What Is a Special Needs Trust?

A special needs trust (also called a supplemental needs trust) is a legal arrangement designed to hold and manage assets for the benefit of a person with disabilities without disqualifying them from essential government benefits like Supplemental Security Income (SSI) and Medicaid. These means-tested programs impose strict asset and income limits on eligibility. An individual generally cannot have more than $2,000 in countable resources ($3,000 for a couple) to qualify for SSI, and Medicaid eligibility is similarly restricted in most states. A properly drafted special needs trust holds assets outside the beneficiary's countable resources, preserving their eligibility while providing supplemental support that improves their quality of life.

The concept is straightforward but the execution is highly technical. If a family member leaves an inheritance directly to a person receiving SSI, that inheritance becomes a countable resource the moment it is received. If the inheritance exceeds $2,000, the beneficiary loses their SSI eligibility and, in most states, their Medicaid coverage along with it. Losing Medicaid can be catastrophic for a person with disabilities, because Medicaid often covers services worth tens of thousands of dollars per year, including personal care attendants, supported employment services, day programs, residential habilitation, therapies, durable medical equipment, and prescription medications. A special needs trust prevents this outcome by ensuring that inherited or gifted assets are held by a trustee who distributes funds at their discretion for the beneficiary's supplemental needs.

The trust operates as a supplement to government benefits, not a replacement. The trustee uses trust funds to pay for goods and services that SSI and Medicaid do not cover: a cell phone and service plan, a vacation, educational courses, a computer, personal care items, recreational activities, transportation, home modifications for accessibility, and countless other expenses that enhance the beneficiary's independence and well-being. The trustee must understand the rules governing distributions, because certain types of payments (particularly for food and shelter) can reduce SSI benefits, while others have no impact at all.

Our attorney-reviewed templates guide you through the critical decisions involved in creating a special needs trust: choosing between a first-party and third-party trust, selecting the right trustee, defining the scope of distributions, naming remainder beneficiaries, and complying with your state's trust law and Medicaid regulations. Each template is designed to satisfy the requirements of the Social Security Administration and your state's Medicaid agency.

Benefits Preserved

Maintain eligibility for SSI, Medicaid, and other government programs

Quality of Life

Fund supplemental needs that government benefits do not cover

Asset Protection

Shield trust assets from creditors and financial exploitation

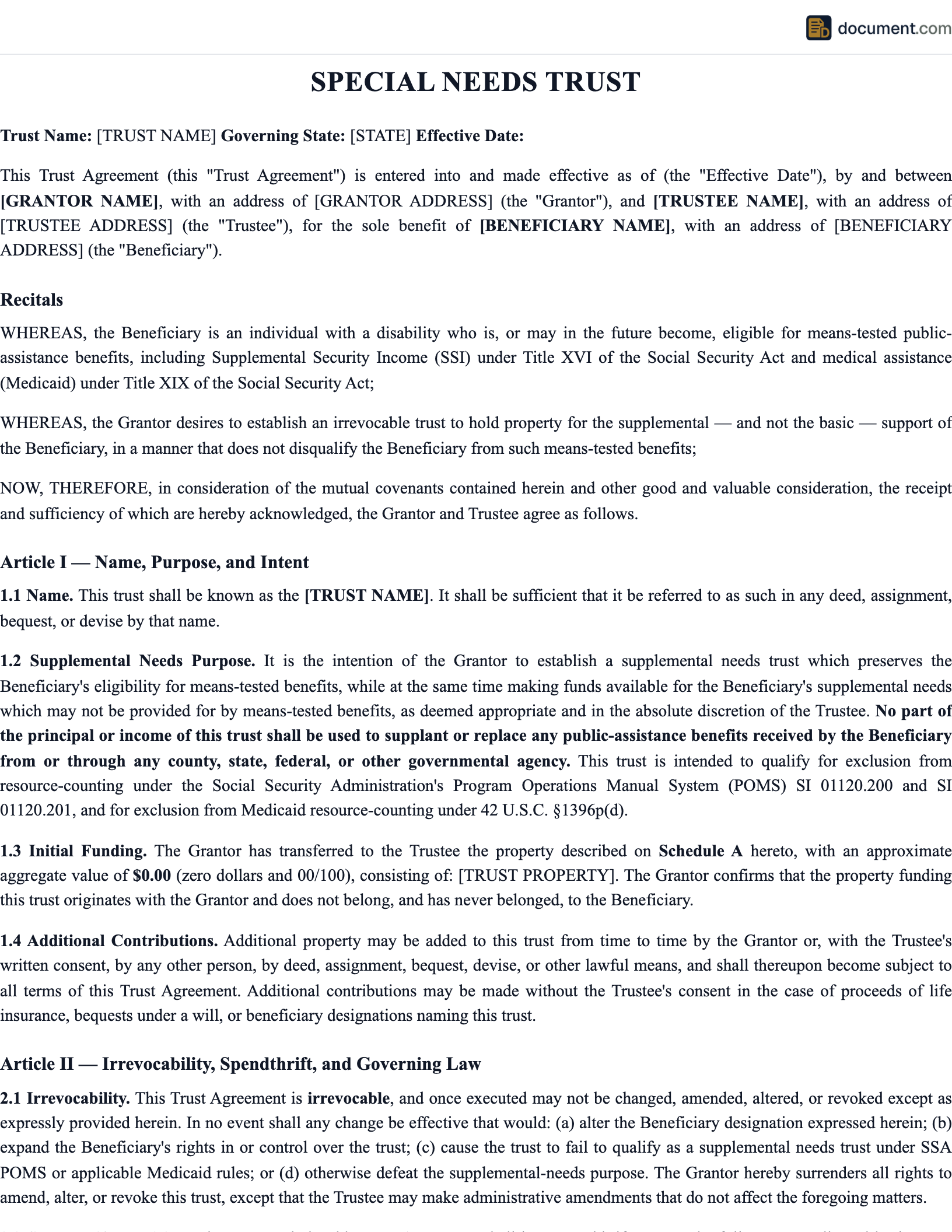

Special Needs Trust Form Preview

Below is a visual preview of the sections and fields in a special needs trust document. Your completed trust will be customized for your beneficiary's situation, the type of trust, and your state's requirements.

Special Needs Trust Agreement

Supplemental Needs Trust

Section 1: Grantor and Beneficiary

Section 2: Trustee Designation

Section 3: Trust Purpose and Distributions

Section 4: Execution

Grantor Signature / Date

Trustee Signature / Date

Witness Signature

Notary Public

Types of Special Needs Trusts

The right type of special needs trust depends on where the funding comes from, the beneficiary's age and circumstances, and whether a Medicaid payback provision is required. Each type serves a different planning objective.

Third-Party Special Needs Trust

Funded by family members, friends, or other parties with their own assets to benefit a person with disabilities without affecting benefits

First-Party Special Needs Trust (d4A)

Funded with the disabled beneficiary's own assets, such as an inheritance or personal injury settlement, with a Medicaid payback provision

Pooled Trust (d4C)

Managed by a nonprofit organization that pools assets from multiple beneficiaries for investment while maintaining separate accounts

ABLE Account Companion Trust

Works alongside an ABLE (Achieving a Better Life Experience) account to provide additional supplemental support beyond ABLE limits

Testamentary Special Needs Trust

Created through a will and takes effect after the grantor's death, often used by parents planning for a child with disabilities

First-Party vs Third-Party Special Needs Trust

The most fundamental decision in special needs trust planning is whether you need a first-party or third-party trust. The answer depends on whose money will fund the trust.

Key Differences

Third-Party Trust

- - Funded by someone other than the beneficiary

- - No age restriction on establishment

- - No Medicaid payback when beneficiary dies

- - Remainder goes to chosen beneficiaries

- - Can be revocable during grantor's lifetime

- - Most common for family planning

First-Party Trust (d4A)

- - Funded by the beneficiary's own assets

- - Beneficiary must be under 65 at establishment

- - Medicaid payback required at beneficiary's death

- - Remainder after payback goes to other beneficiaries

- - Must be irrevocable

- - Common for injury settlements and inheritances

Planning tip: Whenever possible, use a third-party trust because it avoids the Medicaid payback requirement. If a family member wants to leave assets to a person with disabilities, they should name the third-party special needs trust as the beneficiary in their will or beneficiary designations, rather than leaving assets directly to the person (which would require a first-party trust to preserve benefits).

How to Create a Special Needs Trust: A 7-Step Guide

Creating a special needs trust requires careful planning to ensure it preserves government benefits while providing meaningful supplemental support. Follow these seven steps to build a trust that protects your loved one.

Assess the Beneficiary's Current Benefits and Needs

Before creating the trust, understand exactly which government benefits the beneficiary currently receives or may need in the future. This includes SSI, Medicaid (including waiver services), Social Security Disability Insurance (SSDI), Medicare, Section 8 housing, SNAP (food stamps), and any state-specific disability programs. Document the monthly value of these benefits, because the trust must be designed to preserve them. Also assess the beneficiary's supplemental needs that are not covered by these programs: transportation, recreation, personal care beyond what Medicaid covers, technology, education, and other quality-of-life expenses. This assessment determines how the trust should be structured and helps the trustee understand their role.

Choose Between First-Party and Third-Party Trust

If the trust will be funded with the beneficiary's own assets (inheritance received outright, personal injury settlement, or the beneficiary's savings), you need a first-party (d4A) trust. If the trust will be funded by family members, friends, or others using their own assets, you need a third-party trust. If the beneficiary is over 65, a first-party individual trust cannot be established, but a pooled trust (d4C) managed by a nonprofit may be available. This choice has significant implications for the Medicaid payback requirement, the trust's flexibility, and what happens to remaining assets when the beneficiary dies.

Select the Trustee Carefully

The trustee will control the beneficiary's supplemental resources and must understand the complex rules governing distributions. Consider whether a family member, a professional fiduciary, or a combination through co-trustees is best for your situation. The trustee must be someone who will be attentive to the beneficiary's needs, financially responsible, willing to learn the SSI and Medicaid rules affecting distributions, and available for the long term (potentially decades). Name at least one successor trustee and consider including a mechanism for replacing trustees who are not serving effectively.

Define Distribution Standards

The trust document must include specific language giving the trustee sole and absolute discretion over distributions. The trust should state that distributions are intended to supplement, not replace, government benefits. Avoid language that gives the beneficiary any right to demand distributions, as this could cause the trust to be treated as a countable resource. Include guidance on approved expenditures (clothing, personal care, transportation, recreation, education, home modifications, assistive technology) and caution the trustee about distributions that could reduce benefits (food and shelter payments reduce SSI under the in-kind support and maintenance rules).

Name Remainder Beneficiaries

Decide who will receive any assets remaining in the trust when the beneficiary dies. For third-party trusts, remainder beneficiaries are often the beneficiary's siblings, nieces and nephews, or charitable organizations. For first-party trusts, remember that the state Medicaid agency must be reimbursed first for all medical assistance paid during the beneficiary's lifetime before any remainder can pass to other beneficiaries. Consider naming multiple contingent remainder beneficiaries in case the primary remainder beneficiary predeceases the beneficiary.

Fund the Trust

For third-party trusts, the most common funding strategies include purchasing life insurance with the trust named as beneficiary (creating a substantial fund at relatively low premium cost), transferring cash or investment assets directly, naming the trust as a beneficiary in wills and retirement accounts, and directing gifts from family and friends to the trust. For first-party trusts, funding typically involves transferring a personal injury settlement, inheritance, or other assets belonging to the beneficiary. The transfer must be done carefully to minimize the period during which the beneficiary holds excess countable resources.

Execute, Fund, and Review Regularly

Sign the trust document with proper formalities (notarization and witnesses as required by your state). For first-party trusts involving minors or incapacitated individuals, court approval may be required. After execution, fund the trust promptly and provide the trustee with a copy of the trust document, a letter of intent describing the beneficiary's needs and preferences, and contact information for the beneficiary's service providers. Review the trust periodically (at least every few years) to ensure it remains compliant with current SSI, Medicaid, and tax law, and update it if the beneficiary's circumstances change significantly.

Key Components of a Special Needs Trust

A properly drafted special needs trust contains specific provisions required by federal and state law to preserve government benefits. Below are the essential components that every special needs trust must address.

| Component | Description |

|---|---|

| Supplemental Purpose Statement | Explicit language stating the trust supplements, not supplants, government benefits |

| Discretionary Distribution Standard | Sole and absolute discretion vested in the trustee for all distributions |

| Beneficiary Identification | Full identification of the beneficiary including disability and government benefit programs |

| Trustee Designation | Initial trustee, successor trustees, and mechanism for trustee removal and replacement |

| Trust Protector Provisions | Optional designation of a trust protector to modify the trust for legal compliance |

| Distribution Guidelines | Guidance on approved expenditures and cautions about distributions affecting benefits |

| Spendthrift Clause | Prohibition on the beneficiary assigning or pledging their interest in the trust |

| Medicaid Payback Provision | Required for first-party trusts: state Medicaid reimbursement from remaining assets at death |

| Remainder Beneficiaries | Designation of who receives remaining assets after the beneficiary's death and Medicaid payback |

| Trustee Powers | Comprehensive list of trustee powers for investment, tax, and administrative decisions |

| Trustee Compensation | Whether and how the trustee is compensated for their services |

| Accounting Requirements | Frequency and scope of trust accountings provided to interested parties |

| Governing Law | Which state's law governs the trust's interpretation and administration |

| Irrevocability Statement | For first-party trusts, a statement that the trust cannot be revoked |

| Disability Certification | Documentation of the beneficiary's qualifying disability |

Approved Expenditures from a Special Needs Trust

Understanding what trust funds can and cannot be used for is essential for both the grantor and the trustee. Improper distributions can reduce or eliminate the beneficiary's government benefits.

No Impact on Benefits

- - Personal care attendants and companion services

- - Education, tutoring, and vocational training

- - Transportation (vehicle, modifications, transit)

- - Therapy (PT, OT, speech, recreational)

- - Electronics, computers, and assistive technology

- - Entertainment, hobbies, and vacations

- - Clothing and personal items

- - Furniture and household goods

- - Legal fees and guardianship costs

- - Pre-paid burial and funeral expenses

May Reduce SSI Benefits

- - Rent or mortgage payments (in-kind support)

- - Property taxes and homeowner's insurance

- - Utility payments (electric, gas, water)

- - Groceries and food purchases

- - Cash given directly to the beneficiary

Food and shelter payments are treated as "in-kind support and maintenance" (ISM) and can reduce SSI by up to 1/3 of the federal benefit rate plus $20. Sometimes paying for better housing is worth the SSI reduction.

The Cardinal Rule of Trust Distributions

Never give cash directly to the beneficiary. Direct cash payments are treated as unearned income and reduce SSI dollar-for-dollar. Instead, the trustee should pay vendors and service providers directly for goods and services the beneficiary needs. If the beneficiary needs spending money, the trustee can purchase prepaid debit cards loaded with specific amounts, though even this approach should be used cautiously and documented carefully.

Legal Requirements for Special Needs Trusts

Special needs trusts must comply with both federal requirements (set by the Social Security Administration and CMS/Medicaid) and state trust law. The requirements differ depending on whether the trust is a first-party or third-party trust.

Federal Statutory Authority

First-party special needs trusts are authorized under 42 U.S.C. Section 1396p(d)(4)(A), which exempts certain trusts containing the assets of a disabled individual from being counted as resources for Medicaid eligibility purposes. The trust must be established by a parent, grandparent, legal guardian, or the court (the beneficiary themselves can also establish the trust under the Special Needs Trust Fairness Act of 2016). The beneficiary must be under 65 at the time of establishment, must be disabled as defined by the Social Security Act, and the trust must contain a provision requiring that upon the beneficiary's death, the state Medicaid agency will be reimbursed for medical assistance paid on behalf of the beneficiary. Pooled trusts under Section 1396p(d)(4)(C) have different rules, including that the beneficiary's account may be retained by the nonprofit organization managing the pool.

Essential Elements for Compliance

- Supplemental Purpose Language: The trust must explicitly state that its purpose is to supplement, not replace, government benefits. Language like "the trustee shall not make any distribution that would reduce or eliminate the beneficiary's eligibility for any government benefit program" is essential.

- Sole Discretion of Trustee: The trustee must have sole and absolute discretion over distributions. If the beneficiary has any right to demand distributions, the trust assets will be treated as the beneficiary's countable resources.

- Spendthrift Provisions: The trust must prohibit the beneficiary from assigning, pledging, or otherwise transferring their interest in the trust. This protects trust assets from the beneficiary's creditors.

- Medicaid Payback (First-Party Only): First-party trusts must include a provision requiring that upon the beneficiary's death, remaining trust assets reimburse the state Medicaid program before passing to remainder beneficiaries.

- Disability Qualification: The beneficiary must meet the Social Security Administration's definition of disability. For first-party trusts, they must also be under age 65 at the time the trust is established.

- Proper Execution: The trust must be signed with the formalities required by your state's trust law, typically including notarization and witnesses. First-party trusts may require court approval depending on the beneficiary's capacity and the source of the funds.

Sample Special Needs Trust Document

Below is a condensed preview showing the structure and critical language of a special needs trust. Your completed document will be fully customized for your beneficiary's situation and your state's requirements.

SPECIAL NEEDS TRUST AGREEMENT

State of [State]

This Special Needs Trust Agreement ("Trust") is established on[Date] by[Grantor Name]("Grantor") for the benefit of[Beneficiary Name]("Beneficiary"), a person with disabilities as defined in 42 U.S.C. Section 1382c(a)(3).

ARTICLE I: PURPOSE

The purpose of this Trust is to provide supplemental and additional goods, services, and support for the Beneficiary beyond those provided by any local, state, or federal government benefit program. This Trust is intended to supplement, not supplant, impair, or diminish any government benefits or assistance for which the Beneficiary may be eligible. The Trustee shall not make any distribution that would reduce or eliminate the Beneficiary's eligibility for any government benefit program...

ARTICLE II: TRUSTEE

[Trustee Name] shall serve as the initial Trustee. If the initial Trustee is unable or unwilling to serve,[Successor Trustee]shall serve as successor Trustee. The Trustee shall have sole and absolute discretion over all distributions from the Trust...

ARTICLE III: DISTRIBUTIONS

The Trustee, in the Trustee's sole and absolute discretion, may distribute trust income and principal for the Beneficiary's supplemental needs, including but not limited to: personal care, education, recreation, transportation, technology, home modifications, dental and vision care, therapy, and any other goods or services that enhance the Beneficiary's quality of life and are not provided by government benefits...

ARTICLE IV: TERMINATION

Upon the death of the Beneficiary, the Trustee shall distribute remaining trust assets as follows: [For first-party trusts: first, to reimburse the State Medicaid program for all medical assistance paid on behalf of the Beneficiary; then] to[Remainder Beneficiary], or if not surviving, to[Contingent Beneficiary]...

Frequently Asked Questions

Find answers to common questions about special needs trusts, government benefits preservation, trustee responsibilities, and trust administration.

Official Resources

For additional information on special needs trusts, government benefits, and disability planning, consult these official and reputable sources.

SSA - Trusts and SSI

Social Security Administration guidance on how trusts affect SSI eligibility

Medicaid.gov

Official federal Medicaid resource with state-by-state program information

Special Needs Alliance

National organization of attorneys dedicated to special needs planning

ABLE National Resource Center

Comprehensive resource on ABLE accounts and their interaction with trusts

The Arc of the United States

National advocacy organization for people with intellectual and developmental disabilities

NAMI

National Alliance on Mental Illness resources for families and caregivers

Create your Special Needs Trust in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.