What Is a Partnership Dissolution Agreement?

A partnership dissolution agreement is a binding written contract signed by all partners that formally ends a partnership and sets the terms for winding up its affairs. It documents the partners' collective decision to cease operations, describes how the partnership's remaining assets and liabilities will be handled, allocates final profits and losses, assigns responsibility for post-dissolution tasks like final tax returns, and provides mutual releases so the partners can close the books on their business relationship with as little lingering legal exposure as possible.

Under the Revised Uniform Partnership Act (RUPA) — adopted in some form by nearly every state — dissolving a partnership is a three-stage process. First, a dissolution event occurs: the partners vote to dissolve, a partner withdraws, a triggering event specified in the partnership agreement happens, a court orders dissolution, or some operation of law (like the business becoming illegal) ends the partnership. Second, the partnership enters a "winding up" period during which its only authorized activities are those reasonably necessary to conclude partnership affairs. Third, after winding up is complete, the partnership terminates and ceases to exist.

The dissolution agreement is the governing document for this entire process. It memorializes the effective date of dissolution, identifies who is responsible for winding up, establishes how assets will be liquidated or distributed in kind, sets the order of payment for creditors and partners, addresses ongoing contracts and litigation, handles the partnership's intellectual property and trade name, and provides the releases and indemnifications needed to protect the partners from future disputes. Without a written dissolution agreement, the process is governed entirely by default state law — which is often not what any of the partners actually want.

Partnership dissolutions happen for many reasons: the partners have accomplished what they set out to do, one partner is retiring or moving on, the business is no longer profitable, the partners have fundamental disagreements, or a triggering event in the original agreement has occurred. No matter the reason, a clear written dissolution agreement protects every partner and provides the structure needed to wind down the business in an orderly, fair, and legally compliant way.

Orderly Wind-Up

Set a clear roadmap for settling accounts, paying creditors, and distributing assets

Mutual Releases

Release partners from future claims arising out of the partnership relationship

Legal Compliance

Meet state filing requirements and creditor-notice rules for a clean termination

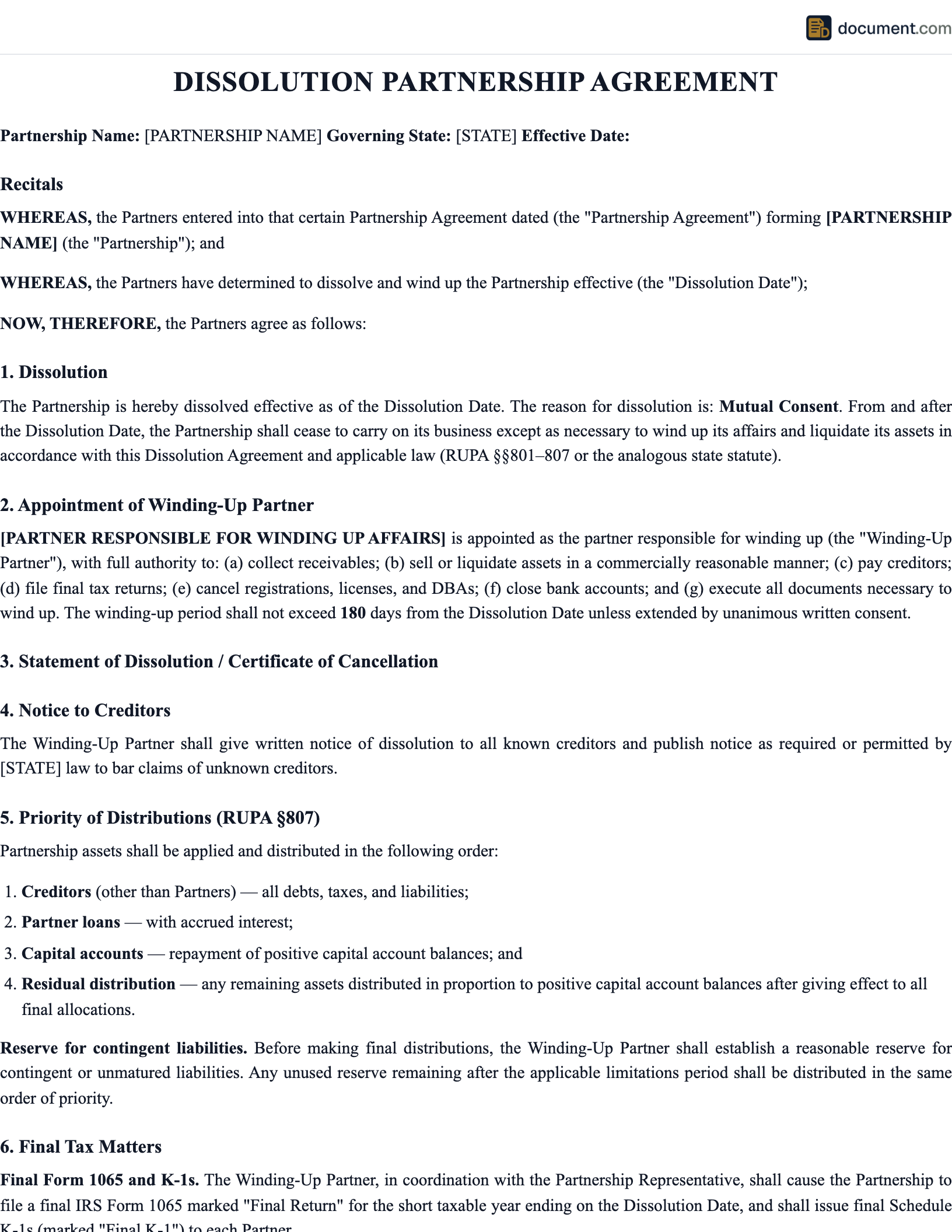

Dissolution Agreement Form Preview

Below is a visual preview of the sections included in our dissolution agreement template.

Partnership Dissolution Agreement

And Plan of Winding Up

Section 1: Partnership Information

Section 2: Assets & Liabilities

Section 3: Winding-Up Tasks

Section 4: Execution

Partner Signature

Notary Public

Reasons for Dissolving a Partnership

Partnerships end for a wide variety of reasons. Some are planned, some are triggered by external events, and some are driven by interpersonal conflict. A written dissolution agreement is valuable in every scenario — even a friendly dissolution — because it locks in the terms before memories fade or disputes arise.

Mutual decision to wind down

The partners agree that the business has run its course, that a major partner is retiring, or that each partner wants to pursue new opportunities. This is the cleanest form of dissolution and typically proceeds on a cooperative basis.

The partnership reached its original term

Many partnership agreements set a fixed term (e.g., 5 years for a specific project). When the term expires, the partnership dissolves automatically under the agreement unless the partners explicitly extend it.

A triggering event occurred

The partnership agreement specifies events that trigger dissolution — such as the death, incapacity, or bankruptcy of a partner, the loss of a required license, or a material breach by a partner. When the event happens, the wind-up process begins.

Irreconcilable disagreement

The partners have reached a deadlock they cannot resolve, and continuing the business has become impracticable. If the partners cannot voluntarily dissolve, any partner can petition a court for judicial dissolution under most state statutes.

Financial distress

The partnership can no longer meet its obligations, is not profitable, or is heading toward insolvency. Dissolution is often the responsible choice to prevent further losses and protect creditors.

Conversion to a new entity

The partners want to convert the business to a different entity type (LLC, corporation) for tax, liability, or operational reasons. The partnership is dissolved and its assets are contributed to the new entity.

Types of Dissolution

Dissolutions fall into several categories based on how and why they occur. The category affects the procedural requirements, the default asset-distribution rules, and the rights of the partners.

Voluntary Dissolution

All partners mutually agree to wind up and terminate the partnership

Expiration of Term

The partnership reaches the end date set forth in the original agreement

Event-Triggered Dissolution

A specified event (death, bankruptcy, withdrawal) triggers dissolution under the agreement

Judicial Dissolution

A court orders dissolution due to deadlock, misconduct, or impracticability

Dissolution by Operation of Law

Automatic dissolution triggered by illegality, loss of required license, or similar

Buyout in Lieu of Dissolution

Remaining partners buy out a departing partner instead of winding up

Technical Termination

Tax-driven dissolution tied to 50%+ change in partnership interests

Dissolution with Continued Business

Dissolve the partnership but continue the business under a new entity

Dissolution vs. Withdrawal vs. Buyout

Dissolution is not the only way a partner can exit a partnership. Understanding the differences helps you choose the right approach.

| Approach | What Happens | Business Continues? |

|---|---|---|

| Dissolution | Partnership is wound up and terminated | No — business ends |

| Withdrawal | One partner exits; remaining partners may continue | Often, if agreement permits continuation |

| Buyout | Remaining partners purchase departing partner's interest | Yes — ownership changes but business continues |

| Conversion | Partnership is dissolved and converted to LLC or corporation | Yes — under a new legal structure |

How to Dissolve a Partnership

Dissolving a partnership properly protects all partners from future liability and ensures the business ends on solid legal footing. Follow these steps.

Review the partnership agreement

Find the dissolution section. Identify the vote required, the effective date rules, who handles winding up, and how assets and liabilities are allocated.

Hold a partners' meeting and vote

Convene a formal partners' meeting (or circulate a written consent) and vote on dissolution. Document the vote in meeting minutes or a signed written consent resolution.

Draft and sign the dissolution agreement

Use our template to draft the dissolution agreement. Include effective date, wind-up plan, asset and liability allocations, releases, and signature blocks for every partner.

Notify creditors, customers, and third parties

Send written notice of dissolution to all known creditors, customers, vendors, lenders, and the landlord. Consider publishing a notice of dissolution in a local newspaper for constructive notice to unknown creditors.

File state dissolution documents

For LPs and LLPs, file a Certificate of Cancellation or Statement of Dissolution with the Secretary of State. Some states also allow general partnerships to file a Statement of Dissolution under RUPA § 805 for third-party notice.

Wind up operations

Collect receivables, pay debts in the statutory order, complete or assign existing contracts, liquidate non-distributable assets, and cancel business licenses, permits, leases, and insurance policies.

File final tax returns

File the final federal Form 1065 (marked 'Final Return'), final state partnership returns, and final payroll and sales tax returns. Issue final Schedule K-1s to each partner. Close the partnership's EIN with the IRS.

Distribute remaining assets

After all liabilities are paid, distribute the remaining assets according to the capital account balances and the dissolution agreement. Document each distribution in writing.

Preserve records

Store the dissolution agreement, final financial statements, final tax returns, creditor notices, and signed releases for at least seven years. Former partners may need these records for tax audits or future disputes.

Key Components of a Dissolution Agreement

A complete dissolution agreement should include each of these elements.

Partnership identification

Full legal name, state of formation, date of original partnership agreement, and names of all partners.

Recitals

Short background explaining why the partners are dissolving and any relevant facts about the partnership's history.

Effective date of dissolution

The date the partnership is considered dissolved for legal purposes. This may differ from the date winding up completes.

Winding-up responsibilities

Designate a winding-up partner (or committee), describe their duties, and set authority limits for post-dissolution actions.

Asset and liability schedule

Complete list of partnership assets (cash, receivables, equipment, IP, real estate) and liabilities (debts, pending contracts, tax obligations).

Order of payment

Confirm that creditors will be paid before partners, in the order required by state law and the partnership agreement.

Distribution plan

How final surplus will be allocated among the partners after all creditors and partner loans are paid.

Mutual releases and indemnification

Mutual releases of claims arising from the partnership and indemnification provisions for pre-dissolution liabilities.

Tax and reporting responsibilities

Who will prepare and file the final Form 1065, state returns, and K-1s; who will retain records.

Non-compete / non-solicit (if applicable)

Any post-dissolution restrictions on the former partners, such as not soliciting the same clients for a specified period.

Dispute resolution

How disputes arising out of the dissolution will be resolved (negotiation, mediation, arbitration, or litigation).

Signature block

Signature lines for every partner, with dates, printed names, and (optionally) notary acknowledgment.

Winding Up & Asset Distribution

Winding up is the period between dissolution and termination during which the partnership settles its affairs. Under RUPA, the partnership continues to exist during winding up, but its authority is limited to actions reasonably necessary to conclude its business.

Order of distribution under RUPA: (1) Obligations to creditors other than partners (trade debts, loans, taxes, judgments); (2) Obligations to partners other than for capital or profits (e.g., loans a partner made to the partnership); (3) Return of partner capital contributions; (4) Profits or any surplus remaining after the first three categories are satisfied. Each category must be fully paid before the next category receives anything.

Negative capital accounts:If a partner's capital account has a negative balance after allocating losses, that partner typically must contribute additional capital to restore their account to zero. This is most common when the partnership has sustained losses or when a partner took distributions in excess of their capital. Partnership agreements can modify this default rule, but most do not.

In-kind distributions:Some partnership assets (real estate, equipment, intellectual property) may be distributed in kind to a partner rather than sold. In-kind distributions require unanimous consent in many partnerships and create tax consequences for the receiving partner based on the asset's fair market value and the partner's outside basis. Work with a CPA to structure in-kind distributions properly.

Tax Consequences of Dissolution

Dissolving a partnership has significant federal and state tax consequences that every partner should understand before signing the dissolution agreement.

- Final Form 1065. The partnership must file a final federal partnership return (Form 1065) marked "Final Return" for the year in which it dissolves. Final K-1s must be issued to each partner.

- Gain or loss on distribution. Each partner may recognize gain or loss on the final distribution depending on their outside basis. Cash distributions in excess of basis trigger gain; property distributions generally do not trigger immediate gain.

- Depreciation recapture. Distribution of depreciated property can trigger ordinary-income recapture under IRC § 1245 or § 1250.

- Hot assets. Sale or distribution of "hot assets" (unrealized receivables and inventory) under IRC § 751 can convert capital gain into ordinary income for the selling partner.

- State-level taxes. Many states impose franchise taxes, gross receipts taxes, or minimum fees that continue until the partnership formally terminates and files final state returns.

- Close the EIN. After the final Form 1065 is filed and accepted, the partnership should send a letter to the IRS to close the EIN.

Always consult a CPA or tax attorney before finalizing the dissolution. Small timing changes (e.g., dissolving on January 2 vs. December 31) can have significant tax impact.

Legal Requirements

A partnership dissolution must meet several legal requirements, some of which vary based on the type of partnership and the state of formation.

- Vote required. The vote required to dissolve must match what the partnership agreement or state law specifies — typically unanimous consent for a partnership at will, or as set forth in the agreement for a term partnership.

- Written agreement. While some states recognize oral dissolutions in limited circumstances, a written dissolution agreement signed by all partners is always the best practice.

- Creditor notice. Partners must give written notice to known creditors and should consider publishing notice for unknown creditors.

- State filings. LPs and LLPs must file dissolution documents with the state. General partnerships may optionally file under RUPA § 805 for third-party notice.

- Tax filings. Final federal and state partnership returns are mandatory. Final employment tax and sales tax returns are also required for businesses with employees or taxable sales.

- Distribution priority. Assets must be distributed in the statutory order: creditors first, then partners for non-capital claims, then capital, then surplus.

- Fiduciary duties. Partners retain fiduciary duties during winding up and must act in good faith with respect to the wind-up process.

Sample Dissolution Agreement

Below is a condensed preview of our dissolution agreement template.

PARTNERSHIP DISSOLUTION AGREEMENT

and Plan of Winding Up

This Partnership Dissolution Agreement ("Agreement") is entered into as of [Effective Date] by and among the partners of [Partnership Name] (the "Partnership"), a partnership formed under the laws of the State of [State].

1. DISSOLUTION

The Partners hereby agree to dissolve the Partnership effective as of the Effective Date. The Partnership shall cease all business operations other than those necessary to wind up the Partnership's affairs.

2. WINDING UP

[Name] shall serve as the Winding-Up Partner and shall be responsible for collecting receivables, paying obligations, liquidating assets, and distributing remaining proceeds to the Partners in accordance with this Agreement and applicable law.

3. DISTRIBUTION OF ASSETS

After payment of all Partnership liabilities (including amounts owed to third parties and amounts owed to Partners other than for capital or profits), the remaining assets shall be distributed to the Partners in accordance with their respective capital account balances, and any surplus shall be distributed according to the profit-sharing percentages set forth in the original Partnership Agreement.

4. MUTUAL RELEASE

Except for the obligations set forth in this Agreement, each Partner hereby releases and forever discharges each other Partner from any and all claims, demands, actions, and causes of action, whether known or unknown, arising out of or related to the Partnership...

5. TAX REPORTING

The Winding-Up Partner shall cause the Partnership to file a final Form 1065 and issue final Schedule K-1s to each Partner. The Partners agree to cooperate in the preparation of all final tax filings.

6. STATE FILINGS

The Winding-Up Partner shall file any certificates, statements, or other documents required to effectuate the dissolution under applicable state law, including a Certificate of Cancellation if the Partnership is registered with the Secretary of State...

7. GOVERNING LAW

This Agreement shall be governed by and construed in accordance with the laws of the State of [State].

Frequently Asked Questions

Common questions about partnership dissolution, winding up, and termination.

Official Resources

For authoritative information on dissolving partnerships and post-dissolution obligations.

IRS - Closing a Business

Federal checklist for closing a business, including final tax return requirements

IRS - Partnerships

IRS guidance on Form 1065, K-1s, and final partnership returns

ULC - Revised Uniform Partnership Act

Uniform Law Commission text of RUPA and state adoption status

SBA - Close or Sell Your Business

U.S. Small Business Administration guide to closing a business

NASS - Secretary of State Directory

Find your state's business filing office for dissolution paperwork

Cornell Law - Uniform Partnership Act

Full text of the Uniform Partnership Act with annotations

ABA - Business Law Section

ABA resources on partnership dissolution and wind-up

IRS - Canceling an EIN

How to close your partnership's EIN after final return

Create your Dissolution Partnership Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.