What Is a Debt Validation Letter?

A debt validation letter is a written request sent to a third-party debt collector demanding that the collector prove the debt is yours, that the collector is authorized to collect it, and that the amount being claimed is accurate. The right to demand validation comes from section 809 of the federal Fair Debt Collection Practices Act (FDCPA), one of the strongest consumer protection laws on the books. Sending a validation letter is the single most effective first step a consumer can take when contacted by a debt collector — particularly for older debts, debts that have been resold, or debts that may not even be theirs.

When a debt collector first contacts you, they are required by the FDCPA to send a written notice (called the "initial communication" or "G-notice") that informs you of the debt and your right to dispute it within 30 days. If you send a written validation request within that 30-day window, the collector must stop all collection activity and cannot call, write, or sue you again until it provides written validation of the debt. This temporary pause is one of the most powerful protections in the FDCPA, and it gives you breathing room to investigate the debt, gather your records, and decide how to respond.

Many debt collectors — especially debt buyers who purchase old portfolios for pennies on the dollar — are unable to provide proper validation because they simply do not have the underlying records. The original creditor may have lost the contract, the account may have been sold and resold multiple times, and the chain of assignment may be broken. When a collector cannot validate, the FDCPA prohibits it from continuing collection activity, and credit reporting of the unverified debt becomes a potential FDCPA and FCRA violation. In many cases, a single validation letter is enough to make a collector go away entirely.

Even when the debt is real and you remember it, sending a validation letter is still worthwhile. The collector may have inflated the balance with unauthorized fees and interest, the statute of limitations may have expired, or the debt may have been reported to the credit bureaus inaccurately. A validation letter forces the collector to put its case in writing, which gives you leverage to negotiate a settlement, demand pay-for-delete terms, or challenge the debt in court if it ever comes to that.

Our attorney-reviewed debt validation letter templates include all of the language required by the FDCPA and the CFPB's Regulation F, request the specific documentation courts have required collectors to produce, and put the collector on notice that any further collection activity without validation is a federal violation. Whether you are responding to your first collection letter, dealing with a zombie debt, or pushing back on a collector you believe is acting illegally, our templates give you a strong starting point that costs nothing and takes only minutes to complete.

FDCPA Power

Federal law forces the collector to prove the debt

Pauses Collection

Stops all calls and letters until validation arrives

Often Ends Collection

Many collectors cannot produce the documentation

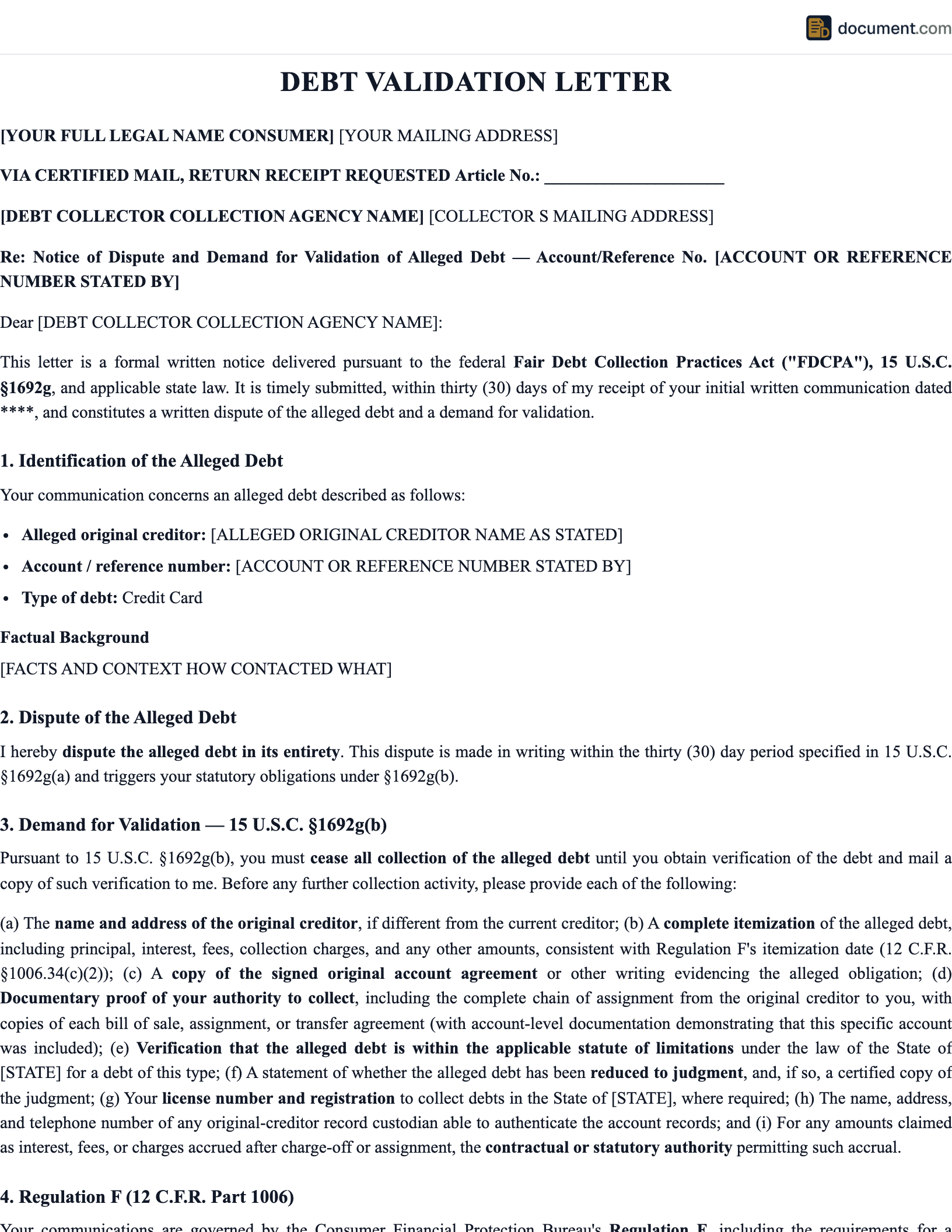

Form Preview

Our validation letter is a single-page document that includes the FDCPA citation, a list of the documentation you are demanding, and a clear notice that any continued collection activity without validation is a federal violation.

[Your Name & Address]

[Date]

[Collection Agency Name and Address]

RE: Debt Validation Request — Account No. _______

This letter is sent under section 809 of the FDCPA...

I dispute this debt and request validation, including:

- Original creditor name & address

- Itemized accounting of the debt

- Proof of your authority to collect

- Date of last payment / first delinquency

Sincerely, [Signature]

Types of Debt Validation Letters

Different situations call for different versions of a validation letter. Below are the most common types of letters consumers send to debt collectors.

Validation vs Verification vs Dispute

Consumers often confuse three different but related letters. Knowing which to use is the difference between protecting yourself and wasting time.

| Feature | Validation (FDCPA) | Verification (FCRA) | Original Creditor Dispute |

|---|---|---|---|

| Sent To | Debt collector | Credit bureau | Original creditor |

| Governing Law | FDCPA § 809 | FCRA § 611 | FCRA § 623 |

| Deadline to Send | 30 days from G-notice | Anytime | Anytime |

| Pauses Collection | Yes | No | No |

| Best For | Stopping collectors | Removing inaccurate items | Direct creditor errors |

How to Write a Debt Validation Letter

A strong validation letter is short, formal, and tightly tied to the language of the FDCPA. Here is the step-by-step process.

Confirm the 30-Day Window

Find the first written notice you received from the collector and check the date. You have 30 days from receipt to send a validation request that triggers the FDCPA pause.

Identify the Collector

Use the collector's full legal name, address, and any reference number from the original notice. Avoid sending the letter to a generic call center address.

State the Dispute Clearly

Open with a clear statement that you dispute the debt and request validation under section 809 of the FDCPA.

List the Required Documentation

Demand the original creditor's name and address, the itemized amount, the date of first delinquency, the chain of assignment, and a copy of the original signed agreement.

Add a Cease Communication Demand (Optional)

If the collector has been calling at unreasonable hours or contacting your workplace, include a demand to cease all communication except through the mail.

Sign and Mail by Certified Mail

Sign the letter, keep a copy, and send it via USPS certified mail with return receipt requested. Save the receipt and tracking number.

Wait for the Response

Until the collector provides validation in writing, it cannot continue collection activity. If it does, document every contact for a future FDCPA claim.

Key Components of a Validation Letter

Every effective validation letter includes the same core elements that meet the FDCPA requirements and put the collector on notice of your demands.

- Personal Identification: Your name and current address — never send your full SSN to a collector

- Account Reference: Any reference number from the collector's original letter

- Dispute Statement: A clear, unambiguous statement that you dispute the debt

- Validation Request: Specific list of documents and information you require

- FDCPA Citation: Reference to section 809 and the statutory pause on collection

- Optional Cease Demand: Request that the collector limit communication to writing

- Signature: Handwritten signature and printed name

Your Rights Under the FDCPA

The FDCPA gives consumers an extensive list of protections against abusive third-party debt collection. Understanding these rights helps you use a validation letter as part of a broader strategy for dealing with collectors.

Regulation F (CFPB)

In November 2021 the CFPB's Regulation F took effect, modernizing the FDCPA for the digital age. Regulation F caps phone calls at seven per week per debt, requires a detailed validation notice with itemization, and creates new rules for email and text message communication. Our templates incorporate Regulation F requirements where applicable.

- Right to Validation: Force the collector to prove the debt is real and accurate.

- Right to Cease Communication: Demand that the collector stop contacting you.

- Time Restrictions: Collectors cannot call before 8 a.m. or after 9 p.m. local time.

- Workplace Restrictions: Collectors cannot call your workplace if you tell them not to.

- No Harassment: Collectors cannot use threats, profanity, or repeated calls to annoy you.

- Right to Sue: $1,000 statutory damages plus actual damages and attorney's fees for FDCPA violations.

What Happens After You Send the Letter

Once the collector receives your validation letter, several things can happen. Knowing what to expect helps you respond effectively at each stage.

Collection Activity Stops

If you sent the letter within the 30-day window, the collector must immediately stop all collection activity until it provides written validation.

Collector Investigates

The collector contacts the original creditor or the debt seller and tries to gather the required documentation.

Validation or Silence

Many collectors are unable to validate and simply close the file. Others mail back partial documentation that does not meet the FDCPA standard.

You Evaluate the Response

If validation is received, decide whether to negotiate a settlement, dispute further, or pay. If validation is incomplete, send a re-validation request.

Escalation if Needed

If the collector continues collection without validation, file CFPB and state AG complaints and consider an FDCPA lawsuit.

Sample Debt Validation Letter

Below is a condensed preview of our debt validation letter template.

[Your Full Name]

[Street Address]

[City, State, ZIP]

[Date]

[Collection Agency Name]

[Agency Address]

RE: Debt Validation Request — Account No. [Acct #]

To Whom It May Concern,

This letter is sent in response to your communication regarding the above account. I dispute the debt and request validation pursuant to section 809 of the Fair Debt Collection Practices Act (15 U.S.C. § 1692g).

Please provide the following:

- Name and address of the original creditor

- Itemized accounting of the alleged debt, including all fees and interest

- Date of first delinquency on the original account

- Complete chain of assignment from the original creditor to your agency

- Copy of the original signed agreement creating the debt

- Proof that your agency is licensed to collect debts in my state

Until I receive the requested validation in writing, you must cease all collection activity, including reporting the debt to any consumer reporting agency. Any continued collection activity without validation is a violation of the FDCPA and may also violate the Fair Credit Reporting Act.

Sincerely,

[Printed Name]

Frequently Asked Questions

Common questions about validation letters, the FDCPA, statute of limitations, and how to handle aggressive debt collectors.

Official Resources

Authoritative resources for consumers dealing with third-party debt collectors.

CFPB - Debt Collection

Consumer Financial Protection Bureau debt collection hub and complaint portal

FTC - Full Text of the FDCPA

Complete federal statute on debt collection practices

CFPB - Regulation F

Modern CFPB rules implementing the FDCPA

NACA - Find a Consumer Attorney

National Association of Consumer Advocates attorney directory

National Consumer Law Center

Consumer protection research and self-help resources

USA.gov - Debt Collection

Official federal guide to consumer rights against collectors

Create your Debt Validation Letter in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.