What Is a Promissory Note?

A promissory note is a legally binding written instrument in which one party — known as the maker, borrower, or promisor — makes an unconditional promise to pay a specified sum of money to another party — known as the payee, lender, or promisee — either on demand or at a defined future date. The note sets forth the principal amount of the debt, the interest rate (if any), the repayment schedule, the maturity date, and the consequences of default. Once signed by the maker, a promissory note creates a legally enforceable obligation to repay the debt according to the stated terms, and the payee can pursue legal remedies if the maker fails to perform.

It is important to distinguish a promissory note from a simple IOU and from a formal loan agreement. An IOU is merely an informal acknowledgment that a debt exists — it says "I owe you $5,000" but does not specify when or how the money will be repaid, what interest will accrue, or what happens if the debtor fails to pay. A promissory note, by contrast, contains all of these terms and constitutes a complete, enforceable promise to pay. A loan agreement goes further still: it is a bilateral contract signed by both the lender and the borrower that includes detailed covenants, representations, warranties, conditions precedent, and default provisions. For most personal and small business loans, a well-drafted promissory note provides all the legal protection the lender needs.

Under the Uniform Commercial Code (UCC) Article 3, a promissory note is classified as a negotiable instrument — the same legal category as checks and drafts. This means a promissory note can be transferred, endorsed, and negotiated to third parties, much like a check can be endorsed and deposited by someone other than the original payee. This negotiability is what allows promissory notes to be bought and sold in secondary markets, used as collateral for other loans, and bundled into mortgage-backed securities and other financial products. For a note to qualify as a negotiable instrument, it must contain an unconditional promise to pay a fixed amount, be payable on demand or at a definite time, be payable to order or to bearer, and not require any additional act beyond payment of money.

Promissory notes are used in an enormous range of financial transactions. Individuals use them to formalize personal loans between family members or friends, ensuring clear repayment expectations and satisfying IRS requirements for interest on below-market loans. Businesses use promissory notes to borrow working capital, finance equipment purchases, and document shareholder or partner loans to the company. In real estate, promissory notes are a fundamental part of every mortgage transaction — the note is the borrower's promise to repay the loan, while the mortgage or deed of trust provides the security interest in the property. Student loans, auto loans, and lines of credit are all documented with some form of promissory note.

Whether you are lending money to a friend, financing a vehicle purchase, structuring a business loan, or documenting a real estate transaction, a promissory note is your essential legal instrument for establishing the terms of repayment and protecting your right to collect. Our attorney-reviewed templates are designed to cover every critical provision, comply with UCC Article 3 requirements and state usury laws, and give you a professionally formatted document that stands up in court. Each template is customized for the specific type of promissory note you need — secured, unsecured, demand, installment, balloon, or convertible — and tailored to your state's legal requirements.

Legally Enforceable

UCC Article 3 compliant negotiable instrument enforceable in all 50 states

Clear Payment Terms

Defines principal, interest, schedule, late fees, and default provisions

Protects Both Parties

Establishes borrower obligations and lender rights with clear remedies

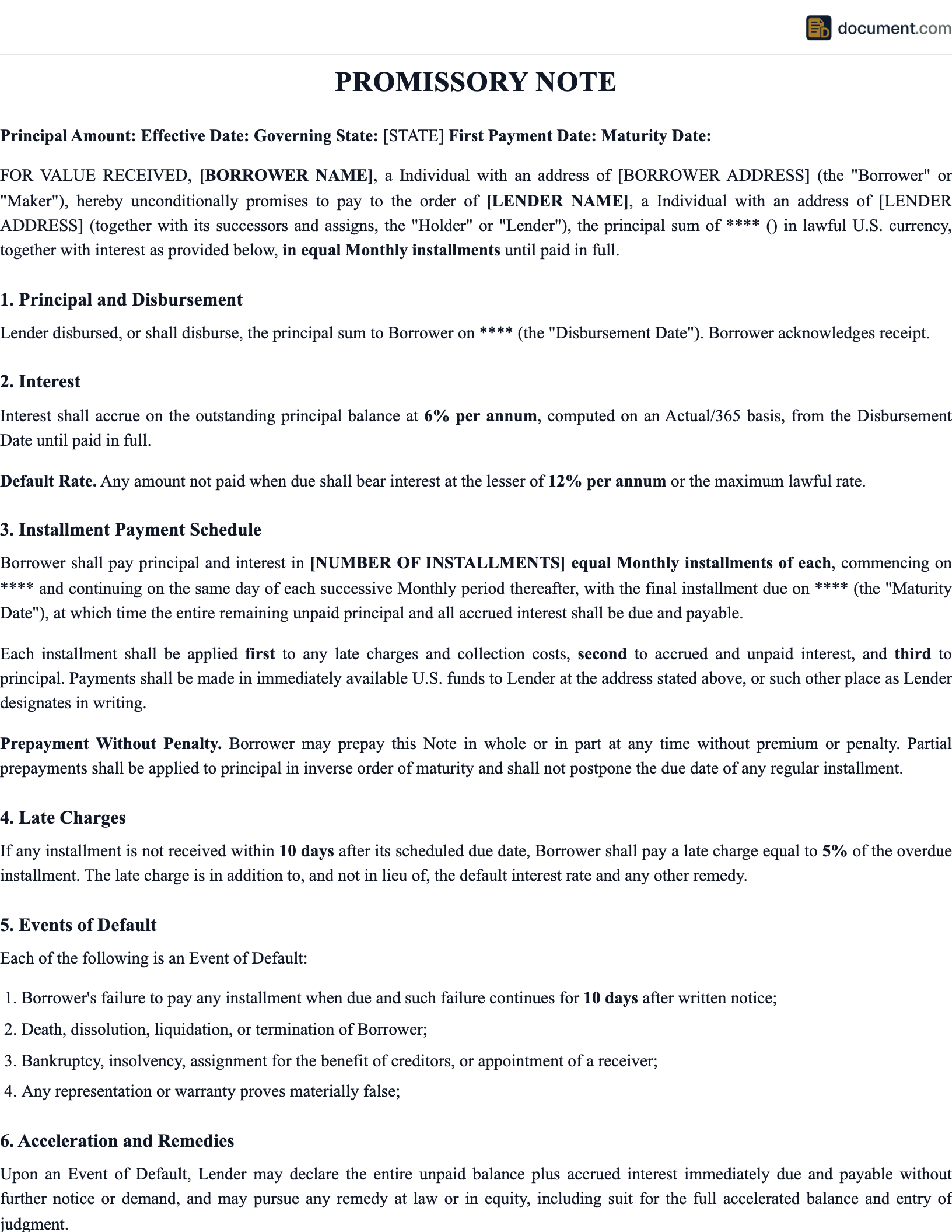

Promissory Note Form Preview

Below is a visual preview of the sections and fields included in a standard promissory note. This mockup illustrates the structure and level of detail our templates provide. Your completed document will be fully formatted, professionally styled, and customized for your specific note type and state.

Promissory Note

Unconditional Promise to Pay

Section 1: Principal Amount

Section 2: Interest Rate

Section 3: Payment Schedule

Section 4: Late Fees & Prepayment

Section 5: Default Provisions

Section 6: Signatures

Borrower (Maker) Signature

Lender (Payee) Signature

Types of Promissory Notes

Different lending situations call for different promissory note structures. A secured note backed by collateral is very different from a convertible note used in startup financing. Select the note type that matches your lending arrangement to get a template with the right provisions, payment terms, and legal language for your specific situation.

Secured Promissory Note

Backed by collateral such as property, vehicles, or other valuable assets

Unsecured Promissory Note

No collateral required — based on the borrower's creditworthiness and promise to pay

Demand Promissory Note

Payable in full when the lender demands repayment — no fixed maturity date

Installment Promissory Note

Fixed regular payments of principal and interest over a set repayment period

Balloon Promissory Note

Smaller periodic payments with a large lump-sum balloon payment at the end

Convertible Promissory Note

Debt that converts into equity or ownership shares under specified conditions

Release

Release a borrower from further obligation once the promissory note is paid in full

Promissory Note vs Other Documents

A promissory note is often confused with other debt and financial documents. Understanding the differences is critical for choosing the right document for your situation and knowing when you may need more than one.

Promissory Note vs IOU

Promissory Note

- - Contains a formal, unconditional promise to pay

- - Specifies interest rate, payment schedule, and maturity date

- - Includes default provisions, late fees, and remedies

- - Negotiable instrument under UCC Article 3

- - Easily enforceable in court with clear terms

IOU

- - Informal acknowledgment of debt only

- - No payment terms, schedule, or interest rate

- - No default provisions or remedies specified

- - Not a negotiable instrument — cannot be transferred

- - Difficult to enforce — requires proving additional terms

Bottom line: An IOU simply acknowledges that money is owed. A promissory note is a complete legal instrument that defines exactly how, when, and under what conditions the money will be repaid. Always use a promissory note instead of an IOU when lending money.

Promissory Note vs Loan Agreement

Promissory Note

- - Unilateral — only borrower signs

- - Focuses on the promise to repay

- - Simpler, shorter document (1-4 pages)

- - Negotiable instrument that can be transferred

- - Ideal for personal and simple business loans

Loan Agreement

- - Bilateral — both parties sign

- - Includes lender's obligations and conditions

- - More detailed document (5-50+ pages)

- - Contains covenants, reps, warranties, conditions

- - Required for complex commercial financing

When to use both: In commercial lending, it is standard practice to use both a loan agreement (which sets forth all terms and conditions) and a promissory note (which is the actual evidence of the debt). The loan agreement is the contract; the promissory note is the instrument that can be enforced and transferred.

Promissory Note vs Mortgage Note

General Promissory Note

- - May be secured or unsecured

- - Used for any type of loan or debt

- - Does not require recording with the county

- - Collateral can be any asset (if secured)

- - Simpler default and collection process

Mortgage Note

- - Always secured by real property

- - Paired with a mortgage or deed of trust

- - Mortgage/deed of trust is recorded with county

- - Default triggers foreclosure proceedings

- - Subject to TILA, RESPA, and state mortgage laws

Key distinction: A mortgage note is a specific type of promissory note that is secured by real property. The note itself is the promise to pay; the mortgage (or deed of trust) is the separate document that creates the lien on the property as security for the note. If the borrower defaults, the lender forecloses under the mortgage, not the note.

Promissory Note vs Bond

Promissory Note

- - Private agreement between specific parties

- - Not publicly traded on exchanges

- - Terms are individually negotiated

- - Typically shorter-term (months to a few years)

- - Minimal regulatory requirements for private notes

Bond

- - Tradeable security issued to the public

- - Bought and sold on securities exchanges

- - Standardized terms with a bond indenture

- - Typically longer-term (5 to 30+ years)

- - Heavily regulated by SEC and securities laws

In practice: Both promissory notes and bonds represent debt obligations. The key difference is that bonds are securities issued to a broad market of investors and are subject to securities regulation, while promissory notes are private instruments between identified parties. Selling promissory notes to the general public may trigger securities law requirements.

How to Write a Promissory Note: A 10-Step Guide

Writing a thorough promissory note requires careful attention to the terms of repayment and applicable legal requirements. Each provision serves a specific purpose, and omitting key terms can weaken the note's enforceability or leave the lender without adequate protection. Follow these ten steps to create a comprehensive promissory note.

Identify the Parties

Begin by clearly identifying the borrower (maker) and the lender (payee) using their full legal names. If the borrower is an individual, use their name as it appears on their government-issued identification. If the borrower is a business entity, use the exact legal name of the entity (LLC, Corporation, Partnership) along with the state in which it is organized and the name of the authorized representative signing on its behalf.

Include the mailing address of each party. If there are co-borrowers, each must be named individually and each will be jointly and severally liable for the debt unless the note specifies otherwise. If a guarantor is involved, they should be identified separately and a personal guarantee document should accompany the note.

Tip: Use the exact legal name of each party. Misspellings or informal names can create enforcement problems if the note needs to be collected through legal proceedings.

State the Principal Amount

Clearly state the principal amount — the total sum of money being borrowed — in both numerical and written form to eliminate ambiguity. For example: "$25,000.00 (Twenty-Five Thousand Dollars)." If the amounts conflict, most legal jurisdictions treat the written-out amount as controlling. The principal amount should reflect only the amount being lent, not including interest or fees.

If the loan will be disbursed in multiple draws or installments (such as a construction loan), specify the maximum principal amount, the draw schedule, and the conditions that must be met before each disbursement. The note should make clear that interest accrues only on the amount actually disbursed, not the total commitment.

Set the Interest Rate

Specify the annual interest rate as a percentage and indicate whether it is a fixed rate or variable rate. If variable, identify the index (such as the prime rate or SOFR) and the margin added to the index. State whether interest is calculated using simple interest (interest on principal only) or compound interest (interest on principal plus accrued interest), and specify the compounding frequency (monthly, quarterly, annually).

Before setting the interest rate, verify that it complies with your state's usury laws. Every state imposes a maximum legal interest rate for private loans, and exceeding this limit can result in forfeiture of interest, voiding of the note, or even criminal penalties. If the loan carries zero interest, the IRS may impute interest at the Applicable Federal Rate (AFR) for loans over $10,000, creating phantom income for the lender.

Warning:Charging interest above your state's usury limit can void the entire note or subject you to penalties. Check state usury laws before setting any interest rate.

Define the Payment Schedule

Specify exactly how and when the borrower will repay the loan. For installment notes, state the payment amount, frequency (weekly, bi-weekly, monthly), the date each payment is due, and the total number of payments. For demand notes, state that the full balance is payable upon demand by the lender and specify the number of days' notice required before payment is due (commonly 30 days). For balloon notes, define the periodic payment amount and the date and amount of the final balloon payment.

Indicate whether payments are applied first to interest and then to principal (the standard approach) or in some other order. Include the date of the first payment, the maturity date (final payment date), and the total amount the borrower will pay over the life of the loan including interest. Specify the acceptable payment methods (check, bank transfer, ACH, etc.) and the address or account to which payments should be sent.

Address Late Fees and Grace Periods

Define what happens when a payment is late. Include a grace period — typically 10 to 15 days after the due date — during which a late payment will not incur a penalty. After the grace period, specify the late fee: this is usually either a flat dollar amount (e.g., $25) or a percentage of the overdue payment (e.g., 5%), sometimes expressed as the greater of the two.

Some states cap the amount that can be charged as a late fee, so verify your state's requirements. Also specify whether a default interest rate will apply to overdue amounts — this is a higher rate of interest (e.g., 18% per annum) that kicks in after default to compensate the lender for the increased risk and cost of collection.

Tip: Reasonable late fees serve as an incentive for timely payment. Excessive late fees may be struck down by a court as unenforceable penalties. Keep them proportionate to the payment amount.

Include Prepayment Terms

State whether the borrower has the right to prepay the note in whole or in part before the maturity date, and whether a prepayment penalty will apply. Many personal and small business notes allow prepayment without penalty, which encourages faster repayment and benefits both parties. However, for longer-term loans where the lender relies on the interest income stream, a prepayment penalty may be appropriate.

If a prepayment penalty applies, specify the calculation method — common approaches include a percentage of the outstanding balance (e.g., 2%), a set number of months' interest, or a declining penalty that decreases over time. Some states restrict or prohibit prepayment penalties on certain types of consumer loans, so check your state's regulations.

Define Default and Acceleration

Clearly define what constitutes a default (event of default). Common triggers include failure to make a payment when due, breach of any term or condition of the note, bankruptcy or insolvency of the borrower, death of the borrower (if an individual), and material misrepresentation. For secured notes, default may also include failure to maintain insurance on the collateral, unauthorized sale or disposal of the collateral, or a material decline in the value of the collateral.

Include an acceleration clause that allows the lender to declare the entire remaining balance immediately due and payable upon default. Without this clause, the lender can only sue for each missed payment as it becomes due, which is impractical and expensive. The acceleration clause is the lender's most important protective provision. Also specify the remedies available to the lender, including the right to collect attorney's fees and costs.

Identify Collateral (If Secured)

If the note is secured, describe the collateral in sufficient detail to identify it clearly. For real property, this means a legal description and the street address; for vehicles, the year, make, model, and VIN; for equipment, serial numbers and descriptions; for financial assets, account numbers and institution names. A separate security agreement, mortgage, or deed of trust should also be executed to create and perfect the security interest.

The note should reference the security agreement and state that the lender's rights under the note are secured by the collateral described in that agreement. If the collateral is personal property, a UCC-1 financing statement should be filed with the state to perfect the lender's security interest. If the collateral is real property, the mortgage or deed of trust must be recorded with the county.

Warning: Failing to properly perfect a security interest (by filing a UCC-1 or recording a mortgage) means other creditors may have priority over your claim to the collateral. Always perfect your security interest promptly.

Add General Provisions

Include standard legal provisions (boilerplate) that protect the enforceability of the note. These typically include: governing law (which state's law applies), severability (if one provision is invalid, the rest of the note remains enforceable), waiver of presentment and demand (the borrower waives formal notice requirements under UCC Article 3), successors and assigns (the note binds heirs, estates, and successors), entire agreement (the note constitutes the complete agreement and supersedes prior negotiations), and amendments (the note can only be modified in writing signed by both parties).

Consider including a dispute resolution clause specifying whether disputes will be resolved through mediation, arbitration, or litigation, and in which jurisdiction. A choice of venue clause that designates the county or district where legal proceedings must be brought can also be valuable, particularly when the parties are in different states.

Execute the Note Properly

The borrower (maker) must sign and date the promissory note. While the lender's signature is not legally required for the note to be valid (since it is the borrower's promise), many practitioners include a signature line for the lender as an acknowledgment. If there are co-borrowers, each must sign individually. If the borrower is an entity, the authorized representative must sign on behalf of the entity, and their title should be included to demonstrate authority.

While notarization is not required in most states for a promissory note to be enforceable, it is recommended for notes involving large sums. If the note is secured by real property, the accompanying mortgage or deed of trust will need to be notarized and recorded. Electronic signatures are valid under the federal ESIGN Act and state UETA laws. Keep the original signed note in a secure location — the holder of the original note is the party entitled to enforce it.

Best practice:The lender should retain the original signed note. If the note is ever paid in full, the lender should mark it "PAID IN FULL," sign it, and return the original to the borrower as evidence the debt has been satisfied.

Key Components of a Promissory Note

A comprehensive promissory note addresses every aspect of the loan obligation. Missing critical components can weaken the note's enforceability, create ambiguity about repayment terms, or leave the lender without adequate legal protection. The table below outlines the essential elements every promissory note should include.

| Component | Description |

|---|---|

| Maker (Borrower) | Full legal name, address, and identification of the person or entity promising to pay |

| Payee (Lender) | Full legal name and address of the person or entity to whom payment is promised |

| Principal Amount | Total sum borrowed, stated in both numerical and written form |

| Date of Note | The date the note is executed and the loan obligation begins |

| Interest Rate | Annual percentage rate, whether fixed or variable, and the calculation method (simple or compound) |

| Payment Schedule | Amount, frequency, due dates, and total number of payments required |

| Maturity Date | The final date by which all principal and interest must be repaid in full |

| Late Fee Provision | Grace period duration, late fee amount or percentage, and how late fees are applied |

| Prepayment Terms | Whether early repayment is allowed and any prepayment penalty that may apply |

| Default Provisions | Events that constitute default, notice requirements, and cure periods |

| Acceleration Clause | Lender's right to demand full immediate payment upon borrower's default |

| Collateral (If Secured) | Description of property pledged as security, with reference to the security agreement |

| Attorney's Fees | Borrower's obligation to pay lender's legal costs if collection action is required |

| Governing Law | Which state's laws govern the interpretation and enforcement of the note |

| Waivers | Borrower's waiver of presentment, demand, protest, and notice of dishonor under UCC Article 3 |

| Severability | If any provision is held invalid, the remaining provisions continue in full force |

| Signatures & Date | Dated signatures of the maker (and co-makers), with witness or notary lines if applicable |

Interest Rate Rules for Promissory Notes

Interest is the cost of borrowing money, and the rules governing interest rates on promissory notes are a patchwork of state usury laws, federal regulations, and IRS requirements. Understanding these rules is essential for creating an enforceable note that does not expose the lender to penalties.

Usury Laws Overview

Usury laws set the maximum interest rate a private lender can charge on a loan. These limits vary by state and by loan type. Charging interest above the legal limit (usury) can have severe consequences: some states void the entire note, others require forfeiture of all interest (leaving only the principal owed), and a few impose criminal penalties including fines and imprisonment. The penalties for usury are strict because these laws exist to protect borrowers from predatory lending.

Simple vs Compound Interest

Simple Interest

Calculated only on the original principal balance. The interest charge remains the same each period regardless of how long the loan has been outstanding. Formula: Principal x Rate x Time. Example: $10,000 at 6% for 3 years = $10,000 x 0.06 x 3 = $1,800 total interest. Simple interest is the most common method for promissory notes between individuals and is easier to calculate and understand.

Compound Interest

Calculated on the principal plus any previously accrued but unpaid interest. Unpaid interest is added to the principal (capitalized), and future interest is charged on the larger balance. Example: $10,000 at 6% compounded annually for 3 years = $11,910.16 total, or $1,910.16 in interest (compared to $1,800 with simple interest). Compound interest results in higher total payments and must be clearly disclosed in the note. Some states restrict compound interest on consumer loans.

APR Disclosure Requirements

The Annual Percentage Rate (APR) represents the true annual cost of borrowing, including not just the stated interest rate but also fees, points, and other charges expressed as a yearly rate. Under the federal Truth in Lending Act (TILA), lenders who make more than a certain number of loans per year or who regularly extend credit must disclose the APR to consumer borrowers. While private individuals making occasional loans may not be required to provide TILA disclosures, including the APR in any promissory note is considered best practice and demonstrates transparency.

State Usury Rate Ranges

State usury limits for consumer loans generally fall into the following ranges, though exceptions exist for specific loan types, amounts, and licensed lenders:

| Rate Range | Example States |

|---|---|

| 5% - 8% | New York (16% civil, 25% criminal), Connecticut (12%), Vermont (12%) |

| 8% - 12% | New Jersey (6%-30% depending on type), Pennsylvania (6%), Michigan (7%) |

| 12% - 18% | California (10% for personal loans), Florida (18%), Illinois (9%) |

| 18% - 25% | Texas (10% or 18% for commercial), Ohio (8%), Georgia (5% or contract rate) |

| No cap / high cap | New Hampshire (no cap), Utah (no cap for written agreements), Colorado (45% consumer) |

IRS Imputed Interest Rules

The IRS requires that loans between related parties (family members, business owners, etc.) exceeding $10,000 charge at least the Applicable Federal Rate (AFR) of interest. If no interest or below-AFR interest is charged, the IRS will impute interest — treating the forgone interest as income to the lender and potentially as a gift to the borrower. The AFR is published monthly by the IRS and varies based on loan term: short-term (3 years or less), mid-term (3 to 9 years), and long-term (over 9 years). Failure to charge at least the AFR can result in unexpected tax consequences for both parties. Always check the current AFR when structuring a below-market or zero-interest loan.

Legal Requirements for Promissory Notes

Promissory notes are governed by a combination of the Uniform Commercial Code (UCC), state usury laws, federal lending regulations, and general contract law. Understanding these requirements is essential to ensure your note is enforceable and that you comply with all applicable rules.

UCC Article 3 — Negotiable Instruments

The Uniform Commercial Code Article 3, adopted in some form by every state, governs promissory notes as negotiable instruments. For a note to qualify as a negotiable instrument, it must: (1) be in writing and signed by the maker; (2) contain an unconditional promise to pay a fixed amount of money; (3) be payable on demand or at a definite time; (4) be payable to order or to bearer; and (5) not require any act in addition to payment of money. Notes that meet these requirements can be transferred to third parties, and a holder in due course takes the note free of many defenses the borrower might assert against the original lender.

Statute of Limitations

The statute of limitations for enforcing a promissory note varies by state and by the type of note. Most states provide a statute of limitations of 4 to 6 years for written promissory notes, measured from the date of default or the date the last payment was made. Some states have longer periods — up to 10 years. For demand notes, the statute may begin running from the date of the note or from the date demand is made, depending on the state. Once the statute of limitations expires, the lender loses the right to sue for collection, although the underlying debt may still exist. Making a partial payment or written acknowledgment of the debt can restart the statute of limitations in many states.

Acceleration Clauses

An acceleration clause is a provision that allows the lender to demand immediate payment of the entire outstanding balance if the borrower defaults on any payment or violates a condition of the note. Courts generally enforce acceleration clauses as long as the lender acts in good faith and provides reasonable notice before accelerating. Some states require the lender to give the borrower a written notice of default and a cure period (typically 10 to 30 days) before acceleration takes effect. Acceleration clauses are considered standard and essential in commercial and consumer promissory notes.

Due-on-Sale Clauses

A due-on-sale clause (also called an alienation clause) requires the borrower to repay the loan in full if they sell or transfer the property that serves as collateral for the note. This prevents the borrower from transferring the property to a new owner while the original loan remains in place. Due-on-sale clauses are standard in mortgage notes and are enforceable under the federal Garn-St. Germain Depository Institutions Act of 1982, which preempts state laws that would otherwise restrict these clauses. However, certain transfers are exempt from due-on-sale enforcement, including transfers to a spouse, transfers into a revocable trust, and transfers resulting from the borrower's death.

Federal Lending Regulations

- Truth in Lending Act (TILA): Requires creditors who regularly extend consumer credit to disclose key loan terms including the APR, finance charge, amount financed, and total payments. While private individuals making occasional loans may not qualify as "creditors" under TILA, anyone who makes more than 5 mortgage loans in a year may be covered.

- Dodd-Frank Act: Restricts certain lending practices for consumer mortgages, including limits on balloon payments, negative amortization, and interest-only periods for qualified mortgages. Applies primarily to institutional lenders but may affect private lenders who make multiple mortgage loans.

- Equal Credit Opportunity Act (ECOA): Prohibits discrimination in lending based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance. Applies to all creditors, including private individuals who make loans.

- IRS Applicable Federal Rate (AFR): Requires that loans between related parties charge at least the minimum interest rate published monthly by the IRS. Below-market loans of $10,000 or more trigger imputed interest rules, which can create taxable income for the lender and gift tax consequences.

- ESIGN Act and UETA: Electronic signatures on promissory notes are legally valid and enforceable under the federal ESIGN Act and the Uniform Electronic Transactions Act adopted by most states, provided both parties consent to electronic execution.

Promissory Note by State

Each promissory note type has its own 50-state coverage pages. To avoid broken links on the main promissory note page, choose a note type below and then select your state from that type page.

Secured Promissory Note

Backed by collateral such as property, vehicles, or other valuable assets

Unsecured Promissory Note

No collateral required — based on the borrower's creditworthiness and promise to pay

Demand Promissory Note

Payable in full when the lender demands repayment — no fixed maturity date

Installment Promissory Note

Fixed regular payments of principal and interest over a set repayment period

Balloon Promissory Note

Smaller periodic payments with a large lump-sum balloon payment at the end

Convertible Promissory Note

Debt that converts into equity or ownership shares under specified conditions

Release

Release a borrower from further obligation once the promissory note is paid in full

Sample Promissory Note

Below is a condensed preview of our installment promissory note template. This sample shows the structure, language, and sections included in our attorney-reviewed documents. Your completed note will be fully customized for your note type, state, and specific loan terms.

PROMISSORY NOTE

Installment Note with Fixed Interest

FOR VALUE RECEIVED, the undersigned,[Borrower Name]("Maker"), of[Borrower Address], hereby unconditionally promises to pay to the order of[Lender Name]("Payee"), of[Lender Address], or at such other place as the Payee may designate in writing, the principal sum of[Amount in Words]Dollars ($[Amount]), together with interest thereon as set forth below.

1. INTEREST RATE

The unpaid principal balance shall bear interest at a fixed rate of[%] per annum, calculated on the basis of a 365-day year and the actual number of days elapsed. Interest shall be computed using simple interest unless otherwise specified herein.

2. PAYMENT TERMS

Maker shall pay to Payee[Number]consecutive monthly installments of $[Amount]each, commencing on [Date]and continuing on the same day of each month thereafter until the Maturity Date of[Date], on which date the entire remaining unpaid principal balance, together with all accrued and unpaid interest, shall be due and payable in full.

3. LATE CHARGES

If any installment is not received by Payee within[15] days after its due date, Maker shall pay a late charge equal to[5%] of the overdue amount or $[25], whichever is greater...

4. PREPAYMENT

Maker may prepay this Note in whole or in part at any time without premium or penalty. Any partial prepayment shall be applied first to accrued interest and then to the outstanding principal balance. Prepayment shall not excuse Maker from making subsequent scheduled payments until the Note is paid in full...

5. DEFAULT AND ACCELERATION

The occurrence of any of the following shall constitute an Event of Default: (a) failure to make any payment within [10]days after its due date; (b) breach of any term of this Note; (c) bankruptcy, insolvency, or assignment for the benefit of creditors by Maker. Upon the occurrence of an Event of Default, Payee may, at Payee's option, declare the entire unpaid principal balance plus all accrued interest immediately due and payable...

6. GOVERNING LAW

This Note shall be governed by and construed in accordance with the laws of the State of[State], without regard to its conflict of laws provisions...

7. WAIVERS

Maker hereby waives presentment for payment, demand, notice of dishonor, protest, and notice of protest of this Note, and all other notices in connection with the delivery, acceptance, performance, default, or enforcement of the payment of this Note...

Maker (Borrower) Signature

Name:

Date:

Payee (Lender) Acknowledgment

Name:

Date:

Frequently Asked Questions

Find answers to common questions about promissory notes, interest rates, repayment terms, default provisions, and the legal requirements for creating enforceable loan documents.

Official Resources

For additional information on promissory note requirements, interest rate rules, lending regulations, and consumer protections, consult these official government and legal resources.

IRS - Applicable Federal Rates

Monthly AFR tables for imputed interest on below-market loans

CFPB - Consumer Financial Protection

Consumer lending rules, complaint filing, and borrower protections

UCC Article 3 - Negotiable Instruments

Full text of UCC Article 3 governing promissory notes and drafts

State Usury Law References

State-by-state guide to maximum legal interest rates for private loans

IRS Publication 550 - Investment Income

IRS rules on imputed interest, OID, and below-market loan tax treatment

ULC - Uniform Commercial Code

Uniform Law Commission resources on UCC adoption and amendments

CFPB - Promissory Note Information

Consumer guide explaining promissory notes in mortgage transactions

SBA - Small Business Loan Programs

Small Business Administration loan resources and lending guidance

Create your Promissory Note in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.