ohio, Michigan, Arizona, Oregon, and the District of Columbia. UTC §§ 401-409 govern creation; §§ 501-507 govern creditor reach and spendthrift protection; §§ 601-604 govern revocability and grantor capacity; §§ 801-817 govern trustee duties and powers; §§ 1001-1012 govern remedies for breach. The non-UTC states (California, New York, Texas, Illinois, and others) reach similar substantive results through their own probate and trust codes.

Trust creation requirements (UTC § 402)

A valid trust requires: a settlor with capacity to convey property (the same standard as for a contract or deed, higher than testamentary capacity for a will), present intent to create a trust, a definite beneficiary or a charitable, animal, or noncharitable purpose trust authorized by UTC §§ 408-409, a trustee with duties to perform, and trust property. Capacity is presumed but can be challenged on the same grounds as contract incapacity (cognitive impairment, undue influence, fraud). The writing requirement is statutory in most states (California Probate Code § 15206, Florida Statute § 736.0403); only a few states recognize oral revocable trusts of personal property and even those require clear and convincing evidence of the terms. Notarization is required in Florida and several other states and is universally recommended because financial institutions refuse to act on a trust certification without notarization.

Grantor trust income tax treatment

IRC §§ 671-679 treat a trust as a grantor trust for income tax purposes whenever the grantor retains powers that the Internal Revenue Code identifies as inconsistent with a complete transfer. The power to revoke (IRC § 676), the power to control beneficial enjoyment (IRC § 674), the power to revest title in the grantor (IRC § 673), and the power to deal with the trust without adequate consideration (IRC § 675) each independently triggers grantor-trust status. A revocable living trust always satisfies IRC § 676. The consequence: trust income, deductions, and credits flow through to the grantor's Form 1040, the trust uses the grantor's SSN as its TIN, and no Form 1041 is required during the grantor's life. After the grantor's death, the trust becomes a separate taxpayer, must obtain an EIN from the IRS, and files Form 1041 annually. Compressed trust tax brackets reach the top 37 percent federal rate at $15,200 of taxable income in 2025, which makes distributing income to beneficiaries (who are taxed at their own rates) tax-efficient.

Estate tax inclusion (IRC § 2038)

IRC § 2038 includes in the gross estate any property the decedent transferred during life over which the decedent retained the power to alter, amend, revoke, or terminate. A revocable trust satisfies that test by definition. The federal exemption is $13.99 million per individual in 2025, with a top rate of 40 percent on the excess. The exemption is scheduled to drop to roughly $7 million on January 1, 2026 unless Congress extends the Tax Cuts and Jobs Act sunset. State estate tax thresholds are far lower: Oregon $1 million, Massachusetts $2 million, Washington $2.193 million, Maryland $5 million, New York $6.94 million (with a cliff that taxes the entire estate if it exceeds the exemption by more than 5 percent). Twelve states and the District of Columbia impose an estate tax; six states impose an inheritance tax (Iowa, Kentucky, Maryland, Nebraska, New Jersey, Pennsylvania).

State-specific variations

- Trust protectors: Alaska (AS § 13.36.370), Delaware (12 Del. C. § 3313), Nevada (NRS § 163.5553), South Dakota (SDCL § 55-1B-6), Tennessee (T.C.A. § 35-15-1201), and Wyoming explicitly authorize trust protectors with statutory powers to modify, change trustees, or approve distributions. UTC § 808 reaches a similar result by recognizing nonfiduciary advisors.

- Creditor claims after death: California Probate Code §§ 19000-19403 lets the trustee open a 4-month creditor claims window similar to probate; the federal tax lien runs separately under 26 U.S.C. § 6324. Florida (Fla. Stat. § 736.05053) imposes a 2-year limit. Texas leaves trust creditor claims to the general 4-year limitations period.

- Property tax and transfer tax exemptions: California Revenue and Taxation Code § 62(d) excludes transfers to a revocable trust from change-of-ownership reassessment under Proposition 13. Most states grant a transfer tax exemption (R&T Code § 11930 in California, Real Property Law § 257-a in New York), but some require an exemption affidavit at recording.

- Beneficiary notification: UTC § 813 and California Probate Code § 16061.7 require the trustee to send notice to beneficiaries within 60 days of a trust becoming irrevocable (typically the grantor's death), starting a 120-day clock to contest the trust under California Probate Code § 16061.8.

- Witness requirements: Florida (Fla. Stat. § 736.0403) requires two witnesses and a notary for the trust to be valid as to testamentary dispositions. Louisiana requires two witnesses under La. Rev. Stat. § 9:1751. Most other states require only the grantor's notarized signature.

Sample Revocable Living Trust

The condensed sample below shows six anchor articles every revocable living trust contains: trust creation with the grantor's reservation of revocation power (UTC § 602), lifetime distributions to or for the benefit of the grantor (IRC § 676 grantor-trust treatment), incapacity standards triggering successor authority, post-death distribution, trustee succession with Uniform Prudent Investor Act powers, and the spendthrift clause anchoring creditor protection (UTC § 502). Your completed agreement is customized to the controlling state law and includes the additional provisions (A/B split, special needs sub-trust, generation-skipping language) appropriate to your situation.

REVOCABLE LIVING TRUST AGREEMENT

The [Grantor Name] Revocable Living Trust

ARTICLE I: TRUST CREATION

I, [Grantor Name], hereby create this Revocable Living Trust. I transfer to the Trustee the property described in Schedule A attached hereto, and any other property that may be transferred to the Trust from time to time. I reserve the right to amend, revoke, or terminate this Trust at any time during my lifetime...

ARTICLE II: DISTRIBUTIONS DURING LIFETIME

During my lifetime, the Trustee shall distribute to me or for my benefit such amounts of income and principal as I may request. The Trustee shall manage, invest, and reinvest the Trust property as I may direct...

ARTICLE III: INCAPACITY

If I become unable to manage my financial affairs as determined by[one/two] licensed physician(s), the Successor Trustee shall assume management of the Trust and shall use Trust income and principal for my health, education, maintenance, and support...

ARTICLE IV: DISTRIBUTIONS AFTER DEATH

Upon my death, after payment of debts, taxes, and administration expenses, the Trustee shall distribute the remaining Trust property as follows:[Distribution Plan]...

ARTICLE V: TRUSTEE PROVISIONS

I appoint myself as initial Trustee. Upon my incapacity or death, I appoint[Successor Trustee] as Successor Trustee. The Trustee shall have all powers granted by applicable state law, including the power to sell, lease, mortgage, invest, and manage Trust property...

ARTICLE VI: SPENDTHRIFT

No beneficiary shall have the power to anticipate, assign, or encumber any interest in the Trust. No interest of any beneficiary shall be subject to the claims of any creditor of such beneficiary...

Frequently Asked Questions

Common questions on revocable versus irrevocable structure, probate avoidance, trust funding, trustee selection, creditor reach, estate-tax interaction, and the role of a Certificate of Trust under UTC § 1013.

Official Resources

Primary statutory and regulatory sources, plus practitioner references, for living trust drafting, funding, taxation under IRC §§ 671-679, and fiduciary administration.

ABA - Estate Planning Resources

American Bar Association resources on trusts and estate planning

ULC - Uniform Trust Code

Uniform Law Commission information on the UTC and state adoption

AARP - Living Trust Guide

Comprehensive guide to understanding and creating a living trust

IRS - Trust Tax Information

Federal tax requirements for trusts, including Form 1041 filing

Nolo - Living Trust Encyclopedia

Free legal information on living trusts, funding, and administration

CFPB - Fiduciary Guides

Consumer Financial Protection Bureau guides for trustees and fiduciaries

Create your Living Trust in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.