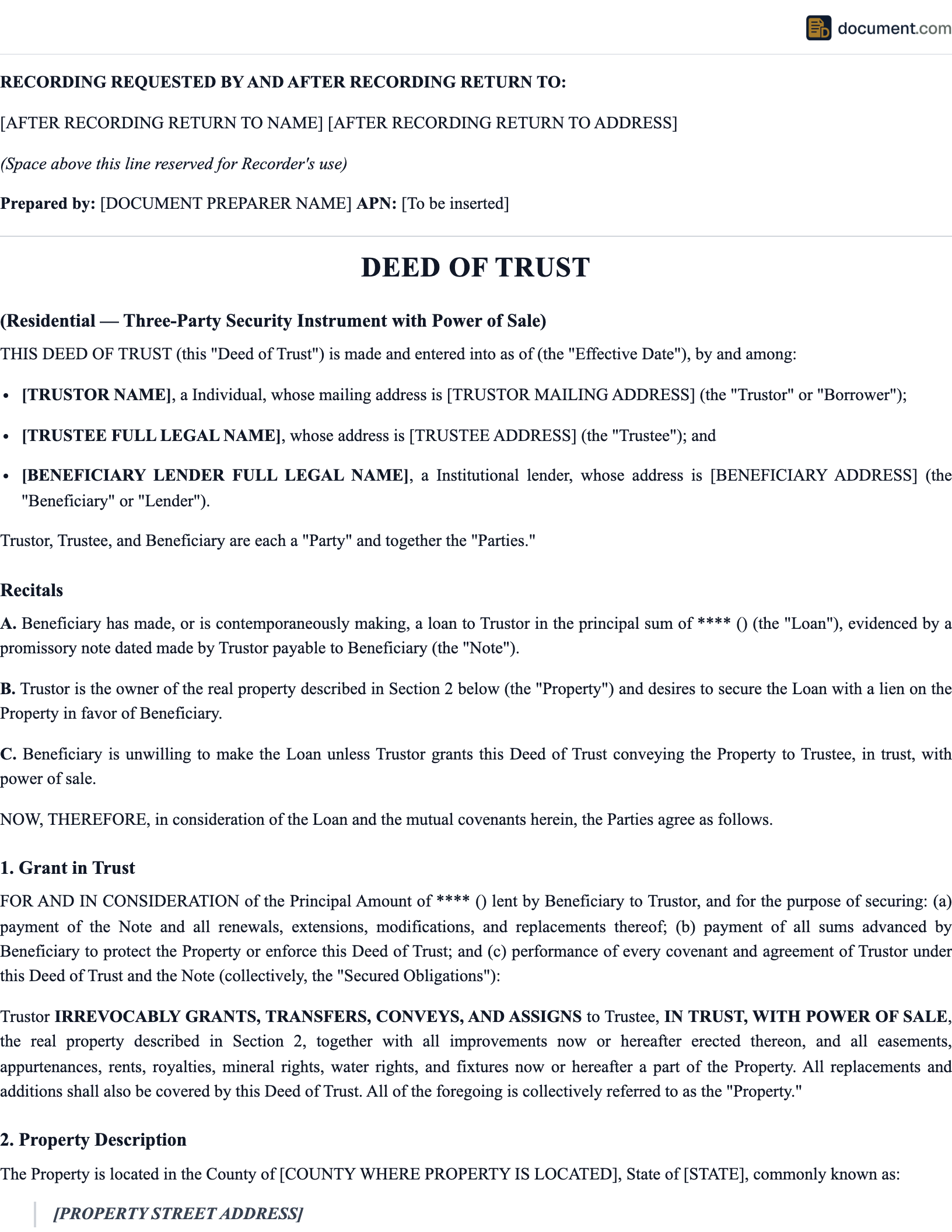

What Is a Deed of Trust?

A deed of trust is a legal instrument used in real estate financing that creates a three-party security arrangement to secure a loan against real property. Unlike a traditional mortgage, which involves only two parties (the borrower and the lender), a deed of trust introduces a neutral third party — the trustee — who holds legal title to the property as collateral for the loan. This three-party structure is the defining characteristic of a deed of trust and is what distinguishes it from a mortgage in both function and foreclosure process.

The three parties to a deed of trust are the trustor (the borrower, who conveys legal title to the trustee), the beneficiary (the lender, who holds the promissory note and benefits from the security), and the trustee(a neutral third party, typically a title company, escrow company, or attorney, who holds bare legal title in trust). The borrower retains equitable title and all practical rights of ownership — they live in the home, make improvements, and can sell the property — while the trustee's role is purely administrative and security-related.

The primary advantage of a deed of trust over a mortgage is the power of sale clause, which authorizes the trustee to sell the property through a non-judicial foreclosure process if the borrower defaults on the loan. Non-judicial foreclosure is significantly faster and less expensive than judicial foreclosure (the process required with a mortgage), which is why approximately thirty states have adopted the deed of trust as the preferred real estate security instrument. From the lender's perspective, the ability to foreclose without court involvement reduces both the cost and the timeline of recovering their collateral.

A deed of trust is always used in conjunction with a promissory note, which is a separate document containing the actual loan terms — the principal amount, interest rate, payment schedule, maturity date, and default provisions. The deed of trust references the promissory note and secures the borrower's repayment obligation by creating a lien on the property. Both documents are executed at the loan closing, but only the deed of trust is recorded with the county recorder's office to provide public notice of the lender's security interest.

Three-Party Security

Trustor, beneficiary, and trustee work together to secure real property financing

Power of Sale

Enables non-judicial foreclosure, saving time and expense for all parties

~30 State Standard

Used as the primary security instrument in approximately thirty states

Deed of Trust by State

Not every state uses deeds of trust — some rely on traditional mortgages instead. Select your state below for a template aligned with local trustee, recording, and non-judicial foreclosure rules.

The Three Parties to a Deed of Trust

The three-party structure is what makes a deed of trust unique among real estate security instruments. Each party has a distinct role, specific legal obligations, and clearly defined rights. Understanding these roles is essential for anyone involved in a real property financing transaction that uses a deed of trust.

Trustor (Borrower)

The trustor is the borrower who takes out the loan and conveys legal title to the trustee as security. Despite transferring legal title, the trustor retains equitable titleand all practical rights of ownership — the right to live in the property, make improvements, collect rental income, and sell the property (subject to the lender's due-on-sale clause). The trustor's primary obligations are to make timely loan payments, maintain property insurance, pay property taxes, and keep the property in reasonable condition.

Key concept:The trustor's transfer of legal title to the trustee is a security measure only. The trustor is the owner for all practical purposes and appears as the owner on property tax records, insurance policies, and in everyday dealings with the property.

Beneficiary (Lender)

The beneficiary is the lender who provides the loan funds and holds the promissory note. The beneficiary benefits from the deed of trust because it gives them a secured interest in the property — if the borrower defaults, the beneficiary can instruct the trustee to exercise the power of sale and sell the property to recover the outstanding loan balance. The beneficiary has the right to assign the note and deed of trust to another lender (which commonly happens when loans are sold on the secondary market), to substitute a new trustee, and to release the deed of trust when the loan is paid in full.

Key concept: The beneficiary does not hold title to the property. They hold the promissory note, which is the evidence of the debt. The deed of trust is the security instrument that gives the beneficiary the right to have the property sold if the debt is not repaid.

Trustee (Neutral Third Party)

The trustee is a neutral third party — typically a title company, escrow company, or attorney — who holds bare legal title to the property in trust for the benefit of both the borrower and the lender. The trustee has no interest in the property and no right to use or profit from it. The trustee's role is entirely administrative: hold title as security during the loan, issue a deed of reconveyance when the loan is paid off, or exercise the power of sale if the borrower defaults. The beneficiary can substitute a new trustee at any time by recording a substitution of trustee document.

Key concept:The trustee holds "bare" or "naked" legal title — title in name only, with no right of possession, use, or benefit. The trustee is a fiduciary who must act impartially in the interests of both the borrower and the lender.

Deed of Trust Form Preview

Below is a visual preview of the sections and fields included in a standard deed of trust. This mockup illustrates the structure and level of detail our templates provide. Your completed document will be fully formatted, professionally styled, and customized for your state's specific recording requirements.

Deed of Trust

With Power of Sale

Section 1: Trustor (Borrower)

Section 2: Beneficiary (Lender)

Section 3: Trustee

Section 4: Property Description

Section 5: Promissory Note Reference

Key Clauses Included

Deed of Trust vs Mortgage: The Key Distinction

This is the most important distinction in real estate security instruments. Although people often use "mortgage" and "deed of trust" interchangeably in casual conversation, they are fundamentally different legal documents with different structures and different foreclosure consequences. The choice between them is typically determined by state law rather than by the parties to the transaction.

The practical significance of this distinction becomes apparent when a borrower defaults. In a mortgage state, the lender must file a lawsuit, serve the borrower, go through court proceedings, and obtain a judicial decree before the property can be sold — a process that can take six to eighteen months or longer and costs the lender thousands of dollars in legal fees. In a deed of trust state, the trustee can sell the property through a non-judicial process — recording notices, publishing advertisements, and conducting a public auction — typically completing the foreclosure in four to six months at a fraction of the cost.

| Feature | Deed of Trust | Mortgage |

|---|---|---|

| Parties | Three (trustor, beneficiary, trustee) | Two (mortgagor, mortgagee) |

| Title Held By | Trustee holds bare legal title | Borrower holds full title (lien theory) |

| Foreclosure Type | Non-judicial (power of sale) | Judicial (court proceeding) |

| Foreclosure Timeline | 4-6 months | 6-18+ months |

| Court Involvement | Not required (unless challenged) | Required |

| Cost of Foreclosure | Lower (no litigation costs) | Higher (attorney fees, court costs) |

| States Using | ~30 states | ~20 states |

| Lien Release | Deed of reconveyance from trustee | Satisfaction/discharge from lender |

Important note:In everyday language, most people refer to their home loan as a "mortgage" regardless of whether the actual security instrument is a mortgage or a deed of trust. If you are buying a home in California, Texas, Colorado, Arizona, or any other deed of trust state, the document you sign at closing to secure the loan is a deed of trust — even though everyone casually calls it a "mortgage."

How a Deed of Trust Works

A deed of trust operates as a security device throughout the life of the loan. From execution at closing through reconveyance at payoff (or foreclosure upon default), the deed of trust creates a framework of rights and obligations for all three parties. Here is how the process unfolds from beginning to end.

Execution at Closing

At the loan closing, the borrower signs both the promissory note (the debt obligation) and the deed of trust (the security instrument). By signing the deed of trust, the borrower conveys bare legal title to the named trustee while retaining equitable title and possession. The deed of trust is then recorded with the county recorder's office, creating a public lien on the property.

During the Loan Period

While the loan is in good standing, the deed of trust sits quietly in the public record. The borrower makes payments, maintains the property, pays property taxes and insurance, and enjoys all rights of ownership. The trustee has no active role during this period. The lender may sell or assign the note and deed of trust on the secondary market, and the lender may substitute a new trustee — both common occurrences that do not affect the borrower's rights.

Loan Payoff — Reconveyance

When the borrower pays off the loan in full — whether through regular payments over the full term, refinancing, or sale of the property — the lender notifies the trustee that the loan has been satisfied. The trustee then records a deed of reconveyance with the county recorder, releasing the lien and returning full legal title to the borrower.

Default — Non-Judicial Foreclosure

If the borrower defaults on the loan, the lender instructs the trustee to exercise the power of sale. The trustee initiates non-judicial foreclosure by recording a notice of default, waiting through the reinstatement period, publishing a notice of sale, and conducting a public auction. The property is sold to the highest bidder, and the trustee issues a trustee's deed to the purchaser.

Non-Judicial Foreclosure: The Power of Sale

The power of sale clause is the defining feature of a deed of trust and the primary reason lenders in approximately thirty states prefer this instrument over a mortgage. The power of sale authorizes the trustee to sell the property at a public auction if the borrower defaults, without the need for court involvement. This non-judicial process is governed entirely by state statute, which prescribes the specific notices, timelines, and procedures the trustee must follow.

How Non-Judicial Foreclosure Proceeds

Notice of Default

The trustee records a notice of default with the county recorder and sends it to the borrower by certified mail. This notice states the amount of the default and gives the borrower a specified period (typically 90 days) to cure the default by paying the past-due amount plus any fees and costs.

Reinstatement Period

During the reinstatement period, the borrower has the right to cure the default by paying the overdue payments, late fees, and foreclosure costs. If the borrower cures the default, the trustee records a notice of rescission and the deed of trust continues as before. The specific reinstatement period varies by state.

Notice of Trustee's Sale

If the borrower does not cure the default, the trustee records and publishes a notice of trustee's sale, specifying the date, time, and location of the public auction. The notice must be published in a newspaper of general circulation and posted on the property. State law specifies the minimum notice period, typically 21 to 30 days.

Trustee's Sale (Public Auction)

The trustee conducts a public auction, selling the property to the highest bidder. The opening bid is typically the outstanding loan balance plus costs and fees. If no third party bids higher, the lender acquires the property (called a credit bid). The winning bidder pays in cash or certified funds, and the trustee issues a trustee's deed transferring title.

Borrower protections: Even in non-judicial foreclosure states, borrowers have significant protections. These include the right to cure during the reinstatement period, the right to receive proper notice, the right to challenge the foreclosure in court if proper procedures were not followed, and in some states, a right of redemption after the sale (allowing the borrower to reclaim the property by paying the full sale price within a specified period).

Reconveyance: What Happens When the Loan Is Paid Off

Reconveyance is the process by which the deed of trust lien is removed from the property when the loan is paid in full. This is the positive outcome that every borrower works toward — the moment when the property is truly free and clear of the lender's security interest. Reconveyance is a critical step because, until it is completed, the deed of trust remains on the property's title record even though the debt has been satisfied.

When the borrower makes the final loan payment (or the loan is paid off through refinancing or sale), the lender sends a payoff demand letter and instructions to the trustee confirming that the loan has been satisfied. The trustee then prepares a deed of reconveyance(also called a full reconveyance, release of deed of trust, or satisfaction of deed of trust depending on the state) and records it with the county recorder's office. This recorded document removes the lien from the property's chain of title, confirming to the public that the borrower owns the property free of that particular encumbrance.

Timely Reconveyance

Most states require the trustee or lender to record the reconveyance within 21 to 60 days after the loan is paid in full. Failure to do so may result in statutory penalties. In California, the penalty is $300 plus actual damages; other states impose similar fines.

Missing Reconveyance

If reconveyance is not recorded, the deed of trust remains on your title record even though the debt is paid. This can create problems when you try to sell or refinance the property. Contact the lender and trustee in writing to demand reconveyance, or consult an attorney.

Key Provisions of a Deed of Trust

A comprehensive deed of trust contains numerous provisions that define the rights, obligations, and remedies of each party. These provisions are not merely boilerplate — each one serves a specific legal purpose and can have significant consequences for the borrower, lender, and trustee. Understanding these provisions helps you know what you are agreeing to when you sign a deed of trust.

| Provision | Purpose |

|---|---|

| Power of Sale | Authorizes the trustee to sell the property through non-judicial foreclosure if the borrower defaults, without court involvement |

| Acceleration Clause | Allows the lender to demand full repayment of the remaining loan balance upon default, rather than waiting for missed payments to accumulate |

| Due-on-Sale (Alienation) | Requires the loan to be paid in full if the borrower sells or transfers the property, preventing assumption of the loan without lender approval |

| Insurance Requirement | Obligates the borrower to maintain hazard insurance on the property with the lender named as loss payee, protecting the collateral |

| Tax Payment Obligation | Requires the borrower to pay property taxes when due, preventing tax liens that would take priority over the deed of trust |

| Property Maintenance | Requires the borrower to maintain the property in good condition, preventing waste that would diminish the collateral's value |

| Subordination | Establishes the priority of the deed of trust relative to other liens and encumbrances on the property |

| Legal Description | Precisely identifies the property being encumbered using the legal description from the county records, not just the street address |

| Reconveyance | Obligates the trustee to release the lien and return clear title when the loan is paid in full, specifying the process and timeline |

| Substitution of Trustee | Allows the lender to replace the trustee at any time by recording a substitution of trustee document with the county |

| Assignment | Permits the lender to sell or assign the note and deed of trust to another party, common when loans are sold on the secondary market |

| Governing Law | Specifies which state's laws govern the deed of trust, typically the state where the property is located |

Which States Use Deeds of Trust vs Mortgages

Whether a state uses deeds of trust or mortgages (or both) is determined by state law and historical practice. The distinction is not academic — it directly affects the foreclosure process, timeline, and cost that applies when a borrower defaults. Understanding which instrument your state uses is essential for anyone buying, selling, or financing real property.

Deed of Trust States (~30)

These states primarily use deeds of trust with non-judicial foreclosure through the power of sale. Major deed of trust states include:

California, Texas, Virginia, Colorado, Arizona, Oregon, Washington, Nevada, Idaho, Montana, Utah, Tennessee, North Carolina, Missouri, Mississippi, West Virginia, Alaska, Wyoming, the District of Columbia, Maryland, Minnesota (both), Michigan (both), and others.

Mortgage States (~20)

These states primarily use mortgages with judicial foreclosure through the court system. Major mortgage states include:

New York, Florida, New Jersey, Illinois, Ohio, Connecticut, Pennsylvania, Massachusetts, Indiana, Wisconsin, Iowa, Kansas, Louisiana, Maine, New Hampshire, North Dakota, South Carolina, South Dakota, Vermont, and others.

Dual-instrument states:Several states allow both mortgages and deeds of trust, and the choice is often left to the lender. In these states (including California, Virginia, Michigan, and Minnesota), most institutional lenders prefer the deed of trust because of the faster and less expensive non-judicial foreclosure process. If you are uncertain which instrument applies to your loan, check the security document you signed at closing — the title of the document will tell you.

Recording Requirements

A deed of trust must be recorded with the county recorder's office (or equivalent office, depending on the state) in the county where the property is located. Recording is not optional — it is essential for the deed of trust to be effective against third parties. Without recording, the lender's security interest in the property is not part of the public record, meaning a subsequent purchaser or lender could take the property free of the unrecorded lien.

Recording also establishes lien priority— the general rule is "first in time, first in right," meaning the first-recorded lien has priority over later-recorded liens. This is critical in foreclosure because senior liens are paid before junior liens from the sale proceeds. If a second deed of trust was recorded after the first, and the first deed of trust is foreclosed, the second deed of trust is extinguished and the second lender loses their security.

- Notarization: The deed of trust must be signed by the trustor (borrower) and notarized before it can be recorded. The notary verifies the signer's identity and confirms that the signature is voluntary.

- Formatting: Many counties have specific formatting requirements for recorded documents, including minimum margins (typically 1 inch on sides and bottom, 3 inches at top of first page), minimum font size (typically 10-point), and black ink on white paper.

- Recording Fees: Counties charge recording fees that vary by jurisdiction, typically ranging from $25 to $200 depending on the state, county, and document length. Some states also charge documentary transfer taxes based on the loan amount.

- Return Address: The document must include a return address where the recorded original (or certified copy) should be mailed after recording. This is typically the lender's or title company's address.

- Legal Description: The property must be identified by its legal description (lot, block, subdivision, or metes and bounds), not just the street address. The legal description must exactly match the county's property records.

How to Create a Deed of Trust

Creating a deed of trust requires attention to detail and compliance with your state's specific requirements. Our guided template walks you through each required field and automatically includes state-specific provisions based on your location.

Select Your State

Choose the state where the property is located. This determines the specific legal language, power of sale provisions, reconveyance requirements, recording format, and notice requirements that must be included. Our template automatically adjusts to comply with your state's laws.

Enter Party and Property Information

Provide the full legal names and addresses of the trustor (borrower), beneficiary (lender), and trustee. Enter the property's legal description, street address, and assessor's parcel number. Reference the promissory note terms including the principal amount, note date, and maturity date. All information must exactly match the promissory note and county records.

Review, Sign, and Record

Preview your completed deed of trust, verify all information for accuracy, and download in PDF or Word format. The trustor must sign the document in the presence of a notary public. Record the notarized deed of trust with the county recorder's office in the county where the property is located. The lender typically handles recording as part of the loan closing process.

Sample Deed of Trust

Below is a condensed preview of our deed of trust template. This sample shows the structure, language, and key provisions included in our attorney-reviewed documents. Your completed deed of trust will be fully customized for your state, your loan terms, and your specific parties.

DEED OF TRUST

With Power of Sale and Assignment of Rents

This Deed of Trust ("Deed of Trust") is made as of [Date], by [Trustor Name]("Trustor"), to [Trustee Name]("Trustee"), for the benefit of [Beneficiary Name]("Beneficiary").

PROPERTY DESCRIPTION

Trustor hereby irrevocably grants, transfers, and assigns to Trustee, in trust, with power of sale, the real property situated in [County], State of [State], described as: [Legal Description]

1. SECURED OBLIGATION

This Deed of Trust is given to secure payment of a promissory note dated [Date] in the principal amount of $[Amount], executed by Trustor in favor of Beneficiary, together with interest thereon and all renewals, extensions, and modifications thereof...

2. POWER OF SALE

If Trustor defaults in the payment of any sum secured hereby or in the performance of any obligation under this Deed of Trust or the Note, Beneficiary may declare all sums secured hereby immediately due and payable, and Trustee, at the request of Beneficiary, shall sell the Property at public auction to the highest bidder in accordance with the laws of the State of [State]...

3. INSURANCE AND TAXES

Trustor shall maintain hazard insurance on the Property in an amount not less than the outstanding balance of the Note, with Beneficiary named as loss payee. Trustor shall pay all property taxes, assessments, and governmental charges when due...

4. RECONVEYANCE

Upon payment in full of all sums secured by this Deed of Trust, Beneficiary shall instruct Trustee to reconvey the Property to Trustor. Trustee shall reconvey the Property without warranty and without charge to Trustor by recording a full reconveyance with the county recorder...

5. DUE-ON-SALE

If all or any part of the Property or any interest in it is sold or transferred without Beneficiary's prior written consent, Beneficiary may, at its option, declare all sums secured by this Deed of Trust immediately due and payable...

Frequently Asked Questions

Find answers to common questions about deeds of trust, including how they differ from mortgages, the role of the trustee, non-judicial foreclosure, reconveyance, and recording requirements.

Official Resources

For additional information on deeds of trust, real estate financing, foreclosure processes, and property recording requirements, consult these official and reputable resources.

CFPB - Housing Resources

Consumer Financial Protection Bureau guide to mortgages and real estate financing

ABA - Real Property Section

American Bar Association resources on real estate law and security instruments

Fannie Mae - Security Instruments

Fannie Mae standard deed of trust and mortgage forms and guidelines

Freddie Mac - Single-Family Forms

Freddie Mac standard security instrument forms for all 50 states

Nolo - Deeds of Trust Encyclopedia

Free legal information on deeds of trust, foreclosure, and reconveyance

HUD - Single Family Housing

U.S. Department of Housing and Urban Development single-family program resources

ALTA - Title Industry Resources

American Land Title Association resources on title insurance, recording, and lien priority

ULC - Real Property Acts

Uniform Law Commission model acts for real property and secured transactions

Create your Deed of Trust in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.