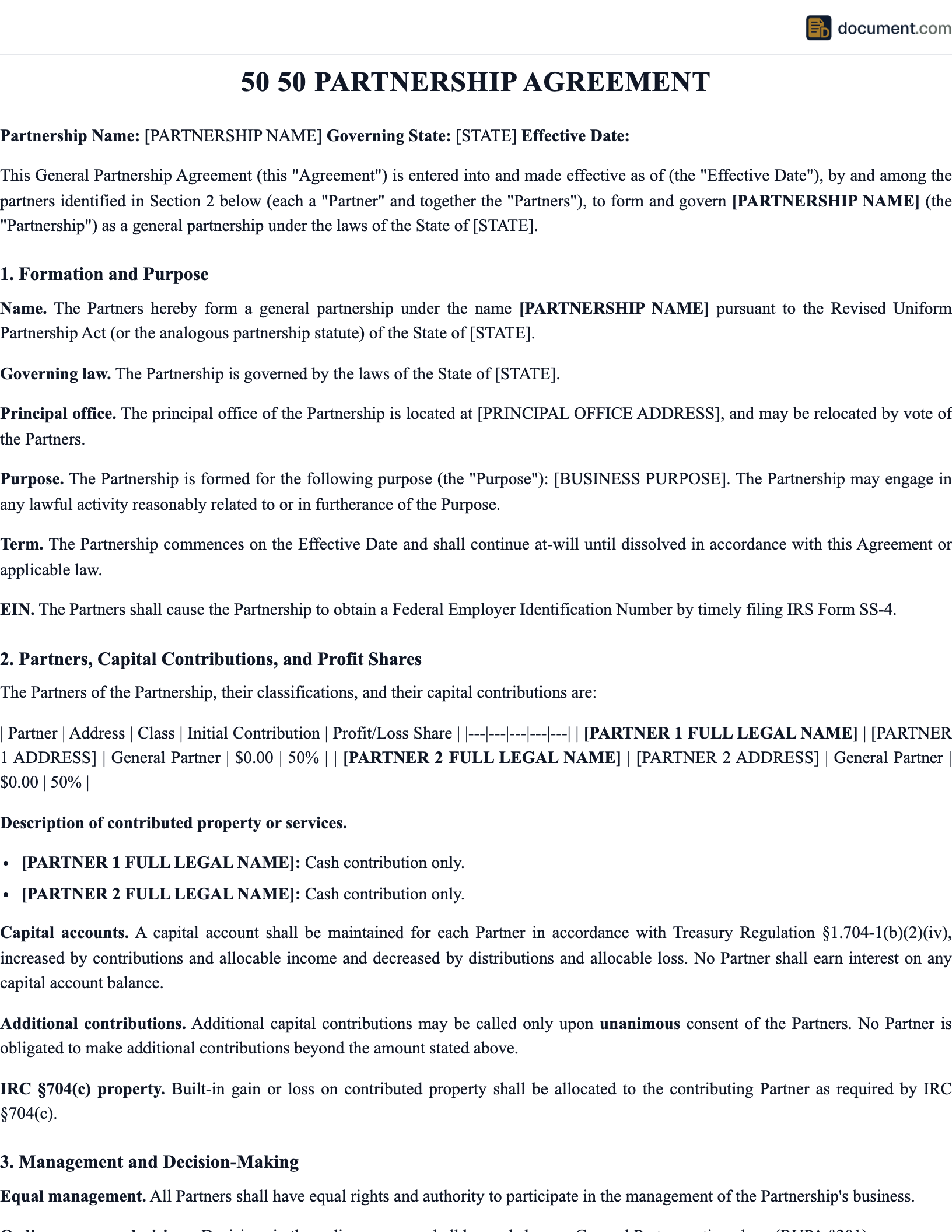

What Is a 50/50 Partnership Agreement?

A 50/50 partnership agreement is a legally binding contract between two individuals (or entities) who jointly operate a business as equal partners. Each partner owns 50% of the partnership, contributes an equal share of capital, participates equally in management decisions, and receives an equal share of profits and losses. The agreement documents the partners' rights and obligations, establishes the decision-making process, defines how disagreements will be resolved, and sets out the procedures for adding new partners, removing existing partners, or dissolving the partnership.

Equal partnerships are one of the most common structures for small businesses founded by two people who want to build something together on equal terms. Co-founders, husband-and-wife teams, siblings, and long-time colleagues often choose 50/50 arrangements to reflect their shared commitment and equal stakes in the venture. The appeal is obvious: neither partner is the "boss," both have equal authority and equal upside, and the structure reflects a genuine partnership of equals.

However, 50/50 partnerships carry a structural risk that other ownership splits avoid: deadlock. If the partners disagree on a material decision, there is no majority to resolve the dispute. The partnership may be unable to act, and a prolonged stalemate can paralyze operations, damage customer relationships, and ultimately force dissolution. A well-drafted 50/50 agreement addresses this risk head-on by including multiple deadlock-breaking mechanisms such as mediation, arbitration, neutral tiebreakers, shotgun buy-sell clauses, and clear definitions of which decisions require unanimous consent versus which can be made by either partner alone.

A comprehensive 50/50 partnership agreement covers capital contributions, profit and loss sharing, distributions, management rights, major decision procedures, banking and financial reporting, compensation and draws, transfer restrictions, buy-sell provisions for death or disability, non-compete and confidentiality obligations, dissolution procedures, and dispute resolution. With all of these terms documented upfront, the partners can focus on growing the business rather than negotiating their relationship every time a decision needs to be made.

True Equality

Equal ownership, equal management, and equal profits reflect a genuine partnership of equals

Deadlock Protection

Built-in mechanisms prevent business paralysis when partners cannot agree

Legal Clarity

Documents every aspect of the partnership relationship to prevent future disputes

50/50 Partnership Agreement Form Preview

Below is a visual preview of the sections included in a standard 50/50 partnership agreement. Your completed document will be fully customized for your partnership name, partners, contributions, decision-making structure, and state requirements.

50/50 Partnership Agreement

Equal Partnership Between Two Partners

Section 1: The Partnership

Section 2: The Partners (50/50 Ownership)

Section 3: Capital Contributions

Section 4: Decision Making

Section 5: Execution

Partner 1 Signature

Partner 2 Signature

When to Use a 50/50 Partnership

A 50/50 structure makes sense in some situations and creates problems in others. The right choice depends on your relationship with your prospective partner, the nature of the business, and your tolerance for risk.

Good Fit for 50/50

- - Two co-founders with complementary skills and shared vision

- - Both partners contributing equivalent capital, time, or expertise

- - Strong personal relationship built on mutual trust

- - A business where both partners bring essential elements

- - Partners who have successfully collaborated in the past

- - Willingness to include robust deadlock-resolution mechanisms

Poor Fit for 50/50

- - One partner is clearly the leader or has much more experience

- - Unequal capital contributions or risk exposure

- - Prior history of disagreements or power struggles

- - Different long-term goals or time horizons

- - Unwillingness to pre-negotiate deadlock procedures

- - Planning to seek outside investors who prefer clear control

Handling Deadlock

Deadlock is the greatest risk in a 50/50 partnership. A well-drafted agreement includes multiple layers of deadlock-resolution, starting with gentle mechanisms and escalating to more definitive solutions if earlier layers fail.

Layer 1: Structured Conversation

Scheduled weekly or monthly partner meetings with an agenda, minutes, and a formal process for raising disagreements. Many disputes can be resolved simply by slowing down and talking through the issue.

Layer 2: Mediation

If direct conversation fails, the partners engage a neutral mediator to facilitate resolution. Mediation is non-binding but often successful because it introduces a new perspective and creates time for reflection.

Layer 3: Neutral Tiebreaker

The agreement designates a trusted third party (attorney, accountant, experienced business advisor) who will break ties on specific categories of decisions. This can be a powerful tool for ongoing disputes over operational matters.

Layer 4: Shotgun Buy-Sell

When all else fails, one partner offers a buyout price and the other must either sell at that price or buy the offeror's interest at the same price. This forces resolution but can produce harsh outcomes if one partner has much more liquidity.

Layer 5: Dissolution

As a last resort, the agreement should provide a clear path to winding up the partnership, selling or distributing assets, paying creditors, and ending the business relationship with minimum conflict.

Capital Contributions

Capital contributions are the assets (cash, property, or services) that each partner contributes to the partnership in exchange for their ownership interest. In a 50/50 partnership, contributions are typically equal, but the form of contribution may differ.

- Cash: The most straightforward contribution. Each partner contributes an equal dollar amount.

- Property: Real estate, equipment, inventory, vehicles, or intellectual property contributed to the partnership. The property must be valued at fair market value and documented in the agreement.

- Services (Sweat Equity): One partner may contribute services rather than cash or property, but sweat equity creates tax complications under IRC Section 83 and must be carefully structured.

- Promissory Notes: Some partners contribute a promise to pay in the future, though this is less common and may affect tax basis.

- Additional Capital Calls: The agreement should address what happens if the partnership needs additional capital — whether partners are obligated to contribute, how much, and what happens if one partner cannot or will not contribute.

Profit and Loss Sharing

In a standard 50/50 partnership, all profits and losses are allocated equally between the partners. The agreement should address how profits are measured, whether profits are distributed or retained, how losses are handled, and whether any special allocations apply.

Allocation vs Distribution

Allocation refers to how profits and losses are assigned to each partner for tax purposes. Distribution refers to actual cash payments to the partners. These can differ — profits may be allocated equally but retained in the business, so partners owe tax on phantom income without receiving corresponding cash.

Tax Draws

Most partnerships include provisions for mandatory tax draws — cash distributions sufficient to cover the partners' tax liability on allocated but undistributed income. This prevents partners from owing taxes on income they haven't actually received.

Guaranteed Payments

One or both partners may receive guaranteed payments for services or capital — fixed amounts paid regardless of partnership profitability. These are treated as ordinary income to the recipient and as deductions to the partnership.

Management and Voting Rights

In a 50/50 partnership, both partners have equal management authority. The agreement should clearly distinguish between decisions that require joint consent and decisions that either partner can make unilaterally.

Equal Capital Contributions

Both partners contribute equal money, property, or services to the partnership

Equal Profit and Loss Sharing

50/50 split of all profits, losses, and distributions regardless of labor or contribution

Joint Management Rights

Each partner has equal authority over day-to-day and strategic business decisions

Deadlock-Breaking Mechanism

Prevents business paralysis when partners disagree on a material decision

Mutual Consent Requirements

Major decisions such as borrowing, hiring, or acquisitions require both partners' approval

Equal Voting Power

Each partner has one vote, ensuring neither can unilaterally override the other

Buy-Sell Provisions

Rules for handling the exit, death, or disability of either partner

Non-Compete and Confidentiality

Protects the partnership from competition by a departing partner

How to Create a 50/50 Partnership Agreement

Drafting a solid 50/50 partnership agreement takes careful planning and honest conversation between the partners. Follow these steps.

Confirm Both Partners Are Truly Equal

Honestly assess whether a 50/50 split reflects reality. If one partner is clearly the leader, a 51/49 or other majority split may be more appropriate.

Define the Business Purpose

State the specific business the partnership will conduct. A narrow purpose prevents disputes about whether a new opportunity is within the scope of the partnership.

Document Capital Contributions

Specify exactly what each partner contributes — cash, property, or services — and the agreed value. Include a schedule of initial contributions and procedures for future capital calls.

Establish Profit and Loss Sharing

Confirm the 50/50 allocation and address distribution timing, tax draws, guaranteed payments, and any special allocations.

Define Management and Voting Rights

Specify which decisions require joint consent and which can be made unilaterally. Consider creating categories (operational, financial, strategic) with different decision rules.

Include Deadlock-Resolution Mechanisms

This is the most important part of a 50/50 agreement. Include multiple layers of escalation from conversation to mediation to shotgun buy-sell to dissolution.

Add Buy-Sell Provisions

Address what happens on the death, disability, retirement, or voluntary exit of a partner. Include valuation methods and funding (typically life insurance).

Include Non-Compete and Confidentiality

Protect the partnership from competitive harm by departing partners. State-law restrictions on non-compete enforceability vary widely.

Address Dissolution and Winding Up

Specify the procedures for ending the partnership, selling assets, paying creditors, and distributing remaining funds.

Sign, Date, and Store Securely

Both partners must sign the agreement. Notarization is not required in most states but is recommended. Each partner should retain a signed copy, and a master copy should be kept with partnership records.

Key Components

A comprehensive 50/50 partnership agreement includes the following essential sections.

- Recitals and Parties: Identification of the partnership and the two partners.

- Purpose and Term: Business purpose and whether the partnership is for a specific period or at-will.

- Capital Contributions: Initial and future contributions by each partner.

- Profit and Loss Allocation: The 50/50 split and any adjustments.

- Distributions: When and how cash is distributed to partners.

- Management and Voting: Decision-making procedures and categories of decisions.

- Major Decisions: Matters requiring unanimous consent.

- Deadlock Resolution: Multi-layer escalation for unresolved disputes.

- Books, Records, and Banking: Financial reporting and account access.

- Transfer Restrictions: Limits on selling or transferring partnership interests.

- Buy-Sell Provisions: Death, disability, and voluntary exit procedures.

- Non-Compete and Confidentiality: Post-termination restrictions.

- Dissolution and Winding Up: Procedures for ending the partnership.

Tax Implications

General partnerships are pass-through entities for federal tax purposes under Subchapter K of the Internal Revenue Code. This has important implications for 50/50 partners.

Pass-Through Taxation

The partnership itself does not pay federal income tax. Instead, profits and losses flow through to the partners, who report their 50% share on their individual tax returns (Schedule E of Form 1040). The partnership files an informational Form 1065 and issues Schedule K-1 to each partner.

Self-Employment Tax

Active partners in a general partnership are typically subject to self-employment tax (Social Security and Medicare) on their distributive share of partnership earnings. This is a significant cost — 15.3% on the first portion of earnings up to the Social Security wage base and 2.9% on amounts above that.

Basis and At-Risk Rules

Partners can generally deduct their share of partnership losses only to the extent of their tax basis in the partnership and only to the extent they are at risk. These limitations can defer the recognition of losses when a partner contributes more services than cash.

Qualified Business Income Deduction

Partners may be eligible for the 20% qualified business income (QBI) deduction under IRC Section 199A, subject to income thresholds and the type of business (specified service trades or businesses face stricter limits).

Sample 50/50 Partnership Agreement

Below is a condensed preview of our 50/50 partnership agreement template. Your completed document will be fully customized for your partnership and partners.

50/50 PARTNERSHIP AGREEMENT

Equal Partnership Between Two Partners

This 50/50 Partnership Agreement ("Agreement") is entered into as of[Effective Date]by and between [Partner 1]and [Partner 2](collectively, the "Partners").

1. FORMATION AND NAME

The Partners hereby form a general partnership under the laws of the State of[State]to be known as [Partnership Name](the "Partnership").

2. OWNERSHIP

Each Partner shall own a 50% interest in the Partnership. The Partners shall have equal rights and obligations with respect to the management, profits, losses, and distributions of the Partnership.

3. CAPITAL CONTRIBUTIONS

Each Partner shall contribute the following to the Partnership:

- Partner 1: [Contribution]

- Partner 2: [Contribution]

4. PROFITS AND LOSSES

All profits and losses of the Partnership shall be allocated equally (50/50) between the Partners. Distributions shall be made quarterly or as otherwise agreed by the Partners, subject to the cash needs of the Partnership.

5. MANAGEMENT

Both Partners shall have equal management authority. Decisions requiring unanimous consent include: borrowing money, hiring or firing key personnel, entering into contracts exceeding $[Amount], acquiring or disposing of significant assets, amending this Agreement, and dissolving the Partnership...

6. DEADLOCK

If the Partners are unable to agree on a material matter after reasonable discussion, the dispute shall be submitted to mediation within 30 days. If mediation fails, either Partner may invoke the shotgun buy-sell procedure set forth in Section 10...

7. SHOTGUN BUY-SELL

In the event of unresolved deadlock, either Partner (the "Offeror") may deliver a written offer to purchase the other Partner's interest at a specified price. The Offeree shall then elect within 30 days to either (a) sell their interest at the offered price, or (b) purchase the Offeror's interest at the same price per percentage point...

8. DISSOLUTION

The Partnership shall dissolve upon the occurrence of any of the following: mutual agreement of the Partners, death or permanent disability of a Partner (unless the surviving Partner exercises buy-out rights), or unresolved deadlock...

Frequently Asked Questions

Find answers to common questions about 50/50 partnerships, deadlock, management, and dispute resolution.

Official Resources

For additional information on partnership law, taxation, and formation requirements, consult these official and reputable resources.

IRS - Partnerships

IRS guidance on partnership taxation, Form 1065, and Schedule K-1

SBA - Business Structures

Small Business Administration guide to partnerships and other entity types

ULC - Revised Uniform Partnership Act

Uniform Law Commission RUPA information and state adoption status

IRC Subchapter K - Partnerships

Statutory rules for partnership taxation under the Internal Revenue Code

ABA Business Law Section

American Bar Association resources on partnership and business law

SCORE - Small Business Mentoring

Free business mentoring and partnership planning resources

Nolo - Partnership Legal Encyclopedia

Free legal information on partnerships and partnership agreements

IRS Form 1065 Instructions

Partnership return of income filing requirements and instructions

Create your 50 50 Partnership Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.