Wisconsin Equipment Lease Overview

In Wisconsin, equipment leasing is governed by the Uniform Commercial Code (UCC) Article 2A, which Wisconsin has adopted. This provides the legal framework for equipment lease formation, performance, warranties, and remedies. Wisconsin businesses commonly lease construction equipment, medical devices, restaurant and kitchen equipment, IT infrastructure, agricultural machinery, and manufacturing tools.

Wisconsin applies a state sales/use tax rate of 5.00% to equipment lease payments. The tax is typically applied to each periodic payment rather than the full equipment value upfront. Some equipment categories may qualify for Wisconsin tax exemptions, particularly manufacturing equipment, agricultural machinery, and equipment used in qualifying industries. Personal property tax on leased equipment in Wisconsin: Yes.

Whether you choose a capital lease (finance lease) or operating lease affects both your Wisconsin tax obligations and financial reporting. Capital leases with $1 buyout options are treated similarly to purchases for tax purposes, while operating lease payments are generally fully deductible as business expenses in Wisconsin.

5.00%

Sales/use tax rate

Adopted

UCC Article 2A

Yes

Personal property tax

Required by most lessors

Insurance

Wisconsin Equipment Leasing Requirements

When entering an equipment lease in Wisconsin, both lessors and lessees should ensure the agreement addresses all critical provisions required under WI law and UCC Article 2A:

Important: UCC Filing Requirements

In Wisconsin, lessors should consider filing a UCC-1 financing statement with the Wisconsin Secretary of State to perfect their interest in leased equipment. While not always required for a "true lease," filing protects the lessor's interest if the lease is later recharacterized as a secured transaction or if the lessee files for bankruptcy.

Essential Wisconsin Equipment Lease Provisions

- Equipment Description: Detailed description including make, model, serial number, year of manufacture, condition, and any accessories or attachments

- Lease Term & Payment: Duration, payment amount and frequency, security deposit, late fees, and any advance payments required

- Maintenance Obligations: Who is responsible for routine maintenance, repairs, and servicing per manufacturer specifications

- Insurance Requirements: Required by most lessors — types of coverage, minimum limits, and named insured requirements

- End-of-Lease Options: Purchase at FMV or fixed price, return conditions, renewal terms, and upgrade provisions

- Default & Remedies: Events of default, cure periods, repossession rights, and damage calculations under Wisconsin law

How to Complete a Wisconsin Equipment Lease

Follow these steps to properly complete your Wisconsin equipment lease agreement with all WI-specific provisions and industry-standard terms.

Identify the Parties

Enter the legal names and addresses of both the lessor (equipment owner) and lessee (equipment user). If either party is a business entity, include the entity type (LLC, Corp, etc.), state of formation, and the name and title of the authorized signer.

Describe the Equipment

Provide a detailed description of the equipment including the type, manufacturer, model number, serial number, year of manufacture, condition (new or used), and any included accessories, attachments, or software. The more specific the description, the better protected both parties are.

Set Lease Terms and Payment

Specify the lease commencement date, term length, payment amount, payment frequency (monthly, quarterly), and any security deposit or advance payments. Choose the lease type — capital lease with $1 buyout or operating lease with FMV purchase option. Factor in Wisconsin's 5.00% sales/use tax on lease payments.

Address Maintenance and Insurance

Define maintenance responsibilities — who maintains the equipment, required service schedules, and authorized repair providers. Specify insurance requirements including coverage types, minimum amounts, and the lessor's status as loss payee and additional insured. Wisconsin insurance requirement: required by most lessors.

Define End-of-Lease Options

Specify what happens when the lease ends: purchase at fair market value, purchase at a fixed price, return the equipment, or renew the lease. Include return condition standards, the process for determining FMV, and notice requirements (typically 60-90 days before expiration).

Execute the Agreement

Both parties sign and date the lease. If a personal guaranty is required, the guarantor signs separately. Each party retains an original executed copy. Consider filing a UCC-1 financing statement with the Wisconsin Secretary of State to protect the lessor's interest.

Wisconsin Equipment Lease Tax Treatment

Understanding the tax implications of equipment leasing in Wisconsin is essential for making the right financial decision between leasing and purchasing.

| Tax Type | Wisconsin Treatment |

|---|---|

| Sales/Use Tax | 5.00% applied to each lease payment |

| Personal Property Tax | Yes — assessed annually on depreciated value |

| Operating Lease Deduction | Payments fully deductible as business expense |

| Capital Lease Treatment | Depreciation + interest deduction (Section 179 may apply) |

| Exemptions | Manufacturing, agricultural, and other qualifying equipment may be exempt |

Wisconsin Equipment Leasing Regulations

Wisconsin equipment leases are governed by UCC Article 2A (adopted) and general Wisconsin contract law. Key regulatory considerations for equipment leasing in Wisconsin include:

UCC Article 2A Compliance

Wisconsin has adopted UCC Article 2A, which provides default rules for equipment lease formation, warranties, risk of loss, and remedies

True Lease vs. Secured Transaction

Wisconsin courts analyze whether an equipment lease is a "true lease" or a disguised secured transaction, which affects UCC filing requirements and bankruptcy treatment

UCC-1 Filing

Lessors should file a UCC-1 financing statement with the Wisconsin Secretary of State to protect their interest, especially for high-value equipment

Sales Tax Collection

Wisconsin requires collection of 5.00% sales/use tax on equipment lease payments, with the lessor typically responsible for collection and remittance

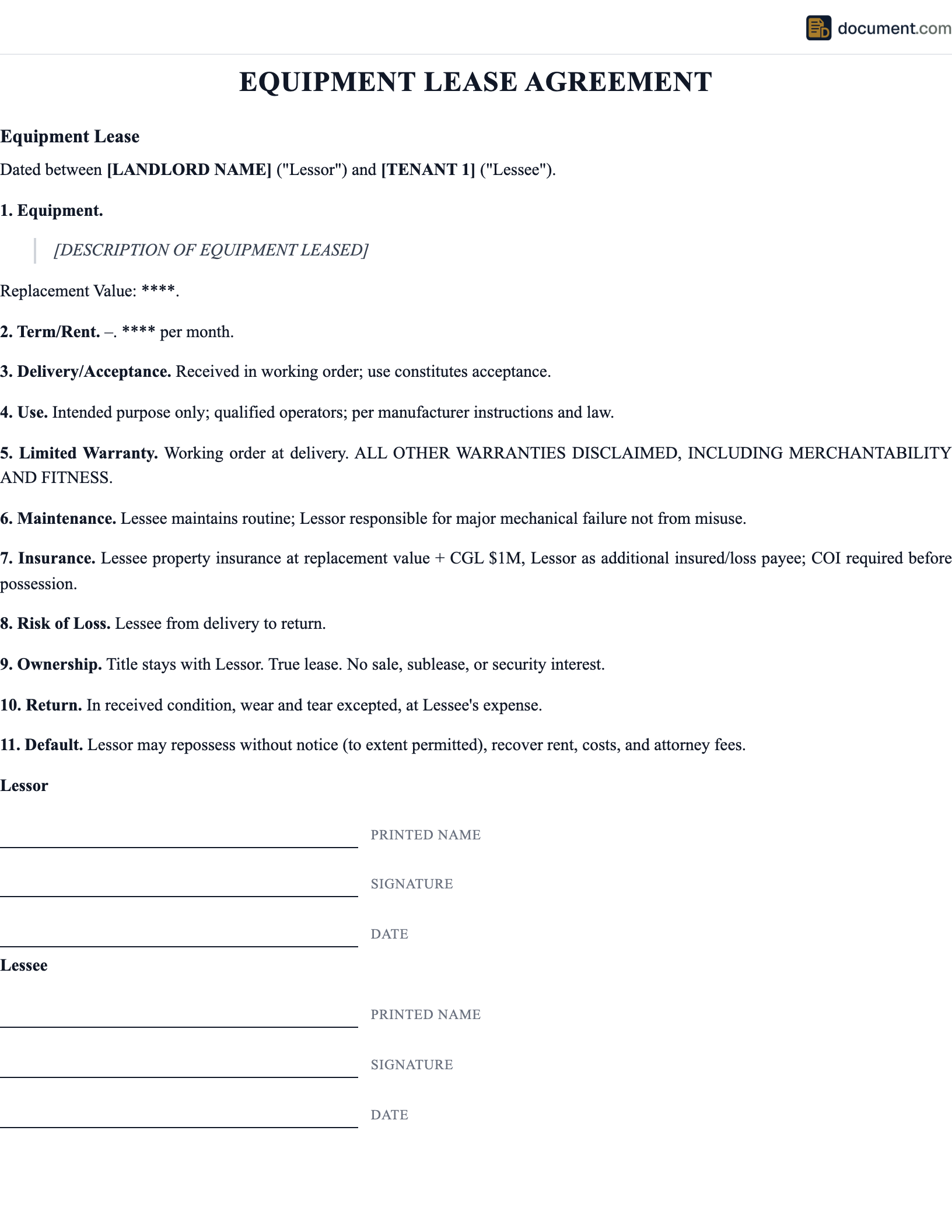

Sample Wisconsin Equipment Lease

Below is a preview of our Wisconsin-specific equipment lease agreement. Your customized document will include all provisions required under WI law and UCC Article 2A.

STATE OF WISCONSIN

EQUIPMENT LEASE AGREEMENT

Capital Lease / Operating Lease

LESSOR:

Name: [Lessor Name]

Address: [Wisconsin Address]

LESSEE:

Business: [Business Name]

Address: [Wisconsin Address]

EQUIPMENT

Type: [Type]

Make/Model: [Make/Model] Serial #: [Serial]

Condition: ☐ New ☐ Used

Lease Type: ☐ Capital ☐ Operating

Wisconsin Equipment Lease FAQ

Answers to common questions about Wisconsin equipment lease agreements, tax treatment, and UCC Article 2A compliance.

Official Wisconsin Resources

Use these official Wisconsin resources to verify equipment leasing regulations, tax requirements, and UCC filing procedures.

Wisconsin Secretary of State

UCC filings and business entity registration

Wisconsin Department of Revenue

Sales tax on equipment leases and exemptions

Equipment Leasing and Finance Association

Industry resources and equipment leasing best practices

SBA — Equipment Financing Resources

Federal small business equipment financing and leasing guidance

Other Wisconsin Lease Agreement Templates

Need a different type of lease agreement for Wisconsin? We offer state-specific templates for every type of rental arrangement.

Wisconsin Residential Lease

Houses, apartments, and condos

Wisconsin Month-to-Month Lease

Flexible rental agreements

Wisconsin Room Rental Agreement

Individual room rentals

Wisconsin Sublease Agreement

Subletting and assignment

Wisconsin Commercial Lease

Office, retail, and industrial space

Wisconsin Land Lease

Ground leases and vacant land

Create your Wisconsin Equipment Lease Agreement in under 5 minutes.

Answer a few questions and download a Wisconsin-compliant document, ready for the state agency.