What Is a Secured Promissory Note?

A secured promissory note is a legally binding loan agreement where the borrower pledges specific property (collateral) to guarantee repayment. If the borrower fails to repay, the lender has the legal right to seize and sell the collateral to recover the outstanding debt. This provides significantly more protection for the lender compared to an unsecured promissory note.

Secured notes are commonly used for large loans, real estate transactions, vehicle financing, equipment purchases, and business lending. The collateral backing reduces risk for the lender, which typically results in more favorable terms for the borrower — including lower interest rates and longer repayment periods.

To be fully enforceable, a secured promissory note should include a detailed description of the collateral and a security agreement. The lender should also “perfect” their security interest by filing a UCC-1 financing statement (for personal property) or recording a mortgage or deed of trust (for real estate) with the appropriate government office.

Collateral-Backed

Specific property pledged to guarantee loan repayment

Lien Perfection

UCC-1 filing establishes priority over other creditors

Default Remedies

Foreclosure or repossession rights if borrower defaults

Secured Promissory Note by State

Each state has different laws governing secured transactions, UCC filings, foreclosure procedures, usury limits, and deficiency judgments. Select your state below for a template that complies with your state's specific requirements.

Types of Collateral for Secured Notes

Almost any property of value can serve as collateral for a secured promissory note. The type of collateral determines how the security interest is perfected and what remedies are available upon default.

Real Property

Residential or commercial real estate used as collateral, secured by a mortgage or deed of trust

Vehicles

Cars, trucks, boats, and other titled vehicles secured through a lien on the vehicle title

Equipment

Business equipment, machinery, and tools pledged as security for the loan

Accounts Receivable

Outstanding invoices and future receivables assigned as collateral for business financing

Inventory

Raw materials, work-in-progress, and finished goods pledged to secure business loans

Securities & Investments

Stocks, bonds, and other financial instruments pledged as loan collateral

UCC-1 Filing & Lien Perfection

Perfecting your security interest is critical to protecting your rights as a lender. Without proper perfection, your claim on the collateral may be subordinate to other creditors or unenforceable in bankruptcy.

Critical: File Your UCC-1 Immediately

Priority among creditors is generally determined by the date of filing. If another creditor files a UCC-1 on the same collateral before you, they will have priority. File your UCC-1 as soon as the loan is signed to protect your position.

Create the Security Agreement

The security agreement is the contract between borrower and lender that creates the security interest. It must describe the collateral, be signed by the borrower (debtor), and state that the borrower grants a security interest to the lender (secured party). This is typically included as part of the secured promissory note or as a separate attachment.

File the UCC-1 Financing Statement

File UCC-1 with your state's Secretary of State (or equivalent filing office). The form requires the debtor's legal name, the secured party's name, and a description of the collateral. Filing fees range from $20 to $50 in most states. For real property collateral, you'll record a mortgage or deed of trust with the county recorder instead.

Monitor and Renew

UCC-1 filings are effective for 5 years. If the loan extends beyond 5 years, file a UCC-3 continuation statement within 6 months before expiration. When the loan is fully repaid, file a UCC-3 termination statement to release the lien. Monitor the debtor's name and legal status — if the debtor changes their legal name, you may need to amend the filing.

Key Components of a Secured Promissory Note

A well-drafted secured promissory note must include all essential loan terms plus detailed collateral provisions. Missing any of these elements could make the note unenforceable or leave the lender's security interest unperfected.

| Component | Description |

|---|---|

| Borrower & Lender Names | Full legal names and addresses of both parties |

| Principal Amount | Total loan amount in numbers and words |

| Interest Rate | Annual rate, must comply with state usury laws |

| Payment Schedule | Monthly/quarterly payments, due dates, and amortization |

| Maturity Date | Date when remaining balance is due in full |

| Collateral Description | Detailed description of pledged property (VIN, serial number, address, etc.) |

| Security Agreement | Grant of security interest, perfection requirements, insurance obligations |

| Default & Remedies | Events of default, cure period, repossession/foreclosure rights, deficiency claims |

| Signatures | Dated signatures of borrower and lender (notarization recommended) |

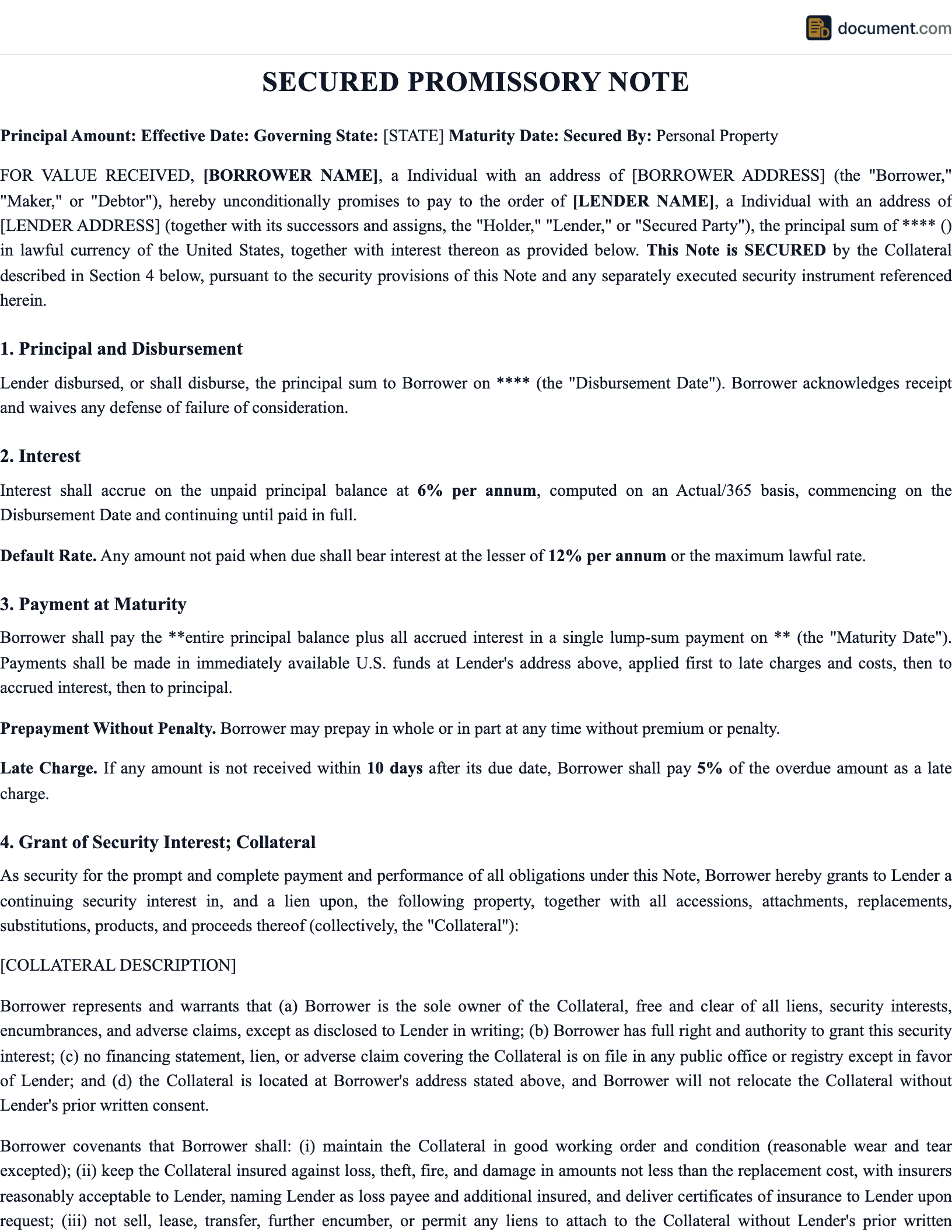

Sample Secured Promissory Note

Below is a preview of our secured promissory note template. Your customized document will include all terms, collateral description, security agreement, and default provisions.

SECURED PROMISSORY NOTE

Collateral-Backed Loan Agreement

This Secured Promissory Note is entered into on[Date]between:

LENDER (Secured Party):

Name: [Lender Name]

Address: [Lender Address]

BORROWER (Debtor):

Name: [Borrower Name]

Address: [Borrower Address]

1. PRINCIPAL & INTEREST

Principal: $[Amount]

Interest Rate: [Rate]% per annum

2. COLLATERAL

Description: [Collateral Description]

Estimated Value: $[Value]

Frequently Asked Questions

Find answers to common questions about secured promissory notes, collateral requirements, and UCC filings.

Create your Secured Promissory Note in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.