What Is a Pour-Over Will?

A pour-over will is a specialized estate planning document designed to work in conjunction with a revocable living trust. Its primary function is deceptively simple: it directs that any assets remaining in the decedent's individual name at the time of death be transferred — or "poured over" — into the existing living trust. From there, the trust's terms govern how those assets are managed and distributed to beneficiaries. The pour-over will acts as a backstop for the trust-based estate plan, catching property that was never formally transferred into the trust during the grantor's lifetime and ensuring it reaches its intended destination.

The need for a pour-over will arises from a practical reality of trust-based estate planning: no matter how diligent a grantor is about funding their trust, some assets almost inevitably remain outside of it. A checking account opened after the trust was created, a vehicle purchased without titling it in the trust's name, an unexpected inheritance, a tax refund check, or personal property that was simply overlooked — any of these can slip through the cracks. Without a pour-over will, these unfunded assets would pass under the state's intestacy laws, potentially going to heirs the grantor never intended to benefit or in proportions that contradict the carefully crafted trust distribution plan.

It is essential to understand that a pour-over will does notavoid probate. Assets caught by the pour-over will must pass through the probate process before they reach the trust. The probate avoidance advantage comes from the living trust itself — assets properly titled in the trust's name bypass probate entirely. The pour-over will is a safety mechanism, not a probate-avoidance tool. Its value lies in ensuring that the grantor's unified distribution scheme is preserved even for assets that were not successfully funded into the trust during life.

The concept originated from a tension in estate planning law: traditionally, a will could only distribute property to identifiable beneficiaries or entities in existence at the time the will was executed. Because a revocable trust can be amended after the will is signed, courts initially questioned whether a will could validly direct assets to a trust whose terms might change. The Uniform Testamentary Additions to Trusts Act (UTATA), first approved in 1960 and revised in 1991, resolved this issue by explicitly permitting pour-over devises to inter vivos trusts, including trusts that are amended after the will's execution. Today, all 50 states recognize pour-over wills in some form.

A properly drafted pour-over will is an indispensable component of any trust-based estate plan. Combined with a revocable living trust, durable power of attorney, and advance healthcare directive, the pour-over will ensures comprehensive coverage of all contingencies. Our attorney-reviewed templates reference your specific trust by name and date, comply with your state's will execution requirements, and include provisions for executor designation, guardian appointment for minor children, and specific personal property bequests where appropriate.

Safety Net

Captures any assets that were not transferred into your living trust during your lifetime

Unified Plan

Ensures all assets ultimately follow your trust's distribution plan, regardless of how they are titled

Intestacy Protection

Prevents unfunded assets from passing under default state intestacy laws to unintended heirs

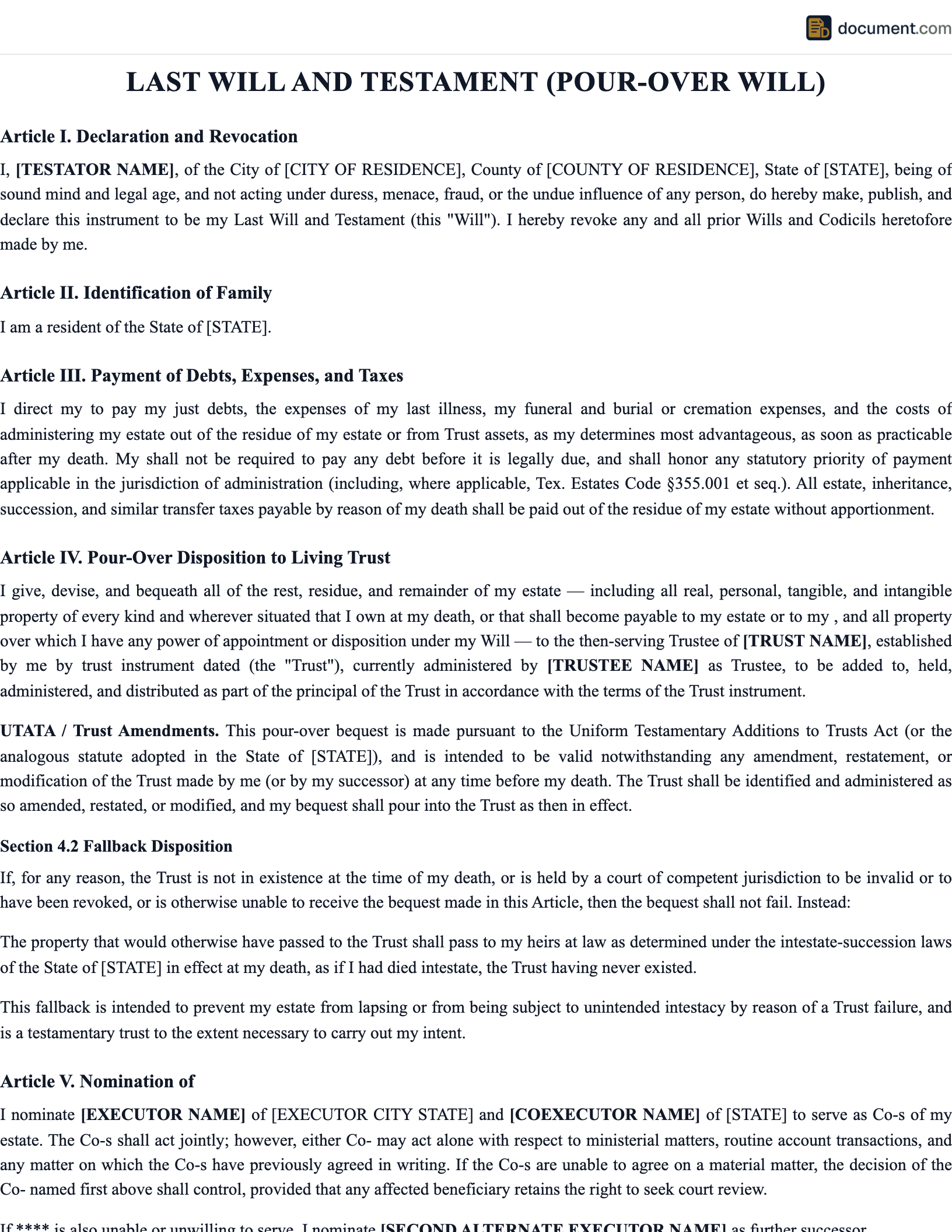

Pour-Over Will Form Preview

Below is a visual preview of the sections and fields included in a standard pour-over will form. This mockup illustrates how the will references the living trust and structures the pour-over directive. Your completed document will be customized for your state's execution requirements and your specific trust information.

Pour-Over Last Will and Testament

With Trust Designation

Section 1: Testator (Person Making This Will)

Section 2: Revocable Living Trust Reference

Section 3: Executor (Personal Representative)

Primary Executor

Alternate Executor

Section 4: Pour-Over Provision

"I give, devise, and bequeath all of my estate, including all real and personal property and all property over which I have a power of appointment, to the then-acting Trustee of The Catherine M. Harrington Revocable Living Trust, dated March 14, 2022, as amended from time to time, to be added to and administered as part of that trust according to its terms."

Section 5: Guardian of Minor Children (If Applicable)

Section 6: Execution

Testator Signature

Notary Public

Witness 1 Signature

Witness 2 Signature

How a Pour-Over Will Works

Understanding the mechanics of a pour-over will requires seeing it in the context of a complete trust-based estate plan. The pour-over will does not operate independently — it functions as one piece of a coordinated system that manages assets during life, at incapacity, and after death.

During Your Lifetime: Fund the Trust

You create a revocable living trust and transfer assets into it — retitling bank accounts, deeding real estate, reassigning brokerage accounts, and changing beneficiary designations. Assets held in the trust's name avoid probate. The pour-over will sits dormant during this period, ready to activate only at your death.

At Death: Identify Unfunded Assets

When you pass away, the executor named in the pour-over will identifies any assets still held in your individual name — not in the trust. This might include a recently opened bank account, a vehicle, personal property, pending insurance claims, or an inheritance you received shortly before death. These assets constitute the probate estate.

Probate: Process the Unfunded Assets

The executor files the pour-over will with the probate court, opens a probate proceeding, notifies creditors, pays valid debts and taxes from the probate estate, and obtains court authorization to transfer the remaining assets. This process typically takes 6 to 18 months depending on the jurisdiction and whether the estate qualifies for simplified probate procedures.

Pour-Over: Transfer Assets to the Trust

Once probate is complete, the executor transfers the remaining probate assets into the living trust. The trustee then distributes those assets along with all other trust assets according to the trust's distribution provisions. The result is that all assets — whether funded during life or caught by the pour-over will — follow the same unified distribution plan.

Key insight: The more assets you successfully transfer into your trust during your lifetime, the fewer assets must pass through probate via the pour-over will. Diligent trust funding minimizes the probate estate, reduces costs and delays, and keeps more of your estate private. The pour-over will should be your backup, not your primary transfer mechanism.

Pour-Over Will vs Other Documents

A pour-over will occupies a unique role in estate planning. Understanding how it differs from related documents helps clarify when and why it is needed.

Pour-Over Will vs Standard Last Will & Testament

Pour-Over Will

- - Directs assets into a living trust

- - Trust controls final distribution, not the will

- - Designed to work with an existing trust

- - Typically has one primary beneficiary: the trust

- - Distribution details stay private (in the trust)

Standard Will

- - Distributes assets directly to beneficiaries

- - The will itself specifies who gets what

- - Works as a standalone document

- - Names multiple beneficiaries with specific bequests

- - Distribution details become public through probate

Key takeaway:A pour-over will is not a replacement for a standard will — it is a companion to a living trust. If you do not have a living trust, a standard will is the appropriate document. If you do have a trust, the pour-over will ensures that all assets eventually reach the trust.

Pour-Over Will vs Revocable Living Trust

Pour-Over Will

- - Activates only at death

- - Handles assets NOT in the trust

- - Requires probate to function

- - Becomes a public document when filed

- - Names an executor, not a trustee

Revocable Living Trust

- - Operates during life and after death

- - Handles assets titled IN the trust

- - Avoids probate entirely for funded assets

- - Remains a private document

- - Names a trustee to manage assets

Best practice: These two documents are designed to work as a pair. The trust handles assets you successfully fund during your lifetime (avoiding probate), and the pour-over will catches everything else (through probate) and directs it to the trust.

Pour-Over Will vs Transfer-on-Death (TOD) Designations

Pour-Over Will

- - Catches all unfunded assets broadly

- - Requires probate to transfer assets

- - Transfers to the trust as a whole

- - One document covers all asset types

TOD Designation

- - Applies to specific accounts or property

- - Avoids probate — transfers automatically at death

- - Names specific beneficiaries per account

- - Must be set up individually for each asset

When to use both: TOD designations on individual accounts can direct specific assets to the trust at death without probate. But TOD designations only cover assets where you specifically set them up. The pour-over will covers everything else as a catch-all.

How to Create a Pour-Over Will: An 8-Step Guide

Creating a valid pour-over will requires coordination with your existing living trust (or one you are creating simultaneously). Follow these steps to ensure your pour-over will properly references your trust and meets your state's execution requirements.

Establish Your Revocable Living Trust First

A pour-over will requires an existing trust to pour into. Most states require the trust to be in existence at the time the pour-over will is executed, or to be created simultaneously. Create your revocable living trust first, fund it with your major assets, and then create the pour-over will as the companion document. If you are working with an attorney, both documents are typically prepared and signed in the same session.

Gather Your Trust Details

You will need the exact legal name of your trust (e.g., "The John and Jane Smith Revocable Living Trust"), the date it was executed, the name of the current trustee, and the name of the successor trustee. The pour-over will must reference the trust with precision so there is no ambiguity about which trust receives the poured-over assets. If you have amended the trust, include language indicating the will refers to the trust "as amended from time to time."

Name Your Executor (Personal Representative)

The executor is responsible for managing the probate process for assets caught by the pour-over will. Many people name the same person as executor and successor trustee for administrative simplicity. Choose someone who is organized, trustworthy, and willing to serve. Name at least one alternate executor in case your first choice is unable or unwilling to act.

Tip: If the executor and successor trustee are the same person, the transfer of probated assets into the trust is simplified because the same individual controls both sides of the transaction.

Draft the Pour-Over Provision

The core of the pour-over will is the residuary clause that directs all remaining estate assets to the trustee of your living trust. This clause should reference the trust by its full name and date of execution, include language addressing future trust amendments (so the trust as it exists at your death controls distribution), and contain a contingency provision in case the trust is not in existence or has been revoked at the time of your death.

Include Guardian Designation (If You Have Minor Children)

A living trust cannot name a guardian for minor children — only a will can do this. Your pour-over will should include a guardian designation if you have minor children, naming the person you want to serve as guardian of their person (physical custody and care) and potentially a separate person as guardian of their estate (financial management). This is one of the most important functions of a pour-over will beyond the pour-over provision itself.

Consider Specific Bequests for Tangible Personal Property

While the pour-over will directs the residuary estate to the trust, many states allow you to include a separate memorandum for tangible personal property (jewelry, furniture, art, family heirlooms) that can be updated without re-executing the will. Alternatively, you can include specific bequests directly in the pour-over will for items of particular sentimental or monetary value that you want to go to specific individuals.

Execute the Will According to State Law

A pour-over will must meet the same execution requirements as any other will in your state. This typically means signing the will in the presence of two disinterested witnesses (three in Vermont) and, in most states, having the will notarized or having the witnesses sign a self-proving affidavit. The testator must be of legal age (usually 18) and of sound mind. Failure to comply with execution formalities can invalidate the entire will.

Store Safely and Inform Your Executor

Store the original pour-over will in a fireproof safe, with your attorney, or in a probate court filing (some states allow pre-filing). Inform your executor where the original will and trust documents are stored. Provide copies to your executor and successor trustee. Do not store the only copy in a safe deposit box that may be sealed at your death and require court authorization to open.

Key Components of a Pour-Over Will

A pour-over will is simpler than a standard will because the distribution details are in the trust, not the will. However, every component must be precisely drafted to ensure the pour-over mechanism functions as intended.

| Component | Description |

|---|---|

| Testator Identification | Full legal name, date of birth, and domicile address of the person making the will |

| Revocation Clause | Statement revoking all prior wills and codicils to prevent conflicts with earlier documents |

| Trust Identification | Full legal name and date of execution of the revocable living trust receiving the poured-over assets |

| Pour-Over Provision | The residuary clause directing all remaining assets to the trustee of the living trust, including language honoring trust amendments |

| Executor Designation | Primary and alternate executor responsible for managing the probate estate and transferring assets to the trust |

| Executor Powers | Specific authority granted to the executor including paying debts, managing property, selling assets, and hiring professionals |

| Guardian Designation | Named guardian for minor children (this can only be done in a will, not in a trust) |

| Contingency Provision | Alternate distribution plan if the trust is no longer in existence at the time of the testator's death |

| Debt & Tax Directive | Instructions on how debts, taxes, and administration expenses should be paid before assets pour into the trust |

| Personal Property Memorandum | Optional reference to a separate list of tangible personal property bequests that can be updated without re-executing the will |

| Self-Proving Affidavit | Notarized statement by witnesses confirming proper execution, allowing the will to be admitted to probate without witness testimony |

| Governing Law | The state whose laws govern the will's interpretation, execution requirements, and probate procedure |

Common Trust Funding Gaps

Even the most diligent grantor will likely have some assets outside their trust at the time of death. Understanding the most common funding gaps helps you minimize what passes through probate while relying on the pour-over will as your safety net for anything that slips through.

Newly Acquired Assets

Bank accounts opened after trust creation, vehicles purchased without trust titling, new investment accounts, and recently acquired property are the most common unfunded assets. Grantors often forget to title new acquisitions in the trust's name.

Inheritances & Gifts

If you receive an inheritance or significant gift shortly before death, there may not be time to retitle the assets into the trust. This is especially common with inherited real estate, cash bequests, and inherited securities accounts.

Legal Claims & Settlements

Pending lawsuit recoveries, insurance claims, tax refunds, and settlement proceeds are typically paid to the individual, not the trust. These assets are easily overlooked in trust funding because they are contingent and may not exist at the time the trust is created.

Titled Personal Property

Vehicles, boats, RVs, ATVs, motorcycles, and aircraft all have titles that must be individually transferred into the trust. Many grantors fund their major assets (home, bank accounts) but overlook titled personal property because the transfer process varies by state and asset type.

Important:Some states have adopted simplified probate procedures for small estates — typically those under $50,000 to $200,000 in value (thresholds vary by state). If the assets caught by your pour-over will fall below your state's small estate threshold, your executor may be able to use an affidavit or summary administration procedure instead of full probate, significantly reducing time and cost.

Legal Requirements for Pour-Over Wills

A pour-over will must satisfy two sets of legal requirements: the general will execution requirements of your state, and the specific requirements for pour-over devises to inter vivos trusts. Failing to meet either set can invalidate the pour-over provision.

Uniform Testamentary Additions to Trusts Act (UTATA)

The Uniform Testamentary Additions to Trusts Act, first approved by the Uniform Law Commission in 1960 and revised in 1991, explicitly authorizes pour-over wills. It permits a will to devise property to the trustee of a trust that was established before, concurrently with, or in some states after the will's execution. The revised act also validates pour-overs to trusts that have been amended after the will was signed, meaning you can modify your trust without re-executing your pour-over will. Most states have adopted UTATA or similar legislation.

Will Execution Requirements

- Testamentary Capacity: The testator must be of legal age (18 in most states, 16 in Georgia, 14 in Idaho for personal property) and of sound mind — meaning they understand the nature of their property, the natural objects of their bounty, and the effect of making the will.

- Witnesses: Most states require two disinterested witnesses who observe the testator sign the will (or acknowledge their signature) and then sign the will themselves. Vermont requires three witnesses. Witnesses should not be beneficiaries of the will or trust to avoid the appearance of undue influence.

- Self-Proving Affidavit: Most states allow (and many strongly encourage) a self-proving affidavit — a notarized statement signed by the witnesses at the time of execution that allows the will to be admitted to probate without the witnesses needing to appear in court and testify.

- Trust Existence: Under UTATA, the trust must be identified in the will by its name and date. Most states require the trust to exist at the time the will is executed, though some permit the trust to be established concurrently or even afterward. The will should include language referencing the trust "as amended from time to time" to honor future amendments.

What If the Trust Is Revoked Before Death?

If the revocable living trust referenced in your pour-over will is revoked or terminated before your death, the pour-over provision may fail — there is no trust to receive the assets. In this scenario, the poured-over assets may pass under your state's intestacy laws, which could produce unintended results. A well-drafted pour-over will includes a contingency provision specifying an alternate distribution plan if the trust is no longer in existence at the time of death.

Sample Pour-Over Will

Below is a condensed preview of our pour-over will template. This sample illustrates the structure, trust reference language, and pour-over provision included in our attorney-reviewed documents. Your completed will is customized with your specific trust details and state execution requirements.

POUR-OVER LAST WILL AND TESTAMENT

With Revocable Living Trust Designation

I, [Full Legal Name], a resident of [County],[State], being of sound mind and legal age, declare this to be my Last Will and Testament. I hereby revoke all prior wills and codicils.

ARTICLE 1: EXECUTOR

I appoint [Executor Name] as Executor of this Will. If my Executor is unable or unwilling to serve, I appoint[Alternate Executor Name] as alternate Executor. My Executor shall serve without bond unless required by the court.

ARTICLE 2: DEBTS AND EXPENSES

I direct my Executor to pay all legally enforceable debts, funeral expenses, and costs of administration from the assets of my probate estate as soon as practicable after my death.

ARTICLE 3: POUR-OVER PROVISION

I give, devise, and bequeath all the rest, residue, and remainder of my estate, whether real, personal, or mixed, and wherever situated, including any property over which I may have a power of appointment, to the then-acting Trustee of the[Trust Name], dated [Trust Date], as said trust may be amended from time to time prior to my death, to be added to the trust estate and held, administered, and distributed in accordance with the provisions of said trust as they exist at the time of my death.

ARTICLE 4: CONTINGENCY

If the above-referenced trust is not in existence at the time of my death, or if it has been revoked or is otherwise inoperative, then I direct that the residue of my estate be distributed to [Contingent Beneficiary/ies], in equal shares, per stirpes.

ARTICLE 5: GUARDIAN OF MINOR CHILDREN

If I have minor children surviving me, I nominate[Guardian Name] as guardian of the person of my minor children...

Frequently Asked Questions

Find answers to common questions about pour-over wills, their relationship with revocable living trusts, probate implications, and how to ensure your estate plan works as intended.

Official Resources

For additional information on pour-over wills, trust-based estate planning, and probate procedures, consult these official and reputable resources.

ULC - Testamentary Additions to Trusts Act

Uniform Law Commission information on UTATA and state adoption

ABA - Real Property, Trust & Estate Law

American Bar Association resources on trusts, estates, and wills

Nolo - Pour-Over Will Guide

Free legal information on pour-over wills and trust planning

ACTEC - Estate Planning Resources

American College of Trust and Estate Counsel educational materials

AARP - Living Trust Guide

Understanding living trusts and their relationship to pour-over wills

NAELA - Elder Law Attorneys

Find an estate planning attorney near you

Create your Pour Over Will in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.