What Is an Irrevocable Living Trust?

An irrevocable living trust is a legal entity created during the grantor's lifetime that, once funded, cannot generally be amended, revoked, or terminated by the grantor. Assets transferred into the trust legally belong to the trust itself — held and administered by a trustee for the benefit of named beneficiaries. This permanent transfer of ownership is what distinguishes the irrevocable form from the revocable living trust, and it is the single reason irrevocable trusts deliver their signature tax, asset protection, and Medicaid planning benefits.

The irrevocable trust is governed in most states by the Uniform Trust Code, enacted in 2000 and adopted in some form by 35+ jurisdictions. Federal tax treatment is governed by Subchapter J of the Internal Revenue Code (IRC §§641 et seq.), with the grantor-trust rules of §§671-679 determining whether the trust is a separate taxpayer or is treated as transparent to the grantor. These dual sources — state trust law and federal tax law — must be reconciled in every irrevocable trust document.

The defining feature of the irrevocable trust — loss of grantor control — is precisely what creates its legal effects. Because the grantor has permanently surrendered ownership, the assets are removed from the grantor's taxable estate under IRC §2036, placed beyond the reach of future creditors under spendthrift doctrine (when properly drafted), and shielded from Medicaid asset tests after the five-year lookback period under 42 U.S.C. §1396p. A grantor who retains too much control defeats all of these benefits.

Because the decision to create an irrevocable trust is effectively permanent, the document must be drafted with unusual care. Once funded, mistakes can be corrected only through court modification, decanting, or beneficiary consent under narrow UTC provisions. This page provides a general-purpose template framework — suitable for many common uses — but complex structures such as ILITs, SLATs, GRATs, and dynasty trusts warrant individual professional drafting.

Permanent Transfer

Assets leave the grantor's estate and are owned by the trust

Creditor Shield

Spendthrift protection against future creditors and judgments

Estate Tax Removal

Assets excluded from the taxable estate under IRC §2036

Irrevocable vs. Revocable Living Trust

The two trust forms share probate avoidance but diverge sharply on control, taxation, and asset protection. Use the table below to confirm which fits your planning goals.

| Feature | Irrevocable | Revocable |

|---|---|---|

| Grantor can amend | No (limited exceptions) | Yes, at any time |

| Grantor can revoke | No | Yes |

| Removes assets from estate | Yes (IRC §2036) | No |

| Asset protection from creditors | Yes, after 5-year lookback | No |

| Medicaid planning benefit | Yes, after 5-year lookback | No |

| Avoids probate | Yes | Yes |

| Separate taxpayer (Form 1041) | Usually yes | No (grantor reports) |

| Drafting cost | $2,500–$10,000+ | $1,000–$3,000 |

| Trustee | Independent required for full benefits | Grantor can serve |

Common Uses for Irrevocable Trusts

The irrevocable trust is a flexible vehicle that supports a number of specialized estate planning structures. The most frequent variants are summarized below.

Medicaid Asset Protection Trust (MAPT)

Shields assets from the Medicaid spend-down requirement after the five-year lookback period, preserving wealth for heirs while qualifying for long-term care benefits.

Irrevocable Life Insurance Trust (ILIT)

Owns a life insurance policy on the grantor's life so death benefits are excluded from the taxable estate under IRC §2042, saving up to 40% in federal estate tax.

Special Needs Trust (SNT)

Provides for a disabled beneficiary without disqualifying them from means-tested government benefits like SSI and Medicaid.

Charitable Remainder Trust (CRT)

Generates a lifetime income stream, provides an immediate income tax deduction, and benefits a named charity at termination under IRC §664.

Dynasty Trust

Holds wealth across multiple generations, leveraging generation-skipping transfer tax exemption to avoid estate tax at each generational handoff.

Spousal Lifetime Access Trust (SLAT)

An irrevocable gift trust for the benefit of the grantor's spouse, indirectly providing the grantor continued access to the assets while removing them from the estate.

Key Components of an Irrevocable Trust

Every well-drafted irrevocable trust contains the same essential clauses, regardless of the specific planning purpose.

Grantor Identification

Full legal name, address, and declaration of intent to create an irrevocable trust.

Trustee Appointment

Independent trustee with no beneficial interest; successor trustees named in order of succession.

Beneficiary Designations

Current income beneficiaries, remainder beneficiaries, and contingent beneficiaries clearly identified.

Distribution Standards

HEMS (health, education, maintenance, support) or fully discretionary standards governing trustee distributions.

Spendthrift Clause

UTC §502 spendthrift provision protecting beneficiary interests from creditors and voluntary alienation.

Trust Protector Powers

Optional independent fiduciary with authority to modify administrative provisions in changed circumstances.

Tax Provisions

Grantor trust elections under IRC §§671-679, GST allocations, and instructions for separate EIN and Form 1041 filings.

Funding Schedule

Schedule A listing assets transferred into the trust at inception and procedures for subsequent contributions.

How to Establish an Irrevocable Trust

Because the decision to create an irrevocable trust is effectively permanent, the formation process matters as much as the document itself. Follow the six steps below to keep the planning intact.

Define the purpose

Decide whether the trust is for Medicaid planning, estate tax reduction, asset protection, life insurance ownership, or charitable giving. The purpose drives every drafting decision that follows.

Select an independent trustee

Choose a family member, attorney, or corporate fiduciary with no personal interest in the trust. Avoid naming the grantor or the grantor's spouse unless using a specialized DAPT structure.

Draft the trust agreement

Include spendthrift provisions, HEMS or discretionary distribution standards, GST tax allocation, and grantor-trust elections if desired. UTC compliance is essential in adopting states.

Execute with formalities

Sign before a notary public; some states require witness signatures as well. Florida requires two witnesses for trusts containing testamentary distributions under Fla. Stat. §736.0403.

Obtain a federal EIN

Non-grantor irrevocable trusts are separate taxpayers and must obtain an employer identification number from the IRS via Form SS-4 before funding.

Fund the trust

Re-title assets into the name of the trustee. Real estate requires recorded deeds, securities require broker re-titling, and bank accounts must be reopened in the trust's name. Funding is what makes the trust operational — an unfunded trust is an empty shell.

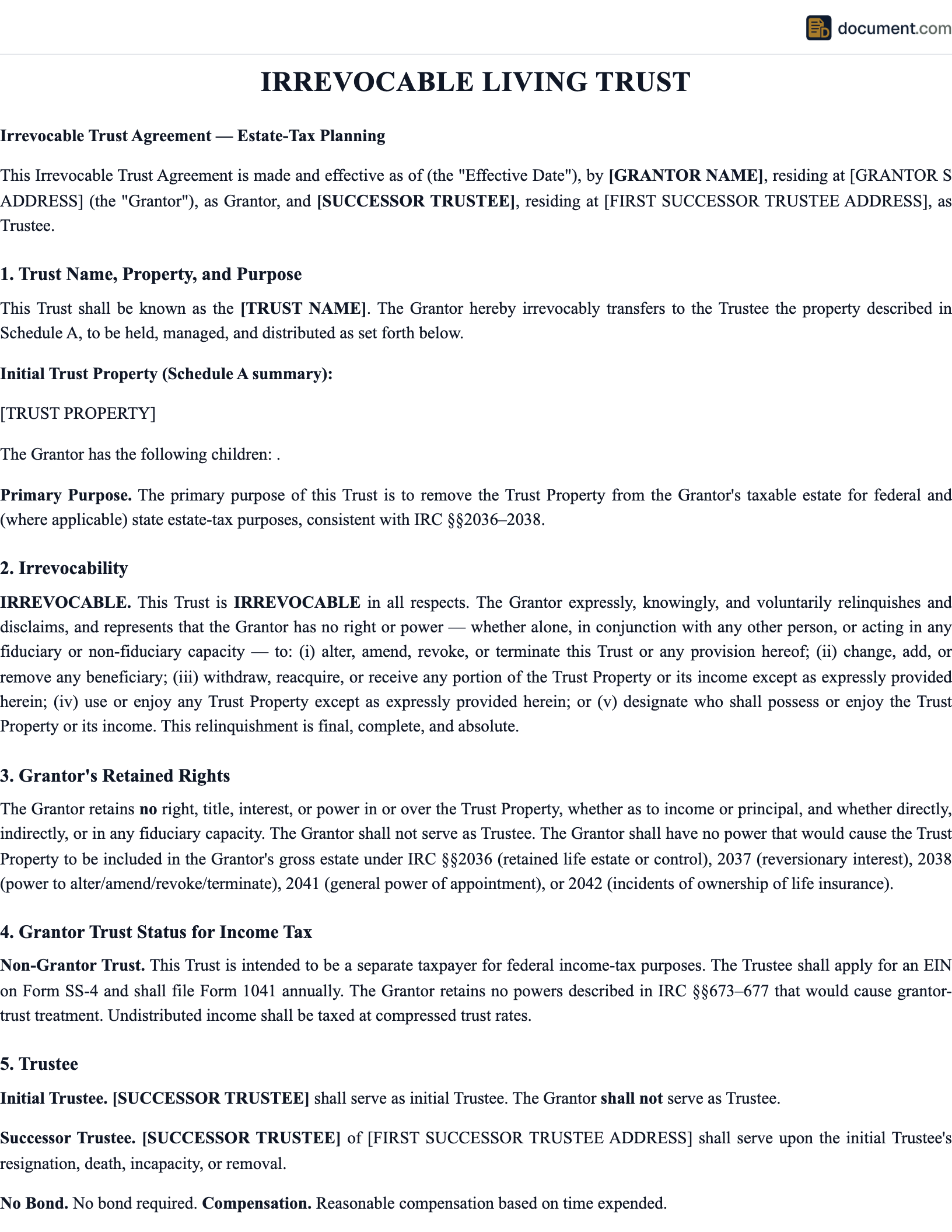

Form Preview

Below is a structural shell of a typical irrevocable trust agreement. Your final document will be expanded with the specific tax, distribution, and trustee provisions that match your planning purpose.

Irrevocable Living Trust Agreement

of [Grantor Name]

This Irrevocable Living Trust Agreement is made this ______ day of __________, 20___, by and between [Grantor], as Grantor, and [Trustee], as Trustee.

Article I — Irrevocability. This trust is irrevocable. The Grantor expressly waives any right to alter, amend, revoke, or terminate this Agreement in whole or in part.

Article II — Trust Property. The Grantor hereby transfers to the Trustee the property listed in Schedule A, to be held in trust for the benefit of the beneficiaries herein named.

Article III — Beneficiaries. The primary beneficiaries of this trust are [Beneficiary Names].

Article IV — Distributions. The Trustee may distribute income and principal to the beneficiaries for their health, education, maintenance, and support (HEMS).

Article V — Spendthrift Provision. No beneficiary may assign, pledge, or otherwise transfer any interest in this trust, and no creditor may reach any beneficiary's interest.

_____________________________ Grantor

_____________________________ Trustee

Sample Clause Language

Representative language for the three clauses that anchor every irrevocable trust: irrevocability, distribution standard, and spendthrift protection.

Irrevocability Declaration

"The Grantor acknowledges that this trust is irrevocable and that no provision hereof may be amended, modified, or revoked by the Grantor, whether acting alone or in conjunction with any other person, except as specifically permitted under applicable state law."

HEMS Distribution Standard

"The Trustee shall distribute so much of the net income and principal of the trust as the Trustee, in its sole discretion, deems necessary or advisable for the health, education, maintenance, and support of the beneficiaries in their accustomed manner of living."

Spendthrift Clause

"To the maximum extent permitted by law, no interest of any beneficiary in the income or principal of this trust shall be subject to assignment, anticipation, or attachment by any creditor or spouse of the beneficiary."

Plan before you fund

Funding triggers the Medicaid five-year lookback under 42 U.S.C. §1396p and the federal gift tax under IRC §2511. Confirm with counsel that the trust structure, trustee selection, and asset transfer sequence achieve your intended tax and protection results before titling assets into the trust.

Frequently Asked Questions

Common questions about irrevocable trusts, Medicaid planning, ILITs, grantor trust taxation, and the limited paths to modify an irrevocable instrument.

Official Resources

Authoritative sources for irrevocable trust law, federal tax treatment, and Medicaid lookback rules.

IRS - Abusive Trust Tax Evasion Schemes

IRS guidance on legitimate vs. abusive irrevocable trust structures

IRS Form 1041 (Trust Income Tax Return)

Federal income tax return for non-grantor irrevocable trusts

Uniform Trust Code (Uniform Law Commission)

Official text and adoption status for the UTC, including modification rules under §§411-416

Medicaid.gov - Transfer of Asset Rules

Federal Medicaid eligibility and lookback rules for asset transfers

42 U.S.C. §1396p - Medicaid Lookback Statute

Statutory text of the five-year transfer-of-asset rule

ABA Real Property, Trust and Estate Section

American Bar Association resources on irrevocable trust drafting and administration

Create your Irrevocable Trust in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.