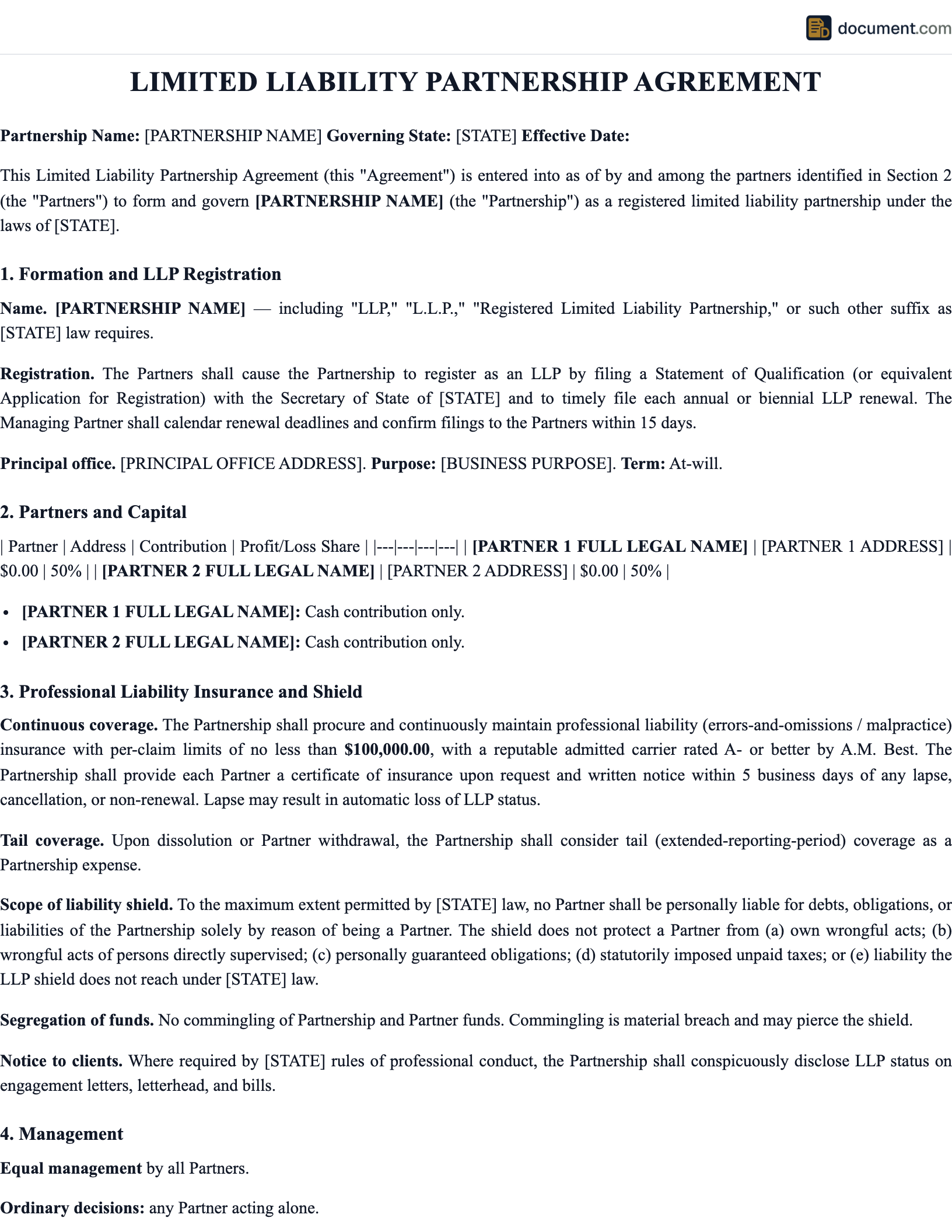

What Is a Limited Liability Partnership?

A limited liability partnership (LLP) is a business entity that combines the pass-through taxation and management flexibility of a general partnership with a personal liability shield for its partners. Originally developed in the early 1990s in response to the savings-and-loan crisis — in which innocent partners in large law and accounting firms were held personally liable for the malpractice of colleagues involved in failed thrifts — LLPs protect each partner from personal liability arising from the wrongful acts of other partners. Today, LLPs are available in all 50 states and are the predominant form of organization for large professional practices.

The central feature of an LLP is the "liability shield." In a traditional general partnership, every partner is jointly and severally personally liable for all debts and obligations of the partnership, including obligations arising from the negligence or intentional misconduct of other partners. This meant that a partner in a 500-lawyer firm could lose their house because of a mistake made by a colleague they had never met. The LLP structure eliminates this exposure. In an LLP, each partner remains personally liable for their own acts and for the ordinary business debts of the partnership, but is not liable for the malpractice of other partners.

There are two main flavors of LLP liability shield: the "partial shield" and the "full shield." Under a partial shield, partners are protected only from claims arising from the professional malpractice or negligence of other partners — they remain personally liable for ordinary business debts such as unpaid leases or vendor invoices. Under a full shield, partners are protected from both professional malpractice claims and ordinary business debts. The majority of states have now adopted the full shield, making LLPs functionally similar to LLCs in terms of liability protection.

LLPs are formed by filing a registration statement with the secretary of state and typically must maintain annual filings, pay annual fees, and (in many states) carry minimum professional liability insurance. The internal rules governing the partners are set out in a separate LLP partnership agreement that addresses capital contributions, profit and loss sharing, management and voting rights, admission of new partners, withdrawal and retirement of partners, dissolution, and dispute resolution.

Liability Shield

Protects partners from personal liability for the malpractice of other partners

Pass-Through Tax

No entity-level tax; profits flow through to partners' individual returns

Professional Focus

Ideal for lawyers, accountants, architects, engineers, doctors, and consultants

LLP Agreement Form Preview

Below is a visual preview of the sections included in a standard LLP partnership agreement. Your completed document will be customized for your firm name, partners, capital structure, and state-specific registration and insurance requirements.

Limited Liability Partnership Agreement

For Registered LLPs

Section 1: The LLP

Section 2: The Partners

Section 3: Liability Shield

Pursuant to state LLP statute, no partner shall be personally liable for the debts, obligations, or liabilities of the partnership arising from negligence, wrongful acts, or misconduct committed by another partner or any employee not under the first partner's direct supervision.

Section 4: Professional Liability Insurance

The LLP shall maintain professional liability insurance in the minimum amount of $1,000,000 per claim and $3,000,000 in the aggregate, as required by state law and in a form reasonably acceptable to all partners.

Section 5: Execution

Partner 1 Signature

Partner 2 Signature

Partner 3 Signature

LLP vs Other Business Entities

Understanding how an LLP compares to other entity types helps you choose the right structure for your business.

LLP vs General Partnership

Both are taxed as pass-through entities and managed directly by the partners, but only an LLP provides limited liability for partners. A general partnership can form by default (no filing required); an LLP requires formal registration with the state and ongoing compliance.

LLP vs Limited Partnership (LP)

In an LP, there are general partners with unlimited liability and limited partners with limited liability but no management role. In an LLP, every partner has limited liability and can participate in management. LPs are commonly used for investment funds and real estate; LLPs for professional practices.

LLP vs LLC

Both provide limited liability and pass-through taxation. LLCs are available for virtually any business; LLPs in many states are limited to professional services. LLCs offer more flexible management structures (member-managed or manager-managed); LLPs are always managed by the partners directly. LLPs may have mandatory insurance requirements that LLCs do not.

LLP vs Professional Corporation (PC)

Both are used by licensed professionals and provide some liability protection. A PC is a corporation taxed as a C-corp or S-corp, while an LLP is a partnership taxed as a pass-through. LLPs are generally more flexible in profit-sharing and admission/withdrawal of partners, and they avoid the double taxation that can affect C-corp PCs.

Who Uses LLPs?

LLPs are most common among licensed professionals, though availability to non-professional businesses varies by state.

Law Firms

The original use case for LLPs — and still the most common. Protects each lawyer from personal exposure to the malpractice of colleagues.

Accounting Firms

Including the Big Four and mid-sized CPA firms, which adopted LLP structure in the 1990s to limit partner exposure.

Medical Practices

Where permitted, physicians in group practice use LLPs to protect each doctor from liability for colleagues' malpractice.

Architecture and Engineering Firms

Design professionals use LLPs for similar reasons — to shield each partner from liability for others' design errors.

Consulting Firms

Management consultants, financial advisors, and other service professionals use LLPs when state law permits.

Dental Practices

Dentists in group practice form LLPs to limit personal exposure while preserving partnership-style management.

LLP Formation Requirements

Forming an LLP is more involved than forming a general partnership. You must comply with state-specific filing, insurance, and naming requirements.

- Eligibility Check: Confirm that your business is eligible for LLP status in your state. Some states restrict LLPs to professional services.

- Name Requirements: The LLP name must include "LLP," "L.L.P.," or "Limited Liability Partnership." Some states have additional naming rules.

- Registration Filing: File a statement of qualification or registration with the secretary of state, typically including the partnership name, principal office, registered agent, number of partners, and filing fee.

- Insurance Requirements: Many states require LLPs to carry minimum professional liability insurance (often $100,000 to $1,000,000 per claim). Confirm the specific requirements in your state.

- Partnership Agreement: Draft a detailed LLP partnership agreement covering capital, management, profit-sharing, admission and withdrawal of partners, and dispute resolution.

- Annual Renewal: Most states require annual or biennial renewal filings and fees to maintain LLP status. Failure to renew can cause loss of the liability shield.

- Tax Registration: Obtain an EIN from the IRS and register for state and local taxes as applicable.

How the LLP Liability Shield Works

The liability shield is the defining feature of an LLP. Understanding how it works — and what it does not protect against — is critical.

Personal Liability Shield

Partners are not personally liable for the negligence or malpractice of other partners

Pass-Through Taxation

Profits and losses flow through to partners' personal tax returns

Professional Practice Friendly

Designed for law firms, accounting firms, medical practices, and other licensed professionals

State Registration Required

LLPs must register with the state — not the case for general partnerships

Annual Renewal

Most states require annual filings and fees to maintain LLP status

Mandatory Insurance

Many states require LLPs to carry minimum professional liability insurance

Partnership Management

Partners manage the business directly like a general partnership

Flexible Ownership

Any number of partners with flexible profit-sharing and capital arrangements

What the LLP Shield Does NOT Protect

The LLP shield does not protect a partner from: (1) liability for their own malpractice or wrongful acts; (2) liability for malpractice committed by someone under their direct supervision; (3) personal guarantees the partner signs on loans, leases, or other obligations; (4) liability in states with partial shields for ordinary business debts; or (5) liability incurred before the LLP was properly registered or during periods when the LLP has lost its status due to failure to file annual reports.

Management and Voting

Unlike an LLC, which can be manager-managed, an LLP is always managed directly by its partners. The agreement should specify how management authority is allocated and which decisions require joint or supermajority consent.

Executive Committee

Larger LLPs often designate an executive committee (3-7 partners) responsible for day-to-day management, hiring, compensation, and strategic decisions. The full partnership typically retains authority over major matters such as admission of new partners, mergers, and dissolution.

Managing Partner

Many LLPs elect a managing partner who serves as the chief executive and is responsible for implementation of firm policies and day-to-day operations. The managing partner is accountable to the full partnership or to the executive committee.

Voting Rights

Voting can be per capita (one vote per partner) or proportional to ownership percentage. Major decisions — admission of new partners, mergers, dissolution, amendment of the agreement — typically require a supermajority (commonly 2/3 or 3/4 of partners).

How to Create an LLP Agreement

Creating an LLP involves both state filings and drafting a comprehensive partnership agreement. Follow these steps.

Confirm State Eligibility

Verify that your business qualifies for LLP status in your state. Some states limit LLPs to specific professional practices.

Choose a Name

Select a name that complies with state naming requirements, including the required LLP designation.

File Registration Statement

Submit the statement of qualification or LLP registration to the secretary of state along with the applicable filing fee.

Obtain Required Insurance

Secure minimum professional liability insurance as required by state law. Maintain coverage continuously to preserve the liability shield.

Draft the Partnership Agreement

Create a comprehensive internal agreement covering capital, management, profit-sharing, admission and withdrawal, and dispute resolution.

Obtain EIN and Tax Registrations

Apply for a federal EIN from the IRS and register for state tax IDs and any required local business licenses.

Open Partnership Banking Accounts

Establish dedicated banking accounts in the LLP name. Do not commingle partnership funds with personal funds.

Adopt the Agreement

All partners must sign the partnership agreement. Retain original signed copies with the partnership records.

Comply with Annual Requirements

File annual reports, pay renewal fees, and maintain required insurance. Monitor compliance deadlines carefully.

Review and Update Annually

Review the agreement each year for needed updates and amend as necessary when partners join or leave or the business changes.

Key Components

A comprehensive LLP partnership agreement includes the following essential sections.

- Recitals and Parties: Identification of the LLP and partners.

- Formation and Registration: Reference to state filing and maintenance of LLP status.

- Purpose and Term: The business purpose and duration of the partnership.

- Capital Contributions: Initial and future contributions by each partner.

- Profit and Loss Sharing: Allocation formulas and distribution timing.

- Liability Shield Provisions: Confirmation of the LLP shield and exceptions.

- Insurance Requirements: Minimum coverage and maintenance obligations.

- Management and Voting: Decision-making procedures and voting rights.

- Admission of New Partners: Requirements and approval process.

- Withdrawal and Retirement: Procedures and financial entitlements.

- Expulsion: Grounds and procedures for removing a partner.

- Dissolution and Winding Up: Procedures for ending the LLP.

Tax Implications

LLPs are taxed as pass-through entities for federal purposes, but state tax treatment varies significantly.

Federal Pass-Through Taxation

LLPs file a Form 1065 informational return and issue Schedule K-1 to each partner. Profits and losses flow through to the partners' individual returns (Schedule E of Form 1040) without entity-level federal income tax.

Self-Employment Tax

Active partners are typically subject to self-employment tax on their share of partnership earnings. Limited partners in an LLP may escape self-employment tax on certain passive income — but this is a complex area of tax law that depends on state LLP rules and partner activity.

State Entity-Level Taxes

Some states impose entity-level taxes on LLPs — California, for example, charges an $800 annual franchise tax plus a fee based on gross receipts. Other states impose LLP-specific filing and annual fees. Factor these costs into your entity-choice analysis.

QBI Deduction

Partners may qualify for the 20% qualified business income (QBI) deduction under IRC Section 199A, subject to income thresholds and restrictions on specified service trades or businesses (which includes most professional services).

Sample LLP Agreement

Below is a condensed preview of our LLP partnership agreement template.

LIMITED LIABILITY PARTNERSHIP AGREEMENT

Professional Services LLP

This Limited Liability Partnership Agreement ("Agreement") is entered into as of [Effective Date]by and among the undersigned partners (collectively, the "Partners") of[LLP Name], a registered limited liability partnership under the laws of[State].

1. FORMATION AND REGISTRATION

The Partners have registered the Partnership as a limited liability partnership under the laws of the State of [State]. The Partners shall cause all required annual filings and fees to be timely paid to maintain the LLP status.

2. LIMITATION OF LIABILITY

Pursuant to applicable state law, no partner shall be personally liable, directly or indirectly, by way of contribution, indemnification, or otherwise, for any debts, obligations, or liabilities of the Partnership arising from negligence, wrongful acts, or misconduct committed by another partner or by any employee not under the first partner's direct supervision...

3. PROFESSIONAL LIABILITY INSURANCE

The Partnership shall maintain professional liability insurance with minimum limits of $[Amount]per claim and $[Amount]in the aggregate, satisfying all applicable state law requirements...

4. CAPITAL CONTRIBUTIONS

Each Partner shall contribute to the Partnership the amounts set forth on Schedule A. Additional capital contributions may be required upon[Vote]vote of the Partners.

5. PROFIT AND LOSS ALLOCATION

Profits and losses shall be allocated among the Partners in accordance with their respective ownership percentages set forth on Schedule A. Distributions shall be made [Frequency]subject to the cash needs of the Partnership.

6. MANAGEMENT

The Partnership shall be managed by an Executive Committee consisting of[Number]partners elected annually by the full Partnership. The Executive Committee shall have authority over day-to-day operations, while major decisions shall require approval of a supermajority of the Partners...

7. ADMISSION OF NEW PARTNERS

New partners may be admitted upon the unanimous consent (or supermajority vote) of the existing Partners. New partners must sign this Agreement and make the required capital contribution...

8. WITHDRAWAL AND RETIREMENT

A Partner may withdraw upon [Notice]days' prior written notice. Upon withdrawal, the Partner shall be entitled to their capital account balance plus accrued but undistributed profits...

Frequently Asked Questions

Find answers to common questions about limited liability partnerships, formation, liability protection, and taxation.

Official Resources

For additional information on limited liability partnerships, consult these official and reputable resources.

IRS - Partnerships

IRS guidance on partnership taxation, Form 1065, and Schedule K-1

SBA - Business Structures

Small Business Administration guide to partnerships and LLPs

ULC - Revised Uniform Partnership Act

Uniform Law Commission RUPA information covering LLP provisions

IRC Subchapter K - Partnerships

Federal tax rules for partnerships including LLPs

ABA Business Law Section

American Bar Association resources on business entities

IRS Form 1065 Instructions

Partnership return of income filing requirements

IRC Section 199A - QBI Deduction

Qualified business income deduction for pass-through entities

ABA Professional Responsibility

Professional conduct and ethics rules for LLP practices

Create your Limited Liability Partnership Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.