What Is a Residential Purchase Agreement?

A residential purchase agreement (also called a real estate contract, home purchase contract, or contract of sale) is a legally binding document between a buyer and seller that outlines all terms and conditions for the sale of a residential property. This is the single most important document in any home purchase — it defines the purchase price, earnest money deposit, contingencies, closing date, and the rights and obligations of both parties throughout the transaction.

Unlike a simple bill of sale that records a completed transaction, a purchase agreement is a forward-looking contract that governs the entire period from offer acceptance through closing. It establishes the legal framework for home inspections, appraisals, mortgage financing, title searches, and the eventual transfer of ownership. If either party fails to meet their obligations under the agreement, the other party has legal remedies including specific performance (forcing the sale to proceed) or monetary damages.

Every state has different requirements for residential real estate contracts. Some states require attorney involvement in the closing process, others mandate specific disclosure forms, and transfer tax rates vary dramatically. Our state-specific templates ensure your purchase agreement complies with local laws and includes all required provisions for your jurisdiction.

Legally Binding

Enforceable contract that protects both buyer and seller throughout the transaction

Contingency Protection

Built-in safeguards for financing, inspection, and appraisal issues

State-Compliant

Tailored to meet your state's specific real estate laws and requirements

Residential Purchase Agreement by State

Each state has unique requirements for residential real estate transactions — from mandatory attorney involvement and specific disclosure forms to varying transfer tax rates and closing customs. Select your state below for a purchase agreement template that meets your jurisdiction's specific legal requirements.

The Home Buying Process

Understanding where the purchase agreement fits into the overall home buying process helps you prepare for each step and avoid costly mistakes. Here is a comprehensive overview of the residential real estate transaction from start to finish.

Get Pre-Approved for a Mortgage

Before house hunting, obtain a mortgage pre-approval letter from your lender. This tells you exactly how much you can afford and shows sellers you are a serious, qualified buyer. The pre-approval process involves a credit check, income verification, and review of your debt-to-income ratio. Most pre-approval letters are valid for 60-90 days. Having a pre-approval in hand strengthens your offer significantly — many sellers will not even consider offers without one.

Find a Property and Make an Offer

Work with a buyer's agent to identify suitable properties. When you find the right home, your agent will help you draft and submit a purchase offer, which includes your proposed price, earnest money amount, desired closing date, and any contingencies. In a competitive market, you may need to act quickly and consider strategies like escalation clauses or waiving certain contingencies (though this carries risk).

Negotiate and Sign the Purchase Agreement

The seller may accept your offer, reject it, or submit a counteroffer. Negotiations typically focus on price, closing date, contingencies, repair credits, and included fixtures or appliances. Once both parties agree to all terms, the purchase agreement is signed by both buyer and seller, and the property enters "pending" or "under contract" status. This is when the clock starts on all contingency deadlines.

Complete Due Diligence (Inspections, Appraisal, Title)

During the escrow period, the buyer completes home inspections, the lender orders an appraisal, and the title company conducts a title search. If the inspection reveals major issues, you can negotiate repairs, request a price reduction, or exercise your inspection contingency to cancel the contract. The appraisal ensures the property is worth the purchase price. The title search confirms the seller has clear ownership.

Finalize Financing and Obtain Clear to Close

Your lender will process your mortgage application, verify employment and income, review the appraisal, and issue a final underwriting approval called "clear to close." You will receive a Closing Disclosure (CD) at least 3 business days before closing, which details your final loan terms, monthly payment, and all closing costs. Review this document carefully and compare it to your initial Loan Estimate.

Closing Day — Sign Documents and Get Your Keys

At closing, both parties sign the final documents. The buyer signs the mortgage note, deed of trust, and closing disclosure. The seller signs the deed transferring ownership. Funds are disbursed — the buyer's down payment and closing costs are collected, the seller's mortgage is paid off, and the seller receives their net proceeds. The deed is recorded with the county, and the buyer receives the keys to their new home.

Earnest Money Deposits

Earnest money (also called a "good faith deposit") is a sum of money the buyer deposits into an escrow account after the purchase agreement is signed to demonstrate their serious intent to purchase the property. The amount is negotiable but typically ranges from 1% to 3% of the purchase price — though in hot markets, buyers may offer 5% or more.

The earnest money is held by a neutral third party (typically the title company, escrow company, or the seller's real estate brokerage) until closing, at which point it is applied toward the buyer's down payment or closing costs. If the deal falls through due to a satisfied contingency, the earnest money is returned to the buyer. If the buyer defaults without a valid contingency reason, the seller may be entitled to keep the earnest money as liquidated damages.

Protect Your Earnest Money

Always ensure your purchase agreement includes clear contingency clauses that specify the conditions under which your earnest money will be refunded. Never deposit earnest money directly to the seller — always use a licensed escrow or title company. Keep copies of all receipts and the escrow agreement.

| Market Condition | Typical Earnest Money | Example ($350K Home) |

|---|---|---|

| Buyer's Market | 1% of purchase price | $3,500 |

| Balanced Market | 1-3% of purchase price | $3,500 - $10,500 |

| Seller's Market | 3-5%+ of purchase price | $10,500 - $17,500+ |

Common Contingencies in a Residential Purchase Agreement

Contingencies are conditions that must be met for the sale to proceed. They protect the buyer (and sometimes the seller) by providing a legal way to cancel the contract and recover the earnest money if certain requirements are not satisfied. Here are the most common contingencies included in residential purchase agreements:

Financing Contingency (Mortgage Contingency)

Allows the buyer to cancel the contract if they are unable to secure mortgage financing by a specified deadline (typically 21-30 days). The contingency should specify the loan type (conventional, FHA, VA), interest rate cap, and loan amount. If the buyer's mortgage application is denied, they can exit the contract and receive their earnest money back. This is the most important contingency for buyers who are not paying cash.

Inspection Contingency

Gives the buyer the right to hire a licensed home inspector to examine the property's condition within a specified period (typically 7-14 days). If the inspection reveals significant defects — such as foundation issues, roof damage, mold, electrical problems, or plumbing leaks — the buyer can request repairs, negotiate a price reduction, ask for a repair credit at closing, or cancel the contract entirely. Some buyers also include separate contingencies for specialized inspections (radon testing, sewer scope, pest inspection).

Appraisal Contingency

Protects the buyer if the property appraises for less than the agreed purchase price. The lender will not finance more than the appraised value, so if the home appraises low, the buyer has several options: negotiate a lower price with the seller, make up the difference in cash, or cancel the contract with their earnest money returned. In competitive markets, some buyers waive this contingency or include an "appraisal gap guarantee" offering to cover a specified shortfall.

Title Contingency

Allows the buyer to review the title commitment (or preliminary title report) and cancel the contract if there are unresolvable title issues such as liens, encumbrances, easements, or boundary disputes. The title company searches public records to ensure the seller has clear, marketable title to the property. Common issues include unpaid property taxes, contractor liens, HOA liens, or errors in public records. Most title problems can be resolved before closing, but this contingency provides protection if they cannot.

Home Sale Contingency

Allows the buyer to make their purchase conditional on selling their current home by a specified date. This protects buyers who need the proceeds from their existing home sale to fund the new purchase. Sellers often view this contingency less favorably because it introduces uncertainty and effectively ties their sale to a third-party transaction. Some sellers may accept it with a "kick-out clause" that allows them to continue marketing the property and accept other offers.

Understanding Closing Costs

Closing costs are the fees and expenses — beyond the property's purchase price — that buyers and sellers pay to complete a real estate transaction. For buyers, closing costs typically total 2-5% of the purchase price. For sellers, costs are higher at 6-10% (primarily due to real estate agent commissions). Your purchase agreement should address who pays what.

Buyer's Typical Closing Costs

- Loan Origination Fee: 0.5-1% of loan amount

- Appraisal Fee: $300 - $600

- Home Inspection: $300 - $500

- Title Insurance (Lender's Policy): $500 - $1,500

- Title Search Fee: $200 - $400

- Prepaid Property Taxes: 2-6 months

- Prepaid Homeowners Insurance: 1 year

- Recording Fees: $50 - $250

Seller's Typical Closing Costs

- Real Estate Agent Commissions: 5-6% of sale price

- Transfer Taxes: Varies by state (0-2%+)

- Title Insurance (Owner's Policy): $500 - $2,000

- Mortgage Payoff: Remaining loan balance

- Prorated Property Taxes: Seller's share to closing

- HOA Transfer Fee: $200 - $500

- Repair Credits: As negotiated

- Attorney Fees: $500 - $1,500 (if applicable)

Seller Disclosures

Seller disclosures are legally required documents in which the property owner reveals known material defects and conditions that could affect the property's value or the buyer's decision to purchase. Disclosure requirements vary significantly by state, but most jurisdictions require sellers to disclose information about the following categories:

Structural Issues

Foundation cracks, roof leaks, wall damage, settling

Water & Flooding

Past flooding, water intrusion, drainage issues, sump pump

Environmental Hazards

Lead paint, asbestos, radon, mold, underground storage tanks

Systems & Appliances

HVAC age/condition, plumbing, electrical, appliance defects

Pest Infestations

Termite damage, rodents, bedbugs, past treatments

Legal & Boundary

Easements, encroachments, zoning violations, pending litigation

Federal Lead Paint Disclosure (Pre-1978 Homes)

Federal law requires sellers of homes built before 1978 to disclose known lead-based paint hazards, provide any available lead inspection reports, and give buyers a 10-day opportunity to conduct a lead inspection. This applies in ALL states regardless of state disclosure laws. Failure to comply can result in fines up to $19,507 per violation.

Title Insurance & Escrow

Title insurance protects the buyer and lender against losses from defects in the title — such as unknown liens, forged documents, recording errors, or undisclosed heirs who may have a claim to the property. Unlike other types of insurance that protect against future events, title insurance protects against past events that may come to light after closing.

There are two types of title insurance policies: the lender's policy (required by virtually all mortgage lenders, protects the lender's investment) and the owner's policy(optional but highly recommended, protects the buyer's equity). Title insurance is a one-time premium paid at closing and provides coverage for as long as you own the property.

Escrow refers to the process by which a neutral third party holds funds, documents, and instructions on behalf of the buyer and seller during the transaction. The escrow agent ensures that all conditions of the purchase agreement are met before funds are disbursed and the deed is recorded. In some states, attorneys handle the escrow function; in others, title companies or dedicated escrow companies manage the process.

Home Warranty

A home warranty is a service contract that covers repair or replacement costs for major home systems and appliances (HVAC, plumbing, electrical, water heater, kitchen appliances) for one year after closing. The seller often provides a home warranty as a selling incentive, or the buyer can purchase one independently. Typical cost: $350 - $600 per year with service call fees of $75 - $125.

Escrow Account (Impound Account)

After closing, your lender may require an escrow account to collect monthly installments for property taxes and homeowners insurance along with your mortgage payment. This ensures these critical bills are paid on time. The lender holds the funds in escrow and pays the tax and insurance bills on your behalf when they come due.

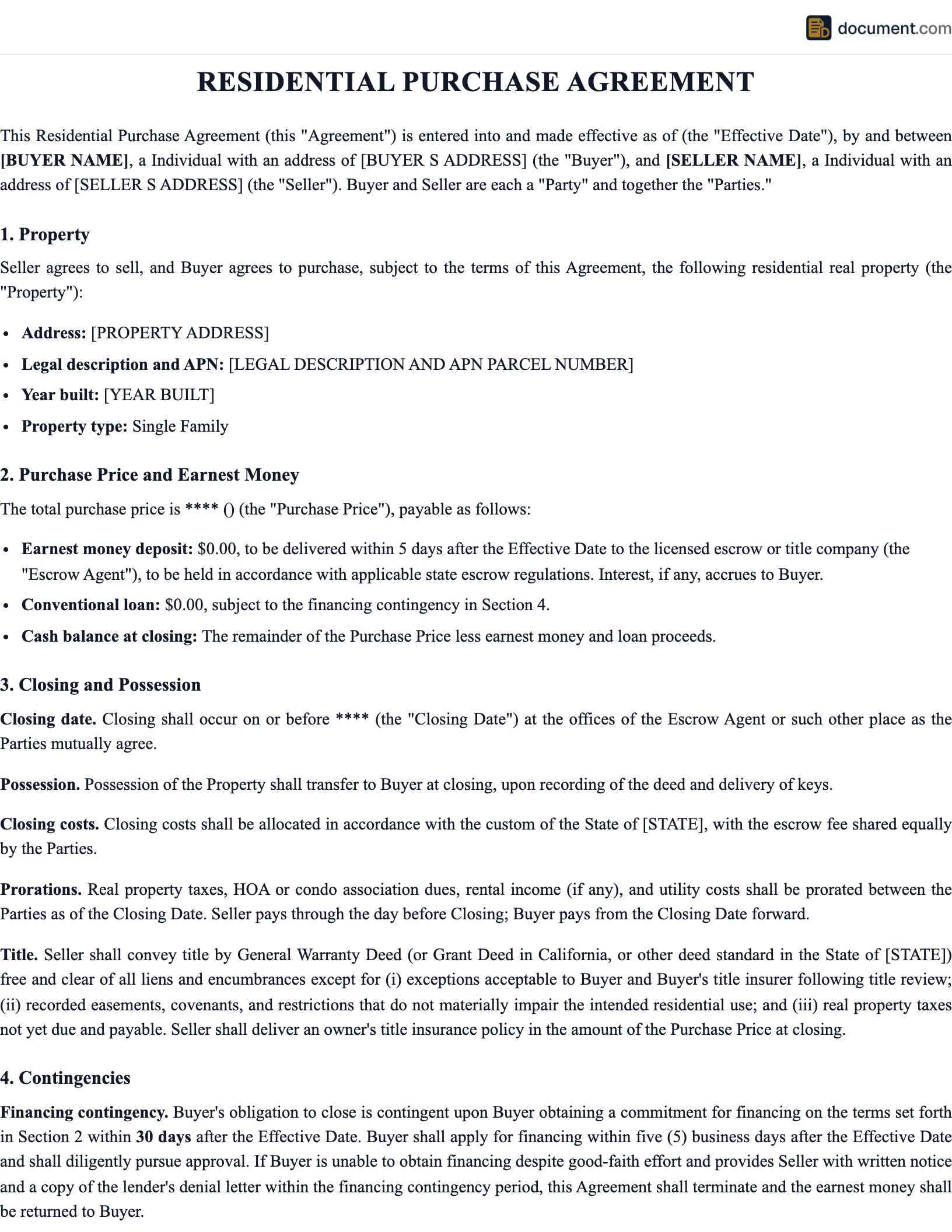

Form Preview: Residential Purchase Agreement

Below is a preview of our residential purchase agreement template. Your customized document will include all fields required by your state's real estate laws, with pre-filled contingency language and disclosure requirements.

RESIDENTIAL REAL ESTATE PURCHASE AGREEMENT

This Purchase Agreement is entered into as of the Effective Date set forth below

This Residential Real Estate Purchase Agreement ("Agreement") is entered into on[Date]between:

BUYER(S):

Name: John A. Smith

Address: 456 Current Ave, Anytown, ST 12345

Phone: (555) 123-4567Email: [email protected]

SELLER(S):

Name: Jane B. Doe

Address: 789 Oak Street, Anytown, ST 12345

Phone: (555) 987-6543Email: [email protected]

1. PROPERTY DESCRIPTION

Address: 789 Oak Street, Anytown, ST 12345

Legal Description: Lot 14, Block 3, Oakwood Subdivision

County: [County]Parcel/Tax ID: 123-456-789

2. PURCHASE PRICE & EARNEST MONEY

Purchase Price: $350,000.00

Earnest Money Deposit: $7,000.00

Escrow Agent: First American Title Company

Deposit Deadline: 3 business days after acceptance

3. FINANCING TERMS

Loan Type: Conventional 30-Year Fixed

Loan Amount: $280,000.00

Down Payment: $70,000.00 (20%)

Financing Contingency Deadline: 21 days after acceptance

4. CONTINGENCY DEADLINES

Inspection Period: 10 days

Appraisal Contingency: 21 days

Title Review Period: 14 days

Closing Date: 45 days after acceptance

Frequently Asked Questions

Find answers to common questions about residential purchase agreements, the home buying process, contingencies, and closing.

Create your Residential Purchase Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.