What Is a Debt Collector Cease and Desist Letter?

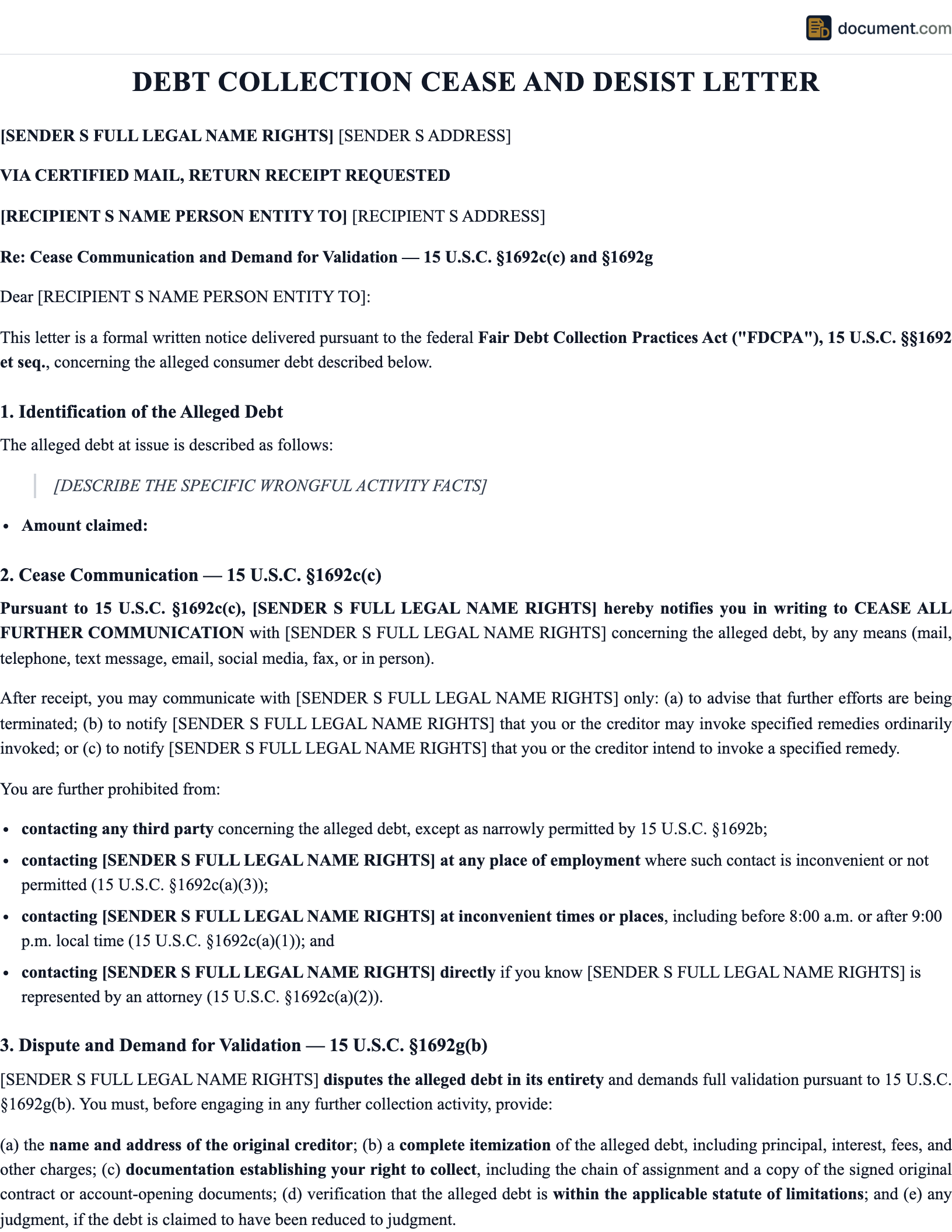

A debt collector cease and desist letter is a written notification sent to a third-party debt collector that legally requires them, under federal law, to stop contacting you about a debt. Unlike most cease and desist letters, which have no direct legal force, this one does. Section 805(c) of the Fair Debt Collection Practices Act (FDCPA), codified at 15 U.S.C. § 1692c(c), requires a debt collector to cease all further communication with a consumer after receiving written notice that the consumer refuses to pay the debt or wants the collector to stop communicating.

The FDCPA was enacted in 1977 to eliminate abusive, deceptive, and unfair debt collection practices. It applies only to third-party debt collectors — collection agencies, debt buyers (who buy old debt portfolios for pennies on the dollar), and attorneys who regularly collect debts for others. It does not generally apply to original creditors collecting their own debts, though many states have parallel laws that do. The statute covers only consumer debts — debts incurred primarily for personal, family, or household purposes. Business debts fall outside the FDCPA.

Once the collector receives your written cease and desist letter, they are legally permitted only three kinds of follow-up contact: to acknowledge receipt of the letter; to tell you they are ceasing collection efforts; or to inform you of a specific remedy they intend to invoke, such as filing a lawsuit. Any other contact — phone calls, letters, texts, emails, or contact with third parties — is a violation that gives you a private right of action under 15 U.S.C. § 1692k for actual damages, statutory damages up to $1,000, and reasonable attorney fees and costs.

Important caveat: a cease and desist letter stops communication, but it does noteliminate the underlying debt. The creditor or collector retains the legal right to sue you. In some cases, sending a cease and desist letter actually pushes the collector to file suit sooner because informal collection is no longer an option. If you have any ability to pay or to negotiate a settlement, consider whether a debt validation letter under 15 U.S.C. § 1692g, or a negotiated settlement, might better serve your interests before you invoke the cease and desist right.

Stops Contact

Legally required under 15 U.S.C. § 1692c(c) once the collector receives the letter

$1,000 Statutory Damages

If they violate the FDCPA, you can recover statutory damages plus attorney fees

Workplace Protection

Ends calls to your workplace and contact with third parties

Form Preview

FDCPA Cease and Desist Notice

Pursuant to 15 U.S.C. § 1692c(c)

Section 1: Consumer Information

Section 2: Collector Information

Section 3: Cease and Desist Demand

Pursuant to 15 U.S.C. § 1692c(c), you are hereby notified to CEASE all further communication with me regarding the above-referenced account. This includes phone calls, letters, text messages, emails, and contact with any third parties...

Types of Debt Collection Letters

Credit Card Debt

Collection activity on credit card balances by original creditors or third-party collectors

Medical Debt

Collection on hospital bills, doctor invoices, or other medical expenses

Student Loan Debt

Private student loan collection; note FDCPA limits for federal loans

Zombie Debt

Old debts beyond the statute of limitations that collectors try to revive

Debt Not Owed

Letters disputing debts that are not yours or have already been paid

Time-Barred Debt

Debts past the statute of limitations where legal collection is barred

Harassing Calls

Letters demanding that phone harassment and repeated calls stop

Workplace Contact

Stopping collectors from contacting you at your job or workplace

Your Rights Under the FDCPA

The FDCPA gives consumers powerful protections against abusive collection practices. Even before sending a cease and desist letter, you have the right to:

No contact before 8 a.m. or after 9 p.m.

Under § 1692c(a)(1), collectors cannot call at inconvenient hours.

No calls to your workplace

Under § 1692c(a)(3), once a collector knows your employer prohibits personal calls.

No harassment or abuse

Section 1692d prohibits threats, obscene language, and repeated calls intended to annoy.

No false or misleading representations

Section 1692e prohibits false claims about the debt, the consequences, or the collector's identity.

No unfair practices

Section 1692f prohibits collecting amounts not authorized and other unfair conduct.

Right to validation

Section 1692g gives you 30 days to demand validation of the debt.

Right to stop communication

Section 1692c(c) gives you the right to send a cease and desist letter.

Right to sue

Section 1692k gives you a private right of action with statutory damages and attorney fees.

Effect of the Letter on Your Debt

| What Happens | Yes | No |

|---|---|---|

| Collector must stop calling | Yes | — |

| Debt is erased | — | No |

| Collector may still sue | Yes | — |

| Credit report changes | — | No |

| Statute of limitations changes | — | No |

| Third-party contact must stop | Yes | — |

How to Draft the Letter

Step 1: Confirm FDCPA coverage

Verify that the entity is a third-party debt collector and the debt is a consumer debt.

Step 2: Identify the account

Use the reference number the collector provides — never your full Social Security number.

Step 3: State the cease and desist demand

Explicitly invoke 15 U.S.C. § 1692c(c) and demand all communication stop.

Step 4: Reserve your rights

State that you dispute the debt and preserve all legal defenses.

Step 5: Sign and date

Keep a signed copy for your records.

Step 6: Send by certified mail, return receipt

The green card is your proof of receipt and starts the legal clock.

Key Components

Consumer name and mailing address

Your full legal name; no SSN required or recommended

Account reference

The collector's file or account number from their prior letter

Collector name and address

The name and mailing address on the most recent collection letter

Statutory citation

Explicit reference to 15 U.S.C. § 1692c(c)

Cease-communication demand

Clear instruction to stop all contact with you, your family, and your employer

Dispute of debt

Statement that you dispute the debt and reserve all defenses

Warning of FDCPA liability

Notice that continued contact will expose the collector to damages

Signature and date

Your signature and the date mailed

Debt Validation Letters

Before (or instead of) sending a cease and desist letter, consider sending a debt validation letter under 15 U.S.C. § 1692g. Within thirty days of the collector's first contact, you can demand written proof of the debt. Until the collector provides validation — typically an itemized accounting and a copy of the original agreement or account statement — they must suspend collection activity. Many debt buyers cannot produce adequate documentation, and the debt is written off. A validation letter preserves your ability to negotiate, dispute, or settle, while a cease and desist letter ends communication entirely.

FDCPA Damages Under 15 U.S.C. § 1692k

Actual damages

Out-of-pocket losses, emotional distress, lost wages, and related harms caused by the collector's violation.

Statutory damages up to $1,000

Awarded per lawsuit regardless of actual damages, at the court's discretion.

Class action damages

Up to $500,000 or 1% of the collector's net worth, whichever is less.

Attorney fees and costs

Reasonable attorney fees and costs are awarded to successful plaintiffs, which is why many consumer rights attorneys take FDCPA cases on contingency.

Risks and Warnings

Litigation risk increases

A collector who can no longer call or write may decide to sue instead.

The debt remains

Your credit report, statute of limitations, and underlying obligation do not change.

Do not acknowledge old debt

For time-barred debt, avoid statements that could be construed as acknowledging the debt or agreeing to pay, as this can restart the statute of limitations in many states.

FDCPA only covers third-party collectors

Original creditors are not generally covered. Check your state law for additional protections.

Sample Letter

VIA CERTIFIED MAIL — RETURN RECEIPT REQUESTED

April 7, 2026

Aegis Portfolio Recovery LLC

Attn: Compliance Department

1900 Corporate Blvd

Boca Raton, FL 33431

Re: File No. APR-881-22094 — Notice to Cease Communication Pursuant to 15 U.S.C. § 1692c(c)

To Whom It May Concern,

This letter serves as formal written notice pursuant to Section 805(c) of the Fair Debt Collection Practices Act, 15 U.S.C. § 1692c(c), that I hereby demand you CEASE ALL COMMUNICATION with me regarding the above-referenced account.

From the date you receive this letter, you are permitted only the limited communications expressly allowed by 15 U.S.C. § 1692c(c): to advise that further collection efforts are being terminated, or to notify me that you intend to invoke a specific remedy. You are prohibited from making any further contact with me by telephone, letter, text message, email, or any other means, and from contacting my employer, family, friends, or any other third party regarding this alleged debt.

I additionally dispute this debt in full. All of my legal rights and defenses are expressly reserved.

Be advised that any violation of the FDCPA will subject your agency to civil liability under 15 U.S.C. § 1692k, including actual damages, statutory damages up to $1,000, and reasonable attorney fees and costs. I will not hesitate to pursue those remedies.

Govern yourselves accordingly.

Sincerely,

Priscilla D. Fontaine

Frequently Asked Questions

Official Resources

CFPB - Debt Collection

Consumer Financial Protection Bureau guidance on your rights and how to complain

FTC - FDCPA Full Text

Federal Trade Commission copy of the Fair Debt Collection Practices Act

CFPB - Regulation F

Current regulation implementing the FDCPA, effective November 2021

CFPB Complaint Portal

File a complaint against a debt collector directly with the CFPB

FTC - Full FDCPA Text

Complete federal statute with amendments

NACA - Consumer Advocates

National Association of Consumer Advocates - find an FDCPA attorney

Nolo - Debt Collection Guide

Plain-English guide to your rights against debt collectors

USA.gov - Debt Collection

Federal government consumer guide to debt collection

Create your Debt Collection Cease and Desist Letter in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.