What Is a Credit Dispute Letter?

A credit dispute letter is a formal written request sent to one of the three major consumer credit reporting agencies — Equifax, Experian, or TransUnion — asking the bureau to investigate and correct inaccurate, incomplete, unverifiable, or outdated information appearing on your credit report. The letter is the most powerful tool a consumer has under the Fair Credit Reporting Act (FCRA), the federal law that governs how credit information is collected and reported in the United States.

When a credit bureau receives a written dispute, it is legally required to launch an investigation within 30 days (or 45 days in certain circumstances). The bureau must contact the furnisher of the disputed information — the bank, lender, collection agency, or court that originally reported the item — and verify whether the information is accurate. If the furnisher cannot verify the item, or if it agrees that the information is incorrect, the bureau must correct or delete the disputed entry from your report. Items that cannot be verified within the investigation window must be removed.

Inaccurate credit information has real consequences. A single late payment can lower your credit score by 60 to 110 points, raising the cost of mortgages, auto loans, and credit cards by thousands of dollars. Inaccurate collection accounts can prevent you from renting an apartment, getting a security clearance, or even passing a pre-employment credit check. The CFPB receives hundreds of thousands of credit reporting complaints every year, making it the single most-complained-about consumer finance issue. Sending a well-drafted dispute letter is the first and most effective step toward fixing the problem.

While the major credit bureaus also accept disputes online and by phone, sending a written dispute letter by certified mail with return receipt requested creates a permanent paper trail, locks in the 30-day deadline, and preserves your right to sue under the FCRA if the bureau fails to comply. Online disputes through the bureau's websites often require you to waive certain rights or accept arbitration clauses, and they leave you with no proof of what you submitted or when. A traditional written dispute remains the gold standard for serious credit corrections.

Our attorney-reviewed credit dispute letter templates include all of the language required by the FCRA, identify the specific items being disputed, cite the relevant sections of the law, and request that the disputed items be corrected, deleted, or verified within the legal timeframe. Whether you are challenging an account that is not yours, an incorrect balance, an outdated negative item, or a duplicate listing, our templates give you a professional letter that the credit bureaus must take seriously.

FCRA Protection

Triggers federal law requiring a 30-day investigation

Paper Trail

Certified mail proof of when the bureau received your letter

Higher Success Rate

Written disputes are taken more seriously than online forms

Form Preview

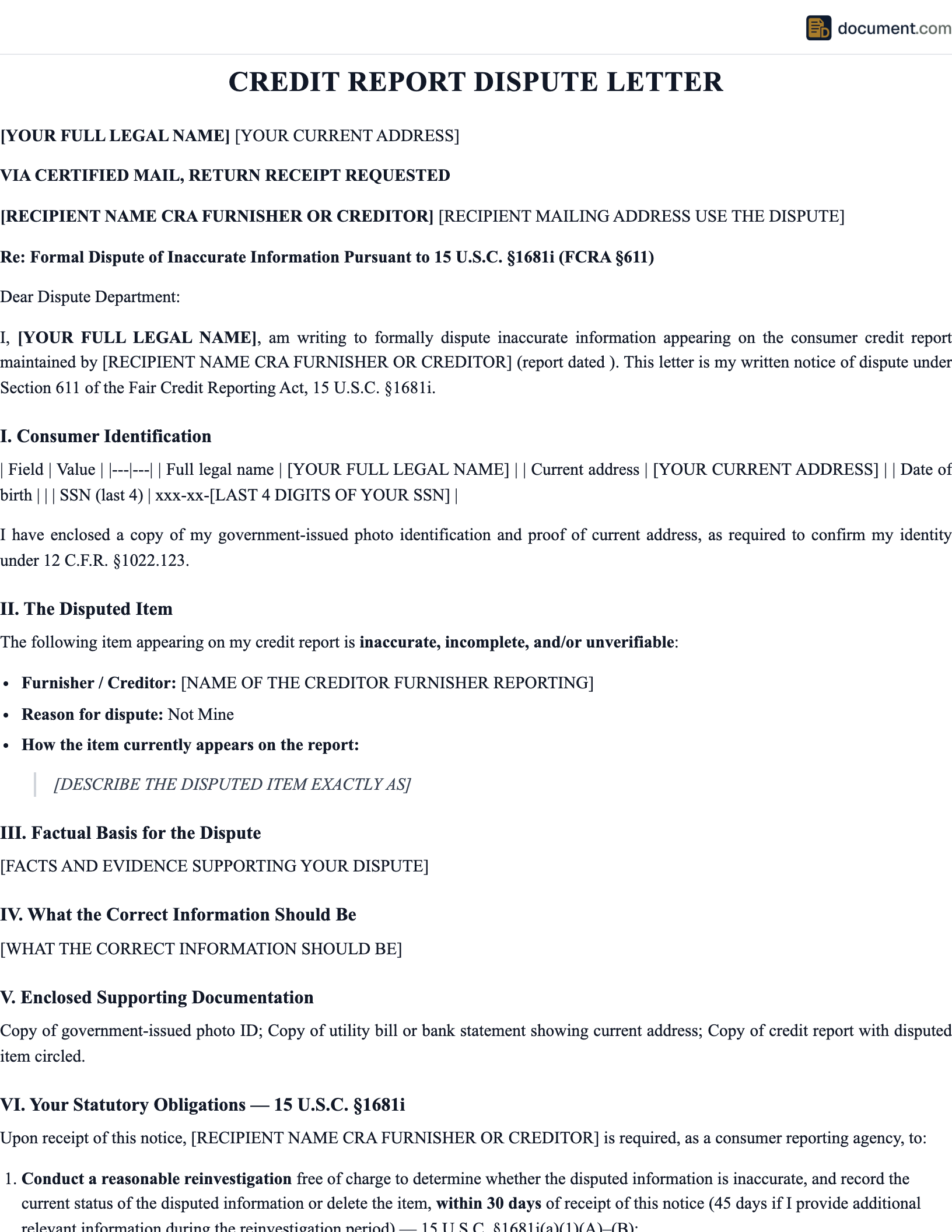

Our dispute letter template includes the required FCRA language, a clear identification of the disputed items, and a request for written results. Below is the structure of the finished letter.

[Your Name & Address]

[Date]

[Credit Bureau Name and Address]

RE: Dispute of Inaccurate Information — [Account Number]

To Whom It May Concern:

I am writing to dispute the following items on my credit report...

Disputed Item(s): _____________________

Reason for Dispute: ____________________

Enclosed Documentation: _______________

Sincerely,

[Signature]

Types of Credit Disputes

The right dispute letter depends on the kind of error you are challenging. Below are the most common categories of credit report disputes.

Mailed Dispute vs Online Dispute vs Phone Dispute

All three methods are accepted by the credit bureaus, but they offer very different levels of legal protection. Understanding the differences helps you pick the strongest approach for your situation.

| Feature | Certified Mail | Online | Phone |

|---|---|---|---|

| Paper Trail | Strong | Limited | None |

| Documentation | Unlimited | File upload only | None |

| Arbitration Clause | No | Often required | No |

| Triggers 30-Day Rule | Yes | Yes | Yes |

| Best For | Serious or repeat disputes | Simple errors | Quick fixes only |

How to Write a Credit Dispute Letter

Follow these steps to draft a credit dispute letter that the credit bureaus must take seriously and investigate within the federal 30-day window.

Pull All Three Credit Reports

Get a free copy of your credit report from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Identify every inaccurate item on each report.

Identify the Specific Items

List the account name, account number, and the exact reason each item is wrong (not yours, wrong balance, paid in full, past 7 years, etc.).

Gather Supporting Documents

Collect statements, payment receipts, court records, identity theft affidavits, and any other evidence that supports your dispute.

Draft the Letter

Use a clear, professional letter that cites the FCRA, identifies you, lists the disputed items, and requests correction or deletion within 30 days.

Make Copies and Sign

Sign the letter, make copies of the letter and all enclosures for your records, and never send original documents.

Mail by Certified Mail

Send each bureau its own letter via USPS certified mail with return receipt requested. Save the receipts and tracking numbers.

Track the 30-Day Deadline

Mark your calendar 30 days from the date the bureau received the letter. If you do not receive a response, follow up immediately.

Key Components of a Dispute Letter

Every effective dispute letter contains the same core elements that the credit bureaus need to identify you, locate the disputed items, and conduct a reasonable reinvestigation under the FCRA.

- Personal Identification: Full legal name, current and previous address, date of birth, and last four of SSN

- Specific Items in Dispute: Account name, account number, and exact reason the item is incorrect

- Statement of Inaccuracy: Clear assertion that the information is inaccurate, incomplete, or unverifiable

- FCRA Citation: Reference to section 611 of the FCRA and the 30-day investigation requirement

- Requested Outcome: Explicit request to correct, delete, or verify the disputed information

- Supporting Documentation: Copies of statements, receipts, court records, or identity theft reports

- Signature: Handwritten signature and printed name beneath it

Your Rights Under the FCRA

The Fair Credit Reporting Act gives consumers powerful rights against credit bureaus and the furnishers that report data to them. Understanding these rights is the key to using a dispute letter effectively.

The FCRA at a Glance

Enacted in 1970 and amended many times since, the FCRA is enforced by the CFPB, the FTC, and state attorneys general. It applies to every nationwide credit bureau, every specialty consumer reporting agency, and every furnisher of credit information. Violations can lead to actual damages, statutory damages of up to $1,000 per willful violation, and attorney's fees for the consumer.

- Free Annual Reports: One free credit report per year from each bureau via AnnualCreditReport.com (and free weekly reports through 2026).

- Right to Dispute: The right to dispute any inaccurate or incomplete item with both the credit bureau and the original furnisher.

- 30-Day Investigation: Credit bureaus must investigate disputes within 30 days (45 days if additional information is provided).

- Removal of Unverifiable Items: Items that cannot be verified must be deleted from the report.

- Limits on Negative Reporting: Most negative items must be removed after 7 years; bankruptcies after 10.

- Right to Sue: Consumers can sue credit bureaus and furnishers for FCRA violations and recover damages and attorney's fees.

What Happens After You Send the Letter

Once the credit bureau receives your dispute letter, the FCRA timeline begins. Here is what to expect over the following 30 to 45 days.

Day 1-5: Bureau Logs the Dispute

The credit bureau enters your dispute into its system and forwards it to the furnisher of the disputed information.

Day 5-25: Furnisher Investigates

The furnisher reviews its records, compares them to your dispute, and reports back to the credit bureau with a verification, correction, or deletion.

Day 25-30: Bureau Updates Your File

The credit bureau processes the furnisher's response and updates your credit report accordingly.

Day 30-35: Written Results Mailed

You receive a written notice of the investigation results along with a free updated copy of your credit report if changes were made.

After Day 30: Escalation Options

If the dispute fails or the bureau misses the deadline, you can re-dispute with new evidence, file a CFPB complaint, or consult a consumer attorney.

Sample Credit Dispute Letter

Below is a condensed preview of our credit dispute letter template. Your finished letter will be customized for your specific dispute, accounts, and chosen credit bureau.

[Your Full Name]

[Street Address]

[City, State, ZIP]

[Date]

[Credit Bureau Name]

[Bureau Dispute Address]

RE: Dispute of Inaccurate Credit Report Information

To Whom It May Concern,

I am writing to formally dispute the following inaccurate information on my credit report. Under section 611 of the Fair Credit Reporting Act (15 U.S.C. § 1681i), you are required to investigate this dispute and respond within 30 days.

DISPUTED ITEM(S):

Account: [Creditor Name]

Account Number: [Acct #]

Reason: [Reason for Dispute]

I am enclosing copies of supporting documentation, including [List Documents]. Please investigate this matter, correct or delete the inaccurate information, and provide me with written confirmation of the outcome along with an updated copy of my credit report.

I also request that you notify all parties who received my credit report in the past two years of any changes made as a result of this dispute, as required by the FCRA.

Sincerely,

[Printed Name]

Enclosures: Copy of credit report, copy of ID, supporting documents

Frequently Asked Questions

Common questions about credit disputes, FCRA rights, and how the credit reporting system works.

Official Resources

These official agencies and consumer protection resources offer additional help with credit reporting issues.

CFPB - Credit Reports and Scores

Official Consumer Financial Protection Bureau guide to credit reports

AnnualCreditReport.com

Federally mandated source for free credit reports from all three bureaus

FTC - Fair Credit Reporting Act

Full text of the FCRA and related federal regulations

Equifax - Dispute Center

Equifax official dispute submission and contact information

Experian - Dispute Center

Experian official online and mail dispute portal

TransUnion - Dispute Center

TransUnion official dispute resources and mailing address

IdentityTheft.gov

FTC resource for victims of identity theft and synthetic ID fraud

NACA - Find a Consumer Attorney

National Association of Consumer Advocates attorney directory

Create your Credit Report Dispute Letter in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.