What Is a Convertible Promissory Note?

A convertible promissory note is a form of short-term debt used primarily in startup financing that converts into equity shares of the company upon a specified triggering event. Instead of being repaid in cash like a traditional loan, the investor's principal plus accrued interest converts into ownership shares — typically preferred stock — at a discounted price.

Convertible notes bridge the gap between a startup's early funding needs and a full priced equity round. They allow founders and investors to defer the difficult question of company valuation to a later date when the company has more traction and market data to support a fair valuation. The conversion discount and valuation cap reward early investors for taking on the additional risk of investing before a valuation is established.

Key terms include the valuation cap (maximum conversion price), discount rate (percentage below the next round's price), interest rate, maturity date, and conversion triggers (qualified financing, change of control, maturity). Convertible notes are securities and must comply with federal and state securities regulations.

Startup Financing

The standard instrument for pre-seed and seed stage startup funding

Deferred Valuation

Skip the valuation debate now; convert at a discount to the next round

Investor Protection

Valuation cap, discount rate, and debt status protect early investors

Convertible Promissory Note by State

Securities regulations vary by state. Each state has different exemption requirements, filing obligations, and investor protection rules. Select your state for a compliant template.

How Conversion Works

Understanding the conversion mechanics is essential for both founders and investors.

Investment and Note Issuance

The investor provides capital to the startup. In return, the company issues a convertible promissory note documenting the investment amount, interest rate, valuation cap, discount rate, and conversion triggers. Interest begins accruing from the investment date.

Qualified Financing Round Occurs

When the company raises a qualifying equity round (e.g., Series A above the minimum threshold), the note automatically converts. The conversion price is the LOWER of: (a) the price per share based on the valuation cap, or (b) the new round's price per share minus the discount rate.

Principal Plus Interest Converts

The total amount that converts includes the original principal investment PLUS all accrued interest. This total is divided by the conversion price to determine the number of shares the note holder receives. The investor typically receives the same class of stock as the new round investors (usually preferred stock).

Alternative Scenarios

If no qualified financing occurs before maturity, the note may: convert at the cap valuation, be repaid in cash, or be extended by mutual agreement. If the company is acquired (change of control), the note typically converts at the cap or is repaid at a premium (often 1.5-2x the principal).

Key Terms Explained

| Term | Description |

|---|---|

| Valuation Cap | Maximum company valuation at which the note converts, protecting early investors |

| Discount Rate | Percentage discount to the next round's price (typically 15-25%) |

| Interest Rate | Annual rate that accrues and adds to conversion amount (typically 2-8%) |

| Maturity Date | Deadline for conversion or repayment (typically 18-24 months) |

| Qualified Financing | Minimum equity raise that triggers automatic conversion |

| Pro-Rata Rights | Right to invest in future rounds to maintain ownership percentage |

| Most Favored Nation | Terms automatically match any better terms offered to later note investors |

| Change of Control | Acquisition or merger trigger — typically converts or repays at premium |

SAFE vs. Convertible Note

The SAFE (Simple Agreement for Future Equity) was created by Y Combinator as a simpler alternative to convertible notes. Understanding the differences helps founders and investors choose the right instrument.

Important Distinction

A convertible note is DEBT — it creates a legal obligation to repay and gives the investor creditor status. A SAFE is NOT debt — it is an agreement to issue equity in the future with no repayment obligation. This distinction matters for bankruptcy priority, balance sheet treatment, and tax implications.

| Feature | Convertible Note | SAFE |

|---|---|---|

| Legal Status | Debt instrument | Equity-like agreement |

| Interest Rate | Yes (2-8% typical) | No |

| Maturity Date | Yes (18-24 months) | No |

| Repayment Right | Yes, at maturity | No |

| Complexity | More complex, higher legal costs | Simpler, lower legal costs |

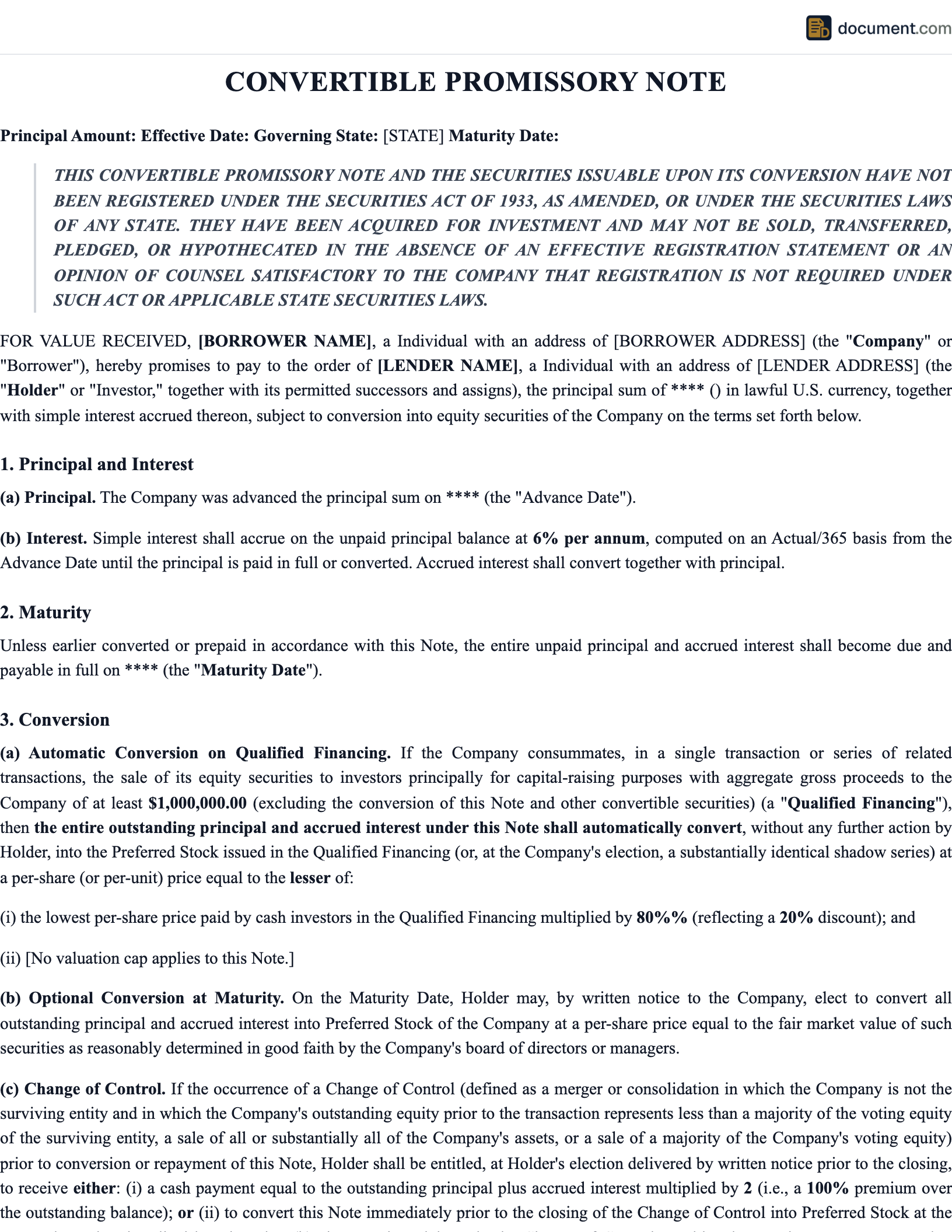

Sample Convertible Promissory Note

Below is a preview of our convertible promissory note template.

CONVERTIBLE PROMISSORY NOTE

Startup Financing Instrument

COMPANY:

Name: [Company Name]

State of Incorporation: [State]

INVESTOR:

Name: [Investor Name]

KEY TERMS

Principal: $[Amount]

Interest Rate: [Rate]% per annum

Valuation Cap: $[Amount]

Discount Rate: [Rate]%

Maturity Date: [Date]

Frequently Asked Questions

Find answers to common questions about convertible promissory notes, conversion mechanics, and securities compliance.

Create your Convertible Promissory Note in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.