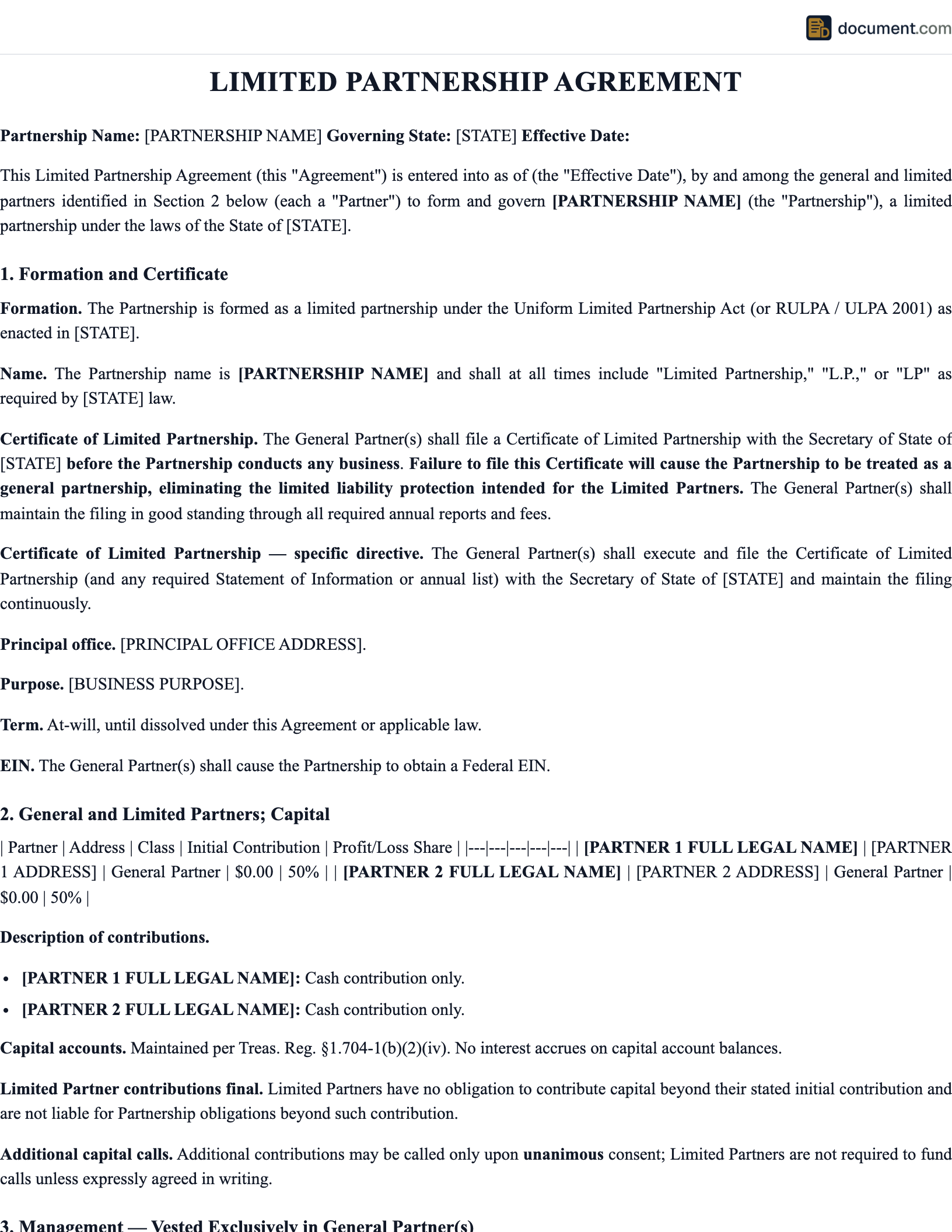

What Is a Limited Partnership?

A limited partnership (LP) is a specific form of business entity governed by state limited partnership statutes. It consists of at least one general partner (GP), who manages the business and has unlimited personal liability for partnership debts, and one or more limited partners (LPs), who contribute capital but have no management role and whose personal liability is limited to the amount of their investment. The LP structure allows investors to participate in a business opportunity — often with significant financial upside — without exposing their personal assets to unlimited risk.

Limited partnerships have a long history. They trace back to medieval Italian commenda arrangements that allowed merchants to raise capital from passive investors for risky overseas trading ventures. Modern American LP statutes began with the Uniform Limited Partnership Act (ULPA) of 1916 and have been revised several times since, culminating in the ULPA of 2001 that many states have now adopted. Today, LPs are the dominant legal structure for private investment funds — including private equity, venture capital, hedge funds, real estate investment partnerships, and oil and gas programs.

The central bargain of a limited partnership is a trade between control and liability. Limited partners give up the right to manage the business — they cannot bind the partnership, participate in day-to-day decisions, or exercise control — and in exchange they receive limited liability, meaning they can only lose the amount of capital they contributed. General partners retain full control over management but accept unlimited personal liability for partnership obligations. This is why modern LPs almost always use an LLC or corporation as the general partner — the individuals running the partnership enjoy the limited liability of the GP entity, while the partnership as a whole retains clear GP management authority.

A comprehensive limited partnership agreement addresses capital commitments and contribution schedules, the distribution waterfall (including preferred returns and carried interest), management fees, GP and LP rights and obligations, restrictions on transfer of partnership interests, GP removal procedures, LP voting rights, investor reporting obligations, dissolution and winding up, and dispute resolution. For investment fund LPs, the agreement also addresses investment restrictions, diversification limits, related-party transactions, key-person provisions, and clawback obligations.

Limited Liability for LPs

Passive investors risk only the amount they contribute, not their personal assets

Professional Management

A dedicated general partner runs the business while LPs remain passive investors

Pass-Through Taxation

Profits and losses flow through to partners without entity-level tax

LP Agreement Form Preview

Below is a visual preview of the sections in a standard limited partnership agreement. Your completed document will be customized for your partnership's structure, capital commitments, waterfall, and state.

Limited Partnership Agreement

Between General Partner and Limited Partners

Section 1: The Partnership

Section 2: General Partner

Section 3: Capital Commitments

Section 4: Distribution Waterfall

1. Return of capital to Limited Partners (100% to LPs)

2. Preferred return of 8% per annum compounded (100% to LPs)

3. GP catch-up until GP receives 20% of cumulative profits

4. Thereafter, 80% to LPs and 20% to GP (carried interest)

Section 5: Execution

General Partner

Limited Partner

General Partners vs Limited Partners

The LP structure has two distinct classes of partners with fundamentally different rights, obligations, and risks. Understanding these differences is essential to structuring a compliant and workable LP.

General Partner (GP)

- - Manages the business day-to-day

- - Has unlimited personal liability

- - Signs contracts and binds the partnership

- - Makes all investment decisions

- - Typically receives a management fee

- - Receives carried interest above the preferred return

- - Usually structured as an LLC or corporation

Limited Partner (LP)

- - Passive investor — no management role

- - Personal liability limited to committed capital

- - Cannot bind the partnership

- - Has voting rights on fundamental matters only

- - Receives return of capital plus preferred return

- - Shares in profits above preferred return

- - Receives periodic reports from the GP

Common Uses of Limited Partnerships

LPs are used across a wide range of investment structures and business purposes.

Private Equity Funds

LPs raise capital from institutional investors, pension funds, endowments, and high-net-worth individuals to acquire and improve mature private companies.

Venture Capital Funds

LPs invest in early-stage and growth-stage technology and other high-growth companies, typically with a 10-year fund life.

Hedge Funds

Though many modern hedge funds use LLC structures, traditional hedge funds remain organized as LPs for regulatory and tax reasons.

Real Estate Syndications

Sponsors raise capital from passive investors to acquire, develop, or manage real estate projects, with sponsor compensation through management fees and promotes.

Oil and Gas Programs

Working interest owners and passive investors pool capital to explore, drill, and operate oil and gas properties.

Family Limited Partnerships

Wealth planning vehicles that allow parents to transfer assets to children while retaining management control, with estate tax benefits.

LP Formation Requirements

Forming a limited partnership requires both state filings and a comprehensive internal agreement.

General Partner (GP)

Manages the business day-to-day and has unlimited personal liability for partnership debts

Limited Partner (LP)

Contributes capital but has no management role and liability limited to their investment

Capital Commitment

Each limited partner agrees to contribute a specified amount of capital when called

Profit Waterfall

Defines how distributions flow between LPs and GPs, including preferred returns and carried interest

Management Fee

Ongoing fee paid to the general partner for managing the partnership's affairs

Passive Investor Protection

Limited partners are not personally liable beyond their capital contributions

Investor Reporting

Regular financial reporting and communication obligations to limited partners

Transfer Restrictions

Limits on LP ability to sell or transfer interests without general partner consent

The Distribution Waterfall

The distribution waterfall is the heart of a limited partnership agreement. It defines the order in which cash is paid out to LPs and the GP as investments are realized. A well-drafted waterfall aligns the GP's incentives with the LPs' returns and provides transparent rules for profit sharing.

Tier 1: Return of Capital

100% of distributions go to the LPs until each LP has received back their full capital contribution. No GP participation until LPs are made whole on their original investment.

Tier 2: Preferred Return

100% of distributions go to the LPs until they have received a preferred return on their capital — typically 6% to 10% per annum, compounded. The GP does not participate in profits until the LPs have received this minimum return.

Tier 3: GP Catch-Up

Once the LPs have received their capital and preferred return, distributions go to the GP until the GP has received an amount equal to a specified percentage (typically 20%) of the cumulative profits allocated to that point. This tier catches the GP up to their carry percentage.

Tier 4: Split Distribution

Remaining profits are split between LPs and GP according to the carry percentage — typically 80% to LPs and 20% to GP. This is the GP's ongoing share of the upside in well-performing investments.

Clawback Provisions

Many LP agreements include a clawback provision that requires the GP to return previously distributed carried interest if, at the end of the partnership's term, the LPs have not received their full preferred return and capital back. Clawbacks protect LPs from receiving interim distributions that prove excessive when calculated over the entire life of the fund.

Management Fees and Carried Interest

Compensation to the general partner typically consists of two components: an annual management fee and carried interest.

Management Fee

An annual fee paid to the GP to cover operating expenses such as salaries, office rent, travel, and professional services. The industry standard is 2% of committed capital during the investment period and 2% of invested capital thereafter, though fees vary by fund size and strategy. Large funds typically charge lower percentages; smaller, specialized funds may charge more.

Carried Interest

The GP's share of profits above the preferred return. The industry standard is 20%, sometimes higher for top-tier fund managers. Carried interest aligns the GP's incentives with the LPs' returns — the GP only earns significant compensation if the LPs earn their expected return first. Carried interest is currently taxed as capital gains at the federal level, which is a source of ongoing tax policy controversy.

Fee Offset

Many modern LP agreements include fee offset provisions that require the GP to credit certain fees received from portfolio companies (transaction fees, monitoring fees, directors' fees) against the management fee, reducing the fee paid by the LPs. Fee offsets can range from 50% to 100% of portfolio-company fees.

How to Create a Limited Partnership Agreement

Drafting an LP agreement is a sophisticated undertaking that typically involves experienced fund counsel. Follow these steps.

Establish the GP Entity

Form an LLC or corporation to serve as the general partner. This insulates the individual principals from personal liability.

File the Certificate of Limited Partnership

File with the secretary of state in the chosen state of formation. Delaware is the most popular choice for sophisticated LP structures.

Draft the Offering Documents

Prepare a private placement memorandum (PPM) and subscription agreement that comply with federal and state securities laws.

Negotiate the LP Agreement

Work with investors to finalize the LP agreement terms, including the waterfall, management fees, governance, and reporting obligations.

Comply with Securities Laws

Ensure that the offering qualifies for an exemption from SEC registration (typically Rule 506(b) or 506(c)). File Form D with the SEC and any required state notice filings.

Establish Banking and Administrative Infrastructure

Set up partnership banking accounts, fund administration, audit relationships, and legal and tax advisors.

Close the Fund

Accept subscriptions from qualifying investors (typically accredited or qualified purchasers), collect initial capital contributions, and issue confirmation to each LP.

Begin Operations

Start making investments, drawing down committed capital through capital calls, and providing regular reports to LPs.

Maintain Ongoing Compliance

File annual reports with the state, complete annual audits, distribute K-1s to LPs, and comply with SEC and state securities reporting.

Wind Down at End of Term

Liquidate remaining investments, make final distributions according to the waterfall, apply clawback provisions if required, and dissolve the partnership.

Key Components

A comprehensive LP agreement includes the following essential sections.

- Formation and Name: Partnership name, state of formation, and principal office.

- Purpose and Investment Strategy: The business purpose and permitted investments.

- Term and Extensions: Partnership duration and any extension rights.

- Capital Commitments: Total and individual capital commitments and contribution schedule.

- Capital Calls: Procedures for drawing down committed capital.

- Distribution Waterfall: Order of distributions and carried interest.

- Management Fees: Annual fee structure and fee offsets.

- GP Rights and Obligations: Management authority, fiduciary duties, and indemnification.

- LP Rights and Obligations: Limited liability, voting rights, and information rights.

- Transfer Restrictions: Limits on transfer of LP interests.

- GP Removal: Procedures for replacing the general partner.

- Clawback: GP obligation to return excess distributions.

- Reporting Obligations: Frequency and content of LP reports.

- Dissolution and Winding Up: End-of-term procedures.

Tax Implications

LPs are pass-through entities for federal tax purposes, which creates specific issues for limited partners and general partners alike.

Federal Pass-Through Taxation

The LP files Form 1065 and issues K-1s to the GP and each LP. Profits and losses flow through without entity-level tax. Limited partners generally do not pay self-employment tax on their distributive share because they are passive investors.

Carried Interest Taxation

Carried interest is currently taxed as capital gains under IRC Section 1061, with a 3-year holding period requirement. This treatment is a frequent target of tax reform proposals but remains the law as of this writing. GPs benefit significantly from capital gains treatment on their carried interest.

UBTI for Tax-Exempt LPs

Tax-exempt limited partners (pension funds, endowments, IRAs) may owe unrelated business taxable income (UBTI) on LP investments that use leverage or engage in active trade or business. Many funds set up blocker entities or side-car structures to minimize UBTI for tax-exempt investors.

State Tax Issues

Limited partners may owe state income tax in each state where the LP operates, creating complex compliance issues. Composite state returns and withholding arrangements can simplify the compliance burden.

Sample Limited Partnership Agreement

Below is a condensed preview of our limited partnership agreement template.

LIMITED PARTNERSHIP AGREEMENT

Between General Partner and Limited Partners

This Limited Partnership Agreement ("Agreement") is entered into as of[Effective Date]by and among [GP Entity]as general partner (the "General Partner"), and the limited partners listed on Schedule A (collectively, the "Limited Partners").

1. FORMATION

The Partnership has been formed as a limited partnership under the laws of[State]by the filing of a Certificate of Limited Partnership with the Secretary of State.

2. PURPOSE

The Partnership is formed to [Business Purpose]and to engage in any and all activities reasonably related thereto.

3. CAPITAL COMMITMENTS

Each Limited Partner commits to contribute to the Partnership the amount set forth opposite their name on Schedule A. Capital contributions shall be made in response to capital calls issued by the General Partner with at least[Days]days' prior notice.

4. DISTRIBUTIONS

Distributions shall be made in the following order of priority (the "Waterfall"):

- First, 100% to LPs until return of capital;

- Second, 100% to LPs until they have received an 8% preferred return;

- Third, 100% to GP until GP catches up to 20% of cumulative profits;

- Thereafter, 80% to LPs and 20% to GP.

5. MANAGEMENT FEE

The Partnership shall pay the General Partner an annual management fee equal to [%]of committed capital during the investment period and[%]of invested capital thereafter...

6. MANAGEMENT AUTHORITY

The General Partner shall have exclusive authority to manage the business and affairs of the Partnership. Limited Partners shall not participate in management, and any attempt by a Limited Partner to take control of the Partnership's business shall be ineffective and may jeopardize their limited liability...

7. CLAWBACK

If, upon dissolution of the Partnership, the General Partner has received carried interest distributions in excess of 20% of aggregate profits after return of capital and preferred return, the General Partner shall repay such excess to the Partnership for distribution to the Limited Partners...

8. TERM

The Partnership shall continue for a term of[Years]years from the Effective Date, subject to extension by the General Partner for up to two additional one-year periods with the consent of a majority in interest of the Limited Partners.

Frequently Asked Questions

Find answers to common questions about limited partnerships, distribution waterfalls, carried interest, and fund formation.

Official Resources

For additional information on limited partnerships, investment fund structures, and securities compliance, consult these official and reputable resources.

SEC - Rule 506 Exempt Offerings

Regulation D exemptions commonly used for LP offerings

IRS - Partnerships

IRS guidance on partnership taxation, Form 1065, and Schedule K-1

ULC - Uniform Limited Partnership Act

Uniform Law Commission ULPA 2001 information and state adoption

IRC Section 1061 - Carried Interest

Statutory rules for carried interest taxation and 3-year holding period

SEC - Investment Advisers Act

Registration and compliance requirements for fund managers

Delaware Division of Corporations

Formation filings and information for Delaware limited partnerships

ABA Business Law Section

American Bar Association resources on LP and fund formation

Institutional Limited Partners Association

ILPA principles and best practices for LP agreements

Create your Limited Partnership Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.