What Is a Loan Agreement?

A loan agreement is a legally binding contract between a lender and a borrower that documents the terms and conditions of a loan. It establishes the principal amount being lent, the interest rate charged, the repayment schedule, any collateral securing the loan, default provisions and remedies, and the rights and obligations of both parties throughout the life of the loan. A loan agreement transforms an informal exchange of money into a structured legal relationship with clear expectations and enforceable obligations.

Unlike a simple promissory note — which is a one-sided promise by the borrower to repay — a loan agreement is a bilateral contract signed by both the lender and the borrower. This bilateral structure allows the agreement to include detailed provisions that a promissory note typically does not: conditions that must be met before the loan is disbursed (conditions precedent), ongoing obligations of the borrower during the loan term (covenants), representations the borrower makes about their financial condition, events that constitute default, and the specific remedies available to the lender if default occurs. These additional provisions provide significantly more protection to the lender and more clarity to the borrower than a promissory note alone.

Loan agreements are used across a wide spectrum of lending situations: personal loans between friends or acquaintances, family loans between relatives (which have important IRS implications), business loans from investors or private lenders, real estate financing, vehicle financing, student loans, and any other situation where money is lent with the expectation of repayment. The complexity of the agreement scales with the size and risk of the loan — a $2,000 loan between friends may require a straightforward 2-page agreement, while a $500,000 business loan may need a 30-page agreement with financial covenants, personal guarantees, and collateral documentation.

From a legal perspective, a loan agreement must comply with your state's usury laws (maximum interest rate limits), consumer lending regulations (if applicable), and contract law principles. Charging an interest rate above the state usury limit can result in the lender forfeiting all interest, facing civil penalties, and in some states being subject to criminal prosecution. For loans between family members, the IRS requires the interest rate to meet or exceed the Applicable Federal Rate (AFR) to avoid gift tax implications.

Our attorney-reviewed templates provide comprehensive loan agreements for every lending scenario — from simple personal loans to complex secured business loans. Each template includes usury-compliant interest rate guidance for your state, amortization schedule generators, collateral provisions where applicable, and clear default and remedy provisions that protect both the lender's investment and the borrower's rights.

Legal Protection

Creates an enforceable obligation with clear remedies if the borrower defaults on repayment

Usury Compliance

Ensures interest rates comply with your state's usury laws and IRS requirements for family loans

Clear Terms

Eliminates misunderstandings by documenting every aspect of the lending arrangement in writing

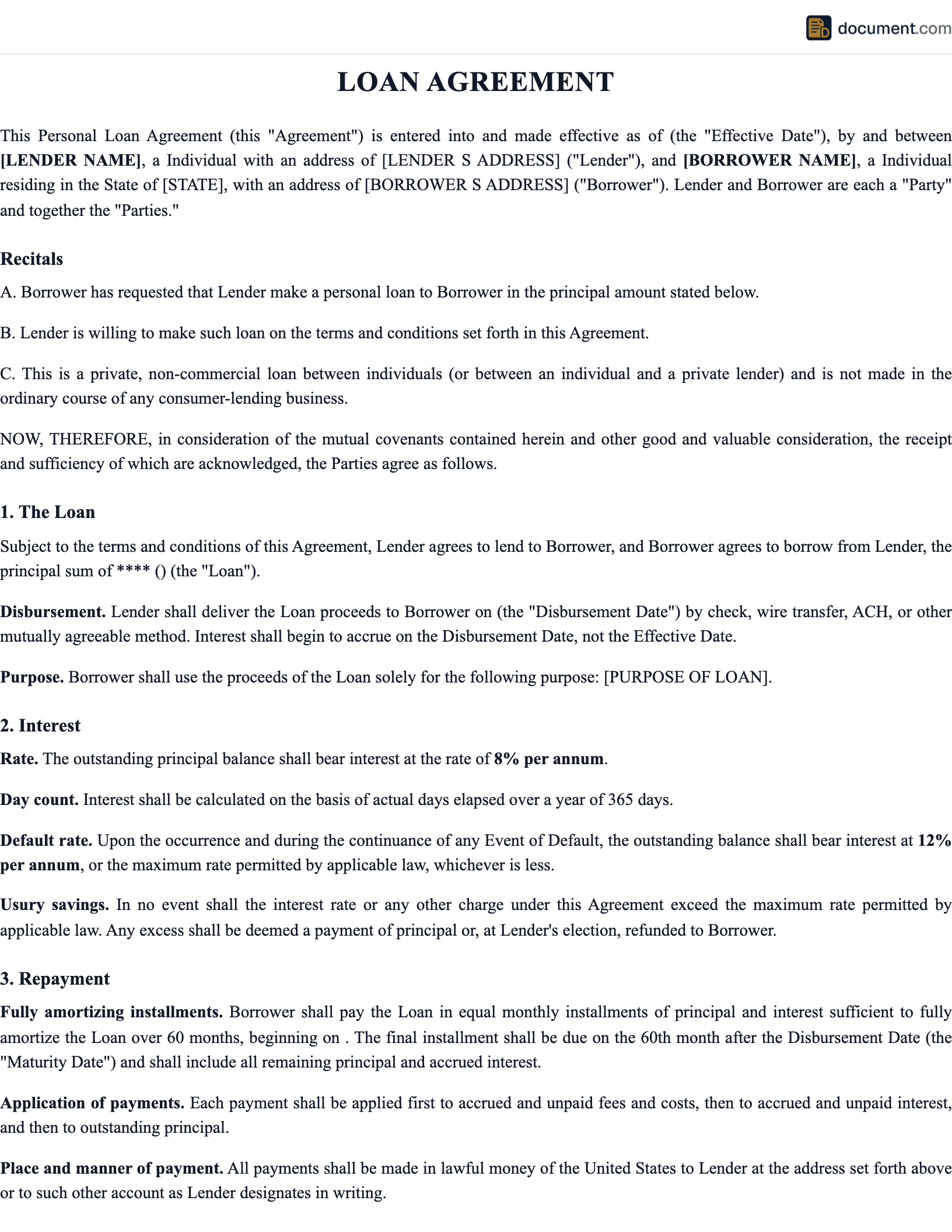

Loan Agreement Form Preview

Below is a visual preview of the sections and fields included in a standard loan agreement form. This mockup illustrates the level of detail our templates provide for documenting the lending relationship between the parties.

Personal Loan Agreement

Between Lender and Borrower

Section 1: Lender Information

Section 2: Borrower Information

Section 3: Loan Terms

Section 4: Security / Collateral

Section 5: Execution

Lender Signature

Borrower Signature

Types of Loan Agreements

Different lending situations call for different types of loan agreements. Each type addresses the specific needs and risks of a particular lending scenario.

Personal Loan Agreement

Standard agreement for loans between individuals, covering repayment terms, interest, and default provisions

Family Loan Agreement

Loan between family members with IRS-compliant interest rates, gift tax documentation, and clear repayment expectations

Business Loan Agreement

Commercial lending agreement with business-specific provisions including financial covenants and reporting requirements

Demand Loan Agreement

Loan with no fixed repayment schedule that becomes due when the lender demands repayment

Secured Loan Agreement

Loan backed by collateral such as real estate, vehicles, or other assets that the lender can seize upon default

Unsecured Loan Agreement

Loan based solely on the borrower's creditworthiness with no collateral requirement

Payment Plan Agreement

Structured installment plan for repaying an existing debt with specified payment amounts and dates

Payment Plan

Installment schedule breaking loan repayment into manageable periodic payments with set due dates

Release Of Personal Guarantee

Releases a guarantor from personal liability once loan conditions or payment obligations are met

Loan Agreement vs Other Documents

A loan agreement is one of several documents that can formalize a lending arrangement. Understanding the differences helps you choose the right document for your situation.

Loan Agreement vs Promissory Note

Loan Agreement

- - Bilateral contract signed by both parties

- - Detailed covenants, representations, and conditions

- - Comprehensive default provisions and remedies

- - Best for larger or complex loans

Promissory Note

- - Unilateral promise signed by borrower only

- - Simpler document with basic terms

- - Limited default provisions

- - Suitable for small, simple loans

When to use which: Use a promissory note for small, simple loans between trusted parties. Use a loan agreement for any loan over $5,000, business loans, secured loans, or any situation where you want comprehensive legal protection.

Loan Agreement vs IOU

Loan Agreement

- - Legally binding enforceable contract

- - Includes interest, schedule, remedies

- - Provides comprehensive legal protection

- - Admissible as primary evidence in court

IOU

- - Informal acknowledgment of debt

- - Usually lacks detailed terms

- - Limited legal enforceability

- - Better than nothing, but minimal protection

Recommendation: An IOU is better than a verbal agreement, but a loan agreement is far superior for any amount you would be upset to lose. The small effort of creating a proper loan agreement can save thousands in unrecoverable losses.

Loan Agreement vs Security Agreement

Loan Agreement

- - Establishes the loan itself and its terms

- - Covers principal, interest, repayment, default

- - May reference but does not create the security interest

Security Agreement

- - Creates the lender's interest in collateral

- - Describes collateral and lender's rights

- - Usually accompanies a loan agreement for secured loans

When to use both: For secured loans, you typically need both a loan agreement (documenting the loan terms) and a security agreement (granting the lender rights in the collateral). For unsecured loans, only the loan agreement is needed.

How to Create a Loan Agreement: A 10-Step Guide

A well-drafted loan agreement protects both the lender and borrower by clearly documenting every aspect of the lending arrangement. Follow these steps to create a comprehensive, enforceable agreement.

Identify the Parties

Document the full legal names, addresses, and contact information of both the lender and borrower. For business loans, include the legal entity name, state of incorporation, and the name and title of the authorized signatory. If a personal guarantor is involved, include their information as well. Accurate identification prevents disputes about who is bound by the agreement.

Define the Loan Amount and Disbursement

Specify the exact principal amount of the loan in both numbers and words (e.g., 'Twenty-Five Thousand Dollars ($25,000.00)'). State how and when the funds will be disbursed — as a single lump sum, in installments, or as a line of credit. Include any conditions that must be met before disbursement, such as the borrower providing certain documents or the lender verifying certain information.

Set the Interest Rate

Choose an interest rate that complies with your state's usury laws. For family loans, ensure the rate meets or exceeds the IRS Applicable Federal Rate (AFR) for the loan term. Specify whether the interest is simple or compound, the compounding period (if compound), and whether the rate is fixed or variable. If variable, define the index rate and margin. Include the total interest that will be paid over the life of the loan for transparency.

Establish the Repayment Schedule

Define when and how the borrower will make payments — monthly, quarterly, or on a custom schedule. Specify the payment amount (calculated using an amortization formula), the first and last payment dates, and how payments are applied (typically to interest first, then principal). Attach a complete amortization schedule showing the principal, interest, and remaining balance for each payment period.

Include Late Payment and Default Provisions

Define what constitutes a late payment (e.g., more than 10 or 15 days past due), the late fee amount or percentage, and when the loan is considered in default. Common default triggers include missed payments, breach of covenants, bankruptcy filing, and material misrepresentation. Specify the cure period (if any) and the remedies available to the lender, including acceleration of the full balance, seizure of collateral, and recovery of collection costs and attorney's fees.

Address Collateral (If Secured)

If the loan is secured, describe the collateral in detail — make, model, VIN for vehicles; legal description for real estate; serial numbers for equipment. Reference the separate security agreement and any UCC financing statements or liens that will be filed. Specify the lender's rights regarding the collateral upon default, including the right to repossess, foreclose, or sell the collateral to satisfy the debt.

Include Prepayment Terms

State whether the borrower can prepay the loan in whole or in part without penalty. If a prepayment penalty applies (and is legal in your state for your loan type), specify the penalty amount and the period during which it applies. Many personal and consumer loans prohibit prepayment penalties by state law, so verify compliance before including one.

Add Borrower Representations and Covenants

Include representations (statements of fact the borrower makes at the time of signing) such as legal capacity, authority to enter the agreement, no pending litigation, and accuracy of financial information provided. Include covenants (ongoing obligations) such as maintaining insurance on collateral, providing annual financial statements, notifying the lender of material changes, and not taking on additional debt above a specified threshold.

Specify Governing Law and Dispute Resolution

Designate which state's laws govern the agreement and how disputes will be resolved — through litigation in a specified court, binding arbitration, or mediation followed by arbitration. Include a provision for the prevailing party to recover reasonable attorney's fees and costs, which incentivizes both parties to act in good faith and discourages frivolous disputes.

Execute the Agreement

Both parties should sign and date the agreement. While notarization is not typically required for loan agreements to be valid, it is recommended for loans over $10,000 and strongly recommended for secured loans. Provide each party with a signed original. If a security agreement is involved, file the UCC financing statement with the Secretary of State or record the lien with the county recorder as appropriate.

Key Components of a Loan Agreement

A comprehensive loan agreement addresses every aspect of the lending relationship. Each component serves a specific purpose in protecting the parties and ensuring clear expectations.

| Component | Description |

|---|---|

| Party Identification | Full legal names, addresses, and contact information of lender and borrower (and guarantor if applicable) |

| Principal Amount | The exact amount being lent, stated in both numbers and written words to prevent ambiguity |

| Interest Rate | Annual percentage rate, whether simple or compound, fixed or variable, and total interest over the loan term |

| Repayment Schedule | Payment frequency, amount, first and last payment dates, and how payments are applied (interest vs principal) |

| Amortization Schedule | Complete table showing principal, interest, and remaining balance for each payment period |

| Late Fee Provision | Grace period, late fee amount or percentage, and when and how late fees are assessed |

| Default Provisions | Events that constitute default including missed payments, covenant breaches, bankruptcy, and material misrepresentation |

| Remedies | Lender's rights upon default including acceleration, collateral seizure, and recovery of attorney's fees and costs |

| Collateral Description | For secured loans, detailed description of the pledged collateral and reference to the security agreement |

| Prepayment Terms | Whether early repayment is permitted and any prepayment penalties (where legally allowed) |

| Representations & Warranties | Statements of fact by the borrower regarding their legal capacity, financial condition, and authority to borrow |

| Covenants | Ongoing obligations of the borrower including insurance maintenance, financial reporting, and debt limitations |

| Governing Law | The state whose laws govern the agreement's interpretation and enforcement |

| Dispute Resolution | Whether disputes will be resolved through litigation, arbitration, or mediation, and the venue |

| Signatures & Date | Both parties' signatures, printed names, and the date of execution |

Interest Rates & Usury Laws

Understanding interest rate rules is critical for any loan agreement. Charging an interest rate that exceeds your state's usury limit can result in severe penalties, while charging too little on a family loan can trigger IRS gift tax consequences.

State Usury Limits

Every state sets maximum interest rates for private loans. Limits range from 5% to 45% or more depending on the state and loan type. Penalties for violating usury laws include forfeiture of all interest, civil penalties up to three times the usurious interest, and in some states criminal prosecution. Always verify your state's limit before setting an interest rate.

IRS Applicable Federal Rate (AFR)

For loans between family members, the IRS requires a minimum interest rate equal to the AFR for the loan's term (short-term: 0-3 years, mid-term: 3-9 years, long-term: 9+ years). The AFR is published monthly by the IRS. Charging less than the AFR may cause the IRS to impute interest income to the lender and treat the difference as a taxable gift.

Important:Some states treat loan origination fees, processing fees, and other charges as "disguised interest" that counts toward the usury limit. When determining whether your total cost of borrowing exceeds the usury cap, include all fees and charges — not just the stated interest rate. Our templates include usury-compliant interest rate guidance and fee calculations for your state.

Legal Requirements for Loan Agreements

Loan agreements must comply with contract law principles, state usury laws, and potentially consumer lending regulations. Understanding these requirements ensures your agreement is valid, enforceable, and protects both parties.

- Mutual Consent: Both parties must voluntarily agree to the loan terms. The agreement must be free from fraud, duress, undue influence, or misrepresentation. Both parties must have legal capacity to enter a contract (be of legal age and sound mind).

- Consideration: The lender provides value (the loan proceeds) and the borrower provides value (the promise to repay with interest). This mutual exchange of value is the consideration that makes the contract binding.

- Usury Compliance: The interest rate must not exceed your state's maximum for the applicable loan type. Include all fees and charges when calculating whether the effective rate is within the usury limit.

- Written Documentation: While oral loan agreements may be enforceable for small amounts in some states, the Statute of Frauds in most states requires contracts that cannot be performed within one year to be in writing. Any loan with a term exceeding one year should be documented in a written agreement.

- Truth in Lending (TILA): If the lender regularly extends credit (not just an occasional personal loan), the federal Truth in Lending Act may apply, requiring specific disclosures about the loan's APR, finance charges, total payments, and other terms. TILA generally does not apply to one-time private loans between individuals.

Sample Loan Agreement

Below is a condensed preview of our personal loan agreement template.

LOAN AGREEMENT

Personal Loan Between Individuals

This Loan Agreement ("Agreement") is entered into as of[Date], by and between [Lender Name]("Lender") and [Borrower Name]("Borrower").

1. LOAN AMOUNT

Lender agrees to loan Borrower the principal sum of $[Amount]([Amount in Words] Dollars), to be disbursed on or before [Date].

2. INTEREST

The outstanding principal balance shall accrue simple interest at the rate of[Rate]% per annum. Total interest over the loan term: $[Total Interest].

3. REPAYMENT

Borrower shall repay the loan in [Number]equal monthly installments of $[Payment Amount], commencing on [First Payment Date]and continuing on the same day of each month thereafter...

4. LATE PAYMENT

If any payment is not received within [Days]days of its due date, Borrower shall pay a late fee of[Amount or %]...

5. DEFAULT

The following shall constitute events of default: (a) failure to make any payment within [Days] days of its due date; (b) breach of any representation, warranty, or covenant; (c) Borrower files for bankruptcy or becomes insolvent...

Frequently Asked Questions

Find answers to common questions about loan agreements, interest rates, usury laws, collateral, default remedies, and tax implications.

Official Resources

For additional information on lending laws, usury limits, consumer protection, and IRS requirements for private loans, consult these official resources.

CFPB - Consumer Financial Protection

Federal consumer lending regulations and borrower protections

IRS - Applicable Federal Rates

Monthly AFR tables for family and below-market loans

ULC - Uniform Commercial Code

UCC Article 9 secured transactions information and state adoption

FTC - Truth in Lending Act

Federal Truth in Lending Act text and consumer lending requirements

SBA - Business Loans

Small Business Administration loan programs and resources

Create your Loan Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.