What Is a Partnership Agreement?

A partnership agreement is the master contract between the people who own and operate a partnership business together. It defines who the partners are, what each contributes, how profits and losses are shared, who has management authority, what duties each partner owes the others, how disputes are resolved, and what happens when a partner wants to leave or the partnership winds down. In short, it converts a vague handshake understanding into an enforceable framework that lets the business operate predictably and protects every partner from the other partners' missteps.

Partnerships exist the moment two or more people associate to carry on a business for profit — no state filing is required for a general partnership to come into existence. This means many people are partners without realizing it. Two friends who start a side business, family members who co-manage a rental property, or three contractors who pool resources on a project have all formed a partnership in the eyes of the law, complete with joint and several liability for partnership debts. Without a written agreement, the Revised Uniform Partnership Act (RUPA) — adopted in some form by nearly every state — fills in the rules with defaults that almost never match how real partnerships operate.

RUPA's defaults split profits and losses equally regardless of unequal contributions, give every partner equal management authority regardless of experience or workload, treat every partner as an agent who can bind the partnership to outside contracts, and allow any partner to dissolve the partnership at will. A written partnership agreement lets you override every one of these defaults: weight profit allocations to capital contributions, require unanimous consent for major decisions, restrict who can sign contracts on behalf of the partnership, and prevent unilateral dissolution. The cost of putting these terms in writing is trivial compared to the cost of fighting about them later.

Partnerships come in three main flavors. A general partnership (GP) is the default form: every partner manages the business and bears unlimited personal liability for partnership debts. A limited partnership (LP) has at least one general partner managing the business and one or more limited partners who contribute capital but cannot participate in management without losing their limited liability shield. A limited liability partnership (LLP) is a registered form where every partner enjoys protection from the malpractice and wrongful acts of fellow partners — the dominant structure for law firms, accounting firms, and other licensed professional practices.

Whether you are forming a two-person consulting practice, a multi-family real estate investment vehicle, a professional services LLP, or a complex limited partnership with outside investors, our attorney-reviewed templates give you a thorough framework that addresses the dozens of issues every partnership needs to think through. Each template is configurable for your partnership type and the laws of your state, with optional clauses for capital calls, drag-along rights, non-compete restrictions, and dispute resolution.

Clear Roles

Defines who decides what, who signs contracts, and how disagreements get resolved before they become disputes

Custom Profit Splits

Override the default 50/50 rule to reflect actual capital, time, and value each partner brings

Exit Protection

Defines buyout values and procedures so a partner's departure does not destroy the business

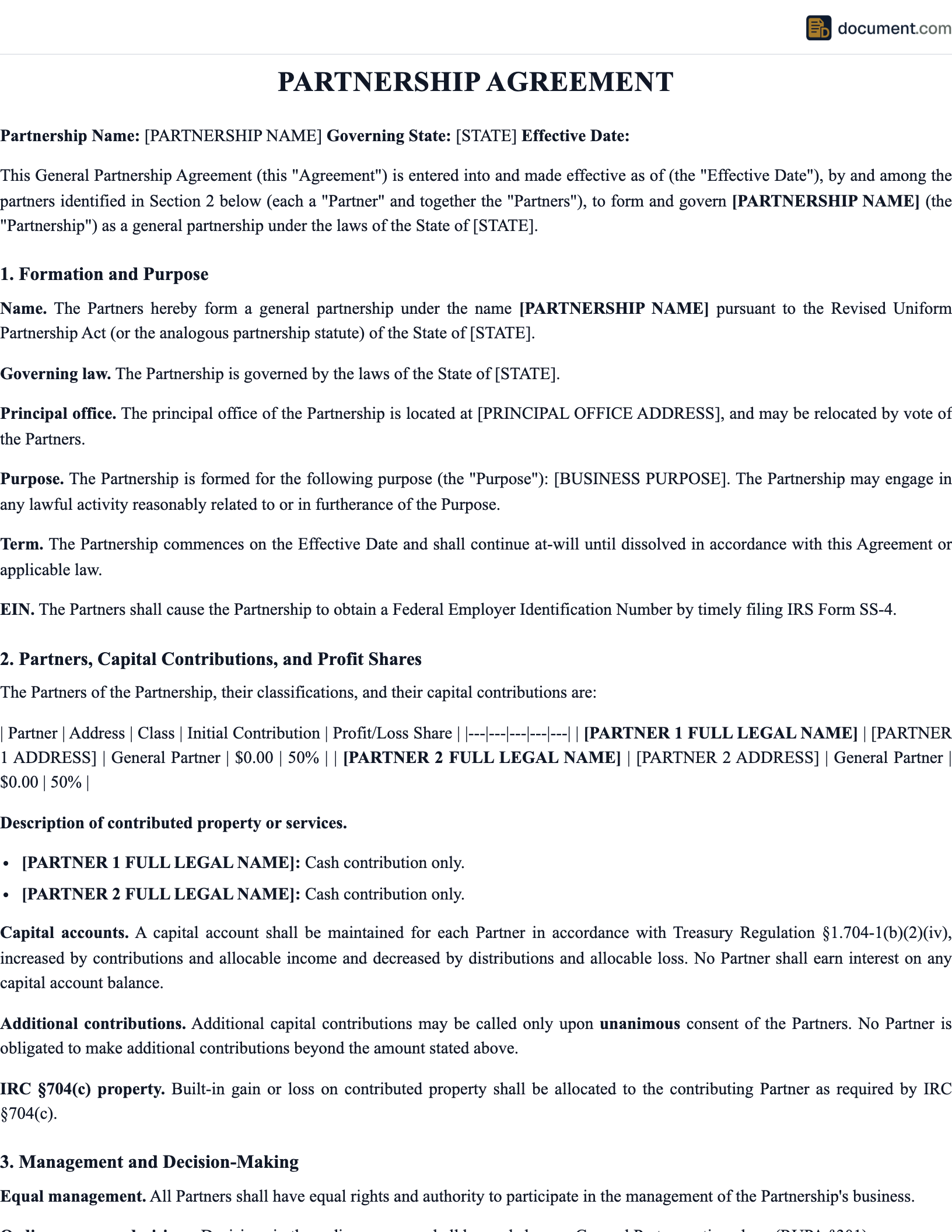

Partnership Agreement Form Preview

Below is a preview of the major sections of a typical general partnership agreement. Your completed document will be fully formatted and customized for your partnership type, state, and the specific terms you negotiate.

Partnership Agreement

General Partnership

Section 1: Partnership Name & Purpose

Section 2: Partners & Capital Contributions

Section 3: Profit & Loss Allocation

Net profits and losses shall be allocated to the Partners in proportion to their Percentage Interests as set forth in Section 2, after first paying each Partner an annual preferred return of 6% on the unreturned balance of their capital account.

Section 4: Management & Voting

Day-to-day operations shall be managed by majority vote of the Partners. The following matters require unanimous consent: admission of a new partner, sale of substantially all partnership assets, incurring debt in excess of $50,000, and amendment of this Agreement.

Section 5: Signatures

Types of Partnerships

Choosing the right partnership form drives liability exposure, management structure, tax treatment, and the formalities required to maintain the entity in good standing.

Limited Partnership (LP)

One or more general partners run the business while limited partners contribute capital with liability capped at their investment

Real Estate Partnership

Used to acquire, develop, manage, or invest in real property, often as a limited partnership for tax and liability reasons

50 50

Partnership agreement between two equal partners sharing ownership, profits, and decisions 50/50

Amendment

Modify an existing partnership agreement to update partners, ownership splits, or operating terms

Dissolution

Formally dissolve a partnership, wind down operations, and divide assets among outgoing partners

Limited Liability

Limited liability partnership agreement protecting each partner from liability for the others' misconduct

Capital Contributions

Capital contributions are what each partner puts into the business in exchange for an ownership interest. They can take many forms, and each form has different tax and accounting consequences.

Cash

The cleanest form of contribution — straightforward valuation, no tax issues, immediately available for partnership use.

Property

Real estate, equipment, vehicles, or inventory. Must be valued at fair market value. Built-in gain or loss on contributed property is allocated back to the contributing partner under §704(c).

Services (Sweat Equity)

A partner can earn an interest in exchange for past or future services. The IRS treats receipt of a capital interest for services as immediate taxable compensation; receipt of a profits interest can be tax-free if structured under Rev. Proc. 93-27.

Intellectual Property

Patents, trademarks, copyrights, customer lists, and trade secrets. Often the most valuable contribution at startup but the trickiest to value defensibly.

Debt Forgiveness

A partner can convert a loan to the partnership into capital, increasing their capital account by the forgiven amount.

Future Contribution Obligations

The agreement can require partners to make additional capital calls when needed, with specified consequences (dilution, loss of voting rights, forced buyout) for failure to fund.

Profit & Loss Allocation

How partners share the financial results of the business is one of the most important — and most negotiated — provisions in any partnership agreement. RUPA's default is equal sharing regardless of contribution; almost every written agreement overrides this.

Pro Rata to Capital Contributions

Profits and losses are allocated in proportion to each partner's capital contribution. Simple and aligned with investment, but does not credit partners for time or expertise.

Negotiated Fixed Percentages

Partners agree to fixed percentages that may differ from capital contribution percentages — often used to credit a working partner who contributes time and skill instead of cash.

Preferred Return Plus Pro Rata Split

Each partner first receives an annual preferred return (typically 6% to 10%) on their unreturned capital, after which remaining profits are split in agreed percentages. Common in real estate partnerships.

Waterfall Distributions

Multi-tiered allocation that returns capital first, then preferred returns, then promotes to working partners — standard in private equity and real estate partnerships with passive investors.

Fiduciary Duties

Partners owe each other and the partnership two principal fiduciary duties under RUPA: the duty of loyalty and the duty of care, plus a contractual obligation of good faith and fair dealing.

Duty of Loyalty

Account for all profits derived from partnership business, refrain from self-dealing without disclosure and consent, and refrain from competing with the partnership.

Duty of Care

Refrain from grossly negligent or reckless conduct, intentional misconduct, and knowing violations of law in conducting partnership business.

Good Faith & Fair Dealing

An overriding obligation that cannot be eliminated by agreement; it requires partners to perform their duties honestly and not in a manner that destroys the other partners' reasonable expectations.

Information & Books

Every partner has the right to access partnership books and records, and partners must furnish information about partnership affairs to one another on demand.

Partnership vs Other Documents

| Document | Entity Type | Liability |

|---|---|---|

| Partnership Agreement | GP, LP, or LLP | Unlimited (GP) or limited (LP/LLP) |

| LLC Operating Agreement | Limited Liability Company | Limited for all members |

| Joint Venture Agreement | Project-specific collaboration | Depends on structure |

| Founders' Agreement | Pre-incorporation startup | Becomes corp/LLC at incorporation |

| Shareholder Agreement | Corporation | Limited to investment |

How to Create a Partnership Agreement

- 1

Choose the partnership form

Decide whether you need a GP, LP, or LLP based on liability exposure, management structure, and licensing requirements.

- 2

Identify all partners

List every partner by full legal name, address, and the role each will play in the business.

- 3

Define contributions and percentages

Document who is contributing what (cash, property, IP, services) and what ownership percentage each receives.

- 4

Spell out profit and loss allocations

Decide whether allocations track ownership percentages or follow a custom formula, preferred return, or waterfall.

- 5

Establish management and voting

Identify who decides what — daily operations, major decisions, admission of new partners, sale of assets.

- 6

Address fiduciary duties and outside activities

Modify (but do not eliminate) the default duties to fit how the partnership actually operates.

- 7

Plan for departures and dissolution

Specify buyout procedures, valuation methods, payment terms, and what triggers dissolution.

- 8

Sign, file, and store the agreement

All partners sign; LP and LLP forms must also file with the state. Keep the original with the partnership records.

Key Components

Name & Purpose

Identifies the partnership and the scope of the business it will conduct.

Term

Whether the partnership is at-will or for a fixed term tied to a project or date.

Capital Contributions

What each partner contributes, the agreed value, and any future contribution obligations.

Capital Accounts

How each partner's capital balance is tracked over time.

Profit & Loss Allocations

The formula for sharing financial results, including any preferred returns or waterfalls.

Distributions

When cash is paid out and in what order — often distinct from tax allocations.

Management & Voting

Who manages day-to-day operations and which decisions require supermajority or unanimous consent.

Books, Records & Tax Matters

Accounting method, fiscal year, tax matters partner, audit rights.

Transfer Restrictions

Limits on transferring partnership interests to outsiders.

Dissociation & Buyout

What happens when a partner leaves, dies, becomes disabled, or is expelled.

Dissolution & Winding Up

The events that trigger dissolution and how partnership affairs are wound up.

Dispute Resolution

Mediation and arbitration provisions to keep disputes out of court.

Dissolution & Winding Up

Dissolution is the legal end of the partnership; winding up is the process of completing unfinished business, paying creditors, and distributing the remaining assets. Under RUPA, events triggering dissolution include the partners voting to dissolve, expiration of a fixed term, completion of a defined undertaking, the occurrence of an event specified in the agreement, a court order, or a partner's wrongful conduct.

- All partnership debts and obligations to creditors (including partners with loans to the partnership) are paid first

- Remaining assets are then distributed to partners in accordance with their positive capital account balances

- Any partner with a negative capital account must contribute the deficit back to the partnership

- The agreement can override these defaults to provide for in-kind distributions, sale of the business as a going concern, or buyout by remaining partners

Sample Partnership Agreement Language

RECITALS. The Partners desire to associate themselves as general partners under the laws of the State of [State] for the purpose of conducting the business described herein, and to set forth their respective rights and obligations to one another and to the Partnership.

SECTION 3 — CAPITAL CONTRIBUTIONS. Each Partner has contributed to the capital of the Partnership the cash and property set forth opposite the Partner's name on Schedule A. No Partner shall be required to make any additional capital contribution except by unanimous written consent of all Partners or pursuant to a Capital Call duly issued under Section 4.

SECTION 6 — ALLOCATIONS & DISTRIBUTIONS. Net profits and net losses of the Partnership for each fiscal year shall be allocated to the Partners in proportion to their Percentage Interests, after first allocating to each Partner an amount equal to a six percent (6%) annual preferred return on the unreturned balance of such Partner's capital account. Cash distributions shall be made not less frequently than quarterly to the extent of available cash, after providing for working capital reserves determined in good faith by the Managing Partners.

SECTION 9 — MANAGEMENT. The day-to-day business and affairs of the Partnership shall be managed by a Managing Partner elected annually by majority vote of the Partners. Notwithstanding the foregoing, the following actions shall require the affirmative vote or written consent of Partners holding at least seventy-five percent (75%) of the Percentage Interests: (i) admission of a new Partner; (ii) sale, lease, or other disposition of substantially all of the Partnership's assets; (iii) merger or consolidation; (iv) incurring debt in excess of $100,000; and (v) amendment of this Agreement.

SECTION 14 — DISSOCIATION. A Partner's voluntary withdrawal, death, permanent disability, bankruptcy, or expulsion shall constitute a Dissociation Event. The Partnership shall continue with the remaining Partners and shall purchase the dissociated Partner's interest at the Buyout Price determined under Section 15, payable over a period not to exceed five (5) years.

Frequently Asked Questions

Official Resources

Ready to Form Your Partnership?

Build a partnership agreement tailored to your partners and state in minutes.

Create Partnership Agreement