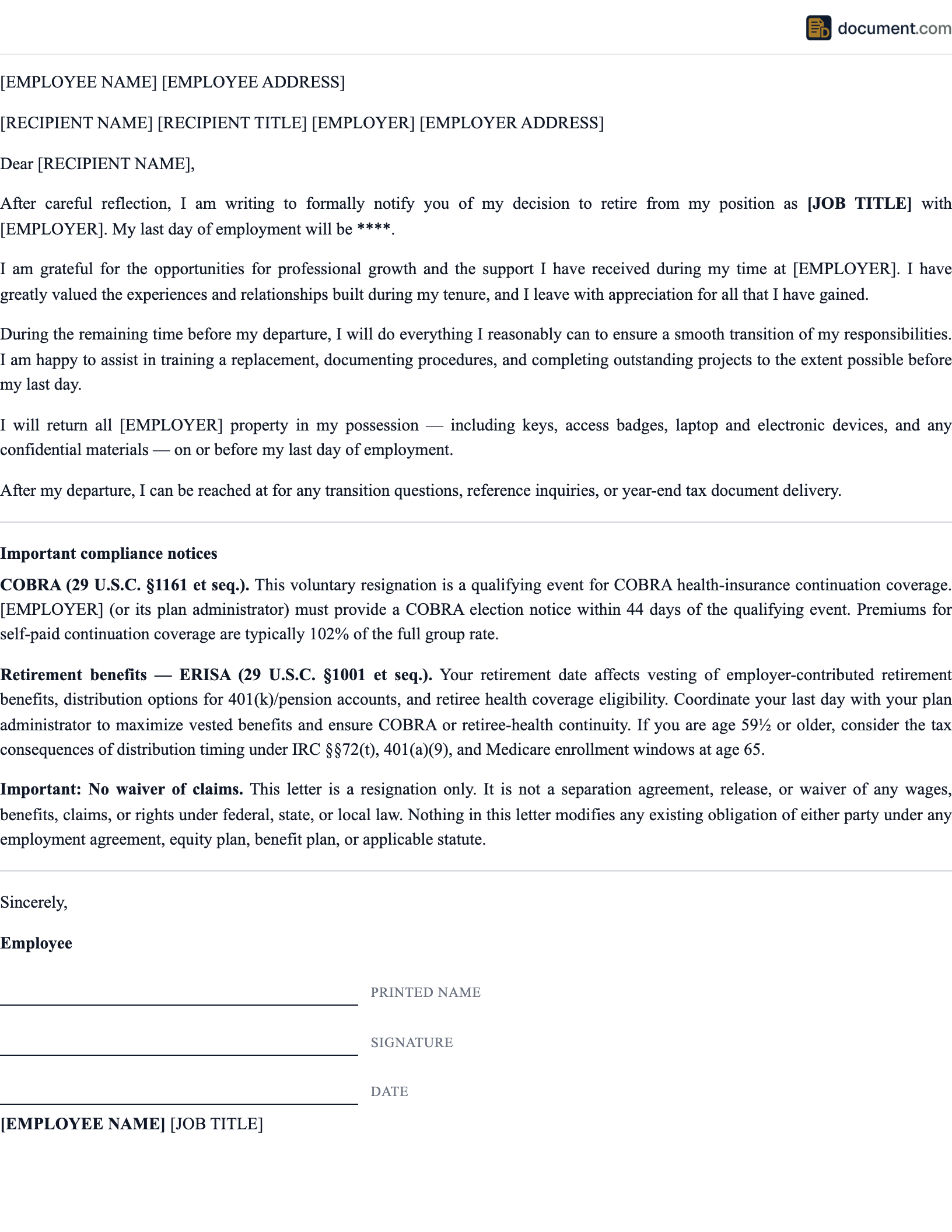

What Is a Retirement Resignation Letter?

A retirement resignation letter is the written instrument by which an employee gives notice of permanent withdrawal from the workforce or transition to phased retirement. It operates as both an HR notice and the trigger for plan- election windows under ERISA-governed retirement plans (29 U.S.C. § 1001 et seq.), Social Security application windows under 42 U.S.C. § 402, and Medicare Initial Enrollment Period under 42 C.F.R. § 407.14. The retirement letter differs from a standard resignation because the date controls more downstream financial determinations than any other employment event.

The financial stakes are quantifiable and material. Pension benefit calculations under defined benefit plans governed by IRC § 415(b) tie the monthly benefit to years of service, final average salary (typically the highest 3 to 5 consecutive years), and a benefit multiplier; leaving one month before a service-year anniversary can reduce the monthly pension by hundreds of dollars permanently. Social Security delayed retirement credits add 8% per year of delay above full retirement age, capped at age 70 under 42 U.S.C. § 402(w). 401(k) distribution sequencing affects lifetime tax burden under IRC §§ 402, 408, and 401(a)(9). The pre-Medicare health insurance bridge (age 55 to 65 for early retirees) can total $180,000 to $300,000 in premiums absent retiree medical benefits.

Social Security election and full retirement age

Full retirement age under the Social Security Act is 67 for those born in 1960 or later (42 U.S.C. § 416(l)). Filing at age 62 produces a permanent reduction of 25% to 30% from the Primary Insurance Amount; filing at age 70 produces a 24% to 32% increase via delayed retirement credits. The earnings test under 42 U.S.C. § 403(b) reduces pre-FRA benefits by $1 for each $2 of earnings above $22,320 (2024 indexed limit). The retirement resignation date and the SSA filing date are independent; coordinating them for maximum lifetime benefit typically requires bridging the gap with 401(k) distributions or taxable savings rather than filing immediately at retirement.

Medicare enrollment, RMDs, and pension elections

Medicare Initial Enrollment Period runs three months before through three months after the 65th birthday (42 C.F.R. § 407.14). Missing the window triggers Part B late-enrollment penalties of 10% per 12-month delay added permanently to the monthly premium. Required Minimum Distributions begin at age 73 under SECURE 2.0 (IRC § 401(a)(9)), increasing to age 75 in 2033. ERISA- governed pension elections include lump-sum versus annuity, single-life versus joint-and-survivor, and spousal-consent waivers under 29 U.S.C. § 1055; spousal consent in writing before a notary is required to elect any non-qualified joint-and-survivor option.

Financial Coordination

Aligns your retirement date with pension, 401(k), Social Security, and insurance milestones.

Legacy Transition

Structured knowledge transfer plan for decades of institutional expertise.

Career Celebration

Acknowledges your contributions and closes a chapter with dignity and gratitude.

Retirement Resignation Letter Preview

Retirement Resignation Letter

Notice of Retirement

1. RETIREMENT ANNOUNCEMENT

After years with , I am writing to formally announce my retirement effective .

2. TRANSITION PLAN

I propose the following knowledge transfer schedule during my remaining months to ensure continuity of operations.

3. BENEFITS AND FINANCIAL MATTERS

I request a meeting with HR and the benefits administrator to finalize pension elections, 401(k) distribution, and retiree health benefit enrollment.

EMPLOYEE SIGNATURE

DATE

Key Components

Eight components, each tied to a specific statute or plan-document mechanic. Omitting the pension-election request, the Medicare timing reference, or the COBRA inquiry can cost the retiree thousands in benefits or trigger permanent late-enrollment penalties.

Employer pension elections under ERISA

ERISA-governed defined benefit plans (29 U.S.C. § 1054) require the participant to elect among lump-sum, single- life annuity, joint-and-survivor annuity, and certain- period options. The default under 29 U.S.C. § 1055 is the qualified joint-and-survivor annuity at 50% to 100% survivor benefit; electing any other form requires written spousal consent before a notary. The retirement letter should request a meeting with the plan administrator at least 90 days before the effective date to receive the Statement of Benefits, the Notice of Annuity Information under 29 C.F.R. § 2520.104b-10, and the election forms. Public-sector systems (CalPERS, NYSLRS, FERS, CSRS) impose system-specific windows; missing the election deadline locks in the default form.

401(k) RMD rules under IRC § 401(a)(9)

Required Minimum Distributions begin at age 73 under SECURE 2.0 (IRC § 401(a)(9), increasing to 75 in 2033). The first RMD must be taken by April 1 of the year after the participant turns 73; subsequent RMDs by December 31. Failure to take the RMD triggers a 25% excise tax under IRC § 4974, reduced to 10% if corrected within two years. The still-working exception under IRC § 401(a)(9)(C) defers RMDs from the current employer's plan until actual retirement for non-5%-owners. The retirement date relative to age 73 controls the timing of the first RMD calculation.

| Component | Purpose | Key Details |

|---|---|---|

| Retirement Date | Anchors all financial calculations | Coordinated with pension vesting, benefit year-end, Social Security strategy |

| Years of Service | Establishes tenure for context and benefits | Total years, hire date, significant milestones or roles held |

| Knowledge Transfer Plan | Preserves institutional memory | Multi-month phased handoff, documentation schedule, successor training timeline |

| Benefits Meeting Request | Initiates financial transition | Pension election, 401(k) rollover, retiree health, life insurance conversion, COBRA |

| Phased Retirement Terms | Documents gradual transition if applicable | Reduced schedule, consulting arrangement, part-time period, final full retirement date |

| Career Reflection | Honors the professional relationship | Gratitude for career-defining experiences, mentors, team members, and growth opportunities |

| Post-Retirement Availability | Offers continued access to expertise | Consulting availability, willingness to mentor successor, contact information |

| Administrative Items | Covers practical departure logistics | Property return, final pay, PTO payout, W-2 mailing address, expense reports |

How to Write a Retirement Resignation Letter

Six steps. Pension and Social Security date optimization precedes drafting because the retirement date is the binding variable in every downstream calculation: pension benefit, 401(k) RMD timing under IRC § 401(a)(9), Medicare Initial Enrollment Period under 42 C.F.R. § 407.14, and Social Security Primary Insurance Amount under 42 U.S.C. § 416.

Optimize the Retirement Date Against Pension and SSA Calculations

Request a written pension benefit calculation from the plan administrator at two or three candidate dates. Confirm vesting cliffs (commonly 10, 20, 25 years), final average salary periods (highest 3 to 5 consecutive years per IRC § 415(b)), and subsidized early-retirement age thresholds. Coordinate with the SSA Estimator at ssa.gov for benefits at age 62, full retirement age (67 for those born 1960+ per 42 U.S.C. § 416(l)), and age 70. Confirm Medicare Initial Enrollment Period dates relative to age 65 under 42 C.F.R. § 407.14. The difference between December 31 and January 1 retirement dates can be worth $100,000+ over a 25-year retirement.

State the Retirement and Effective Date

Operative language with tenure context: 'After [X] years with [employer], I hereby give notice of my retirement effective [date].' The effective date triggers ERISA-governed plan windows, COBRA, and Medicare enrollment timing. For phased retirement under IRS Notice 2007-87 or federal phased retirement under 5 U.S.C. § 8336a, attach the executed phased-retirement agreement and reference its terms by date.

Present a Three-Phase Knowledge Transfer Plan

Structure the transition over the notice period: months 1 through 2 for written process documentation and credential inventory; months 2 through 3 for successor training and shadowing; final month for relationship handoffs, vendor introductions, and administrative closeout. Include specific deliverables per phase. Long-tenured retirees often hold institutional knowledge that exists in no document; the transition plan is the only mechanism to preserve it.

Request the Benefits Transition Meeting

Request a meeting with HR and the plan administrator at least 90 days before the effective date covering: pension election forms and the Notice of Annuity Information under 29 C.F.R. § 2520.104b-10, 401(k) distribution and rollover procedures including NUA election under IRC § 402(e)(4) for employer-stock holdings, COBRA election notice under 29 U.S.C. § 1166, retiree health benefit enrollment if available, life insurance conversion under group policy terms, accrued PTO payout per state statute, and treatment of unvested RSUs or options under retirement-eligibility acceleration provisions.

Include Career Context, Not Sentimentality

Reference two or three specific career-defining experiences: a project that defined a phase of your career, a mentor or team that shaped your trajectory, an organizational milestone you contributed to. Avoid generic gratitude. The letter becomes part of the personnel file and influences how the retirement is remembered organizationally; specific content is durable, generic content fades.

Define Post-Retirement Availability

If open to consulting, reference availability windows and preferred terms in general (3 to 6 months of email and phone availability, defined hours per week, hourly or project-based compensation under a 1099 contractor relationship per IRS Common Law Test factors). Document the consulting arrangement in a separate written agreement; the resignation letter references it but does not formalize it. For executives or senior employees with retention value, the consulting arrangement is a negotiated benefit, not a courtesy.

Frequently Asked Questions

Official Resources

Authoritative resources on retirement planning, pension benefits, and post-employment financial transitions.

SSA - Retirement Benefits

Social Security Administration retirement planning tools and benefit calculators.

DOL - Retirement Plans

Department of Labor guidance on 401(k), pension, and retirement plan rights.

Medicare.gov - Getting Started

Official guide to Medicare enrollment, coverage options, and enrollment periods.

DOL - COBRA Coverage

Health insurance continuation for the gap between employer coverage and Medicare.

IRS - Retirement Plans

Tax rules for 401(k) distributions, IRA rollovers, and retirement income.

PBGC - Pension Benefit Guaranty

Federal agency that protects private-sector pension benefits and insures plan participants.

Create Your Retirement Resignation Letter

Generate a professional retirement letter that honors your career and coordinates your financial transition.

Create DocumentNo account required. Free to create and preview.