What Is a Financial Advisor Consulting Agreement?

A financial advisor consulting agreement is a contract that governs the engagement between a client and an independent financial advisor who provides investment management, financial planning, or both. The independent advisory model has grown rapidly as advisors leave wirehouses and broker-dealers to establish their own registered investment advisory (RIA) firms or join independent advisory platforms, seeking greater autonomy over their investment philosophy, client relationships, and compensation. As of 2024, there are approximately 15,000 SEC-registered RIAs and over 17,000 state-registered RIAs in the United States, collectively managing trillions of dollars in client assets.

What distinguishes a financial advisor agreement from other independent contractor contracts is the overlay of securities regulation. Financial advisors operate in one of the most heavily regulated industries in the United States, subject to overlapping federal and state securities laws, FINRA rules (for broker-dealer representatives), the Investment Advisers Act of 1940 (for RIAs), SEC and state examination programs, and fiduciary duties that cannot be waived by contract. The agreement must navigate these regulatory requirements while establishing clear commercial terms for the advisory relationship.

The agreement also serves as a disclosure document. SEC Rule 204-3 requires RIAs to deliver their Form ADV Part 2A (the "brochure") to prospective clients before or at the time of entering into the advisory agreement. The brochure discloses the advisor's services, fees, investment strategies, potential conflicts of interest, disciplinary history, and other material information that the client needs to make an informed decision. The consulting agreement typically incorporates the Form ADV by reference and requires the client to acknowledge receipt.

Fiduciary Standard

Establishes the advisor's duty to act in the client's best interest.

Fee Transparency

Discloses all fees, conflicts, and compensation arrangements.

Data Protection

Addresses SEC Reg S-P, GLBA, and cybersecurity obligations.

Financial Advisor Agreement Form Preview

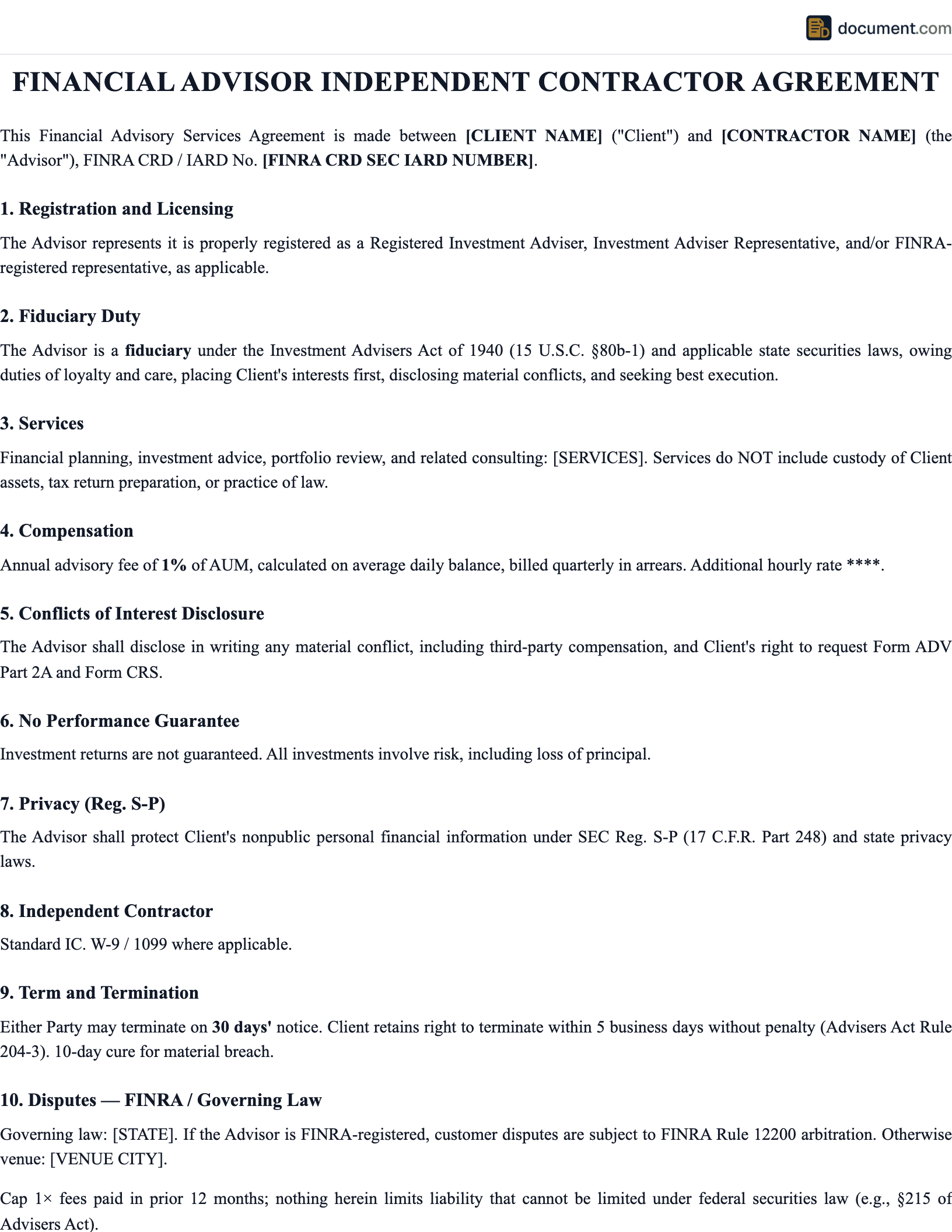

Investment Advisory Agreement

Independent Financial Advisor Engagement

1. ADVISORY SERVICES

Advisor, a registered investment adviser with the , shall provide the following services: . Advisor owes Client a fiduciary duty and shall act in Client's best interest at all times.

2. FEES AND COMPENSATION

Client shall compensate Advisor as follows: . Fees are calculated and billed and may be deducted from Client's account with prior written authorization.

3. CUSTODY AND TRADING AUTHORITY

Client assets shall be held at ("Custodian"). Advisor is granted trading authority over the account(s) listed in Exhibit A.

CLIENT SIGNATURE

ADVISOR SIGNATURE

Key Components

| Component | Purpose | Key Details |

|---|---|---|

| Advisory Scope | Defines services provided | Portfolio management, financial planning, tax planning, estate coordination |

| Fiduciary Duty | Establishes standard of care | Best interest obligation, duty of loyalty, duty of care |

| Fee Structure | Documents all compensation | AUM percentage, hourly, flat fee, retainer, commission disclosures |

| Custody & Trading | Defines asset custody and authority | Custodian identity, discretionary vs non-discretionary, trading limitations |

| Conflicts Disclosure | Identifies potential conflicts | Compensation conflicts, proprietary products, soft dollars, referral fees |

| Privacy & Cybersecurity | Protects client data | Reg S-P compliance, encryption, breach notification, data retention |

| Regulatory Compliance | Ensures legal requirements met | SEC/state registration, Form ADV delivery, recordkeeping, examination cooperation |

| Termination | Governs relationship end | Client right to terminate at any time, account transfer process, prorated fees |

How to Draft a Financial Advisor Consulting Agreement

Verify Regulatory Registrations

Confirm the advisor is registered with the SEC or appropriate state securities regulator, holds all required licenses (Series 65, 66, 7), and has a clean disciplinary record. Check the advisor's Form ADV on the SEC's Investment Adviser Public Disclosure (IAPD) website and review their BrokerCheck profile on FINRA's database.

Define the Scope of Advisory Services

Specify whether the engagement covers portfolio management only, comprehensive financial planning (retirement, education, tax, estate, insurance, cash flow), or both. Define whether the advisor has discretionary authority (the ability to trade without prior client approval for each transaction) or non-discretionary authority (the advisor recommends trades but the client must approve each one).

Document the Fee Structure

Disclose all fees clearly: the AUM rate schedule with breakpoints, the billing frequency (quarterly in advance or arrears), the method of fee deduction (directly from client accounts or by invoice), any financial planning fees in addition to AUM fees, and all third-party costs the client will bear (fund expense ratios, custodial fees, trading commissions). Comply with the fee disclosure requirements in Form ADV Part 2A.

Identify the Custodian and Grant Trading Authority

Specify the qualified custodian (Schwab, Fidelity, Pershing, TD Ameritrade) where client assets will be held. The custodian must be independent from the advisor — this is a core investor protection requirement. Document the scope of trading authority and any investment restrictions or guidelines the client wants to impose (no tobacco stocks, ESG criteria, maximum position sizes).

Disclose Conflicts of Interest

List all material conflicts in the agreement or incorporate the Form ADV Part 2A disclosures by reference. Address compensation conflicts, affiliated products, soft-dollar arrangements, referral relationships, and any other circumstances where the advisor's interests might diverge from the client's interests. Document how the advisor manages each conflict.

Deliver Form ADV and Execute

Deliver Form ADV Part 2A (brochure) and Part 2B (brochure supplement) to the client before or at the time of executing the agreement. Obtain the client's written acknowledgment of receipt. Execute the agreement and provide copies to both parties. Update the agreement annually or whenever there are material changes to the advisory services, fees, or conflicts.

Fee Models Compared

Choosing the right fee model affects the economics, regulatory obligations, and conflicts of interest in the advisory relationship:

| Model | Best For | Conflict Profile | Typical Range |

|---|---|---|---|

| AUM | Ongoing portfolio management | Aligned with growth; bias toward gathering assets | 0.5%-1.5% annually |

| Flat Fee | Comprehensive financial plan | Low conflict; scope must be well-defined | $2,000-$10,000 |

| Hourly | Specific consulting projects | Low conflict; incentive to extend hours | $150-$500/hour |

| Retainer | Ongoing advisory access | Moderate; must deliver ongoing value | $3,000-$12,000/year |

| Commission | Product sales (insurance, annuities) | Highest conflict; subject to Reg BI | Varies by product |

Regulatory Framework

Independent financial advisors operate under a multi-layered regulatory framework that the consulting agreement must address. At the federal level, the Investment Advisers Act of 1940 governs RIAs and imposes fiduciary duties, registration requirements (Form ADV), recordkeeping obligations (books and records rules), and examination authority. The Securities Exchange Act of 1934 and FINRA rules govern broker-dealer representatives. The SEC's Regulation Best Interest (Reg BI), effective since June 2020, imposes enhanced obligations on broker-dealers beyond the traditional suitability standard.

At the state level, each state's securities regulator (often called the "blue sky" administrator) has authority over state-registered investment advisers and may impose additional requirements beyond the federal framework. Several states have adopted fiduciary duty statutes that apply to all advisors serving state residents, and state data breach notification laws add a compliance layer for client data protection. The consulting agreement should identify the advisor's registration status (SEC-registered or state-registered), incorporate the Form ADV by reference, and include representations that the advisor will comply with all applicable federal and state securities laws and regulations throughout the engagement.

SEC Examination Focus Areas

The SEC's Division of Examinations publishes annual priorities that directly affect advisory agreements. Recent focus areas include: compliance with the fiduciary duty, adequacy of fee disclosures, cybersecurity preparedness, business continuity planning, ESG claims and greenwashing, private fund disclosures, and valuation of illiquid securities. The consulting agreement should be reviewed annually to ensure it addresses current examination priorities and reflects any regulatory changes.

Frequently Asked Questions

Official Resources

Authoritative resources on investment advisory regulation, fiduciary standards, and compliance.

SEC - Investment Management

SEC resources on investment adviser regulation, Form ADV, and examination.

SEC IAPD - Investment Adviser Public Disclosure

Search for registered investment advisers and review their Form ADV filings.

FINRA BrokerCheck

Verify financial advisor credentials, registrations, and disciplinary history.

NASAA - State Securities Regulators

North American Securities Administrators Association and state-level regulatory resources.

CFP Board

Certified Financial Planner standards, ethics, and fiduciary duty resources.

SEC Regulation Best Interest

Full text of Reg BI and the standard of conduct for broker-dealers.

Create Your Financial Advisor Agreement

Draft a regulatory-compliant advisory agreement with fiduciary protections and transparent fee disclosures.

Create DocumentNo account required. Free to create and preview.