What Is an Executive Employment Contract?

An executive employment contract is a negotiated, individualized written agreement between a corporation and a senior officer — typically the CEO, CFO, COO, CTO, President, or Executive Vice President — that governs every dimension of the employment relationship, from base compensation and equity grants to termination triggers and post-employment restrictions. Unlike the at-will offer letters issued to most employees, an executive contract is a heavily-bargained instrument that allocates risk between the company, its board of directors, its compensation committee, and the executive. It is the single most important governance document for any senior leadership hire and is reviewed not just by counsel for both sides but, in publicly traded companies, by the compensation committee, outside compensation consultants, ISS and Glass Lewis advisors, and ultimately disclosed in the proxy statement.

The economic core of an executive contract is its compensation architecture. This typically includes a base salary set at or above the 50th percentile of a defined peer group, an annual cash bonus opportunity expressed as a target percentage of base salary (often 100% to 200% for a CEO), a long-term incentive award delivered as restricted stock units, performance share units, or stock options vesting over three to four years, sign-on cash and equity to make up for forfeited compensation at the prior employer, and ongoing perquisites such as supplemental retirement contributions, life insurance, executive medical coverage, financial planning, and personal use of corporate aircraft. Each of these elements has tax, accounting, and disclosure consequences that the contract must address with surgical precision.

Equally important — and often more heavily negotiated than compensation — is the contract's termination architecture. The agreement must define every possible separation scenario (termination for cause, termination without cause, resignation for good reason, voluntary resignation without good reason, death, disability, expiration of term, and termination in connection with a change in control) and specify the precise economic consequences of each. A well-drafted contract distinguishes between involuntary terminations that trigger severance, equity acceleration, COBRA subsidies, outplacement, and continued vesting, and voluntary terminations that result in forfeiture of unvested awards and no severance.

Federal tax law shapes nearly every provision. Section 409A of the Internal Revenue Code governs the timing of all deferred compensation, including severance, and imposes draconian penalties (immediate income inclusion, 20% additional federal tax, and an interest charge) for noncompliance. Section 280G and §4999 impose excise taxes on golden parachute payments that exceed three times the executive's five-year average compensation. Section 162(m) caps the corporate deduction for compensation paid to covered employees at $1 million per year. Each of these provisions must be addressed in the contract language and reflected in the operational design of the compensation program.

Whether you are a board chair negotiating with an incoming CEO, a private-equity sponsor onboarding a portfolio-company management team, a compensation committee chair refreshing a CFO contract, or a pre-IPO startup formalizing founder employment terms, our attorney-reviewed executive contract templates give you a defensible starting point. Each template is built around the leading-practice provisions expected by institutional shareholders, drafted to comply with §409A and §280G, and customizable for your jurisdiction's restrictive-covenant rules.

C-Suite Ready

Drafted for CEO, CFO, COO, CTO, President, and EVP-level appointments at public and private companies

Equity Architecture

Time-vesting RSUs, performance share units, stock options, and double-trigger change-in-control acceleration

§280G Compliant

Best-net cutback language, §409A separation timing, and clawback hooks under Dodd-Frank §954

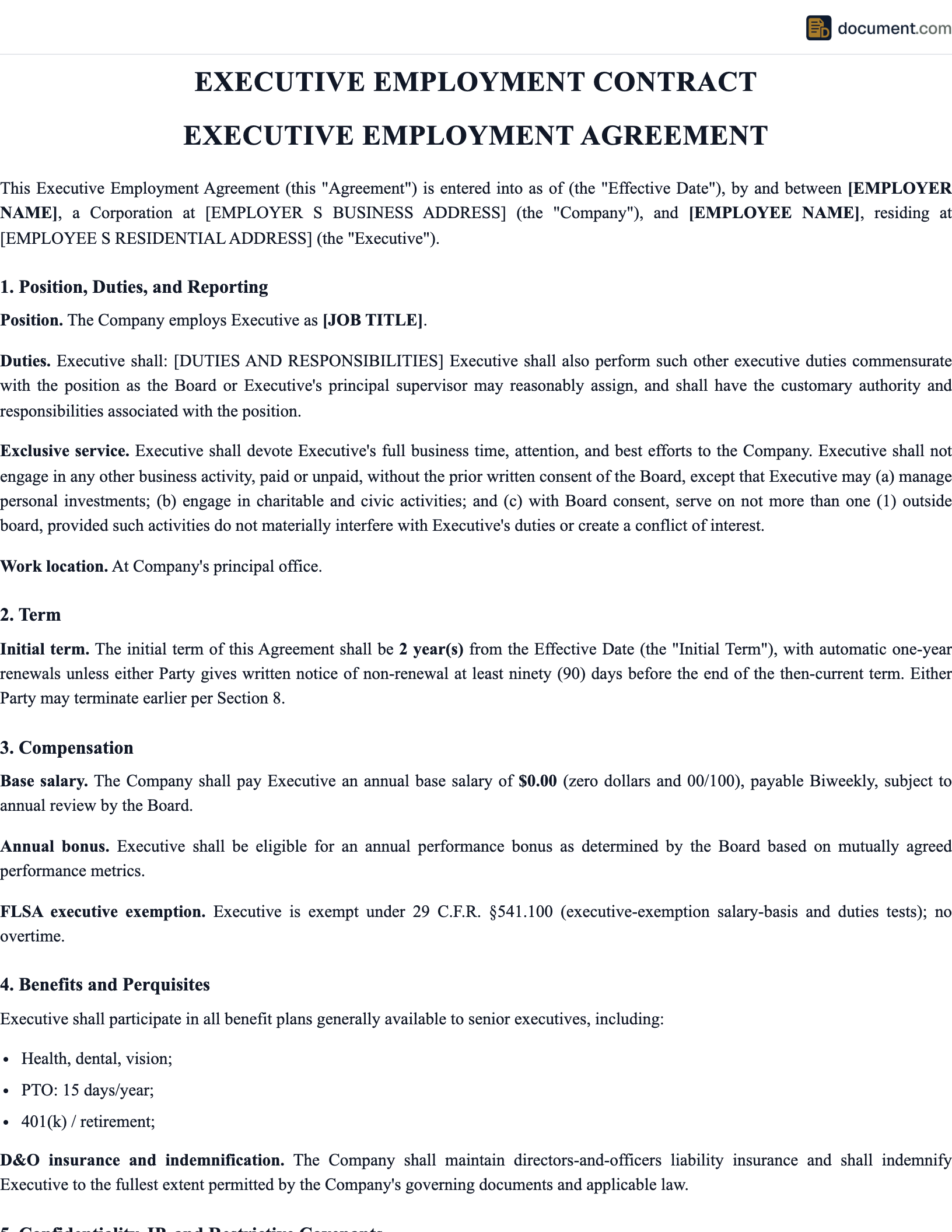

Executive Contract Form Preview

The mockup below illustrates the structure of a complete executive employment contract. Each section is fully customizable in our document builder, with pre-populated leading-practice language and optional clauses keyed to public-company versus private-company use cases.

Executive Employment Agreement

Chief Executive Officer

Section 1: Parties

Section 2: Compensation

Section 3: Severance Schedule

Section 4: Restrictive Covenants

Executive Roles Covered

Our executive employment contract templates are calibrated to the specific compensation structures, governance expectations, and risk profiles associated with each senior officer role. Select your position to begin with leading-practice provisions tailored to that seat.

Chief Executive Officer (CEO)

Top-level executive responsible for overall corporate strategy, P&L, and reporting to the board of directors

Chief Financial Officer (CFO)

Senior financial executive overseeing accounting, treasury, SEC reporting, and capital allocation

Chief Operating Officer (COO)

Executive responsible for day-to-day operations, supply chain, and execution of strategic initiatives

Chief Technology Officer (CTO)

Senior technology leader overseeing engineering, product architecture, and technical strategy

President

Senior corporate officer often serving as second-in-command or division head with P&L responsibility

Executive Vice President

Senior business unit leader with significant operational and strategic authority

Compensation Architecture

Executive compensation is built in layers. At the foundation sits base salary — the only fixed cash component and the reference point against which most other elements are sized. The compensation committee benchmarks base salary against a peer group of typically 12 to 20 companies of similar size, sector, and complexity, drawing from compensation consulting databases such as Equilar, FW Cook, Mercer, Aon Radford, and Willis Towers Watson. CEO base salaries at S&P 500 companies cluster between $1.0 million and $1.6 million, with CFO base typically 50 to 60 percent of CEO base.

The annual cash bonus sits atop base. It is expressed as a target percentage (commonly 100% to 200% of base for a CEO and 75% to 125% for a CFO) with a threshold (often 50% of target), target, and maximum (commonly 200% of target) tied to a scorecard of financial and strategic metrics — most often revenue growth, adjusted EBITDA, free cash flow, EPS, and individual or strategic milestones. The bonus plan must be documented separately from the contract for §162(m) and proxy disclosure purposes, but the contract should specify the target percentage, the metric framework, and treatment on termination.

Long-term incentive compensation typically dwarfs base and bonus combined. For an S&P 500 CEO, LTI commonly represents 60% to 75% of total target compensation. The contract must specify the annual grant date fair value, the mix of instruments (PSU, RSU, option), the vesting schedule (typically three or four years), the performance metrics for the PSU portion (relative TSR vs. an index, three-year cumulative EPS, ROIC), and treatment on termination.

| Component | Typical CEO Range | Tax Treatment |

|---|---|---|

| Base Salary | $1.0M - $1.6M | Ordinary income, FICA, withholding |

| Annual Bonus Target | 100-200% of base | Ordinary income on payment |

| RSU Grant | $2M - $5M annual | Ordinary income on vesting |

| PSU Grant | $4M - $10M annual | Ordinary income on payout |

| Stock Options | $1M - $3M annual GDFV | Ordinary income on exercise (NQSO) |

| Sign-On Cash | $1M - $5M (clawback) | Ordinary income on payment |

Equity & Vesting Provisions

Equity compensation is governed both by the executive contract and by the underlying equity plan document and individual award agreements. The contract should specify the grant date fair value of the annual award, the mix between time-vesting and performance-vesting, the standard vesting schedule (typically four years with 25% cliff or three years pro-rata), and the treatment on each separation scenario. Importantly, the contract should clarify that in the event of conflict between the contract and the award agreement, the more favorable provision controls — preventing the executive from being trapped by less favorable boilerplate in standard form awards.

Performance share units (PSUs) require careful drafting. The contract should specify the performance period (typically three years), the metrics (relative TSR is the most common, often paired with an internal financial metric), the payout curve (threshold of 25% to 50%, target of 100%, maximum of 200%), and the treatment on termination during the performance period. Best practice is pro-rata vesting based on actual performance through the end of the performance period for involuntary termination, full vesting on death or disability, and forfeiture on voluntary resignation.

Change-in-control treatment is the most heavily-negotiated equity provision. Modern best practice is double-trigger acceleration: equity vests in full only if the change in control is followed by a qualifying termination (without cause or for good reason) within a defined protection period (12 to 24 months). Single-trigger acceleration is strongly disfavored by ISS and Glass Lewis and should generally be avoided. The contract must specify how PSUs are treated — typically deemed earned at target (or actual performance through closing if measurable) and converted to time-vesting RSUs for the remainder of the performance period.

Golden Parachute & IRC §280G

Sections 280G and 4999 of the Internal Revenue Code impose a punitive tax regime on golden parachute payments. If the aggregate present value of all parachute payments to a disqualified individual (generally an officer, shareholder owning more than 1%, or highly compensated individual in the top 1% of employees) equals or exceeds three times the individual's base amount (the five-year average W-2 compensation), then the "excess parachute payment" — defined as the amount exceeding one times the base amount — is subject to a 20% nondeductible excise tax under §4999, and the company loses its corporate tax deduction for that excess amount under §280G.

The economic consequences are severe. An executive whose payments cross the 3x threshold by even one dollar can owe excise tax on millions of dollars of compensation. To address this, executive contracts typically use one of three approaches. First, the now-disfavored gross-up: the company pays the executive enough additional cash to make them whole on an after-tax basis. Gross-ups have largely been eliminated due to ISS opposition and shareholder pressure. Second, the "valley" or modified cutback (also called "best net"): payments are reduced to just below the safe harbor (typically 2.99 times the base amount) only if doing so leaves the executive better off on an after-tax basis than receiving the full payment subject to excise tax. Third, the hard cap: payments are reduced to the safe harbor regardless of after-tax outcome.

For private companies, §280G provides a shareholder-approval cleansing mechanism: if the parachute payments are approved by more than 75% of the disinterested shareholders after adequate disclosure, the §280G/§4999 tax does not apply. This is commonly used in private equity portfolio companies prior to a sale to allow management to receive their full transaction bonuses without §280G drag. Public companies cannot use the shareholder-approval exception.

§280G Mitigation Best Practice

Use a best-net cutback rather than a gross-up. Run a §280G analysis at the time of any transaction to confirm the calculation. For private-company sales, use the shareholder-approval exception under §280G(b)(5) where available. Avoid stacking accelerated equity, severance, and retention payments without modeling the parachute exposure.

How to Draft an Executive Employment Contract

Drafting a defensible executive contract is a structured process. Follow these eight steps to move from term sheet to executed agreement.

Negotiate the term sheet

Reach alignment on title, reporting line, base salary, target bonus, sign-on cash and equity, annual LTI, severance multiples, restrictive-covenant scope, and §280G treatment before drafting begins.

Confirm board and committee authority

Public-company contracts must be approved by the compensation committee. Private-equity portfolio companies require sponsor approval. Document the approving body and date.

Draft the compensation schedule

Spell out base, bonus target, LTI grant date fair value, perquisites, retirement contributions, and any one-time make-whole payments tied to forfeited compensation at the prior employer.

Build the termination matrix

For each separation type — cause, no cause, good reason, death, disability, change-in-control — specify cash severance, bonus treatment, equity treatment, COBRA, and outplacement.

Tailor restrictive covenants to state law

Confirm enforceability under the executive's state of residence and the company's principal place of business. California, Minnesota, North Dakota, and Oklahoma broadly bar non-competes.

Address §409A and §280G

Include separation-from-service language, six-month delay for specified employees, payment-timing provisions, and a §280G best-net cutback. Run a 280G model at signing if a transaction is foreseeable.

Add indemnification and D&O

Cross-reference any standalone indemnification agreement, confirm D&O coverage levels, and specify tail coverage on termination.

Execute and disclose

For public companies, file the contract as an Item 5.02 8-K and as an exhibit to the next 10-Q or 10-K. Update the proxy CD&A for the following year.

Key Components of an Executive Contract

Every executive contract should contain the following provisions. Each should be tailored to the company's governance structure, the executive's leverage, and applicable state law.

Position and Duties

Title, reporting line, board seat (if any), principal work location, expected travel, and standard of performance.

Term

Initial term, renewal mechanics (evergreen vs. fixed expiration), and notice period for non-renewal.

Base Salary

Initial amount, review cadence (typically annual by the compensation committee), and no-decrease provision.

Annual Bonus

Target percentage of base, performance metric framework, and treatment on mid-year termination.

Long-Term Incentives

Annual grant value, instrument mix, vesting schedule, and performance metrics for PSUs.

Sign-On Compensation

Cash bonus, RSU/PSU grant, make-whole payments, and clawback if terminated within 12-24 months.

Benefits and Perquisites

Health, dental, vision, 401(k), supplemental retirement, life insurance, disability, financial planning, executive medical.

Termination Provisions

Definitions of cause, good reason, change in control, disability, and the corresponding severance schedules.

Restrictive Covenants

Confidentiality, non-compete, non-solicitation of employees and customers, non-disparagement, and assignment of inventions.

Indemnification & D&O

Indemnification to the maximum extent permitted by law, D&O insurance coverage levels, and tail coverage.

Clawback

Dodd-Frank §954 / Rule 10D-1 mandatory clawback plus contractual clawback for misconduct.

§409A and §280G

Separation timing, six-month delay for specified employees, and best-net cutback for golden parachute exposure.

Termination & Severance Triggers

The termination matrix is the most consequential section of any executive contract. It defines which separation events trigger severance and which result in forfeiture. Each scenario should be addressed explicitly to eliminate ambiguity.

| Trigger | Cash Severance | Equity Treatment |

|---|---|---|

| Cause | None; accrued obligations only | Forfeit unvested; cancel vested options |

| Without Cause | 2x base + target bonus, 18 months COBRA | Pro-rata vesting; PSUs at actual performance |

| Good Reason | Same as without cause (notice + cure) | Same as without cause |

| Death | Pro-rata bonus; accrued obligations | Full vesting; PSUs at target |

| Disability | 6 months base continuation | Full vesting; PSUs at target |

| CIC + Qualifying Termination | 3x base + target bonus, 24 months COBRA | Full acceleration; PSUs at greater of target or actual |

| Voluntary Resignation | None; accrued obligations only | Forfeit unvested |

Restrictive Covenants

Restrictive covenants protect the company's confidential information, customer relationships, and workforce stability after the executive departs. The four standard covenants are confidentiality (perpetual for trade secrets, typically two to five years for other confidential information), non-competition (six months to two years post-termination, geographically limited to areas where the company actively does business), employee non-solicitation (typically twelve to twenty-four months), and customer non-solicitation (typically twelve to twenty-four months, limited to customers the executive interacted with during the final year of employment).

Enforceability varies dramatically by jurisdiction. California (Cal. Bus. & Prof. Code §16600), North Dakota, Oklahoma, and Minnesota broadly refuse to enforce non-competes against employees, with limited exceptions. Several other states (Washington, Illinois, Massachusetts, Maine, Maryland, Virginia, Colorado, and Oregon) have enacted statutory wage thresholds, notice requirements, and garden-leave rules that significantly constrain non-compete enforcement. The contract should be drafted to comply with the law of the executive's state of residence and principal work location.

Even in restrictive states, courts generally enforce well-drafted confidentiality and customer non-solicit provisions, particularly when supported by the executive's access to trade secrets, customer lists, pricing information, and strategic plans. The contract should also include a "blue pencil" provision allowing courts to reform overbroad restrictions to the maximum enforceable scope and a survival clause confirming that restrictive covenants survive termination.

Sample Executive Employment Contract

Below is a condensed excerpt from our executive employment contract template showing the key provisions. The full template runs approximately 30 to 45 pages depending on selected options.

EXECUTIVE EMPLOYMENT AGREEMENT

Chief Executive Officer

This Executive Employment Agreement (this "Agreement") is entered into as of [Effective Date] by and between [Company Name], a [State] corporation (the "Company"), and [Executive Name](the "Executive").

1. EMPLOYMENT AND DUTIES

The Company hereby employs the Executive as Chief Executive Officer of the Company, reporting directly to the Board of Directors. The Executive shall have the duties, responsibilities, and authority customarily associated with this position and such other duties as the Board may reasonably assign. The Executive shall devote substantially all business time and attention to the affairs of the Company.

2. TERM

The initial term of this Agreement shall commence on the Effective Date and continue for a period of three (3) years, unless earlier terminated in accordance with Section 6. Upon expiration of the initial term, this Agreement shall automatically renew for successive one-year periods unless either party provides written notice of non-renewal at least ninety (90) days prior to the end of the then-current term.

3. COMPENSATION

(a) Base Salary. The Company shall pay the Executive an initial annual base salary of $[Amount], payable in accordance with the Company's standard payroll practices. The Compensation Committee shall review the base salary annually and may increase (but not decrease) it.

(b) Annual Bonus. The Executive shall be eligible to earn an annual cash bonus with a target of [%] of base salary, based on achievement of performance objectives established by the Compensation Committee.

(c) Long-Term Incentives. The Executive shall receive an annual long-term incentive award with a grant date fair value of approximately $[Amount], allocated 60% to performance share units, 30% to restricted stock units, and 10% to stock options.

6. TERMINATION

(a) By the Company for Cause.The Company may terminate the Executive's employment for Cause upon a determination by a majority of the Board after written notice and an opportunity for the Executive to be heard with counsel.

(b) By the Company without Cause or by the Executive for Good Reason. Upon such termination, the Executive shall be entitled to (i) two times the sum of base salary and target annual bonus, paid in a lump sum on the 60th day following separation, (ii) eighteen months of COBRA premium reimbursement, and (iii) pro-rata vesting of outstanding equity awards as set forth in the applicable award agreements.

9. SECTION 280G

If any payment or benefit received by the Executive in connection with a change in control would constitute a "parachute payment" under Section 280G of the Code and would be subject to the excise tax under Section 4999, the payments shall be reduced to the largest amount that would not result in any portion being subject to the excise tax, but only if such reduction would result in the Executive receiving a greater after-tax amount than receiving the full payment.

Frequently Asked Questions

Answers to common questions about executive employment contracts, equity compensation, golden parachutes, and §409A.

Official Resources

Authoritative federal and professional resources for executive compensation, securities law, and tax compliance.

SEC - Executive Compensation Disclosure

Compliance and Disclosure Interpretations on executive comp disclosure under Reg S-K Item 402

IRS - Section 409A Guidance

Internal Revenue Service guidance on nonqualified deferred compensation

IRS - §280G Audit Technique Guide

Golden parachute audit guide for IRC §280G and §4999 excise tax

DOL - Employee Benefits Security Administration

ERISA, executive benefit plans, and fiduciary guidance

SEC - Rule 10D-1 Clawback Final Rule

Dodd-Frank Section 954 mandatory clawback final rule

ABA - Business Law Section

American Bar Association corporate governance and executive compensation resources

NACD - National Association of Corporate Directors

Director education on executive compensation governance

Harvard Law - Corporate Governance Forum

Leading academic resource on executive compensation and governance

Create your Executive Employment Contract in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.