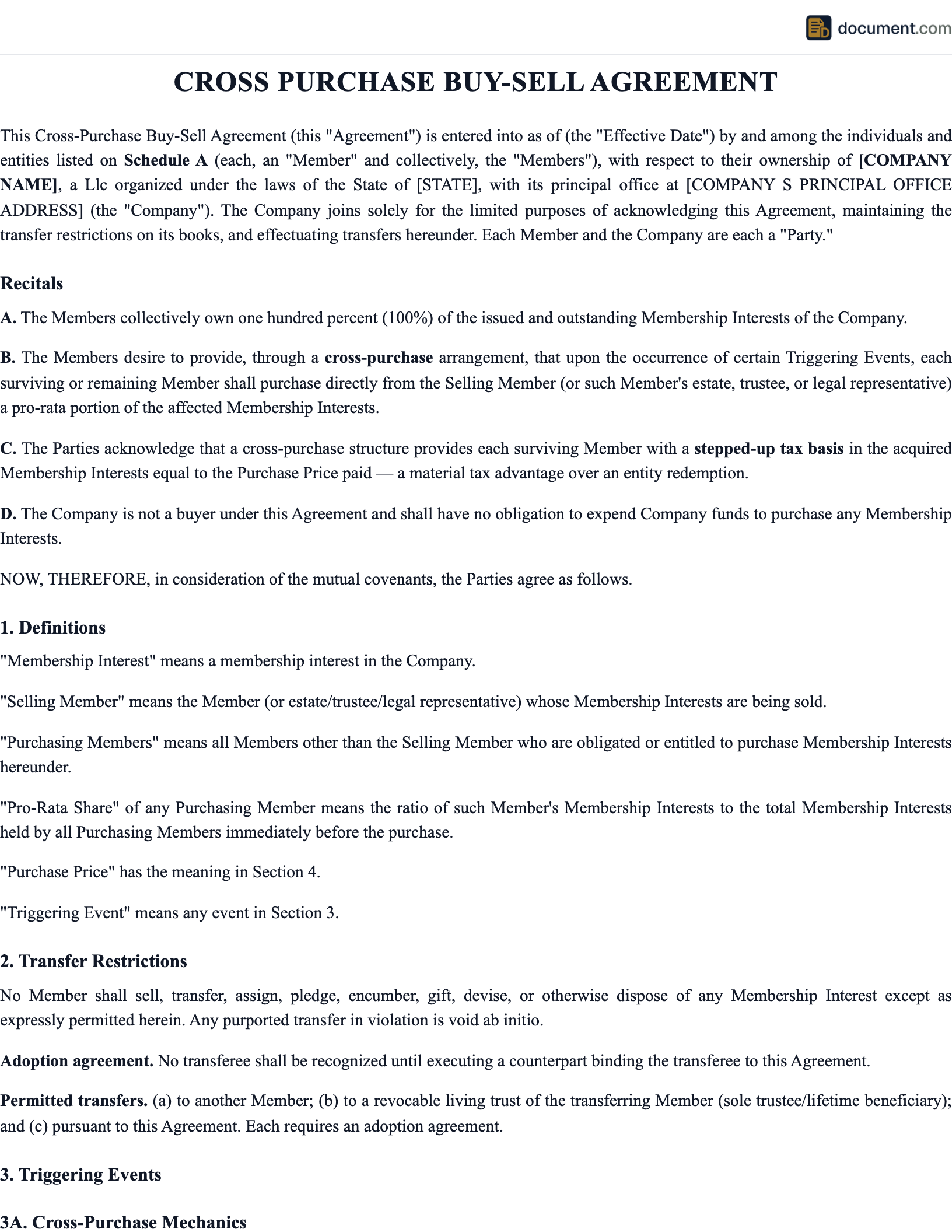

What Is a Cross-Purchase Buy-Sell Agreement?

A cross-purchase buy-sell agreement is a legally binding contract among the individual owners of a closely held business that requires each remaining owner to personally purchase a proportional share of a departing owner's equity interest upon the occurrence of a triggering event. Unlike a redemption agreement, in which the business entity itself buys back the departing owner's interest, a cross-purchase agreement places the purchase obligation directly on the individual owners. The business entity is not a party to the transaction, although the agreement will often be acknowledged by the company.

The cross-purchase structure is particularly well-suited to closely held corporations, partnerships, and limited liability companies with a small number of owners — typically two to four — who want a clean, tax-efficient mechanism for transferring ownership when one of them dies, becomes disabled, retires, or otherwise leaves the business. Because the remaining owners buy the interest themselves, they receive a stepped-up tax basis in the acquired shares equal to the purchase price. This basis adjustment can significantly reduce the capital gains tax the purchasing owners will eventually pay when they sell the business.

Cross-purchase agreements typically address the complete life cycle of ownership transitions. They define the triggering events that will require a buyout, the method for valuing the business at the time of the trigger, the source of funds used to complete the purchase (most commonly life insurance for death triggers and disability buy-out insurance for disability triggers), the payment terms for non-insured buyouts, restrictions on transferring shares to outside parties, rights of first refusal, tag-along and drag-along rights, and dispute-resolution procedures. A well-drafted agreement ensures that every foreseeable ownership transition is handled according to rules the owners agreed on while they were all still engaged, cooperative, and alive.

Without a cross-purchase (or other buy-sell) agreement in place, a closely held business faces serious risks. The deceased owner's shares pass to their heirs under a will or intestate succession, potentially giving a spouse, child, or other family member an ownership interest they have no experience managing. A disabled owner may continue to hold shares and draw income even though they can no longer contribute. A disgruntled departing owner may sell to a competitor or hold out for an unreasonable price. All of these outcomes are avoided by a properly drafted cross-purchase agreement that spells out exactly what happens in each scenario.

Basis Step-Up

Purchasing owners receive a higher tax basis in the acquired shares, reducing future capital gains

Ownership Control

Keeps ownership concentrated among active, approved individuals rather than outside heirs

Liquidity for Estates

Guarantees the departing owner's family receives fair value for an otherwise illiquid interest

Cross-Purchase Agreement Form Preview

Below is a visual preview of the sections included in a standard cross-purchase buy-sell agreement. Your completed document will be fully formatted and customized for your state, business entity type, ownership structure, and chosen valuation and funding methods.

Cross-Purchase Buy-Sell Agreement

Between Individual Business Owners

Section 1: The Company

Section 2: The Owners

Section 3: Triggering Events

Section 4: Valuation

Section 5: Funding

Each owner shall maintain a life insurance policy on each of the other owners in a face amount sufficient to fund the purchase obligation. Disability buy-out insurance shall be maintained by each owner on each of the other owners.

Section 6: Execution

Owner 1 Signature

Owner 2 Signature

How a Cross-Purchase Agreement Works

A cross-purchase buy-sell agreement operates through a sequence of clearly defined steps triggered by a specified event. Understanding this sequence helps owners, heirs, and advisors anticipate what will happen when a buyout is required.

Step 1 — Triggering Event Occurs. A triggering event (death, disability, retirement, termination, etc.) activates the buyout obligation. The departing owner (or their estate) and the company must provide written notice to the remaining owners within the notice period specified in the agreement.

Step 2 — Valuation. The business is valued using the method specified in the agreement. If independent appraisal is required, each party typically selects an appraiser, and the two appraisers either average their valuations or select a third appraiser whose determination is binding.

Step 3 — Allocation.The departing owner's interest is allocated among the remaining owners in proportion to their existing ownership percentages (or another allocation method specified in the agreement).

Step 4 — Funding and Closing. The purchasing owners obtain the purchase price from the designated funding source — most commonly life insurance proceeds for death triggers, disability buy-out insurance proceeds for disability triggers, and cash or installment notes for other triggers. The closing occurs within the period specified in the agreement, typically 30 to 90 days after valuation.

Step 5 — Transfer of Ownership.Upon payment (or delivery of promissory notes for installment sales), the departing owner's shares are transferred to the purchasing owners, who then hold increased ownership percentages in the business. The company's stock ledger or LLC membership records are updated to reflect the new ownership structure, and any necessary filings are made with state authorities.

Cross-Purchase vs Redemption Agreement

Cross-purchase and redemption agreements are the two main structures for buy-sell arrangements. Each has distinct advantages, and the right choice depends on the number of owners, tax considerations, funding preferences, and administrative capacity.

Cross-Purchase

- - Remaining owners personally buy the shares

- - Purchasing owners receive stepped-up basis

- - Best for 2-4 owner businesses

- - Each owner funds their own purchase

- - Life insurance policies: n(n-1) required

- - No corporate-level tax issues

- - Transfer-for-value rule risk on policies

Redemption

- - Company buys back the shares directly

- - No basis step-up for remaining owners

- - Better for 5+ owner businesses

- - Company funds the entire purchase

- - Only n life insurance policies needed

- - Possible accumulated earnings tax issues

- - Dividend treatment risk for selling owner

Hybrid approach:Some agreements use a hybrid structure (sometimes called a "wait and see" agreement) that preserves the option to choose between cross-purchase and redemption at the time of the triggering event. This flexibility allows the owners to pick the most tax-advantageous approach given the circumstances at that time.

Triggering Events

The agreement should explicitly list every event that will activate the buyout obligation. Each trigger should have clearly defined terms, notice requirements, and valuation and funding provisions.

Death of an Owner

Surviving owners purchase the deceased owner's shares directly, typically funded by life insurance

Permanent Disability

Remaining owners buy out a disabled owner whose condition prevents continued participation

Voluntary Retirement

An owner's planned exit triggers a buyout by co-owners at a pre-agreed valuation

Divorce of an Owner

Prevents an ex-spouse from becoming an unintended co-owner of the business

Personal Bankruptcy

Protects the company from creditors obtaining an owner's equity interest

Termination of Employment

Forces a departing owner-employee to sell back shares upon separation

Involuntary Transfer

Triggers purchase if shares would pass to an unapproved third party

Deadlock Among Owners

Provides an exit mechanism when owners cannot agree on material matters

Valuation Methods

The method used to determine the purchase price is one of the most important provisions in any cross-purchase agreement. A well-chosen valuation method produces a fair price that neither overpays the departing owner nor shortchanges the estate.

Fixed Price (Agreed Value)

The owners agree in writing on a fixed price and update that price at least annually. Simple and predictable, but requires discipline — if owners fail to update the value, the stated price may become wildly outdated. Many agreements include a fallback provision (such as appraisal) if the stated price has not been updated within a specified period.

Formula-Based

The agreement specifies a formula — commonly a multiple of EBITDA, multiple of revenue, book value plus goodwill, or capitalization of earnings. Formulas update automatically with changes in the business but may produce unfair results if the business changes character (e.g., transitioning from product sales to recurring subscription revenue).

Independent Appraisal

A qualified business appraiser determines the fair market value at the time of the triggering event. Most accurate but also the most expensive and time-consuming. Many agreements require appraisal only if the owners have failed to update a fixed price or if either party disputes the formula result.

Hybrid Method

Combines two or more methods — for example, using a fixed price if updated within the past 12 months, otherwise falling back to a formula or appraisal. Provides both predictability and a safety net against outdated valuations.

Funding the Buyout

A cross-purchase agreement is only as strong as its funding mechanism. Without adequate funding, the buyout obligation exists on paper but cannot be performed in practice. The agreement should specify how each type of triggering event will be funded.

- Life Insurance: Each owner maintains a life insurance policy on each of the other owners in an amount sufficient to fund the purchase. Proceeds are received tax-free and used to buy the deceased owner's shares directly from the estate. In a three-owner business, this requires six policies (each of three owners insures two others).

- Disability Buy-Out Insurance: Specialized insurance that pays a lump sum or installment benefits if the insured owner becomes permanently disabled as defined in the policy. Essential for agreements that include disability as a trigger.

- Sinking Fund: A savings account (held individually by each owner or in a trust) to which owners contribute over time, building up a reserve to fund buyouts for non-insured triggers.

- Installment Payments: The purchasing owners pay the purchase price in installments over a specified period (commonly 5 to 10 years) at a stated interest rate. The departing owner (or estate) holds a promissory note secured by the purchased shares.

- Third-Party Financing: The purchasing owners obtain a loan from a bank or SBA lender to fund the buyout. Useful when insurance proceeds are insufficient or when the trigger is one that cannot be insured.

The Transfer-for-Value Trap

When restructuring a buy-sell arrangement — for example, when an existing redemption agreement is converted to a cross-purchase — life insurance policies may be transferred among owners. Such transfers can trigger the transfer-for-value rule under IRC Section 101(a)(2), which can cause death benefit proceeds to be partially taxable. Specific exceptions apply, and careful planning is needed when cross-purchase funding arrangements are modified.

How to Create a Cross-Purchase Agreement

Drafting a comprehensive cross-purchase buy-sell agreement requires careful consideration of legal, tax, business, and personal factors. Follow these steps to create an agreement that will protect all of the owners and their families.

Identify All Owners and Their Interests

List every individual owner, their ownership percentage, class of stock or membership interest, and any special rights (voting, economic, etc.). Ensure that the ownership information matches the company's stock ledger or operating agreement.

Define the Triggering Events

Decide which events will activate the buyout obligation — death, disability, retirement, termination, divorce, bankruptcy, and any others. Define each trigger precisely (e.g., 'permanent disability' as inability to perform material duties for 180 consecutive days, certified by a qualified physician).

Choose a Valuation Method

Select from fixed price, formula, independent appraisal, or a hybrid approach. Include provisions for updating the value regularly and for resolving disputes about valuation.

Establish Funding Mechanisms

Determine how each type of buyout will be funded. For death triggers, purchase life insurance policies. For disability triggers, consider disability buy-out insurance. For other triggers, include installment payment terms or other backup funding.

Set Payment Terms

Specify whether the purchase price will be paid in a lump sum or installments. If installments, specify the number of payments, frequency, interest rate, and any prepayment rights. Address default remedies.

Include Transfer Restrictions

Prohibit transfers to non-approved parties without the consent of the other owners. Include rights of first refusal that give existing owners the chance to match any third-party offer before a sale can proceed.

Address Tax Considerations

Consult a tax advisor to ensure the agreement qualifies for favorable treatment under applicable tax law, including Section 2703 for estate tax valuation purposes. Consider the implications of the transfer-for-value rule for life insurance funding.

Include Dispute-Resolution Provisions

Specify the forum (arbitration, mediation, or court) for resolving disputes. Include choice-of-law and venue provisions that designate the applicable state law and the court or arbitration body that will hear any dispute.

Have All Owners Sign and Notarize

Every owner must sign the agreement for it to be enforceable. Notarization is not strictly required in most states but is strongly recommended. Each owner should retain a copy, and a master copy should be kept with the company's records.

Review and Update Annually

Schedule a yearly review of the agreement to update valuations, confirm insurance coverage, and address any changes in ownership, business operations, or tax law. Regular maintenance prevents the agreement from becoming outdated.

Key Components

A comprehensive cross-purchase agreement contains several critical sections. Each one plays an essential role in ensuring the agreement functions as intended when a triggering event occurs.

- Recitals: Background statements identifying the company, the owners, and the purpose of the agreement.

- Definitions: Precise definitions of critical terms such as "disability," "fair market value," "triggering event," and "permitted transferee."

- Ownership Representation: Confirmation of each owner's percentage interest and the class of ownership held.

- Transfer Restrictions: Prohibitions on unauthorized transfers and provisions for permitted transfers (e.g., to family members or revocable trusts).

- Right of First Refusal: Allows existing owners to match any third-party offer before a sale can proceed.

- Purchase Obligation: The core commitment by each owner to purchase a proportional share upon a triggering event.

- Valuation Mechanism: The method used to determine the purchase price.

- Funding Provisions: Life insurance, disability insurance, and other funding arrangements.

- Closing Procedures: The steps and timing for completing the buyout.

- Non-Compete and Non-Solicitation: Protects the remaining owners from competition by the departing owner.

- Dispute Resolution: Arbitration, mediation, or litigation procedures.

- Amendment and Termination: How the agreement can be modified or ended by the owners.

Tax Implications

Cross-purchase agreements have significant tax consequences for the selling owner, the purchasing owners, and (indirectly) the company. Understanding these implications is essential to choosing the right structure and negotiating fair terms.

Selling Owner (or Estate)

The selling owner typically recognizes capital gain equal to the difference between the sale price and their basis in the shares. For shares held until death, the estate receives a step-up in basis under IRC Section 1014 to fair market value at the date of death, typically eliminating most or all capital gains on the subsequent sale under the buy-sell agreement.

Purchasing Owners

Each purchasing owner receives a new basis in the acquired shares equal to the purchase price paid. This higher basis reduces the taxable gain they will recognize when they eventually sell their (now larger) ownership interest. This basis step-up is the primary tax advantage of cross-purchase over redemption structures.

Life Insurance Proceeds

Life insurance death benefit proceeds are generally received income tax-free under IRC Section 101(a), provided the transfer-for-value rule does not apply. If a policy has been transferred for value (except to certain exempt transferees), a portion of the proceeds may be taxable.

Estate Tax Valuation

A buy-sell agreement can establish the value of a business interest for estate tax purposes if it meets the requirements of IRC Section 2703: it must be a bona fide business arrangement, not a device to transfer property to family members for less than fair value, and comparable to similar arrangements entered into by unrelated parties in arm's-length transactions.

Sample Cross-Purchase Agreement

Below is a condensed preview of our cross-purchase buy-sell agreement template. Your completed document will be fully customized for your specific company, owners, triggering events, valuation method, and funding provisions.

CROSS-PURCHASE BUY-SELL AGREEMENT

Between Individual Owners of [Company Name]

This Cross-Purchase Buy-Sell Agreement ("Agreement") is entered into as of[Effective Date]by and among the undersigned owners (collectively, the "Owners") of[Company Name], a [State of Formation / Entity Type](the "Company").

1. PURPOSE

The Owners wish to provide for the orderly transfer of ownership interests in the Company upon the occurrence of certain triggering events, to ensure continuity of management, to establish a fair method for determining the purchase price, and to provide adequate funding for such transfers.

2. TRIGGERING EVENTS

Upon the occurrence of any of the following events with respect to any Owner (the "Departing Owner"), the remaining Owners shall be obligated to purchase, and the Departing Owner (or their estate) shall be obligated to sell, all of the Departing Owner's interest in the Company:

- Death of the Owner

- Permanent disability as defined in Section 8

- Voluntary retirement or withdrawal

- Involuntary termination of employment with the Company

- Personal bankruptcy or insolvency

- Material breach of this Agreement

3. PURCHASE PRICE

The purchase price for the Departing Owner's interest shall be determined as follows: [Valuation Method]. The purchase price shall be reviewed and updated annually by written agreement of the Owners.

4. ALLOCATION

The Departing Owner's interest shall be purchased by the remaining Owners in proportion to their respective ownership interests immediately prior to the triggering event.

5. LIFE INSURANCE FUNDING

Each Owner shall apply for and maintain a life insurance policy on the life of each of the other Owners in a face amount at least equal to the Owner's share of the purchase obligation. Each Owner shall be the owner and beneficiary of the policies they hold on the other Owners...

6. CLOSING

Closing of the purchase shall occur within[Number]days after the triggering event. At closing, the remaining Owners shall deliver the purchase price and the Departing Owner (or their estate) shall deliver the ownership certificates duly endorsed for transfer.

7. TRANSFER RESTRICTIONS

No Owner shall sell, assign, pledge, or otherwise transfer any interest in the Company except as expressly permitted by this Agreement. Any attempted transfer in violation of this Agreement shall be void...

8. NON-COMPETE

For a period of [Period]following the closing, the Departing Owner shall not engage in any business that competes with the Company within[Geographic Area]...

Frequently Asked Questions

Find answers to common questions about cross-purchase buy-sell agreements, funding, valuation, tax treatment, and implementation.

Official Resources

For additional information on buy-sell agreements, business succession planning, and relevant tax provisions, consult these official and reputable resources.

IRS - Business Structures

IRS guidance on entity types, tax implications, and reporting requirements

SBA - Sell or Close Your Business

Small Business Administration guide to business transitions and succession

IRC Section 2703 - Cornell Law

Statutory text on valuation of property for estate and gift tax purposes

Uniform Law Commission

Uniform business entity acts adopted by many states

ABA Business Law Section

American Bar Association resources on corporate and business law

IRC Section 101 - Life Insurance

Tax treatment of life insurance proceeds and transfer-for-value rules

SCORE - Small Business Mentoring

Free business mentoring and succession planning resources

NAEPC - Estate Planning Council

National Association of Estate Planners and Councils

Create your Cross Purchase Buy Sell Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.