What Is a Purchase Agreement?

A purchase agreement is the written contract that fixes the terms of a sale before closing. It identifies the buyer and seller, describes the property or assets, states the price and payment structure, sets the contingencies that allow either party to walk, fixes the closing date, and allocates closing costs and risk of loss. The agreement is the predicate document; the deed (real estate) or bill of sale (personal property) is the closing instrument that actually transfers title. Both must exist to complete a transaction, and confusing the two is the most common documentary mistake in private-party sales.

The legal regime depends on what is being sold. Real-estate sales fall under common law plus state real-property statutes: the Statute of Frauds (every state requires a writing for any conveyance of an interest in land), the recording acts (race, notice, or race-notice depending on state), the marketable-title doctrine, the doctrine of equitable conversion (risk of loss transfers to buyer on contract execution in 27 states under the Massachusetts rule, remains with seller until closing in the rest under the Uniform Vendor and Purchaser Risk Act). Sales of goods over $500 fall under Article 2 of the Uniform Commercial Code, codified in every state except Louisiana. UCC § 2-201 requires a writing signed by the party against whom enforcement is sought; UCC § 2-204 permits enforceable contracts with open terms filled by gap-fillers in §§ 2-305 through 2-310.

The names are interchangeable. "Purchase agreement," "purchase and sale agreement," "PSA," "real estate contract," and "buy-sell agreement" describe the same document in residential real estate. "Sales contract" and "asset purchase agreement" are more common in commercial and business contexts. Use the term your state's form-of-contract conventions favor (Texas TREC One to Four Family Residential Contract, California Residential Purchase Agreement and Joint Escrow Instructions C.A.R. Form RPA, New York Residential Contract of Sale prepared by NY State Bar Association) and the underlying document is identical in function.

Real-estate purchase vs personal-property sale (UCC vs common law)

The two regimes diverge on more than statute number. UCC implies a warranty of merchantability for any sale by a merchant (§ 2-314) and a warranty of fitness for particular purpose where the seller knows the buyer's intended use (§ 2-315). Both can be disclaimed only with conspicuous language and the magic words "merchantability" or "as is" (§ 2-316). Real-estate sales carry no implied warranty of habitability except for new-construction homes in roughly 40 states (Petersen v. Hubschman Construction, 76 Ill. 2d 31 (1979); Conklin v. Hurley, 428 So. 2d 654 (Fla. 1983)). Resales are presumptively caveat emptor subject to disclosure-act override (most states require completion of a residential property condition disclosure under statutes like California Civil Code § 1102, Texas Property Code § 5.008, Florida Stat. § 689.25). UCC permits contract modification without consideration if in good faith (§ 2-209(1)); real-estate modifications require either consideration or the writing's own integration clause.

Statutory deeds and recording

At closing, real-estate purchase agreements are performed by delivery of a deed, not by the agreement itself. Deed types convey different warranties. General warranty deed (covenant of seisin, right to convey, against encumbrances, quiet enjoyment, warranty, further assurances) protects the buyer against any title defect arising at any time, regardless of when. Special or limited warranty deed warrants only against defects arising during the seller's ownership. Quitclaim deed conveys whatever interest the seller has, with no warranties; useful for intra-family transfers and clearing clouded titles. Bargain-and-sale deed implies title but warrants nothing. Texas, California, and most western states default to grant deeds with limited warranties; New York and most northeastern states default to bargain-and-sale with covenants against grantor's acts. Recording in the county where the property sits perfects the buyer's rights against subsequent purchasers under the state recording act and triggers the statute of limitations on title-defect claims; failure to record is the most common cause of title disputes decades later.

Legal Protection

Binding contract that protects both buyer and seller throughout the transaction

Clear Terms

Defines price, contingencies, timelines, and obligations so there are no surprises

Enforceable Rights

Gives both parties legal recourse if the other fails to perform their obligations

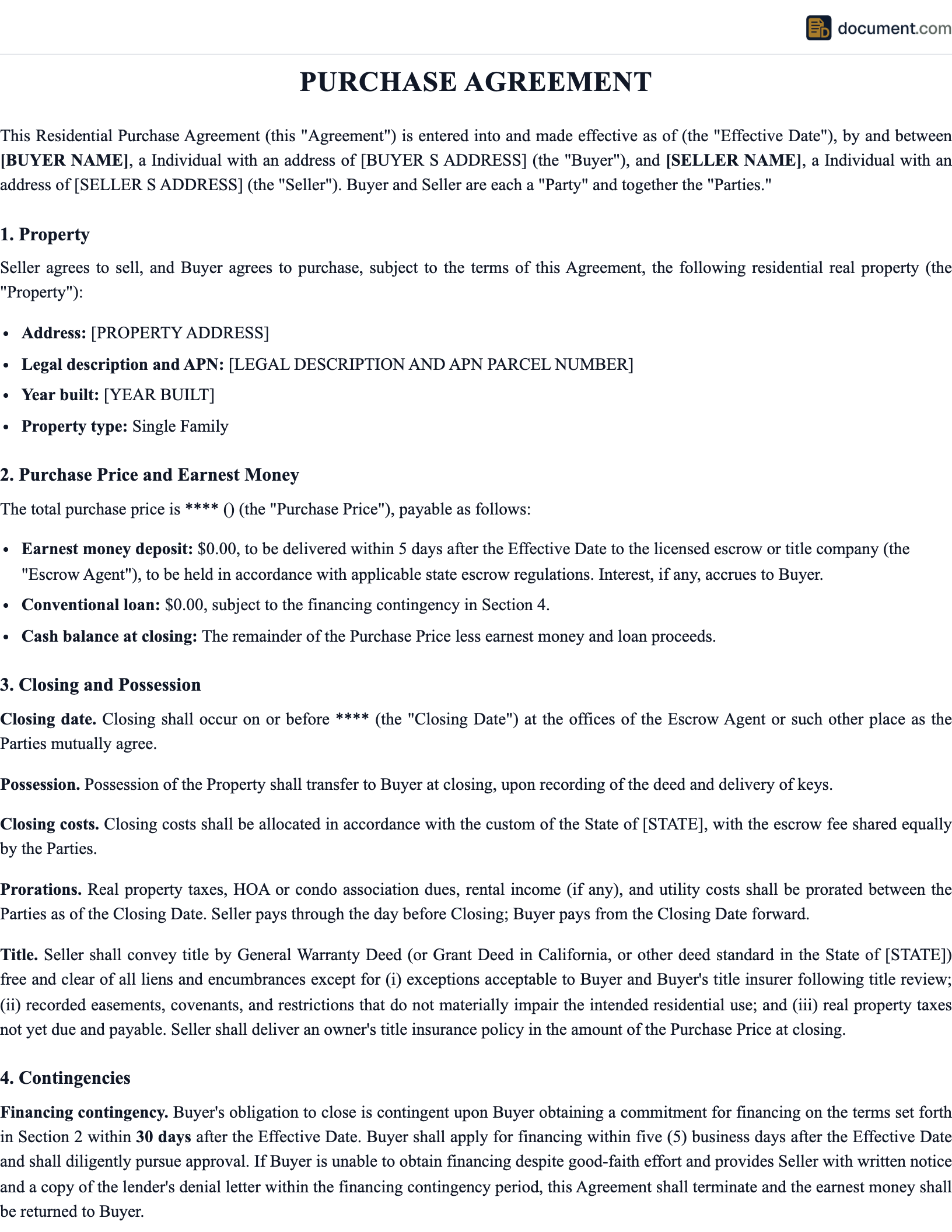

Purchase Agreement Form Preview

Below is a visual preview of the sections and fields included in a standard purchase agreement. This mockup illustrates the structure and level of detail our templates provide. Your completed document will be fully formatted, professionally styled, and customized for your specific transaction type and state.

Purchase Agreement

Contract for the Sale and Purchase of Property

Section 1: Party Information

Buyer

Seller

Section 2: Property / Item Description

Section 3: Purchase Price & Payment Terms

Section 4: Earnest Money / Deposit

Section 5: Contingencies

Section 6: Closing Date & Location

Section 7: Representations & Warranties

The Seller represents and warrants that:

- Seller has good and marketable title to the property, free of all liens and encumbrances except as disclosed herein.

- There are no pending or threatened legal actions affecting the property.

- All systems (plumbing, electrical, HVAC) are in working order as of the date of this agreement.

- Seller has disclosed all known material defects to the Buyer.

- The property complies with all applicable zoning ordinances and building codes.

Section 8: Signatures

Buyer Signature

Seller Signature

Types of Purchase Agreements

Pick the template that matches the asset and the regulatory regime. Residential real estate uses state-specific contracts conforming to local disclosure law. Commercial real estate adds environmental due diligence (ASTM E1527-21 Phase I), tenant estoppels, and SNDA negotiations. Business asset purchases trigger bulk-sale notice obligations in some states and HSR Act review above $119.5 million for 2024. Stock purchases run through corporate or LLC operating-agreement consent provisions. Vehicle purchases trigger state title-transfer and odometer disclosure requirements.

Residential Real Estate Purchase Agreement

Single-family homes, condos, townhouses, and multi-family properties

Commercial Real Estate Purchase Agreement

Office buildings, retail spaces, warehouses, and mixed-use properties

Land / Vacant Lot Purchase Agreement

Undeveloped land, lots, acreage, and raw parcels

Business Purchase Purchase Agreement

Buying or selling an entire business including assets and goodwill

Asset Purchase Purchase Agreement

Specific business assets, equipment, inventory, or intellectual property

FSBO - For Sale By Owner Purchase Agreement

Residential sales without a real estate agent or broker

Stock / Equity Purchase Purchase Agreement

Buying or selling ownership shares or membership interests

Automobile Purchase Purchase Agreement

Private party vehicle purchases with detailed terms and financing

Addendum Purchase Agreement

Attach additional terms or conditions to an existing purchase agreement without rewriting it

Amendment Purchase Agreement

Modify specific terms of an executed purchase agreement such as price, closing date, or contingencies

Farm Purchase Agreement

Purchase agreement for farmland, ranches, or agricultural property including equipment and livestock

How to Write a Purchase Agreement: A 10-Step Guide

A residential real-estate purchase agreement has ten working parts. Work through them in order. Each clause should be specific enough that a stranger reading the agreement could perform the contract without picking up the phone. Use numbers, dates, and proper-noun parties; avoid "reasonable," "timely," and "the parties" without antecedent.

Real-estate license and broker requirements

Real-estate license law (state Real Estate Commission Acts) governs who may negotiate the agreement on behalf of a third party for compensation. Five states require an attorney to handle the closing of every residential real-estate transaction: Connecticut, Delaware, Georgia, Massachusetts, and South Carolina. New Jersey and New York provide a 3-day attorney review window during which counsel may modify or cancel without penalty. Alabama, North Carolina, and Vermont require attorney participation in title work. FSBO (for sale by owner) sales avoid the listing commission but still implicate licensing law if a buyer's agent is involved; the seller must pay a stated cooperation fee to the buyer's broker or accept full commission cost. Brokers hold earnest money in trust accounts under state license law (California Bus. and Prof. Code § 10145, Texas TREC Rule 535.146, Florida § 475.25); commingling broker funds with trust deposits is grounds for license revocation.

RESPA and TRID timing constraints

Federally related mortgage loans (defined broadly under RESPA, 12 U.S.C. § 2602, to include almost every residential mortgage) trigger the TILA-RESPA Integrated Disclosure rule (12 C.F.R. § 1026.19). The lender must deliver a Loan Estimate within 3 business days of application (12 C.F.R. § 1026.19(e)) and a Closing Disclosure at least 3 business days before closing (§ 1026.19(f)). Material changes to the Closing Disclosure (APR change of more than 0.125 percent fixed or 0.25 percent adjustable, loan-product change, or addition of a prepayment penalty) restart the 3-day clock. The closing date in the purchase agreement must build in this 3-day buffer. RESPA Section 8 (12 U.S.C. § 2607) prohibits kickbacks and unearned-fee splits between settlement-service providers; this affects how the buyer's and seller's agents structure any title-company or warranty-company recommendations.

Identify the Parties

Begin by clearly identifying the buyer and seller using their full legal names. If a party is an individual, use their name as it appears on their government-issued ID. If a party is a business entity, use the exact legal name of the entity (LLC, Corporation, Partnership) along with the state in which it is organized and the name of the authorized representative signing on its behalf.

Include the current mailing address, phone number, and email address for each party. For real estate transactions, some states also require the parties' marital status, as a spouse may have community property rights or homestead rights that affect the sale. If multiple buyers or sellers are involved, each person must be named individually.

Tip: Always verify the legal names against official documents. A misspelled name can create title issues and delays at closing.

Describe the Property or Assets

Provide a detailed description of what is being sold. For real estate, this includes the street address, legal description (lot, block, subdivision, or metes and bounds), county, and parcel or tax ID number. A legal description obtained from the deed or title company is more precise than a street address and is preferred for the agreement.

For business purchases, list all assets included in the sale: equipment, inventory, intellectual property, customer lists, goodwill, trade names, and contracts being assigned. For vehicle sales, include the year, make, model, VIN, odometer reading, and color. The more specific you are, the less room there is for disputes about what was included in the sale.

Equally important is specifying what is excluded from the sale. In a home purchase, for example, the seller may want to exclude a custom chandelier or built-in shelving. In a business sale, certain assets or liabilities may be excluded. List exclusions clearly to avoid misunderstandings.

Set the Purchase Price and Payment Terms

State the total purchase price in both numerical and written form to avoid ambiguity. Specify the payment structure: will the buyer pay the full amount in cash at closing, finance the purchase with a mortgage or loan, use seller financing, or pay in installments? If financing is involved, include the type of loan (conventional, FHA, VA), the expected interest rate range, and the loan term.

Break down the payment into components: earnest money deposit, additional down payment at closing, and the financed amount. Specify the acceptable payment methods for the closing payment (wire transfer, certified check, cashier's check). If the seller is providing financing, include the note terms, interest rate, monthly payment amount, and any balloon payment provisions.

Warning: Never accept personal checks for real estate closings. Wire fraud is increasingly common; always verify wiring instructions by phone using a known number, not the number in an email.

Define the Earnest Money Deposit

State the deposit amount in dollars (typically 1 to 3 percent of purchase price; 5 to 10 percent in competitive luxury markets), the delivery deadline (1 to 3 business days after the effective date is standard), and the name of the escrow holder. The escrow holder must be a neutral third party: title company, real-estate brokerage trust account, or attorney IOLTA account. State license law dictates the procedure: California Business and Professions Code § 10145 requires brokers to deposit funds in a non-interest-bearing trust account within three business days; Texas TREC Rule 535.146 and Florida Stat. § 475.25 impose similar fiduciary obligations. Commingling broker funds with trust deposits is grounds for license revocation.

Define release conditions with precision. Funds are typically returned to the buyer on cancellation during any active contingency period and applied to the down payment or closing costs at closing. On buyer default outside contingencies, the contract's liquidated-damages clause governs forfeiture. Several states cap residential liquidated damages: California Civil Code § 1675 limits residential liquidated damages to 3 percent of the purchase price absent a specific finding of reasonableness; Florida courts apply a two-part test (the amount must approximate anticipated damages and the actual damages must be difficult to determine). Where either party disputes release, the title company will hold pending interpleader or written mutual instructions; the typical resolution time is 30 to 90 days.

Include Contingencies and Conditions

Five core contingencies appear in nearly every residential purchase agreement, each with a defined window. Inspection contingency: 7 to 14 days for general home, termite, radon, mold, and sewer-lateral inspections (California requires sewer-lateral inspection in many East Bay municipalities; Florida requires four-point inspections for older homes for insurance binding). Financing contingency: 21 to 30 days for loan commitment, with the TRID Closing Disclosure delivered at least 3 business days before closing under 12 C.F.R. § 1026.19(f). Appraisal contingency tied to financing, requiring the property to appraise at or above the contract price. Title contingency of 5 to 10 days after delivery of the title commitment to object to exceptions. Insurance contingency of 5 to 14 days, increasingly material in Florida (Citizens of last resort), California (FAIR Plan), and Louisiana where the homeowners insurance market has tightened sharply since 2022.

Each contingency should specify whether it expires automatically (passive waiver, the default in California Residential Purchase Agreement) or requires affirmative removal in writing (active waiver, common in Texas TREC One to Four Family Residential Contract). Active waiver is the safer drafting choice for buyers because silence does not forfeit the right to walk; passive waiver is the seller-favored default. Each contingency should also state the consequence of non-satisfaction: cancellation with earnest-money refund (most common), automatic extension, or right to renegotiate.

Drafting note:Use calendar days, not business days, unless the contingency explicitly says otherwise; the difference between "10 days" and "10 business days" over a holiday weekend has cost more than one buyer their earnest money.

Specify the Closing Date and Procedures

Set a specific calendar closing date allowing sufficient time for all contingencies to clear, financing to commit, and title work to complete. Residential closings run 30 to 45 days for financed deals, 7 to 14 days for cash. Include the consequences of delay: time-of-the-essence clauses make a missed closing date a default; without that language, courts apply a reasonable cure period (typically 7 to 30 days). Include extension procedures (mutual written agreement, automatic extension on TRID redisclosure, per-diem penalty for unjustified delay).

Identify the closing agent (title company in escrow states like California, Texas, and Arizona; closing attorney in attorney states like Connecticut, Delaware, Georgia, Massachusetts, and South Carolina; either in hybrid states like New York and Illinois) and the closing location. Allocate closing costs by line item: title insurance owner's policy (buyer pays in California, Florida, and most of the West; seller pays in Texas, Pennsylvania, and Ohio, though local custom varies by county); lender's policy (always buyer); transfer tax (varies widely; California county-level documentary transfer tax of $0.55 per $500 plus city add-ons of up to 2.25 percent in San Francisco; New York combined state and city tax of 1 to 3.275 percent; Florida documentary stamp tax of $0.70 per $100 outside Miami-Dade and $0.60 inside); recording fees (county-specific, $50 to $300); survey ($400 to $800); HOA estoppels (capped by statute in some states, e.g., Florida Stat. § 720.30851 caps at $250). Document every allocation; ambiguity defaults to local custom and triggers disputes at the closing table.

Address Representations and Warranties

Representations and warranties are factual statements that survive closing and support a breach-of-contract claim if false. The seller typically represents marketable title (no undisclosed liens, judgments, mechanic's liens, or easements outside of record); compliance with zoning, building codes, and homeowners-association covenants; functioning mechanical systems as of the effective date; full disclosure of known material defects per the state property-condition disclosure act (California Civil Code § 1102; Texas Property Code § 5.008; Florida common-law doctrine of Johnson v. Davis, 480 So. 2d 625 (Fla. 1985), requiring disclosure of material facts not readily observable); no pending or threatened litigation affecting title; and no notices of governmental violations. Survival period for residential reps is typically the statute of limitations on contracts (3 to 6 years in most states; 4 years under California Code of Civil Procedure § 337).

Business and commercial purchase agreements expand the rep set substantially. Asset purchase agreements include reps on financial statements (in accordance with GAAP), tax compliance (including state nexus and local franchise taxes), employment law (no pending charges, ERISA plan compliance, no unfunded pension obligations), environmental (CERCLA and state equivalent compliance, Phase I and II reports clean), intellectual property (full ownership of registered marks and patents, no infringement claims), material contracts (no defaults, no change-of-control triggers without consent), and customer concentration. Survival is heavily negotiated: 12 to 24 months for general reps, statute of limitations or longer for tax and environmental, perpetual for fundamental reps (organization, authority, capitalization). Caps and baskets (typically 0.5 to 1.5 percent of purchase price for the basket, 10 to 20 percent for the cap) limit indemnification exposure.

Include Required Disclosures

Federal law requires lead-based paint disclosure for any residential property built before 1978 (42 U.S.C. § 4852d, 24 C.F.R. § 35.92), including delivery of the EPA pamphlet "Protect Your Family from Lead in Your Home," a signed acknowledgment, and a 10-day opportunity for the buyer to conduct a lead inspection. Failure to comply triggers triple damages plus attorney fees. The Foreign Investment in Real Property Tax Act (FIRPTA, IRC § 1445) requires the buyer to withhold 15 percent of the gross purchase price if the seller is a foreign person, payable to the IRS within 20 days of closing unless an exception or withholding certificate applies.

State disclosure requirements are extensive and vary by jurisdiction. California Civil Code § 1102 requires the Real Estate Transfer Disclosure Statement (TDS), the Natural Hazard Disclosure (Civil Code § 1103), Megan's Law database disclosure, Mello-Roos special-tax district disclosure, supplemental property tax notice, water-conserving plumbing fixture disclosure (Civil Code § 1101.4), and earthquake hazard reports. Texas Property Code § 5.008 requires the Seller's Disclosure Notice. Florida applies Johnson v. Davis common-law disclosure of any material fact not readily observable, plus statutory radon notice (Stat. § 404.056) and coastal-construction zone notice (Stat. § 161.57). New York and roughly a dozen other "caveat emptor" states still require disclosure of latent defects but allow the seller to issue a $500 credit in lieu of completing the property condition disclosure form (NY Real Property Law § 462). HOA documents (CC&Rs, financials, reserve study, current assessments, pending special assessments) are required in every condominium and planned-unit development sale.

Warning:Concealment of a known material defect supports a fraud claim regardless of any "as-is" clause; an as-is sale waives the implied warranty of habitability for new construction but does not insulate the seller from intentional misrepresentation. When in doubt, disclose.

Define Default and Remedies

Define each party's default events with specificity: failure to close by the contract date (subject to time-of-the-essence treatment), failure to deliver marketable title within the title-cure period, failure to make required deposits, breach of any representation or warranty, and refusal to perform any contractual obligation. For each default, state the non-defaulting party's remedies. Buyer-default remedies typically include retention of earnest money as liquidated damages (capped at 3 percent of purchase price for residential property in California under Civil Code § 1675), specific performance (a real-property remedy granted more freely than for goods because of the unique-property presumption), and recovery of attorney fees if the contract so provides.

Seller-default remedies typically include specific performance (forcing the sale), recovery of the earnest-money deposit, and consequential damages including the difference between the contract price and the buyer's replacement-property cost plus carrying costs. The liquidated-damages clause is enforceable only if the amount approximates anticipated harm at the time of contracting and is not punitive (Restatement (Second) of Contracts § 356). Add mandatory mediation as a condition precedent to litigation (California Residential Purchase Agreement makes this default; the prevailing party still recovers fees if the other refused mediation). Arbitration clauses in residential real-estate contracts are enforceable in most states under the Federal Arbitration Act (9 U.S.C. § 1) but are increasingly disfavored by consumer-protection statutes.

Execute the Agreement Properly

Both buyer and seller sign and date the agreement. Spouses of titleholders must sign in community-property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin) and in homestead states (Florida, Texas, Iowa among others) where a spouse holds homestead rights regardless of title. Corporate or LLC sellers sign through an authorized officer or member with a corporate resolution or operating-agreement consent attached. Print the signer's name and capacity below each signature. A "fully executed" agreement means all parties have signed and the agreement has been delivered.

Notarization is not required for the purchase agreement itself but is required for the deed delivered at closing in every state. Electronic signatures on the agreement are valid under the federal ESIGN Act (15 U.S.C. § 7001) and state UETA equivalents adopted in 49 states (New York follows its own ESRA). Five states require attorney participation in residential closings (Connecticut, Delaware, Georgia, Massachusetts, South Carolina); New Jersey and New York provide a 3-day attorney review window during which counsel may modify or cancel without penalty. Deliver the fully executed agreement and earnest money to the escrow agent immediately; delay in delivering earnest money is itself a default in most form contracts.

Drafting note:Wire-fraud schemes targeting real-estate closings have intensified since 2020. The FBI IC3 reports over $446 million in real-estate wire-fraud losses for 2022. Verify wire instructions by phone using a number from the title company's published website, never the number in the wire-instruction email; instructions arriving at the last minute are presumptively suspicious.

Key Components of a Purchase Agreement

Seventeen sections appear in nearly every enforceable residential real-estate purchase agreement. Omit the price, parties, or property description and the contract fails the Statute of Frauds writing requirement. Omit any other section and the gap defaults to state law, local custom, or litigation.

| Component | Description |

|---|---|

| Buyer Information | Full legal name, address, contact details, and marital status of the buyer |

| Seller Information | Full legal name, address, contact details, and marital status of the seller |

| Property Description | Legal description, street address, parcel ID, and included/excluded items |

| Purchase Price | Total price in numbers and words, payment structure, and financing terms |

| Earnest Money | Deposit amount, delivery deadline, escrow agent, and refund conditions |

| Financing Contingency | Loan type, amount, interest rate, and deadline for mortgage approval |

| Inspection Contingency | Inspection period, scope of inspections, and buyer's remedies for defects |

| Appraisal Contingency | Requirement for property to appraise at or above the purchase price |

| Title Requirements | Commitment to deliver clear, marketable title free of liens and encumbrances |

| Closing Date & Location | When and where the closing will occur, with provisions for extensions |

| Closing Costs Allocation | Which party pays for title insurance, transfer taxes, recording fees, and other costs |

| Possession Date | When the buyer takes physical possession (at closing, before, or after) |

| Representations & Warranties | Seller's statements of fact about the property, title, and disclosures |

| Disclosures | Lead paint, property condition, flood zone, HOA, and other required disclosures |

| Default & Remedies | Consequences of breach, including liquidated damages, specific performance, and dispute resolution |

| Prorations & Adjustments | How property taxes, HOA dues, utilities, and rent are split between buyer and seller at closing |

| Signatures & Date | Dated signatures of all parties, with witness or notary lines if required |

Legal Requirements for Purchase Agreements

Federal statute, state real-property law, and local ordinances all apply. The federal layer fixes uniform disclosure and consumer-protection rules; state law sets the operating regime for title, deeds, recording, and licensure; local ordinances add transfer taxes, point-of-sale inspections, and rent-control transfer disclosures. A clause that conflicts with any layer is unenforceable to that extent.

Statute of Frauds

Every state has adopted some version of the English Statute of Frauds (1677). For real property, any contract for the sale of an interest in land must be in writing and signed by the party against whom enforcement is sought. The writing must contain the essential terms: parties, property description sufficient for identification, and price. The doctrine of part performance permits enforcement of an oral land contract in some states where the buyer has paid all or part of the price, taken possession, and made improvements (Hickey v. Green, 14 Mass. App. Ct. 671 (1982)). For sales of goods, UCC § 2-201 requires a writing for any contract over $500, with exceptions for specially manufactured goods (§ 2-201(3)(a)), admitted contracts (§ 2-201(3)(b)), and goods received and accepted (§ 2-201(3)(c)).

Federal requirements

Federal statutes layer on top of state real-property law for any transaction involving a federally related mortgage loan, a foreign seller, or a pre-1978 dwelling.

- TILA-RESPA Integrated Disclosure (TRID), 12 C.F.R. § 1026.19: Federally related mortgage loans require the lender to deliver a Loan Estimate within 3 business days of application and a Closing Disclosure at least 3 business days before closing. Material changes restart the 3-day clock. Build the buffer into the closing date. RESPA Section 8 (12 U.S.C. § 2607) prohibits kickbacks and unearned-fee splits between settlement-service providers; affiliated business arrangements require written disclosure under 24 C.F.R. § 3500.15.

- Lead-Based Paint Disclosure (42 U.S.C. § 4852d, 24 C.F.R. § 35.92): Required for any residential property built before 1978. Seller must deliver the EPA "Protect Your Family from Lead in Your Home" pamphlet, complete and sign the disclosure form (with knowledge of any known lead-paint hazards and any lead-related reports), include the Lead Warning Statement, and give the buyer a 10-day opportunity for inspection. Failure triggers triple damages plus attorney fees under § 4852d(b)(3).

- FIRPTA, IRC § 1445: If the seller is a foreign person (non-US citizen, non-resident alien), the buyer must withhold 15 percent of the gross purchase price (10 percent for personal residences $300,001 to $1,000,000) and remit to the IRS within 20 days of closing. Buyer is liable for the unpaid tax if withholding is omitted. Withholding certificates (IRS Form 8288-B) reduce the withholding but require advance application.

- Fair Housing Act, 42 U.S.C. § 3604: Prohibits refusal to sell or imposing different terms based on race, color, religion, sex (including sexual orientation and gender identity post-Bostock), national origin, familial status, or disability. Civil penalties for first violation up to $25,597 (2024) under 24 C.F.R. § 180.671. Steering and blockbusting are separate violations under § 3604(c).

- HSR Act premerger notification, 15 U.S.C. § 18a: Business asset and stock purchases above the size-of-transaction threshold ($119.5 million for 2024, indexed annually) require pre-closing notification to the FTC and DOJ Antitrust Division and observance of the 30-day waiting period (15 days for cash tender offers and bankruptcy sales).

- ESIGN Act and UETA: 15 U.S.C. § 7001 and the Uniform Electronic Transactions Act adopted in 49 states establish that electronic signatures on purchase agreements are valid and enforceable provided all parties consent. New York follows ESRA. Notarized closing documents (deeds, mortgages) require remote online notarization (RON) authorization, available in 44 states post-COVID.

Marketable title and the recording acts

Every purchase agreement carries an implied obligation that the seller convey marketable title: title free of reasonable doubt, free from any encumbrance not disclosed in the contract, and defensible against attack. Encumbrances that defeat marketability include undisclosed mortgages, judgment liens, mechanic's liens, easements not of record, restrictive covenants, encroachments, and adverse-possession claims. The title commitment from the title insurer (issued before closing) identifies all matters affecting title; the buyer typically has 5 to 10 days to object to exceptions. Recording the deed in the county where the property sits perfects the buyer's rights against subsequent purchasers under the state's recording act. Race statutes (North Carolina, Louisiana) protect the first to record. Notice statutes (most states) protect the bona fide purchaser without notice. Race-notice statutes (California, New York) protect the BFP who records first. Failure to record is the leading cause of title disputes that surface decades after closing.

State-by-state variations

- Property condition disclosures: California Civil Code § 1102 (Real Estate Transfer Disclosure Statement plus Natural Hazard Disclosure under § 1103). Texas Property Code § 5.008 (Seller's Disclosure Notice). Florida applies Johnson v. Davis, 480 So. 2d 625 (1985), common-law disclosure of any material fact not readily observable. New York Real Property Law § 462 permits a $500 credit in lieu of the property condition disclosure form.

- Attorney review periods: New Jersey (3 days under R. 1:21-1A and the New Jersey State Bar Association resolution), New York (3 days, varies by county custom), Illinois (5 to 10 business days, custom-driven). During the window, counsel may modify or cancel without penalty. Five states require attorney involvement at closing for residential transactions: Connecticut, Delaware, Georgia, Massachusetts, South Carolina.

- Transfer taxes: California county documentary transfer tax of $0.55 per $500 plus city add-ons (San Francisco up to 2.25 percent, Los Angeles 0.45 percent plus Measure ULA mansion tax of 4 to 5.5 percent on sales above $5 million). New York state and city combined 1 to 3.275 percent. Florida documentary stamp tax of $0.70 per $100 outside Miami-Dade and $0.60 inside. Pennsylvania 1 percent state plus 1 percent local. Thirteen states impose no transfer tax (Alaska, Arizona, Idaho, Indiana, Kansas, Louisiana, Mississippi, Missouri, Montana, New Mexico, North Dakota, Texas, Utah, Wyoming).

- Community property and homestead spousal joinder: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin require spousal signature on transfers of community real property. Florida (Art. X § 4 of state constitution) requires spousal joinder on any transfer of homestead property regardless of title; failure voids the conveyance. Texas requires spousal joinder on homestead transfers under Family Code § 5.001. Iowa applies the Mansfield rule requiring joinder on any homestead transfer.

- Closing practice: Escrow states (California, Arizona, Nevada, Oregon, Washington, Idaho, Hawaii, New Mexico, Utah, parts of Texas) use a neutral third party (escrow officer at title company). Attorney states (Connecticut, Delaware, Georgia, Massachusetts, South Carolina, North Carolina, Vermont, Mississippi) require attorney participation at closing. Hybrid states (New York, New Jersey, Illinois, Florida, Pennsylvania) permit either model with local custom dictating.

Common Purchase Agreement Contingencies

Contingencies are conditions precedent: the obligation to close arises only if the condition is satisfied or waived. The six contingencies below appear in nearly every residential purchase agreement. Each should specify the period in calendar days, the form of waiver (active written removal vs passive expiration), and the consequence of non-satisfaction (cancellation with refund is the standard).

Waiving contingencies (cash buyers, escalating-bid markets) shifts the entire risk of financing, appraisal, inspection findings, and title defects onto the buyer; the earnest money is at risk on any default outside the remaining contingencies. In tight markets, partial waivers (waiving the appraisal contingency but retaining the financing contingency, for example) are the negotiation ground.

Financing Contingency

Allows the buyer to cancel if they are unable to secure mortgage approval within a specified timeframe (typically 21 to 30 days). This is the most common contingency and protects the buyer from being forced to purchase a property they cannot finance. Without this contingency, the buyer risks losing their earnest money if their loan falls through.

Inspection Contingency

Gives the buyer a specified period (usually 7 to 14 days) to have the property professionally inspected. If the inspection reveals significant defects, the buyer can negotiate repairs, request a price reduction, or cancel the agreement. This contingency protects buyers from purchasing a property with hidden structural, electrical, plumbing, or environmental issues.

Appraisal Contingency

Requires the property to appraise at or above the purchase price as determined by a licensed appraiser, typically ordered by the buyer's lender. If the appraisal comes in below the purchase price, the buyer can renegotiate, make up the difference in cash, or cancel the agreement. Lenders will not finance more than the appraised value, making this contingency essential for financed purchases.

Title Contingency

Requires the seller to deliver clear, marketable title: title free of outstanding liens, judgments, easements, or other encumbrances that were not disclosed. A title company or attorney conducts the search and issues a title commitment showing exceptions. The buyer typically has 5 to 10 days after delivery of the commitment to object. If the seller cannot cure within the cure period, the buyer may cancel and receive the deposit back. Title insurance owner's policy (premium 0.5 to 1 percent of price as a one-time payment) protects against undiscovered claims that surface after closing; lender's policy is required by every institutional lender.

Home Sale Contingency

Makes the purchase contingent on the buyer selling their existing home by a specified date. This protects buyers from owning two properties simultaneously. Sellers often resist this contingency because it introduces uncertainty, and some markets make it impractical. A "kick-out clause" may allow the seller to continue marketing the property and give the buyer a short period to waive the contingency if another offer comes in.

Insurance Contingency

Allows the buyer to cancel if they are unable to obtain acceptable homeowner's insurance at a reasonable cost. This is increasingly relevant in areas prone to natural disasters (floods, hurricanes, wildfires) where insurance may be expensive, limited, or unavailable. Lenders require homeowner's insurance, so the buyer cannot close without it. This contingency ensures the buyer is not locked into a purchase they cannot insure.

Purchase Agreement vs Other Documents

Four adjacent documents get confused with the purchase agreement. The bill of sale records that transfer happened (signed at or after closing). The letter of intent records the parties' preliminary framework before negotiations crystallize (binding only as to confidentiality, exclusivity, and similar express provisions; otherwise non-binding). The option to purchase obligates only the seller to perform if the buyer chooses to exercise (common in lease-options and developer land assemblages). Knowing which document does which work prevents drafting one when another is required.

Purchase Agreement vs Bill of Sale

Purchase Agreement

- - Signed before the sale closes

- - Outlines terms, contingencies, and conditions

- - Creates a binding obligation to perform

- - Governs the process from offer to closing

- - Used for complex, high-value transactions

Bill of Sale

- - Signed at or after the transaction

- - Records that the sale occurred

- - Serves as a receipt and proof of transfer

- - Documents the completed exchange

- - Used for personal property, vehicles, goods

When to use both: In a vehicle purchase with financing or installment payments, you may use a purchase agreement to set the terms and a bill of sale at closing to document the transfer. In real estate, the purchase agreement governs the deal and a deed (not a bill of sale) transfers title.

Purchase Agreement vs Letter of Intent (LOI)

Purchase Agreement

- - Legally binding and enforceable

- - Contains all final negotiated terms

- - Signed when both parties are ready to commit

- - Includes detailed contingencies and provisions

Letter of Intent

- - Generally non-binding (except certain clauses)

- - Outlines proposed terms for negotiation

- - Signed early in the process as a framework

- - High-level overview without full legal detail

When to use both: LOIs are commonly used in business acquisitions and commercial real estate. The parties sign an LOI to agree on basic terms, then negotiate the detailed purchase agreement. The LOI may include binding exclusivity and confidentiality clauses while the purchase agreement is being drafted.

Purchase Agreement vs Option to Purchase

Purchase Agreement

- - Both parties are obligated to perform

- - Buyer must buy and seller must sell

- - Mutual commitment with defined closing date

- - Default by either party has consequences

Option to Purchase

- - Only the seller is obligated; buyer has a choice

- - Buyer pays for the right (option fee) to buy later

- - Buyer can exercise or let the option expire

- - Common in lease-to-own and land banking

Key difference: An option gives the buyer the right but not the obligation to buy, while a purchase agreement creates a mutual obligation. Options are common in lease-option (rent-to-own) arrangements and developer land assemblages where the buyer needs time to secure zoning or permits before committing.

Purchase Agreement vs Sales Contract

Purchase Agreement

- - Term commonly used in real estate

- - Emphasizes the buyer's perspective

- - May include real estate-specific provisions

- - Typically a single, specific transaction

Sales Contract

- - Term commonly used in commercial/goods sales

- - Emphasizes the seller's perspective

- - May be governed by UCC for goods

- - Can cover one-time or ongoing sales

In practice:These terms are largely interchangeable. The name used often depends on industry convention and regional preference rather than any legal distinction. In real estate, "purchase agreement" or "purchase and sale agreement" is standard. For goods and commercial transactions, "sales contract" may be more common.

Sample Purchase Agreement

Below is a condensed preview of our residential real estate purchase agreement template. This sample shows the structure, language, and sections included in our attorney-reviewed documents. Your completed agreement will be fully customized for your transaction type, state, and specific terms.

PURCHASE AND SALE AGREEMENT

Residential Real Estate

This Purchase and Sale Agreement ("Agreement") is entered into as of[Date], by and between:

SELLER:

Name: [Seller Full Legal Name]

Address: [Seller Mailing Address]

Phone: [Phone]Email: [Email]

BUYER:

Name: [Buyer Full Legal Name]

Address: [Buyer Mailing Address]

Phone: [Phone]Email: [Email]

1. PROPERTY DESCRIPTION

Seller agrees to sell and convey, and Buyer agrees to purchase, the real property located at[Street Address], City of [City], County of [County], State of [State], together with all improvements, fixtures, and appurtenances thereto, legally described as:[Legal Description](the "Property").

2. PURCHASE PRICE

The total purchase price for the Property shall be $[Amount]([Amount in Words] Dollars), payable as follows:

- Earnest Money Deposit: $[Amount]

- Additional Down Payment at Closing: $[Amount]

- Balance Financed by Mortgage: $[Amount]

3. EARNEST MONEY

Within [3] business days of the Effective Date, Buyer shall deposit earnest money in the amount of $[Amount] with[Escrow Agent / Title Company]. Said deposit shall be applied toward the purchase price at closing or refunded to Buyer in accordance with the contingency provisions herein.

4. FINANCING CONTINGENCY

This Agreement is contingent upon Buyer obtaining a commitment for a[Conventional/FHA/VA]mortgage loan in the amount of $[Amount]at a fixed/adjustable interest rate not to exceed [%]per annum, for a term of [30] years. Buyer shall apply for such financing within [5]business days of the Effective Date and shall diligently pursue approval...

5. INSPECTION CONTINGENCY

Buyer shall have [10]calendar days from the Effective Date to conduct or have conducted, at Buyer's expense, inspections of the Property including but not limited to: general home inspection, termite/pest inspection, radon testing, mold testing, and environmental assessment. Seller shall provide reasonable access to the Property for such inspections...

6. CLOSING

Closing shall take place on or before [Date]at the offices of [Title Company / Attorney], or at such other time and place as the parties may mutually agree in writing. At closing, Seller shall deliver a general warranty deed conveying the Property to Buyer, free and clear of all liens and encumbrances except as otherwise provided herein...

7. REPRESENTATIONS AND WARRANTIES

Seller represents and warrants that: (a) Seller has good and marketable title to the Property; (b) there are no pending or threatened actions, suits, or proceedings affecting the Property; (c) all mechanical systems are in working order; (d) Seller has disclosed all known material defects; (e) there are no violations of building codes, zoning ordinances, or restrictive covenants...

8. DEFAULT AND REMEDIES

If Buyer defaults under this Agreement, Seller's sole remedy shall be to retain the earnest money deposit as liquidated damages. If Seller defaults, Buyer may (a) seek specific performance, (b) terminate this Agreement and recover the earnest money deposit, or (c) pursue any other remedy available at law or in equity...

Frequently Asked Questions

Find answers to common questions about purchase agreements, contract terms, contingencies, and the process of buying and selling property.

Official Resources

For additional information on purchase agreement requirements, real estate regulations, and consumer protections, consult these official government and industry resources.

HUD - Buying a Home

U.S. Department of Housing and Urban Development home buying guide

CFPB - Owning a Home

Consumer Financial Protection Bureau tools and resources for homebuyers

FTC - Business Purchase Guides

Federal Trade Commission resources for business buyers and sellers

CFPB - RESPA Information

Learn about the Real Estate Settlement Procedures Act and your rights

EPA - Lead Paint Disclosure

Environmental Protection Agency lead-based paint information for homebuyers

NAR - Research & Statistics

National Association of Realtors real estate market data and research

ALTA - Title Insurance Info

American Land Title Association consumer resources on title insurance

SBA - Buy an Existing Business

Small Business Administration guide to purchasing an existing business

Create your Purchase Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.