What Is a Payment Demand Letter?

A payment demand letter is a formal written notice from a creditor to a debtor demanding payment of a specific sum of money by a specific deadline. Unlike a routine reminder or past-due notice, a demand letter explicitly invokes legal consequences — usually a lawsuit, referral to a collection agency, or reporting to a credit bureau — if the debtor fails to pay within the cure period. It is the bridge between informal collection efforts and formal litigation, and in most cases it is the single most effective collection tool a creditor has.

The letter identifies the parties, references the underlying contract or invoice, itemizes the principal balance, adds any contractual interest, late fees, returned-check penalties, and collection costs, states a hard payment deadline (typically 10 to 30 days), and warns of the consequences of nonpayment. When sent by certified mail with return receipt requested, it also creates a paper trail that becomes evidence if you later have to sue — proof that the debtor was on notice of the debt and chose not to pay.

Most U.S. jurisdictions do not require a demand letter as a precondition to filing a breach-of-contract or collection action, but a few specific statutes do. Nearly every state requires written demand and a 30-day cure period before a creditor can recover statutory penalties on a bounced (NSF) check, often two or three times the face amount. Many commercial contracts also include a notice-and-cure clause as a condition precedent to suit. And even where no statute requires it, judges and small claims clerks consistently view a documented demand letter as evidence of good faith and reasonable behavior.

Recover Money Owed

Demand the principal balance plus interest, fees, and collection costs

Create a Paper Trail

Certified-mail proof of notice becomes evidence in a future lawsuit

Avoid Litigation Costs

Most debts settle after a well-drafted demand without filing suit

When to Send a Payment Demand Letter

Timing matters. Send the demand after you have already made one or two routine collection contacts — a polite past-due email, a follow-up phone call — and the debtor has not responded or has missed a promised payment date. Sending a demand too early can damage an otherwise salvageable customer relationship; sending it too late risks running into the statute of limitations.

- 30 to 60 days past due on a commercial invoice with no response to reminders

- A check has bounced for insufficient funds — required by NSF statutes in nearly every state

- A personal loan has gone unpaid past the due date in the promissory note

- Before filing a small claims action — even where not required, judges view it favorably

- Before referring an account to a collection agency or selling the debt to a debt buyer

- Well before the statute of limitations expires on a written or oral contract claim

Types of Payment Demand Letters

Different debt scenarios call for different language and different legal hooks. Choose the variant that matches the underlying transaction so the letter cites the correct contract terms, statutes, and remedies.

Unpaid Invoice

Recover money owed under a delivered invoice past its due date

Breach of Contract Debt

Demand payment for goods or services delivered under a written or oral contract

Personal Loan

Recover money lent to a friend, family member, or acquaintance

Bounced Check (NSF)

Demand payment plus statutory penalties for a returned check

Account Receivable

Commercial collection demand sent before turning the account over to a collection agency

Unpaid Rent (Commercial)

Demand past-due rent under a commercial lease before unlawful detainer

Demand Letter vs Other Collection Options

A demand letter is one tool in a creditor's collection toolkit. Understanding how it compares to the alternatives helps you choose the right approach for your situation and the size of the debt.

Demand Letter vs Past-Due Reminder

Past-Due Reminder

- - Friendly tone, customer-relationship preserving

- - No legal threats

- - Sent by email or first-class mail

- - Routine accounts receivable workflow

- - 1-3 reminders before escalation

Demand Letter

- - Formal, legalistic tone

- - Explicit threat of suit or collection

- - Sent by certified mail, return receipt

- - Final pre-litigation step

- - One letter, hard deadline, then action

Demand Letter vs Collection Agency Referral

Self-Sent Demand Letter

- - Free or low cost

- - Creditor keeps 100% of recovery

- - FDCPA does not apply (original creditor)

- - Best for amounts under $10,000

- - Preserves customer relationship if cured

Collection Agency

- - Agency keeps 25% to 50% of recovery

- - Reports to credit bureaus on creditor's behalf

- - FDCPA strictly applies

- - Better for large or aging portfolios

- - Permanently damages relationship

Demand Letter vs Filing Suit

Demand Letter

- - Costs roughly the price of a stamp

- - Resolves 60-70% of valid debts

- - No filing fee, no court appearance

- - Preserves litigation as a future option

Lawsuit

- - Filing fees of $30 to $400+ depending on court

- - Months to a year to a judgment

- - Judgment still must be enforced/collected

- - Required for amounts over small claims limits

How to Write and Send a Payment Demand Letter

An effective demand letter is short, factual, and unambiguous. It does not threaten anything you are unwilling to do, it does not insult or harass the debtor, and it does not bluff. Follow these eight steps to draft and send a letter that maximizes your chances of getting paid.

Gather Your Documentation

Before drafting, collect every document supporting the debt: the original contract, invoice(s), purchase order, delivery confirmations, prior correspondence, payment history, and any partial payments. The letter must be factually airtight — every dollar you demand should trace back to a document in your file.

Calculate the Exact Amount Owed

Itemize the principal balance, contractual interest at the rate stated in your agreement (or statutory prejudgment interest if no rate exists), late fees, returned-check penalties under your state's NSF statute, and any collection costs authorized by contract. Show your math so the debtor and a future judge can verify each line.

Identify the Correct Recipient

Send the letter to the legal entity that owes the debt — the corporation, LLC, or individual named on the contract or invoice — at the address on file or the entity's registered agent for service of process. If the debtor is a corporation, look up the registered agent on the Secretary of State's business search portal.

Draft the Letter

Use a clear, professional, formal tone. Open with the parties and the debt. Reference the contract or invoice by date and number. Itemize the amounts. State a specific deadline (a date, not just 'within 14 days'). State the consequences of nonpayment specifically and credibly. Close with payment instructions and contact information.

Cite the Right Authority

If your contract has an interest, late-fee, or attorney's fees clause, quote it. If you are demanding NSF check penalties, cite your state's bad-check statute by section number. If the debtor is a business, reference the underlying purchase order or work order. Specificity signals competence and increases settlement leverage.

Set a Hard Deadline

Give 10, 14, or 30 days from the date of the letter, calendared to a specific date. Ten days is aggressive and signals urgency. Fourteen is standard. Thirty is appropriate when state law requires a longer cure period or when the debtor is a large institution that needs internal processing time.

Send by Certified Mail with Return Receipt

USPS Certified Mail with Return Receipt Requested (PS Form 3811, the green card) is the gold standard. It costs about $8 and produces a signed delivery receipt admissible as evidence. Send a courtesy copy by first-class mail and email so the debtor cannot claim they refused certified mail to avoid notice.

Calendar the Deadline and Follow Through

On the deadline date, check whether payment was received. If yes, send a written acknowledgment and release. If no, follow through on exactly what you said you would do — file the small claims action, refer the account to a collection agency, or escalate to an attorney. Empty threats destroy your credibility for every future demand.

Key Components of a Payment Demand Letter

Every effective payment demand letter contains the same core elements. Missing any one of them weakens the letter and may give the debtor an excuse to delay or dispute.

Sender and Recipient Information

Full legal names, mailing addresses, and contact information for both the creditor and the debtor

Reference to the Underlying Debt

Contract date and number, invoice number, account number, or promissory note date

Itemized Amount Owed

Principal, interest, late fees, NSF penalties, collection costs — broken out and totaled

Specific Payment Deadline

An actual calendar date, typically 10 to 30 days from the letter date

Statement of Consequences

Specific, credible consequences of nonpayment — suit, agency referral, credit reporting

Payment Instructions

Where, how, and to whom payment should be sent — check, wire, ACH, or online

Reservation of Rights

Language preserving all legal rights and remedies if the debt is not cured by the deadline

Signature and Date

Original signature of the creditor or authorized representative, dated the day mailed

Interest, Fees, and Damages You Can Demand

A common mistake creditors make is demanding only the unpaid principal. Depending on your contract and state law, you may be entitled to substantially more — and demanding the full amount you are legally owed often creates settlement leverage.

Contractual Interest

If your contract or invoice terms specify an interest rate on past-due balances (e.g., "1.5% per month on amounts over 30 days past due"), demand that rate. Quote the exact contract language. Most jurisdictions enforce contractual interest up to the state usury cap.

Statutory Prejudgment Interest

If no contractual rate exists, every state provides a default statutory prejudgment interest rate, commonly between 4% and 10% per year. California is currently 10% (Civ. Code § 3289), New York is 9% (CPLR § 5004), Texas is the prime rate plus 5% with a floor of 5% and a ceiling of 15%. Check your state.

NSF (Bounced Check) Penalties

If the debt arose from a returned check, nearly every state allows the holder to recover the face amount of the check plus a statutory penalty — often two or three times the check amount, capped at $500 to $1,500. Most states require a written demand and 30-day cure period as a precondition to recovering the penalty.

Late Fees

If the contract authorizes a flat late fee (e.g., "$25 per month") or a percentage fee, demand it. Courts generally enforce reasonable late fees but may strike down fees that function as a penalty rather than liquidated damages.

Attorney's Fees and Collection Costs

The American Rule presumes each side pays its own legal fees. The exceptions: (1) a fee-shifting clause in the contract, (2) a fee-shifting statute (consumer protection, wage claims, certain housing matters), or (3) bad-faith conduct by the opposing party. If your contract has a prevailing-party attorney's fees clause, quote it in the demand.

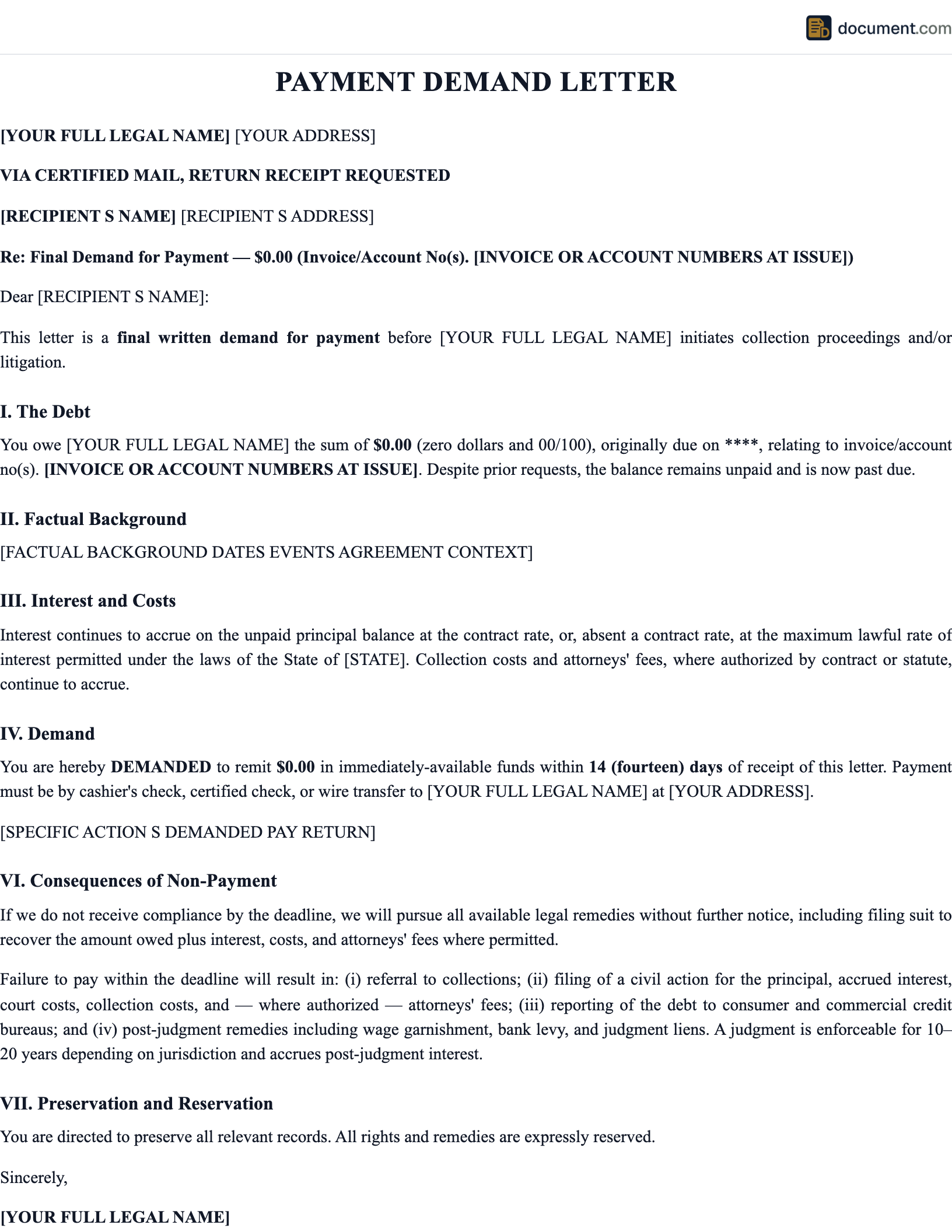

Sample Payment Demand Letter

Below is a condensed preview of our payment demand letter template. Your completed letter will be fully customized for your debt type, state law, and the specific contractual terms between you and the debtor.

[Sender Name]

[Sender Address]

[City, State ZIP]

[Date]

VIA CERTIFIED MAIL — RETURN RECEIPT REQUESTED

[Debtor Name]

[Debtor Address]

[City, State ZIP]

Re: Demand for Payment — Invoice No. [____], Amount Due: $[____]

Dear [Debtor Name]:

This letter is a formal demand for payment of the past-due balance you owe to [Sender Name] in the amount of $[Total], arising from Invoice No. [____] dated [____], for [goods/services] delivered on [____]. The invoice was due on [____] and remains unpaid as of the date of this letter.

ITEMIZATION OF AMOUNT OWED:

Principal balance: $[____]

Contractual interest at [__]% per [month/year] from [date]: $[____]

Late fees pursuant to Section [__] of the agreement: $[____]

Returned-check penalty pursuant to [State Statute §___]: $[____]

TOTAL DUE: $[____]

You are hereby notified that you have [14] days from the date of this letter — that is, no later than [Deadline Date] — to remit payment in full to the address listed above. Payment may be made by [check, wire, ACH, or online portal at ____].

If payment is not received by [Deadline Date], I will pursue all available legal remedies, which may include filing a lawsuit in [Court Name], referral of this account to a collection agency, and recovery of all collection costs and attorney's fees as authorized by Section [__] of our agreement. Nothing in this letter shall be construed as a waiver of any rights or remedies available under law or contract, all of which are expressly reserved.

Sincerely,

[Signature]

[Printed Name]

[Title]

Frequently Asked Questions

Official Resources

CFPB - Debt Collection

Consumer Financial Protection Bureau guidance on debt collection rights and rules

FTC - Fair Debt Collection Practices Act

Full text of the federal FDCPA and enforcement guidance

USPS - Certified Mail

Instructions for sending certified mail with return receipt requested

U.S. Courts - Forms

Federal court forms including civil cover sheets and complaints

SBA - Manage Business Finances

Small Business Administration resources on collections and accounts receivable

ABA - Business Law Section

American Bar Association resources on commercial collections

Create your Payment Demand Letter in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.