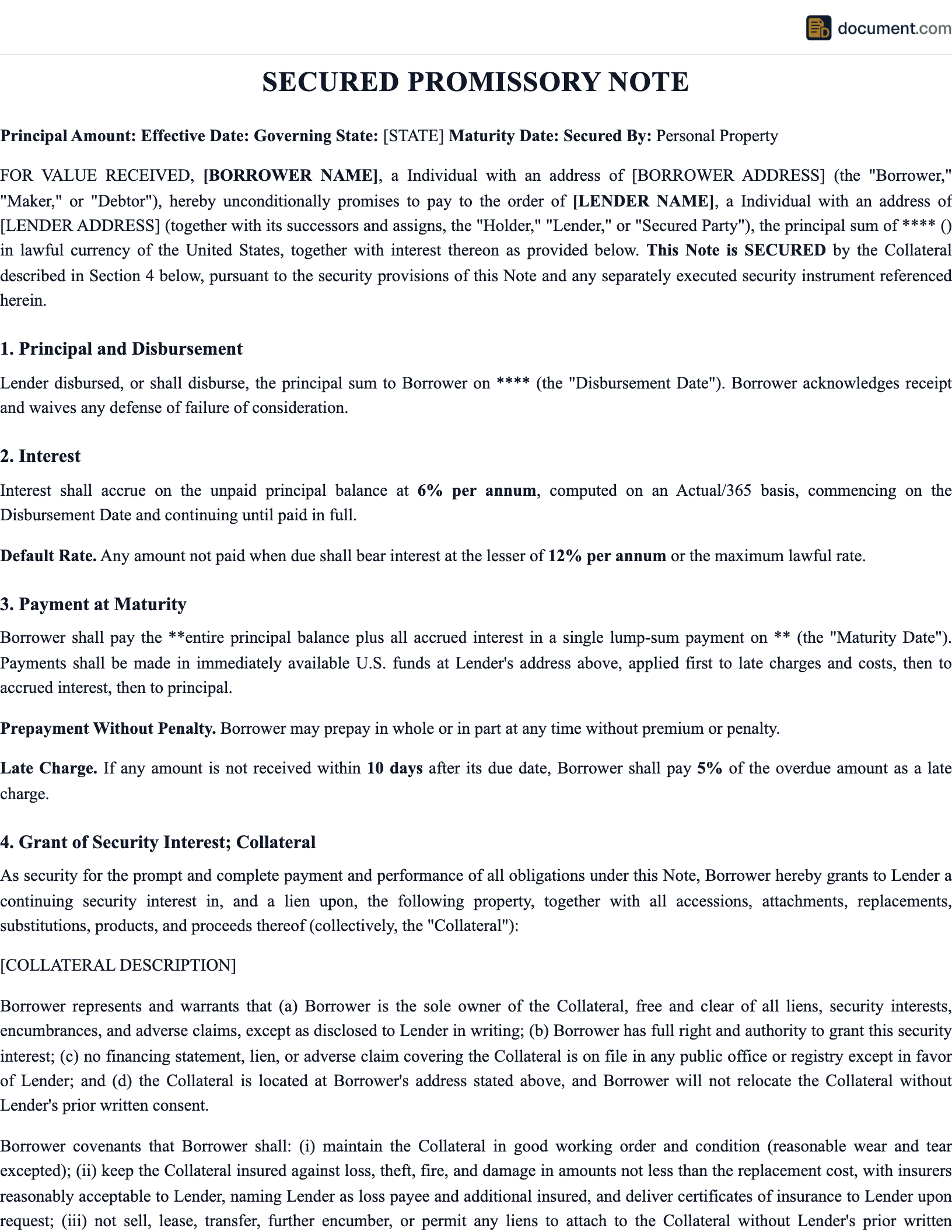

North Carolina Secured Promissory Note Overview

A secured promissory note in North Carolina is a loan agreement where the borrower pledges specific collateral to guarantee repayment. North Carolina law governs the creation, perfection, and enforcement of security interests under the Uniform Commercial Code (UCC) as adopted by the state. The maximum interest rate for most loans in North Carolina is 8%.

8% per annum general cap; 16% for loans under $25,000; higher rates for certain licensed lenders; consumer finance rates regulated by statute. Lenders should verify that the agreed-upon interest rate complies with North Carolina's usury laws before finalizing the note. Charging interest above the legal limit can result in severe penalties, including forfeiture of interest and potential civil liability.

For secured notes involving real property in North Carolina, non-judicial (power of sale, most common) foreclosure applies. Understanding your state's foreclosure process is critical because it determines the timeline, costs, and lender's rights in the event of borrower default.

8%

Usury rate cap

Secretary of State

UCC filing office

Non-judicial

Foreclosure type

Yes

Deficiency judgment

North Carolina Legal Requirements

North Carolina has specific requirements for secured promissory notes. Here's what you need to ensure your note is enforceable under NC law:

Important: North Carolina Usury Laws

North Carolina's maximum interest rate is 8%. 8% per annum general cap; 16% for loans under $25,000; higher rates for certain licensed lenders; consumer finance rates regulated by statute. Exceeding the legal limit may void the interest portion of your note or result in civil penalties.

Essential Elements

- Written Agreement: The note must be in writing, signed by the borrower, and clearly state the loan terms

- Compliant Interest Rate: Must not exceed North Carolina's 8% usury cap

- Collateral Description: Specific, identifiable description of all pledged property

- Security Agreement: Grant of security interest signed by the borrower (debtor)

- UCC-1 Filing: Filed with the Secretary of State, UCC Division for personal property collateral

- Default Provisions: Clear events of default, cure periods, and remedies including foreclosure/repossession rights

UCC Filing in North Carolina

To perfect a security interest in personal property in North Carolina, the lender must file a UCC-1 financing statement with the Secretary of State, UCC Division. This public filing puts other creditors on notice and establishes the lender's priority in the collateral.

Prepare the UCC-1 Form

Include the debtor's exact legal name, secured party name, and detailed collateral description

File with the Secretary of State

Submit online or by mail with the required filing fee

Monitor and Renew

UCC-1 filings last 5 years; file a continuation statement before expiration

Terminate After Payoff

File a UCC-3 termination statement when the loan is fully repaid

North Carolina Foreclosure & Repossession

North Carolina uses non-judicial (power of sale, most common) foreclosure for real property collateral. For personal property (vehicles, equipment, inventory), the lender generally has the right to repossess the collateral without court action, provided it can be done without breaching the peace.

Regarding deficiency judgments in North Carolina: Yes, within 90 days of foreclosure. The lender must follow North Carolina's specific procedures for disposing of collateral in a commercially reasonable manner, providing proper notice to the borrower before any sale.

| Aspect | North Carolina Rule |

|---|---|

| Foreclosure Type | Non-judicial (power of sale, most common) |

| Deficiency Judgment | Yes, within 90 days of foreclosure |

| Statute of Limitations | 3 years (oral), 10 years (written contracts sealed), 6 years (written simple contracts) |

| Usury Rate | 8% |

| UCC Filing Office | Secretary of State, UCC Division |

Sample North Carolina Secured Promissory Note

Below is a preview of our North Carolina-specific secured promissory note. Your customized document will include all terms compliant with NC law.

STATE OF NORTH CAROLINA

SECURED PROMISSORY NOTE

Collateral-Backed Loan Agreement

LENDER (Secured Party):

Name: [Lender Name]

Address: [North Carolina Address]

BORROWER (Debtor):

Name: [Borrower Name]

Address: [North Carolina Address]

LOAN TERMS

Principal: $[Amount]

Interest: [Rate]% per annum (max 8% in NC)

Collateral: [Description]

North Carolina Secured Promissory Note FAQ

Answers to common questions about secured promissory notes, UCC filings, and collateral requirements in North Carolina.

Official North Carolina Resources

Use these official resources to verify North Carolina requirements, file UCC documents, and access state legal information.

Other North Carolina Promissory Note Types

Need a different type of promissory note for North Carolina? We offer state-specific templates for every type.

North Carolina Unsecured Promissory Note

No collateral required

North Carolina Demand Promissory Note

Payable on demand, no fixed maturity

General Promissory Note

Standard promissory note template

North Carolina Loan Agreement

Comprehensive loan documentation

North Carolina Bill of Sale

Document property transfers

Create your North Carolina Secured Promissory Note in under 5 minutes.

Answer a few questions and download a North Carolina-compliant document, ready for the state agency.