What Is an Unsecured Promissory Note?

An unsecured promissory note is a legally binding loan agreement where the borrower promises to repay a specified amount without pledging any collateral. Unlike a secured note, the lender has no claim on specific property if the borrower defaults — the lender relies entirely on the borrower's creditworthiness and promise to pay.

Unsecured promissory notes are commonly used for personal loans between family and friends, small business loans, employee loans, and situations where the borrower lacks suitable collateral. Because the lender bears more risk, unsecured notes typically carry higher interest rates and shorter repayment periods compared to secured notes.

While the lack of collateral increases risk for the lender, a well-drafted unsecured note still provides important legal protections. The note creates a legally enforceable obligation, establishes clear repayment terms, and gives the lender the right to pursue collection through the courts if the borrower defaults.

No Collateral Needed

Based solely on the borrower's promise to repay

Personal Guarantee

Optional personal guarantee for business borrowers

Court Remedies

Enforceable through small claims court or civil litigation

Unsecured Promissory Note by State

Each state has different usury limits, statutes of limitations, small claims court limits, and garnishment rules that affect unsecured promissory notes. Select your state below for a template that complies with your state's specific requirements.

Risks & Collection Remedies

The primary risk of an unsecured promissory note is that the lender has no collateral to seize if the borrower defaults. However, several collection remedies are available:

Higher Risk for Lenders

Without collateral, recovery after default depends entirely on the borrower's assets and income. Consider requiring a personal guarantee, charging a higher interest rate, or limiting the loan amount to manage risk.

Formal Demand Letter

Send a written demand for payment, specifying the amount owed, the original note terms, and a deadline to pay. This creates a paper trail and often prompts payment without further action.

Credit Reporting

Report the delinquent debt to credit bureaus (Equifax, Experian, TransUnion). This damages the borrower's credit score and creates strong motivation to resolve the debt. You must follow the Fair Credit Reporting Act (FCRA) requirements.

Small Claims Court

If the amount owed falls within your state's small claims limit, file in small claims court. It's fast, affordable, and doesn't require a lawyer. Bring the signed note, payment records, and evidence of default.

Civil Lawsuit & Judgment

For larger amounts, file a civil lawsuit. If successful, the court issues a judgment that enables wage garnishment, bank account levies, and property liens to collect the debt.

Personal Guarantees for Unsecured Notes

When lending to a business entity (LLC, corporation, partnership), a personal guarantee from the business owner or key principal is critical protection for unsecured loans. Without a personal guarantee, the lender can only pursue the business entity's assets, which may be minimal.

A personal guarantee makes the guarantor personally liable for the full debt, allowing the lender to pursue their personal assets — bank accounts, real estate, vehicles, investments — if the business fails to pay. This effectively bridges the gap between an unsecured note's higher risk and a secured note's collateral protection.

Key Components of an Unsecured Promissory Note

A well-drafted unsecured promissory note must include all essential loan terms and strong default provisions to protect the lender in the absence of collateral.

| Component | Description |

|---|---|

| Borrower & Lender Names | Full legal names and addresses of both parties |

| Principal Amount | Total loan amount in numbers and words |

| Interest Rate | Annual rate, must comply with state usury laws (typically higher for unsecured) |

| Payment Schedule | Monthly payments, due dates, and total repayment timeline |

| Maturity Date | Date when remaining balance is due in full |

| Late Payment Penalties | Late fees and default interest rates for missed payments |

| Default & Acceleration | Events of default, cure period, and acceleration clause making full balance due |

| Personal Guarantee | Optional guarantee from business owner or third party |

| Signatures | Dated signatures of borrower, lender, and guarantor (if applicable) |

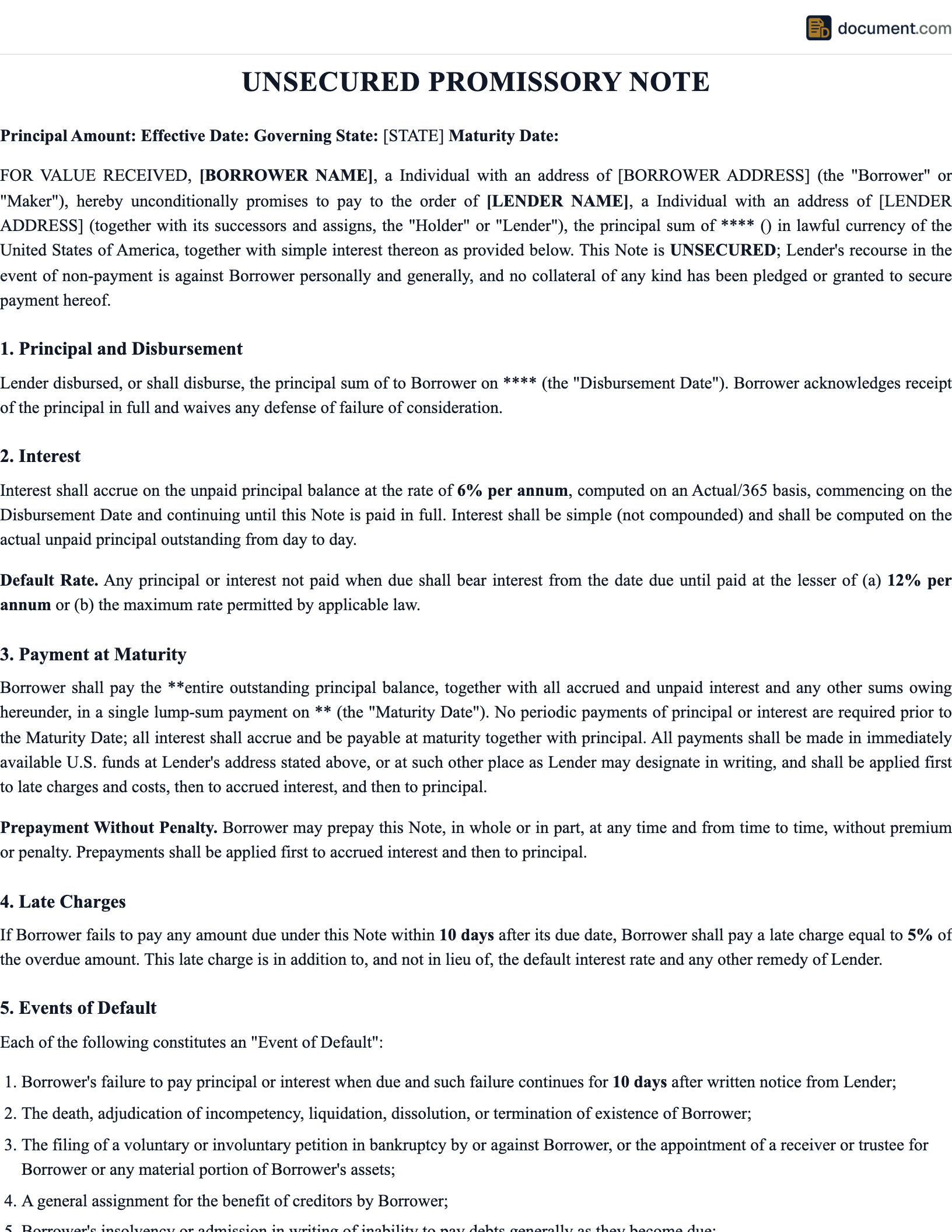

Sample Unsecured Promissory Note

Below is a preview of our unsecured promissory note template. Your customized document will include all terms, default provisions, and optional personal guarantee.

UNSECURED PROMISSORY NOTE

No Collateral Loan Agreement

This Unsecured Promissory Note is entered into on [Date] between:

LENDER:

Name: [Lender Name]

Address: [Lender Address]

BORROWER:

Name: [Borrower Name]

Address: [Borrower Address]

1. PRINCIPAL & INTEREST

Principal: $[Amount]

Interest Rate: [Rate]% per annum

This note is UNSECURED. No collateral has been pledged.

Frequently Asked Questions

Find answers to common questions about unsecured promissory notes, collection remedies, and personal guarantees.

Create your Unsecured Promissory Note in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.