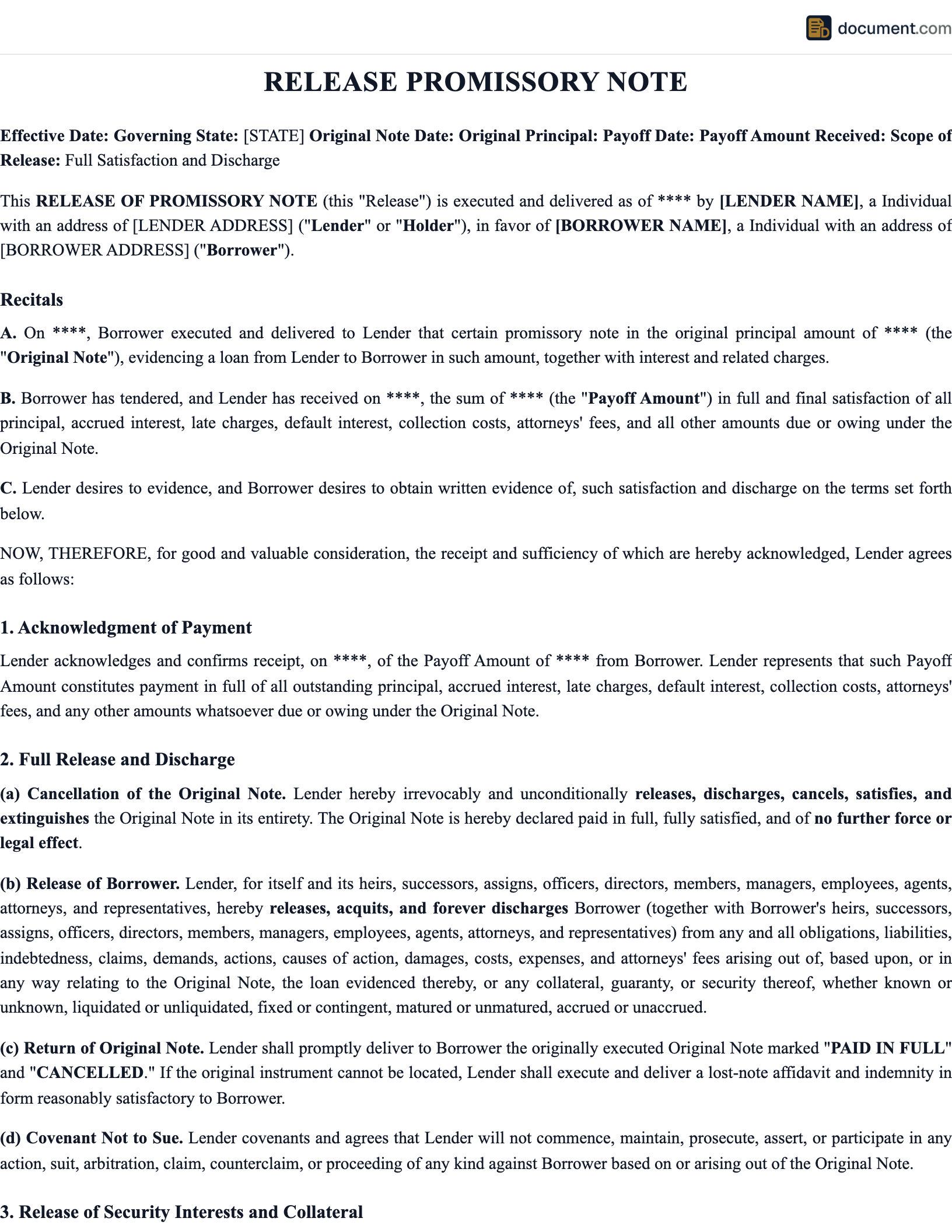

What Is a Promissory Note Release?

A promissory note release (also called a release of promissory note, satisfaction of note, or debt discharge) is a legal document signed by the lender that formally acknowledges the borrower has fulfilled their obligations under a promissory note and releases the borrower from any further liability. The release cancels the debt and provides the borrower with written proof that the obligation has been satisfied.

Obtaining a written release is critically important because a promissory note is a negotiable instrument — it can be transferred, sold, or assigned to third parties. Without a written release from the holder, a borrower who has paid in full has no protection against a subsequent holder claiming the note is still outstanding. The release should be obtained at the time of final payment and stored with the borrower's important financial records.

If the promissory note was secured by collateral, the release should be accompanied by the appropriate lien discharge documents — a UCC-3 termination statement for personal property, a satisfaction of mortgage for real property, or a lien release for titled vehicles. Failing to discharge the lien leaves a cloud on the borrower's title or credit record even after the debt is paid.

Debt Discharge

Formally cancels the borrower's obligation to repay the debt

Written Proof

Protects borrower against future claims on a negotiable instrument

Lien Removal

Triggers UCC-3 termination or mortgage satisfaction for secured notes

When to Use a Promissory Note Release Form

A release should be executed whenever a promissory note obligation ends, regardless of how the obligation was satisfied. Common situations include:

Full Payment of the Note

The borrower has made all scheduled payments (or a lump-sum payoff) and the entire principal and interest balance has been satisfied. This is the most straightforward release scenario.

Negotiated Settlement

The lender agrees to accept less than the full amount owed in exchange for immediate payment and a mutual release. The release should specify the settlement amount and confirm it constitutes full satisfaction of the debt.

Debt Forgiveness

The lender voluntarily forgives the remaining balance. Note that forgiven debt over $600 must be reported to the IRS on Form 1099-C and may constitute taxable income to the borrower.

Refinancing or Note Replacement

When an existing note is being replaced by a new note (refinancing), the original note should be formally released to prevent duplicate obligations and ensure clean title records.

Partial Release of Collateral

In a partial release, the borrower pays down a portion of the debt and the lender releases specific collateral while retaining a security interest in the remaining assets.

Full Release vs. Partial Release

The type of release depends on whether the entire obligation is being discharged or only a portion of it. Each has different legal implications and documentation requirements.

Full Release

Discharges the entire debt and all associated obligations.

- Entire balance paid or forgiven

- All collateral released simultaneously

- UCC-3 termination filed (if secured)

- Original note marked “PAID IN FULL” and returned

Partial Release

Releases specific collateral or reduces the obligation while the note remains active.

- Portion of balance paid

- Specific collateral released; remainder stays secured

- UCC-3 amendment filed (not termination)

- Note remains active for remaining balance

Lien Discharge & UCC-3 Termination

When a secured promissory note is paid off, releasing the borrower from the debt is only half the process. The lender must also discharge the associated lien to clear the borrower's property records.

Important: Lenders Must File Within 20 Days

Under UCC Article 9, a secured party is required to file a UCC-3 termination statement within 20 days of receiving an authenticated demand from the debtor after the secured obligation has been satisfied. Failure to file exposes the lender to statutory damages of $500 per violation in most states, plus actual damages if the borrower suffers harm.

| Collateral Type | Discharge Document | Filed With |

|---|---|---|

| Personal Property | UCC-3 Termination Statement | Secretary of State |

| Real Property (Mortgage) | Satisfaction of Mortgage | County Recorder |

| Real Property (Deed of Trust) | Reconveyance Deed | County Recorder |

| Vehicle | Lien Release / Title Release | State DMV |

| Unsecured Note | Release of Note (no lien to discharge) | Retained by borrower |

Key Components of a Promissory Note Release

A complete release form must contain enough detail to unambiguously identify the obligation being discharged and protect both parties from future disputes.

| Component | Description |

|---|---|

| Identification of Original Note | Date of original note, principal amount, parties, and any identifying number |

| Lender & Borrower Names | Full legal names matching the original promissory note |

| Satisfaction Statement | Acknowledgment that all obligations have been satisfied (or settlement terms) |

| Release Language | Express release of the borrower from all claims arising from the note |

| Collateral Release | If secured: description of collateral being released and lien discharge commitment |

| Lender's Signature | Dated signature of the lender/note holder (notarization recommended) |

Sample Promissory Note Release

Below is a preview of our promissory note release template. Your customized document will include all identification details, satisfaction language, and lien discharge provisions.

RELEASE OF PROMISSORY NOTE

Satisfaction and Discharge of Debt Obligation

This Release is executed on[Date]by the undersigned Lender:

LENDER (Releasing Party):

Name: [Lender Name]

Address: [Lender Address]

BORROWER (Released Party):

Name: [Borrower Name]

Address: [Borrower Address]

ORIGINAL PROMISSORY NOTE:

Date: [Note Date]

Principal: $[Amount]

Final Payment Received: $[Amount]

Frequently Asked Questions

Find answers to common questions about promissory note releases, lien discharges, and debt satisfaction procedures.

Create your Release Promissory Note in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.