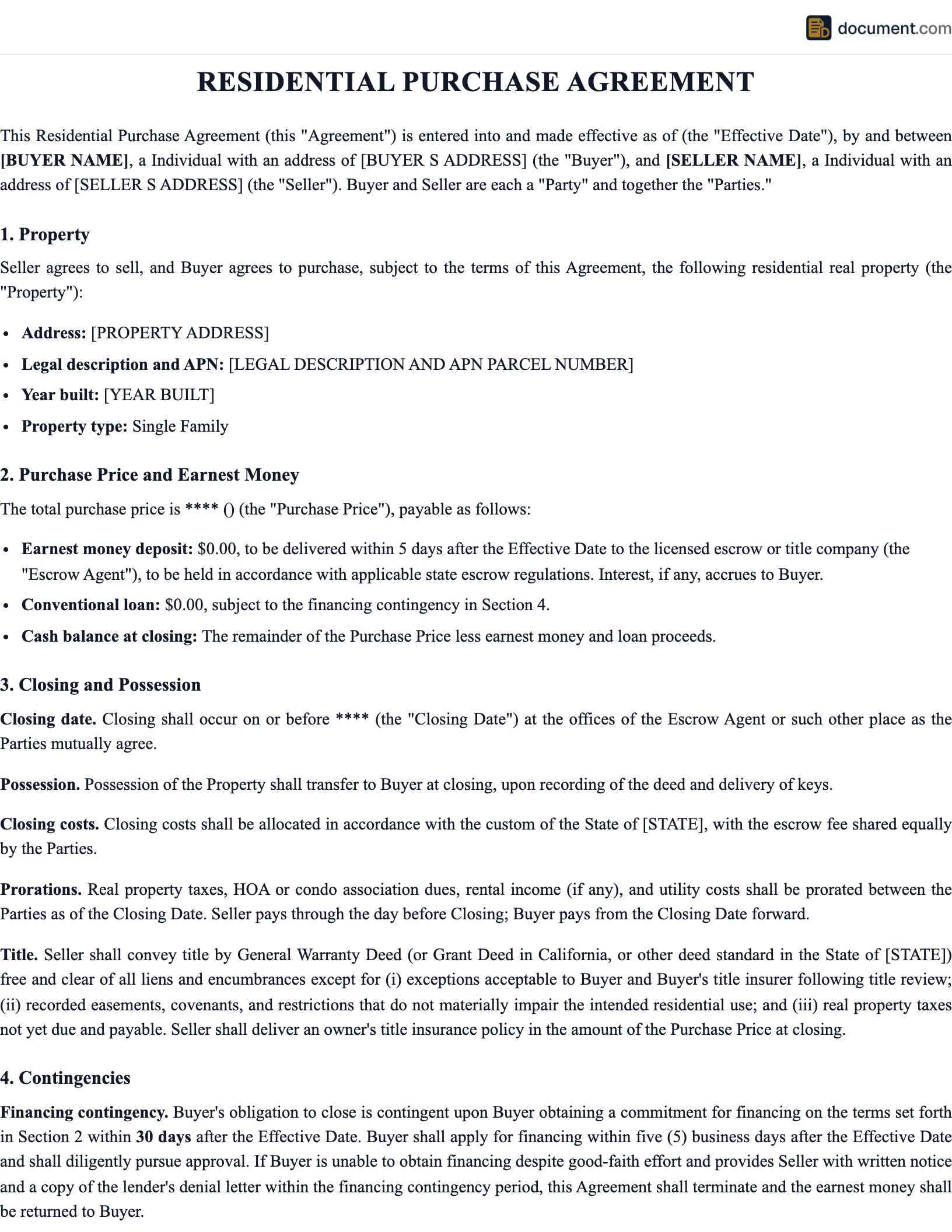

New Hampshire Residential Purchase Agreement Overview

A residential purchase agreement in New Hampshire is a legally binding contract between a buyer and seller that outlines all terms and conditions for the sale of residential real property within the state. New Hampshire real estate transactions are governed by New Hampshire RSA Chapter 331-A, which establishes the legal framework for property transfers, agent licensing, and consumer protections.

New Hampshire is considered an attorney state, meaning that an attorney is required or customarily involved in the real estate closing process. The New Hampshire Real Estate Commission oversees real estate licensing and regulation in the state, ensuring that agents and brokers meet professional standards and comply with state law.

Whether you are buying your first home, upgrading to a larger property, or purchasing investment real estate in New Hampshire, a well-drafted purchase agreement protects both parties by clearly defining the purchase price, earnest money, contingencies, closing date, and all rights and obligations throughout the transaction. Our New Hampshire-specific template addresses all state requirements and local customs.

New Hampshire Real Estate Quick Facts

$7.50 per $1,000 (each party)

Transfer tax rate

Yes

Attorney state

Mandatory disclosure form

Disclosure requirements

$3,876

Avg. closing costs

New Hampshire Real Estate Laws

Real estate transactions in New Hampshire are governed by a combination of state statutes, regulations, and common law principles. The primary statutory framework is found in New Hampshire RSA Chapter 331-A. Key aspects of New Hampshire real estate law that affect residential purchase agreements include:

- Contract Formation: New Hampshire requires a written contract signed by both parties for real estate transactions to be enforceable under the statute of frauds. The contract must include the essential terms: parties, property description, price, and closing date.

- Agency Relationships: New Hampshire law requires real estate agents to disclose their agency relationship (buyer's agent, seller's agent, or dual agent) at the earliest practical opportunity. The New Hampshire Real Estate Commission enforces agent licensing and ethical standards.

- Earnest Money: New Hampshire law governs how earnest money deposits are held in escrow, the conditions for release, and the procedures for resolving disputes over earnest money when a transaction falls through.

- Property Condition: New Hampshire requires sellers to complete a property condition disclosure form detailing known defects, environmental hazards, and other material facts about the property.

- Closing Requirements: New Hampshire requires or customarily involves attorney oversight at closing. The attorney reviews documents, conducts the title examination, and ensures legal compliance.

Required Seller Disclosures in New Hampshire

New Hampshire requires sellers to complete a mandatory property condition disclosure form before or at the time of signing the purchase agreement. This disclosure covers the property's physical condition, systems, environmental hazards, and other material facts that could affect the buyer's decision.

Federal Lead Paint Disclosure (Pre-1978 Homes)

Regardless of New Hampshire state law, federal regulations require sellers of homes built before 1978 to disclose known lead-based paint hazards, provide available lead inspection reports, and give buyers a 10-day opportunity to conduct a lead-based paint inspection. This is a non-negotiable federal requirement that applies in all 50 states.

Structural Condition

Foundation, roof, walls, floors, ceilings, windows, doors

Water & Sewer

Plumbing, water source, sewer/septic, water heater, drainage

HVAC & Electrical

Heating, cooling, electrical panel, wiring, insulation

Environmental Hazards

Lead paint, asbestos, radon, mold, underground tanks

Flood & Natural Hazards

Flood zone status, past flooding, drainage issues, soil stability

Legal & HOA

HOA fees, pending litigation, easements, boundary disputes, liens

New Hampshire Closing Process

The real estate closing process in New Hampshire typically takes 45-60 days from the date both parties sign the purchase agreement. As an attorney state, New Hampshire requires or customarily involves attorney oversight throughout the closing process to ensure legal compliance and protect both parties' interests.

Execute Purchase Agreement

Both parties sign the purchase agreement, and earnest money is deposited into escrow within 1-3 business days

Home Inspection & Due Diligence

Buyer conducts home inspection, reviews seller disclosures, and investigates property condition within the contingency period

Appraisal & Title Search

Lender orders appraisal to verify property value; title company conducts title search and issues title commitment

Loan Approval & Clear to Close

Lender completes underwriting and issues clear-to-close; buyer receives Closing Disclosure at least 3 business days before closing

Final Walkthrough

Buyer conducts final walkthrough 24-48 hours before closing to verify property condition and agreed-upon repairs

Closing Day

Sign closing documents, transfer funds, record deed at New Hampshire county recorder's office, and receive keys

New Hampshire Transfer Taxes & Closing Costs

New Hampshire imposes a real estate transfer tax of $7.50 per $1,000 (each party). This tax is assessed on the transfer of real property and is typically paid at closing. Average total closing costs in New Hampshire are approximately $3,876 (excluding lender fees) for a median-priced home.

| Fee / Tax | Typical Amount |

|---|---|

| State Transfer Tax | $7.50 per $1,000 (each party) |

| Recording Fees | $50 - $250 |

| Title Insurance (Lender's) | $500 - $1,500 |

| Title Insurance (Owner's) | $500 - $2,000 |

| Escrow / Settlement Fee | $500 - $1,500 |

| Appraisal Fee | $300 - $600 |

| Home Inspection | $300 - $500 |

New Hampshire Title Insurance Requirements

Title insurance is a critical component of any real estate transaction in New Hampshire. While not legally mandated for all transactions, virtually all mortgage lenders require a lender's title insurance policy as a condition of the loan. An owner's title insurance policy is optional but provides important protection for the buyer's equity.

In New Hampshire, the title company or attorney conducts a thorough search of public records to identify any liens, encumbrances, easements, or defects that could affect the title. Common issues discovered during title searches include unpaid property taxes, mechanic's liens, judgment liens, HOA liens, boundary disputes, and recording errors. Title insurance protects against losses from these and other title defects, including those not discoverable through the public record search.

Important: Owner's Title Insurance

The lender's title insurance policy only protects the lender's interest — not yours. An owner's title insurance policy protects your full equity in the property for as long as you own it (or have liability from ownership). The one-time premium typically costs $500-$2,000 and is one of the best investments you can make in a real estate transaction.

New Hampshire Residential Purchase Agreement FAQ

Answers to common questions about residential purchase agreements, the closing process, and real estate laws in New Hampshire.

Official New Hampshire Resources

Use these official resources to verify New Hampshire real estate requirements, find licensed professionals, and access state-specific forms and regulations.

New Hampshire Real Estate Commission

Licensing, regulations, and consumer resources

CFPB — Owning a Home

Federal home buying resources and mortgage tools

HUD — Buying a Home

Federal housing resources, counseling, and assistance programs

EPA — Lead Paint Information

Federal lead paint disclosure requirements and safety

Create your New Hampshire Residential Purchase Agreement in under 5 minutes.

Answer a few questions and download a New Hampshire-compliant document, ready for the state agency.