What Are Articles of Incorporation?

Articles of incorporation are the charter document filed with a state government to legally establish a corporation as a separate legal entity. This filing is the single act that transforms a business idea into a recognized corporate person under the law — an entity that can own property, enter into contracts, maintain bank accounts, issue stock, hire employees, and continue to exist in perpetuity regardless of changes in ownership or management. The corporation exists as a legal shield between its owners (shareholders) and the obligations and liabilities of the business itself.

The corporate form has been the foundational business structure for centuries, and for good reason. Corporations offer clear advantages that no other entity type fully replicates: perpetual existence (the corporation does not dissolve when a shareholder dies or sells their shares), free transferability of ownership interests (shares can be sold, gifted, or inherited without disrupting the business), centralized management (a board of directors oversees the company on behalf of all shareholders), and the ability to raise capital through stock issuance (including IPOs, private placements, and employee equity compensation). These structural advantages make corporations the preferred vehicle for venture-backed startups, publicly traded companies, and businesses that plan to grow beyond a small founding team.

The terminology for this document varies by jurisdiction. Most states call it "articles of incorporation." Delaware — where more public companies are incorporated than any other state — uses the term "certificate of incorporation." Some states use "charter" or "corporate charter." Regardless of the name, the document serves the same function: it establishes the corporation under state law, specifies its authorized capital structure (the number and types of shares it can issue), designates a registered agent for service of process, and may include provisions regarding the purpose of the corporation, the liability of directors, and indemnification.

Unlike corporate bylaws — which are an internal governance document — articles of incorporation are filed with the state and become part of the public record. Any person can search the Secretary of State's database and find a corporation's articles, including its authorized share structure, registered agent, and (in some states) the names of initial directors. For this reason, the articles should contain only the provisions required or permitted by statute, with detailed governance rules reserved for the bylaws and shareholder agreements.

Our attorney-reviewed templates are customized for each state's corporation statute and include all required provisions, proper stock authorization language, director liability limitations (where permitted), and filing instructions. Each template reflects the specific requirements of your chosen corporate type — whether you are forming a standard C-Corporation, electing S-Corporation tax status, establishing a tax-exempt nonprofit, creating a professional corporation for licensed practitioners, or organizing a benefit corporation with a dual-purpose mission.

Limited Liability

Shareholders' personal assets are protected from corporate debts and lawsuits

Capital Raising

Issue stock to investors, employees, and advisors to fund growth and incentivize performance

Perpetual Existence

The corporation continues indefinitely regardless of changes in ownership or management

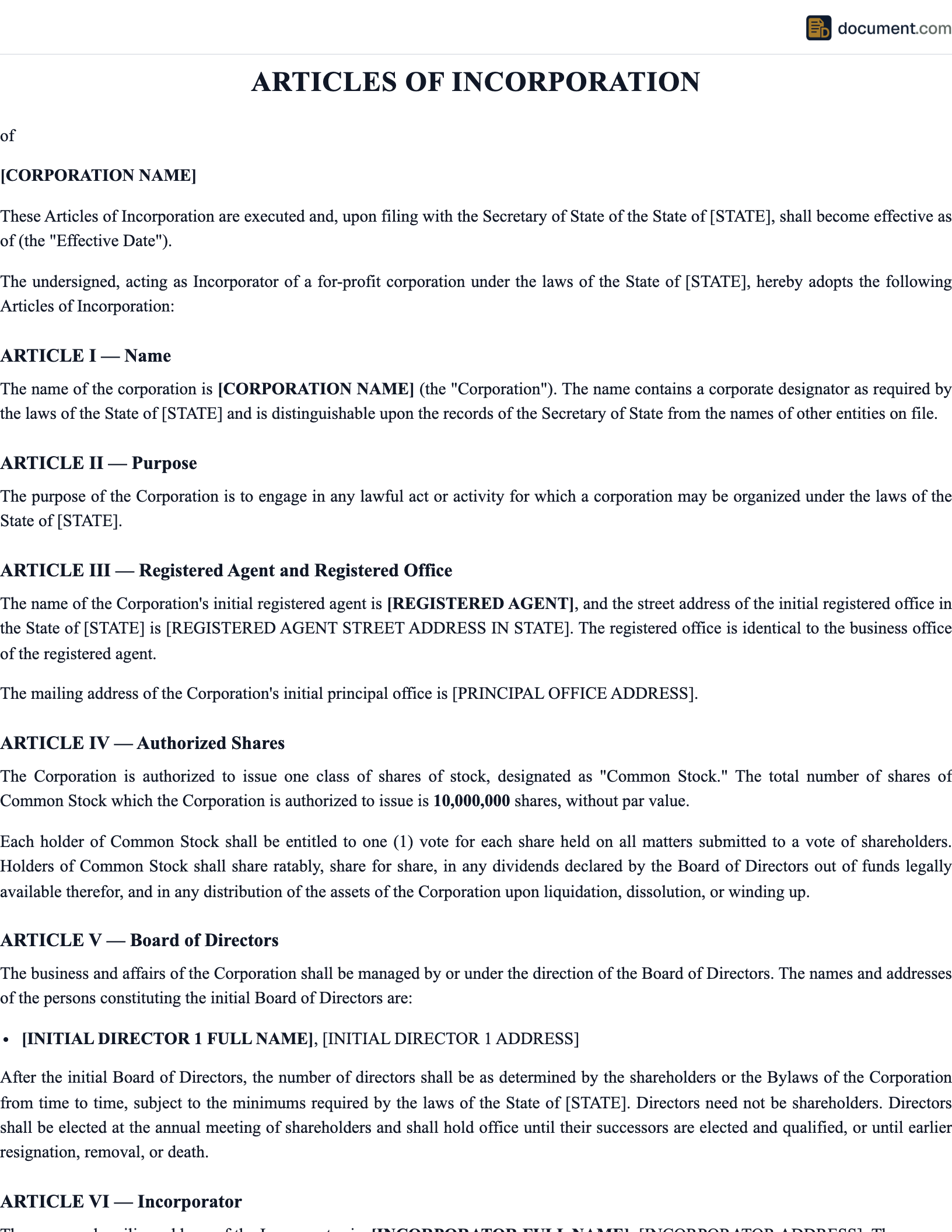

Articles of Incorporation Form Preview

Below is a visual preview of the key sections in a standard articles of incorporation filing. Your completed document will be formatted to meet your state's specific requirements and your chosen corporate structure.

Articles of Incorporation

Domestic For-Profit Corporation

Article I: Corporate Name

Article II: Registered Agent & Office

Article III: Authorized Capital Stock

Article IV: Purpose

Article V: Directors

Incorporator

Incorporator Signature

Types of Corporations

The corporate structure you choose affects your taxation, governance requirements, ownership limitations, and regulatory obligations. Each type has distinct characteristics that make it suitable for different business goals and industries.

C-Corporation

The C-Corporation is the default corporate tax classification and the most flexible corporate structure. C-Corps can issue unlimited shares, create multiple classes of stock (common and preferred with varying rights), have unlimited shareholders of any type (individuals, other corporations, foreign entities, trusts), and retain earnings without mandatory distribution. The trade-off is double taxation — the corporation pays corporate income tax (currently 21% at the federal level) on its profits, and shareholders pay personal income tax on dividends received. Despite this, C-Corps are the preferred structure for venture-backed startups because investors can receive preferred stock with liquidation preferences, the structure supports employee stock option plans (ISOs are only available to C-Corps and S-Corps), and the corporate form is required for an eventual IPO.

S-Corporation

An S-Corporation is not a separate type of corporation under state law — it is a C-Corporation that has filed Form 2553 with the IRS to elect pass-through taxation. Income, losses, deductions, and credits flow through to shareholders' personal tax returns, avoiding double taxation. However, S-Corps have strict eligibility requirements: no more than 100 shareholders, only U.S. citizens or residents as shareholders, only one class of stock (voting and non-voting variations are permitted), and no corporate or partnership shareholders. S-Corps are popular for established small businesses where the owners want to reduce self-employment taxes — shareholders who are also employees pay payroll taxes only on their salary, not on their share of the corporation's profits distributed as dividends.

Nonprofit Corporation

A nonprofit corporation is formed for charitable, educational, religious, scientific, or other exempt purposes and does not distribute profits to its directors, officers, or members. After incorporating under state law, the nonprofit applies to the IRS for tax-exempt status under IRC Section 501(c)(3) (or another applicable subsection), which exempts it from federal income tax and allows donors to deduct contributions. The articles of incorporation must include specific provisions required by the IRS: an exclusive purpose clause, a prohibition on private inurement, limitations on political activity, and a dissolution clause directing assets to another exempt organization. Nonprofits do not issue stock — they may have members with voting rights, but membership does not convey an ownership interest.

Professional Corporation

A professional corporation (PC or PLLC in some states) is a corporate form designed for licensed professionals — including physicians, attorneys, certified public accountants, architects, engineers, and veterinarians. Most states require licensed professionals to use this special corporate structure rather than a standard corporation. Key differences from a regular corporation include: all shareholders must hold the relevant professional license, the corporation's purpose is limited to the specific professional service, and shareholders remain personally liable for their own professional malpractice (though they are protected from liability for other shareholders' malpractice and general business debts). The articles must identify the professional service and comply with the state's professional corporation statute.

Corporation vs LLC vs Partnership

Choosing the right business entity is one of the most consequential decisions you will make. Each structure offers different advantages in terms of liability protection, taxation, management flexibility, and ability to raise capital.

| Feature | Corporation | LLC | Partnership |

|---|---|---|---|

| Liability Protection | Full (shareholders) | Full (members) | None (general partners) |

| Default Tax Status | Double taxation (C-Corp) | Pass-through | Pass-through |

| Ownership Transfer | Freely transferable (stock) | Restricted (by agreement) | Restricted (by agreement) |

| Management | Board + Officers (rigid) | Flexible (member/manager) | Partners (flexible) |

| Raising Capital | Stock issuance, IPO eligible | Membership interests | Partner contributions |

| Existence | Perpetual | Per operating agreement | May dissolve on withdrawal |

| Equity Compensation | Stock options (ISO/NSO) | Profits interests (complex) | Profits interests |

| Formation Document | Articles of Incorporation | Articles of Organization | Partnership Agreement |

How to File Articles of Incorporation

Incorporating requires careful planning of your corporate structure before filing. Follow these steps to ensure your corporation is properly formed and ready to operate.

Choose Your State and Corporate Type

Decide whether to incorporate in your home state or in a different state (Delaware is popular for companies seeking venture capital). Choose the corporate type that matches your goals: C-Corp for maximum flexibility and investor appeal, S-Corp for pass-through taxation (filed after incorporation), nonprofit for tax-exempt charitable purposes, or professional corporation if required by your licensing board. If you incorporate out of state, you will need to register as a foreign corporation in every state where you conduct business.

Plan Your Capital Structure

Determine how many shares to authorize, what par value to assign, and whether to create multiple classes of stock. Most startups authorize 10 million common shares at $0.0001 par value plus a pool of authorized-but-undesignated preferred shares for future investor rounds. For a small closely held corporation, 1,000-10,000 shares is typically sufficient. Remember that authorized shares affect franchise taxes in some states (particularly Delaware), so do not authorize significantly more shares than you plan to use.

Designate a Registered Agent and File

Select a registered agent with a physical address in the state of incorporation, complete the articles of incorporation with all required information, and file with the Secretary of State. Most states offer online filing with processing times ranging from same-day to two weeks. Pay the filing fee (typically $50-$300) and request a certified copy of the filed articles for your records. You will need the certified copy to open a corporate bank account, apply for an EIN, and complete other post-incorporation steps.

Hold the Organizational Meeting

After the state accepts the articles, the incorporator (or the initial directors, if named in the articles) must hold an organizational meeting to: appoint the board of directors (if not named in the articles), adopt corporate bylaws, elect officers (President, Secretary, Treasurer at minimum), authorize the issuance of stock, adopt a fiscal year, designate a bank for the corporate account, approve the form of stock certificate, and adopt any required resolutions (such as the S-Corp election). Minutes of this meeting should be recorded and kept in the corporate records.

Complete Post-Incorporation Compliance

Obtain an EIN from the IRS (free, online at irs.gov), issue stock to founders (with proper stock purchase agreements), file the S-Corp election if applicable (Form 2553, within 75 days of incorporation or by March 15 for the current tax year), open a corporate bank account, register for state and local taxes, file for required business licenses and permits, and set up your stock ledger to track all share issuances. If applicable, file Form 1023 (or 1023-EZ) for nonprofit tax-exempt status and any required state tax exemption applications.

Key Components of Articles of Incorporation

A properly drafted set of articles of incorporation includes both required and optional provisions that establish the corporation's legal framework.

Corporate Identity

- - Corporate name with required designator (Inc., Corp.)

- - Principal office and mailing addresses

- - State of incorporation and filing date

- - Corporate purpose (broad or specific)

- - Duration (perpetual or specified term)

Capital Structure

- - Number of authorized shares (common and preferred)

- - Par value per share (or no-par designation)

- - Classes and series of stock with rights

- - Voting rights per share class

- - Dividend and liquidation preferences

Directors & Officers

- - Number of initial directors (minimum varies by state)

- - Names and addresses of initial directors

- - Director liability limitation provisions

- - Indemnification provisions

- - Board structure (classified/staggered boards)

Protective Provisions

- - Director exculpation clause (DGCL 102(b)(7))

- - Indemnification to the fullest extent of law

- - Preemptive rights (if desired)

- - Cumulative voting provisions

- - Anti-dilution protections

Legal Requirements for Articles of Incorporation

Corporation statutes vary by state, but all states require certain core provisions in the articles of incorporation. Understanding these requirements ensures your filing is accepted on the first attempt and your corporation is properly structured from inception.

Model Business Corporation Act (MBCA)

The Model Business Corporation Act, developed by the American Bar Association, serves as the basis for corporation statutes in approximately 32 states. The MBCA requires articles of incorporation to include: the corporate name, the number of authorized shares, the registered agent and registered office, and the name and address of the incorporator. The MBCA also permits (but does not require) additional provisions such as the purpose of the corporation, the names of initial directors, provisions managing the corporation's internal affairs, and provisions limiting director liability. Delaware follows its own statute (the Delaware General Corporation Law), which has influenced corporate law nationwide and is often the benchmark for corporate governance provisions.

Director Liability Limitation (Section 102(b)(7))

One of the most important optional provisions in articles of incorporation is a director liability limitation clause. Delaware DGCL Section 102(b)(7) (and equivalent provisions in other states) allows the articles to include a provision eliminating or limiting the personal monetary liability of directors for breaches of their duty of care. This protection does not extend to breaches of the duty of loyalty, acts in bad faith, intentional misconduct, or illegal distributions. Virtually every corporation — from startups to Fortune 500 companies — includes this provision to attract qualified directors who might otherwise decline to serve due to personal liability concerns. Our templates include the appropriate exculpation language for your state.

Key State Variations

- Delaware: Uses the term "certificate of incorporation." Minimum filing fee of $89 plus franchise tax. No requirement to list directors in the certificate. Allows "blank check" preferred stock (board can designate rights and preferences without shareholder approval). Court of Chancery provides specialized corporate dispute resolution.

- California: Requires initial statement of information within 90 days of filing. Imposes $800 minimum annual franchise tax. Has specific requirements for close corporations and professional corporations. Does not require par value.

- Texas: Uses "certificate of formation." Filing fee of $300. Requires a minimum of one director. Allows series LLCs and benefit corporations. Texas Business Organizations Code governs all entity types.

- New York: Requires publication in two newspapers for six consecutive weeks within 120 days of incorporation. Requires at least one director. Filing fee of $125. Publication costs vary by county ($200-$1,500+).

Sample Articles of Incorporation

Below is a condensed preview of a Delaware certificate of incorporation for a standard C-Corporation. Your completed document will be customized for your specific state and corporate type.

CERTIFICATE OF INCORPORATION

of [Corporation Name], Inc.

FIRST: NAME

The name of the corporation is [Corporation Name], Inc. (the "Corporation").

SECOND: REGISTERED AGENT

The registered agent of the Corporation in the State of Delaware is[Agent Name], located at[Agent Address].

THIRD: PURPOSE

The purpose of the Corporation is to engage in any lawful act or activity for which corporations may be organized under the General Corporation Law of the State of Delaware.

FOURTH: AUTHORIZED CAPITAL STOCK

The total number of shares of all classes of stock that the Corporation shall have authority to issue is [Number] shares, consisting of:

- [Number] shares of Common Stock, par value $[Amount] per share

- [Number] shares of Preferred Stock, par value $[Amount] per share

The Board of Directors is hereby authorized to provide for the issuance of Preferred Stock in one or more series, and to fix for each series such voting powers, designations, preferences, and relative, participating, optional, or other special rights...

FIFTH: LIABILITY LIMITATION

A director of the Corporation shall not be personally liable to the Corporation or its stockholders for monetary damages for breach of fiduciary duty as a director, except to the extent such exemption from liability or limitation thereof is not permitted under the DGCL as the same exists or may hereafter be amended...

SIXTH: INDEMNIFICATION

The Corporation shall indemnify, to the fullest extent permitted by applicable law, any director or officer of the Corporation who was or is a party or is threatened to be made a party to any action, suit, or proceeding...

Frequently Asked Questions

Find answers to common questions about articles of incorporation, corporate formation, stock structure, and the incorporation process.

Official Resources

For additional information on corporate formation, governance, and compliance, consult these official and reputable resources.

SBA - Business Structure Guide

Compare entity types and choose the right structure for your business

Delaware Division of Corporations

Official Delaware corporate filing portal and fee schedule

IRS - Tax-Exempt Application

Apply for 501(c)(3) tax-exempt status for nonprofit corporations

ABA - Model Business Corporation Act

Official MBCA resources and state adoption information

Nolo - How to Incorporate

Step-by-step guide to incorporating your business

IRS - S Corporation Guide

IRS guidance on S-Corp election, eligibility, and filing requirements

Create your Articles of Incorporation in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.