What Is a Commercial Purchase Letter of Intent?

A commercial purchase letter of intent is a preliminary agreement that establishes the key terms under which a buyer proposes to acquire commercial real estate from a seller. Unlike residential transactions where standardized purchase contracts are common, commercial real estate transactions typically begin with an LOI because the deal structures are far more complex — involving multi-million dollar purchase prices, sophisticated financing arrangements, environmental liability allocations, and extensive due diligence requirements that can take months to complete. The LOI allows both parties to reach agreement on fundamental deal terms before either side invests in the substantial expense of environmental assessments, property condition reports, appraisals, surveys, title searches, and legal documentation.

Commercial property acquisitions present unique risks that the LOI must address. Environmental contamination can create liability that exceeds the property value under federal Superfund (CERCLA) and state environmental statutes. Zoning restrictions may limit the buyer's intended use. Existing tenant leases may contain provisions that affect property value — below-market rents, upcoming lease expirations, tenant improvement obligations, or co-tenancy requirements. The physical condition of the building may require substantial capital expenditures for deferred maintenance, code compliance, or ADA accessibility upgrades. By identifying these risk areas in the LOI and establishing the buyer's right to investigate each during due diligence, both parties set clear expectations for the transaction timeline and potential deal-breakers.

The financial structure of a commercial purchase LOI differs significantly from business acquisition LOIs. Commercial property buyers typically obtain financing through commercial mortgage loans, which require independent appraisals, environmental assessments, and property condition reports as conditions of loan commitment. The LOI must accommodate the lender's requirements and timeline — particularly the appraisal process, which can take 4-8 weeks for complex properties — while also protecting the buyer's earnest money if financing falls through. Additionally, commercial properties may involve seller financing, 1031 exchange accommodations, or assumption of existing mortgage debt, all of which should be addressed at the LOI stage.

Due Diligence Framework

Establishes environmental, physical, financial, and legal investigation rights and timelines.

Financing Structure

Defines purchase price, deposit structure, and financing contingencies with lender timelines.

Risk Allocation

Addresses environmental liability, title defects, and existing lease obligations.

Commercial Purchase LOI Form Preview

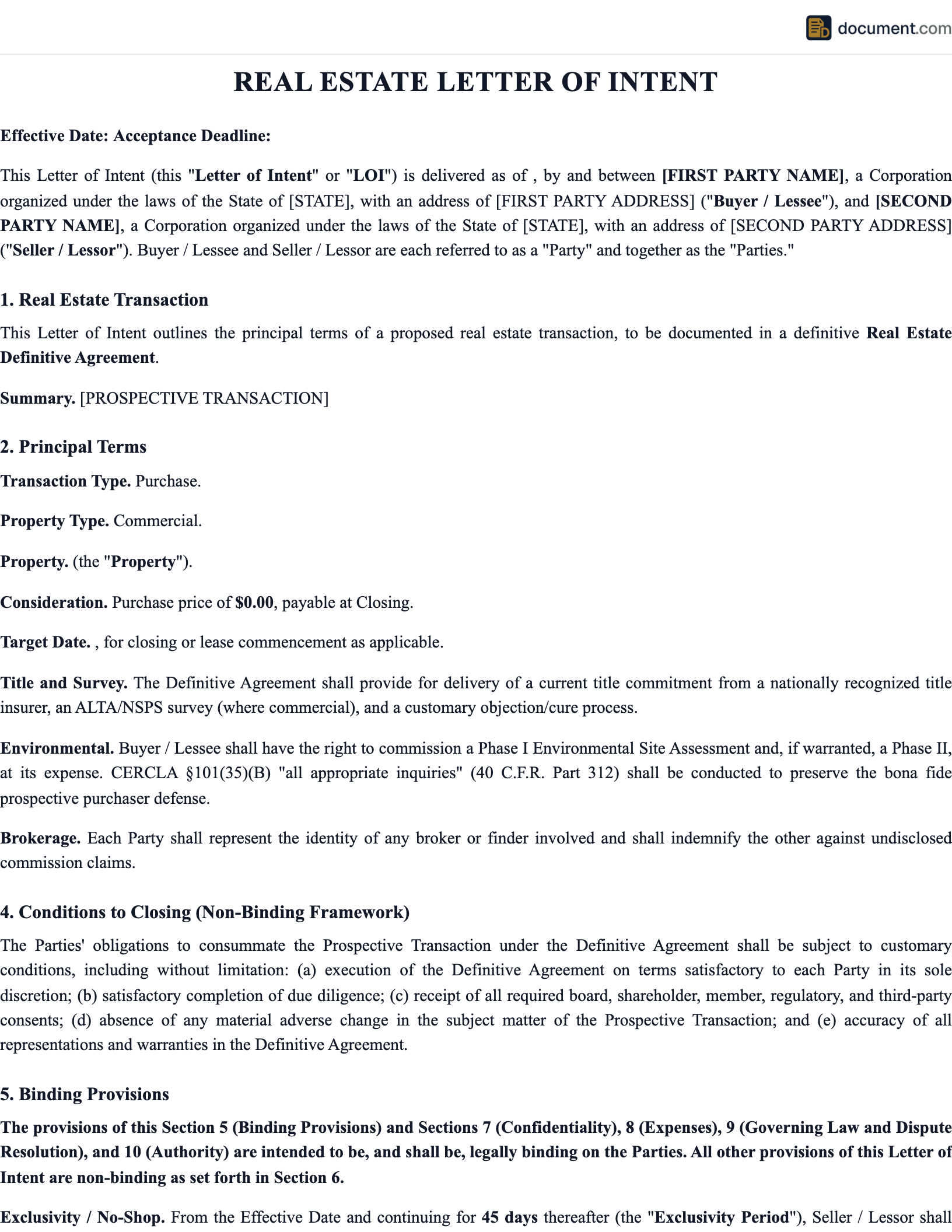

Letter of Intent

Proposed Acquisition of Commercial Property

1. PROPERTY AND PARTIES

This Letter of Intent sets forth the principal terms under which ("Buyer") proposes to acquire the property located at (the "Property") from ("Seller").

2. PURCHASE PRICE

Buyer proposes to acquire the Property for a total purchase price of $ payable at closing, subject to prorations and customary adjustments.

3. DUE DILIGENCE PERIOD

Buyer shall have days from the effective date to conduct environmental, physical, financial, and legal due diligence on the Property.

BUYER

SELLER

Key Components

A commercial purchase LOI must address these essential elements to create a productive framework for negotiating the definitive purchase and sale agreement:

| Component | Purpose | Key Details |

|---|---|---|

| Purchase Price | Establishes property valuation | Total price, price per square foot, valuation methodology, adjustments for deferred maintenance |

| Earnest Money | Demonstrates buyer commitment | Deposit amount (1-3%), soft vs. hard deposit timeline, escrow agent, refund conditions |

| Due Diligence Period | Enables property investigation | Timeline (30-90 days), environmental, physical, financial, legal scope, termination rights |

| Financing Contingency | Protects buyer if financing fails | Loan amount, LTV ratio, interest rate ceiling, commitment deadline, cash purchase alternative |

| Environmental Assessment | Identifies contamination liability | Phase I ESA, Phase II rights, remediation cost allocation, innocent landowner defense |

| Title and Survey | Confirms clear ownership | Title commitment, ALTA survey, permitted exceptions, objection and cure process |

| Closing Conditions | Defines requirements for completion | Target closing date, prorations, transfer documents, tenant estoppels, SNDA agreements |

How to Draft a Commercial Purchase Letter of Intent

Identify the Property and Parties

Provide the complete legal description or street address of the property, the tax parcel identification number, the approximate square footage and acreage, and the current zoning designation. Identify the buyer and seller entities by legal name and state of organization, and specify whether the buyer intends to assign the LOI to a newly formed acquisition entity (an SPE or LLC) prior to closing — a common practice in commercial real estate transactions for liability isolation and financing purposes.

Establish Purchase Price and Earnest Money

State the proposed purchase price and the basis for valuation — whether based on a cap rate applied to net operating income, price per square foot, price per unit for multifamily, or another methodology. Specify the earnest money amount, the escrow agent, the timeline for depositing the funds (typically within 3-10 business days of LOI execution), and the conditions under which the deposit is refundable versus non-refundable. Address whether the deposit goes hard after due diligence expiration and the amount of any additional hard deposit.

Define the Due Diligence Framework

Establish a comprehensive due diligence period (typically 30-90 days for commercial properties) encompassing: Phase I environmental assessment with Phase II rights, property condition assessment by a qualified engineer, ALTA survey, title commitment and exception review, estoppel certificates from tenants, review of existing leases and service contracts, financial audit of property income and expenses, zoning and land use verification, and assessment of any pending or threatened litigation. Specify the seller's obligation to provide access and documentation within defined timeframes.

Address Financing and Contingencies

If the purchase is financed, specify the loan parameters the buyer is seeking: loan-to-value ratio, interest rate range, loan term and amortization, and the deadline for obtaining a financing commitment letter. Include a financing contingency allowing the buyer to terminate if financing on acceptable terms cannot be obtained by the specified deadline. For 1031 exchange transactions, reserve the right to assign the contract to a qualified intermediary and specify cooperation requirements. Address any other contingencies: zoning changes, governmental approvals, partner or board approval, or satisfaction of existing contract conditions.

Outline Closing Terms and Prorations

Establish the target closing date and the documents the seller must deliver: deed (special warranty or general warranty), bill of sale for personal property, assignment of leases and contracts, tenant estoppel certificates, SNDA agreements for tenants with leases, seller's closing certificate, FIRPTA affidavit, and any required state or local transfer tax declarations. Specify proration methodology for property taxes, rents, operating expenses, security deposits, and prepaid items. Address which party pays for title insurance, transfer taxes, recording fees, and other closing costs per local custom.

Include Exclusivity and Binding Provisions

Designate the substantive deal terms as non-binding and specify the binding provisions: exclusivity period preventing the seller from marketing the property or negotiating with other buyers (typically 30-60 days), confidentiality obligations, expense allocation, and governing law. Include a clear statement that no purchase obligation arises until a definitive purchase and sale agreement is executed by both parties, and specify the expiration date of the LOI if a definitive agreement is not executed within the designated timeframe.

Due Diligence Considerations for Commercial Purchases

Due diligence for commercial real estate acquisitions is substantially more complex than for residential purchases and typically involves multiple specialized consultants. The LOI should establish the buyer's right to conduct comprehensive investigations across environmental, physical, financial, legal, and regulatory domains.

Environmental due diligence is often the most critical component because of the strict liability regime under CERCLA (the federal Superfund statute), which can hold current property owners liable for contamination cleanup costs regardless of when the contamination occurred or whether the owner caused it. The buyer must conduct a Phase I Environmental Site Assessment (ESA) meeting ASTM E1527-21 standards to qualify for the innocent landowner defense. If the Phase I identifies recognized environmental conditions (RECs), the buyer typically proceeds to a Phase II ESA involving soil borings, groundwater monitoring wells, and laboratory analysis to determine the nature and extent of any contamination.

Physical due diligence involves a property condition assessment (PCA) by a qualified building engineer who evaluates the structural integrity, roofing, HVAC systems, plumbing, electrical, fire protection, elevators, ADA accessibility, and estimated capital expenditure requirements over a 10-year replacement reserve period. The PCA findings directly affect the buyer's valuation because deferred maintenance and required capital improvements reduce the effective purchase price. Lenders typically require a PCA as a condition of financing and may require the borrower to fund an escrow for identified immediate repairs.

CERCLA Liability

Under the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), current owners of contaminated property can be held strictly liable for cleanup costs regardless of fault. The only reliable defense is the innocent landowner defense, which requires the buyer to conduct "all appropriate inquiries" (a Phase I ESA meeting ASTM standards) before acquiring the property. Failing to conduct environmental due diligence before closing can expose the buyer to cleanup costs that may exceed the purchase price of the property.

Frequently Asked Questions

Official Resources

Authoritative resources on commercial real estate acquisitions, environmental compliance, and property transactions.

EPA Brownfields Program

EPA resources on environmental site assessments, contaminated property transactions, and brownfield redevelopment incentives.

SBA - Buying Business Assets

Small Business Administration guidance on acquiring commercial property and business assets, including SBA loan programs.

IRS Publication 544 - Sales of Assets

IRS guidance on gain or loss from sale of property, including commercial real estate transactions and 1031 exchanges.

ALTA - American Land Title Association

Industry standards for title insurance, survey requirements, and closing procedures in commercial real estate.

CCIM Institute

Certified Commercial Investment Member resources on commercial real estate analysis, valuation, and transaction structuring.

NAIOP Research

National Association of Industrial and Office Properties research on commercial market trends and transaction practices.

Create Your Commercial Purchase LOI

Structure your commercial property acquisition with a professionally drafted letter of intent covering price, due diligence, financing, and closing conditions.

Create DocumentNo account required. Free to create and preview.