Minnesota Unsecured Promissory Note Overview

An unsecured promissory note in Minnesota is a loan agreement where the borrower promises to repay without pledging any collateral. The lender relies on the borrower's creditworthiness and the legally enforceable promise to pay. The maximum interest rate in Minnesota is 8% (default).

8% default rate; no general usury cap for written agreements; consumer loans subject to specific schedules. Unsecured notes carry more risk for the lender, so interest rates are typically higher than secured notes. However, the rate must still comply with Minnesota's usury laws.

If the borrower defaults, the lender's primary remedy is filing a lawsuit within Minnesota's statute of limitations (6 years (oral and written)). The small claims court limit in Minnesota is $15,000, which is ideal for smaller unsecured loans.

8% (default)

Usury rate cap

6 years

Statute of limitations

$15,000

Small claims limit

25%

Max garnishment

Minnesota Legal Requirements

Minnesota has specific requirements for unsecured promissory notes:

Important: Minnesota Usury Laws

Minnesota's maximum interest rate is 8% (default). 8% default rate; no general usury cap for written agreements; consumer loans subject to specific schedules. Exceeding this limit may void the interest or result in penalties.

- Written Agreement: Must be in writing, signed by borrower, clearly stating loan terms

- Compliant Interest Rate: Must not exceed Minnesota's 8% (default) usury cap

- No Collateral Statement: Explicitly state that the note is unsecured with no collateral pledged

- Default Provisions: Events of default, cure period, acceleration clause, and collection remedies

- Personal Guarantee: Recommended for business borrowers to protect the lender

- Governing Law: Specify Minnesota law as the governing jurisdiction

Collection Remedies in Minnesota

If a borrower defaults on an unsecured promissory note in Minnesota, the lender has several collection options:

Send a Formal Demand Letter

Written notice demanding payment within a specified timeframe, creating a paper trail

File in Small Claims Court ($15,000 limit)

Fast, affordable, no attorney required for amounts within the limit

File a Civil Lawsuit

For amounts above small claims limits, file in Minnesota civil court

Enforce the Judgment

Up to 25% of disposable earnings. Bank account levies and property liens also available

Statute of Limitations in Minnesota

The statute of limitations for collecting on a promissory note in Minnesota is 6 years (oral and written). After this period, the lender loses the right to file a lawsuit to enforce the note.

| Aspect | Minnesota Rule |

|---|---|

| Usury Rate | 8% (default) |

| Statute of Limitations | 6 years (oral and written) |

| Small Claims Limit | $15,000 |

| Garnishment Rules | Up to 25% of disposable earnings |

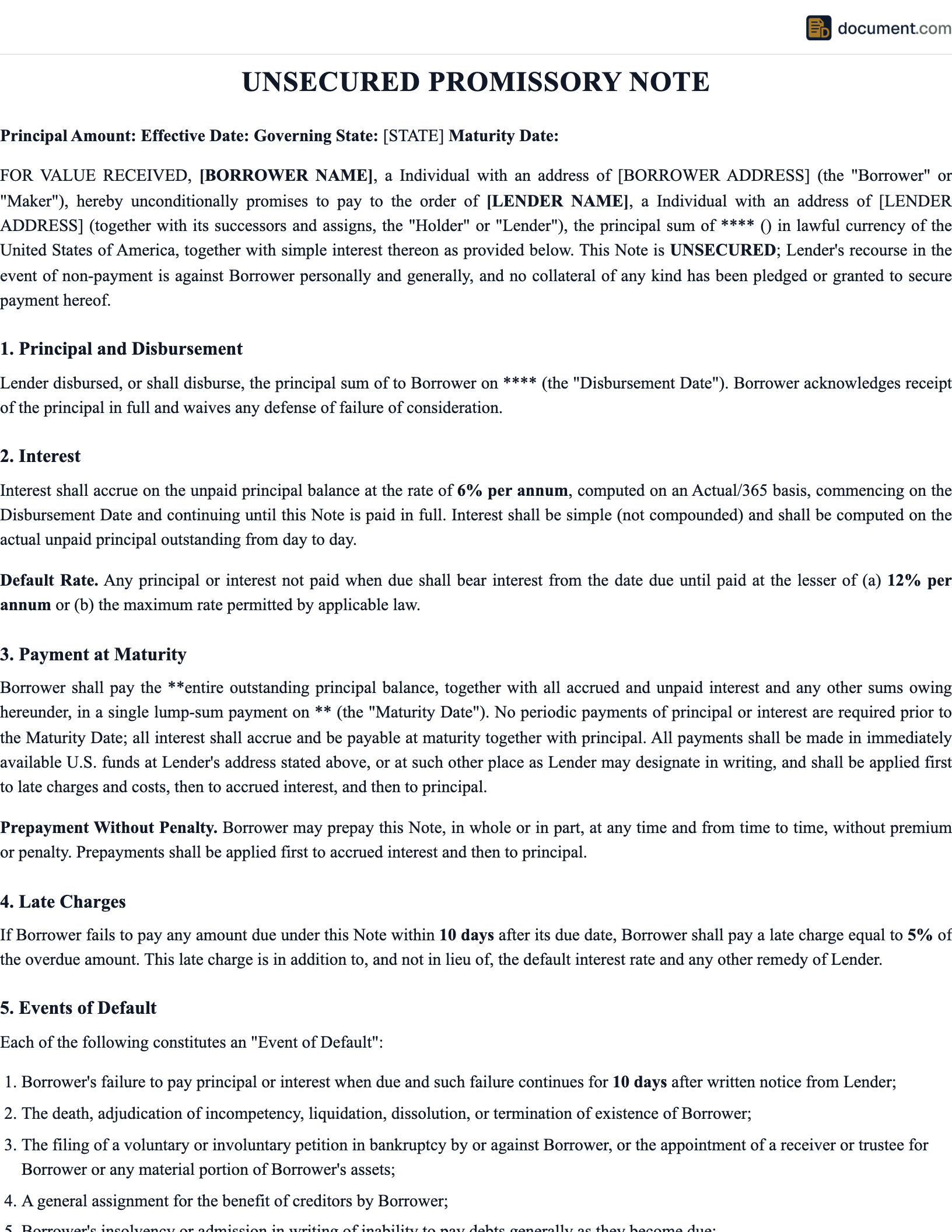

Sample Minnesota Unsecured Promissory Note

Below is a preview of our Minnesota-specific unsecured promissory note template.

STATE OF MINNESOTA

UNSECURED PROMISSORY NOTE

No Collateral Loan Agreement

LENDER:

Name: [Lender Name]

Address: [Minnesota Address]

BORROWER:

Name: [Borrower Name]

Address: [Minnesota Address]

LOAN TERMS

Principal: $[Amount]

Interest: [Rate]% per annum (max 8% (default) in MN)

This note is UNSECURED. No collateral has been pledged.

Minnesota Unsecured Promissory Note FAQ

Answers to common questions about unsecured promissory notes and collection procedures in Minnesota.

Official Minnesota Resources

Use these official resources for Minnesota lending laws and court procedures.

Other Minnesota Promissory Note Types

Need a different type of promissory note for Minnesota?

Create your Minnesota Unsecured Promissory Note in under 5 minutes.

Answer a few questions and download a Minnesota-compliant document, ready for the state agency.