What Is a Profit and Loss Statement?

A profit and loss statement — also known as an income statement, statement of operations, or simply a P&L — is a financial report that summarizes a business's revenues, costs, and expenses over a defined period of time and ends with the bottom-line net income or net loss. It is one of the three core financial statements every business is expected to maintain, alongside the balance sheet and the cash flow statement. Unlike the balance sheet, which captures a single moment in time, the P&L tells a story across a period: how much money came in, how much it cost to produce or deliver the goods and services that generated that money, what was spent on running the company, and what was left over for the owners.

At its simplest, a P&L answers a single question — did the business make money during the period? But the value of a well-prepared P&L goes far beyond that yes-or-no answer. By breaking revenue and expenses into meaningful categories, the income statement reveals whether the business is gross-margin healthy, whether overhead is creeping up faster than sales, whether one product line is subsidizing another, and whether the company is generating enough operating income to support its debt and reward its owners. It is the document that bankers ask for first, that investors study line by line during diligence, and that the IRS effectively reproduces every year on Schedule C, Form 1065, Form 1120-S, or Form 1120.

A profit and loss statement always covers a period — most commonly a calendar month, a fiscal quarter, or a full fiscal year. The header of every P&L should clearly state the period covered (for example, "For the Three Months Ended March 31, 2026") and the basis of accounting (cash or accrual). Within the report itself, line items are organized in a deliberate sequence: revenue at the top, then cost of goods sold to arrive at gross profit, then operating expenses to arrive at operating income, then non-operating items, interest expense, and income taxes to arrive at net income. This ordering — from revenue at the top to net income at the bottom — is why people refer to revenue as the "top line" and net income as the "bottom line."

The P&L is intimately connected to the other financial statements. Net income from the bottom of the income statement flows into retained earnings on the balance sheet, increasing owners' equity. Net income is also the starting point of the indirect-method cash flow statement, which then adjusts for non-cash items like depreciation and changes in working capital to show how much cash the business actually generated. A P&L that does not reconcile to the balance sheet and cash flow statement is a P&L with errors — reconciling all three is one of the core month-end close tasks for any bookkeeper or controller.

Whether you are a sole proprietor preparing for tax season, a startup founder pitching investors, a small business owner applying for an SBA loan, or a controller closing the books at month-end, a clean P&L statement is the foundation of every financial conversation you will have. Our templates are designed to make that foundation easy to build correctly the first time, with the right categories, the right order, and the right level of detail for the audience you are reporting to.

Performance Tracking

Measure revenue, margins, and profitability across any period from one month to a full year

Lender-Ready

Built to satisfy SBA, bank, and investor due-diligence requirements out of the box

Tax-Ready Categories

Expense lines align with IRS Schedule C, Form 1120, and Form 1120-S categories

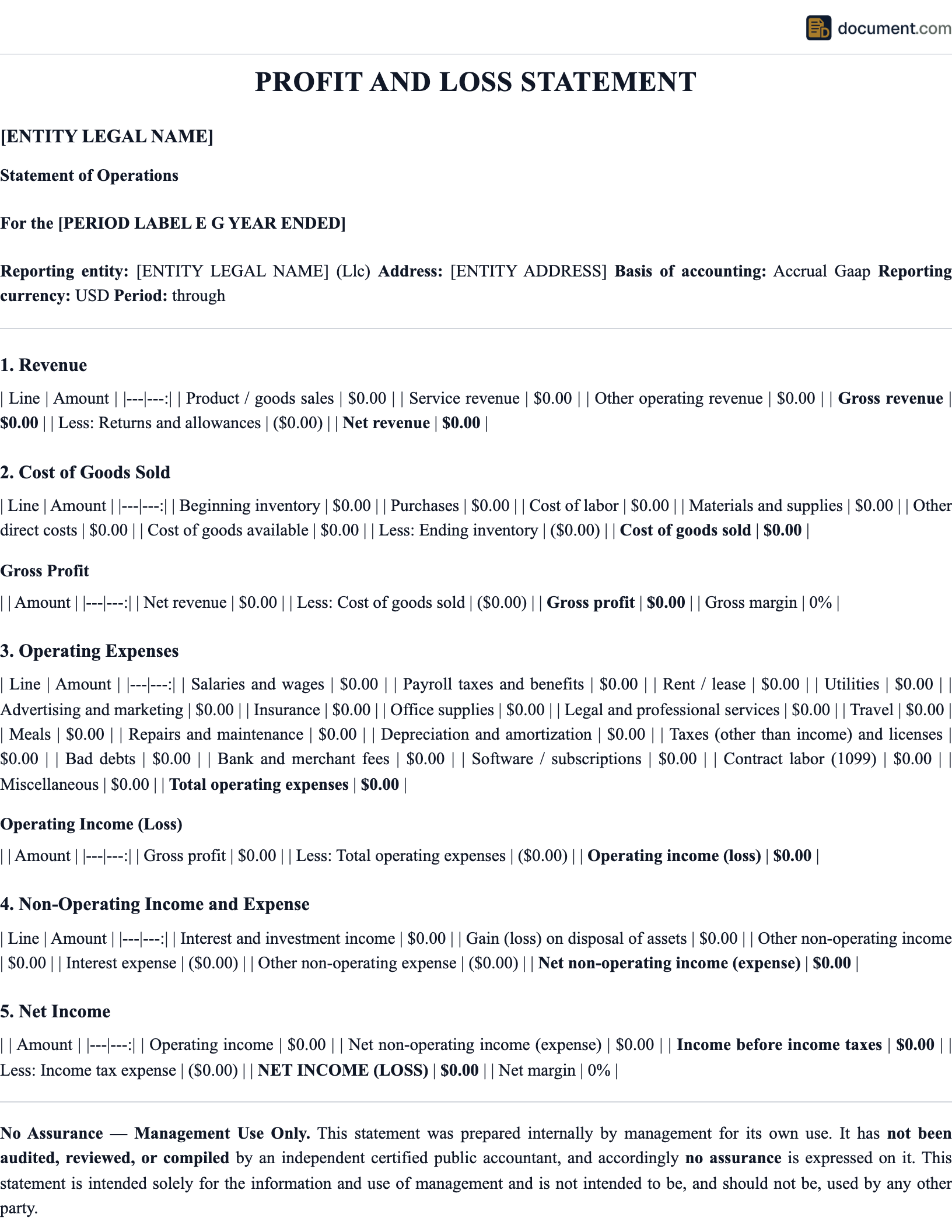

P&L Statement Form Preview

Below is a structured preview of the sections and line items included in our multi-step profit and loss statement template. Your completed statement will be fully formatted in PDF or Excel, with auto-calculated subtotals for gross profit, operating income, and net income.

Profit & Loss Statement

Multi-Step Format — Accrual Basis

Section 1: Revenue

Section 2: Cost of Goods Sold

Gross Profit: 636,100

Section 3: Operating Expenses

Operating Income: 206,700

Section 4: Non-Operating Items

Types of Profit and Loss Statements

P&L statements come in several formats and reporting periods depending on the audience, the level of detail required, and the business's accounting maturity. Choose the format that fits your purpose — a quick monthly internal review needs a different layout than a three-year projection submitted with an SBA loan application.

Single-Step vs Multi-Step Format

The single-step income statement aggregates all revenues into one total and all expenses into another, then subtracts expenses from revenue to arrive at net income in a single calculation. It is the simplest possible form of an income statement and is well-suited for very small businesses, sole proprietors, and informal internal reports. Its weakness is that it tells you almost nothing about why the business made or lost money — there is no way to see whether the gross margin is healthy or whether overhead is the problem.

The multi-step income statement separates operating activities from non-operating activities and calculates several intermediate subtotals: gross profit (revenue minus COGS), operating income (gross profit minus operating expenses), and finally net income (after interest, taxes, and other non-operating items). This structure is preferred by lenders, investors, and CPAs because it makes margin analysis straightforward and supports comparisons across periods and against industry benchmarks.

Single-Step Best For

- Sole proprietors with simple operations

- Cash-basis bookkeeping

- Quick informal reviews

- Service businesses with no inventory

Multi-Step Best For

- Lenders, investors, and SBA loan packages

- Product businesses with COGS and inventory

- Margin analysis and benchmarking

- GAAP-compliant external reporting

P&L vs Other Financial Statements

The profit and loss statement is one of three core financial statements every business should maintain. Each answers a different question, and together they paint a complete picture of financial health.

| Document | What It Shows | Time Frame |

|---|---|---|

| P&L Statement | Revenue, expenses, and resulting profit or loss | A period (month, quarter, year) |

| Balance Sheet | Assets, liabilities, and owners' equity | A single point in time |

| Cash Flow Statement | Sources and uses of cash by activity | A period (month, quarter, year) |

| Statement of Equity | Changes in owners' equity over the period | A period (month, quarter, year) |

| Trial Balance | All ledger account balances at period end | A single point in time |

How to Create a Profit and Loss Statement

Building a clean P&L statement is a methodical process. Whether you are doing it by hand from a shoebox of receipts or pulling numbers out of accounting software, follow these eight steps to produce a statement that will hold up to lender, investor, or IRS scrutiny.

Choose Your Period and Basis

Decide whether the P&L will cover a month, quarter, or year, and whether it will be prepared on a cash or accrual basis. Note both clearly in the header so anyone reading the statement knows exactly what they are looking at.

Gather All Revenue Sources

Pull every invoice, sales receipt, deposit, and Stripe/Square statement for the period. Categorize revenue by product line, service line, or business segment so the top of the P&L tells a meaningful story.

Calculate Cost of Goods Sold

Add beginning inventory, purchases, direct labor, and freight-in, then subtract ending inventory. For service businesses, COGS becomes cost of services and includes only the direct labor and direct costs of delivering the service.

Compute Gross Profit

Subtract COGS from total revenue. This is your gross profit — the money left over to pay overhead, interest, taxes, and ultimately to keep as net income. Express it as a percentage (gross margin) and compare it to the same period last year.

List Operating Expenses

Group operating expenses into clear, consistent categories: payroll, rent, utilities, marketing, insurance, professional fees, software, depreciation, and other administrative costs. Use the same categories every period so trends are easy to spot.

Calculate Operating Income

Subtract total operating expenses from gross profit. The result — operating income or EBIT — measures the profitability of the core business before financing decisions and taxes enter the picture.

Add Non-Operating Items, Interest, and Taxes

Subtract interest expense, add interest or investment income, record any one-time gains or losses, and finally subtract income tax expense. Be careful to only include the interest portion of loan payments, never principal.

Verify and Reconcile

Tie the P&L back to your bank statement, your bookkeeping software, and your prior period for trend analysis. Net income should flow into retained earnings on the balance sheet — if it does not reconcile, there is an error to find before you share the statement.

Key Components of a P&L Statement

Every well-prepared profit and loss statement includes the following building blocks. The exact line items will vary by industry — a SaaS company will not have inventory, and a restaurant will track food cost separately from beverage cost — but the structure below applies to almost every business.

Revenue (Top Line)

All money earned from sales of goods and services during the period, broken down by product line, service line, or business segment.

Sales Returns and Allowances

Credits issued for returned merchandise, discounts, and allowances. Net revenue is gross revenue minus these contra-revenue accounts.

Cost of Goods Sold (COGS)

Direct cost of producing or acquiring whatever was sold, including raw materials, direct labor, and freight-in.

Gross Profit

Net revenue minus COGS. The single most important line for understanding product economics.

Operating Expenses

Indirect costs of running the business — payroll, rent, marketing, software, professional fees, insurance, depreciation, and administrative costs.

Operating Income (EBIT)

Gross profit minus operating expenses. Measures profitability of the core business before financing and tax decisions.

Interest Expense

Interest paid on loans, lines of credit, and other debt. Only the interest portion belongs on the P&L — principal repayments do not.

Income Tax Expense

Federal, state, and local income tax for the period, including current and deferred tax components.

Net Income (Bottom Line)

What is left after all revenue, costs, expenses, interest, and taxes. The number that flows into retained earnings on the balance sheet.

Profit Metrics Explained

The P&L produces several profit measures, and each answers a different question about business performance. Understanding the difference is essential for talking with bankers, investors, or your CPA.

Gross Profit & Gross Margin

Revenue minus COGS, expressed in dollars (gross profit) or as a percentage of revenue (gross margin). Measures how much money is left after the direct cost of producing or delivering what was sold. Healthy gross margins are highly industry-specific: SaaS often runs 75 to 85 percent, retail 25 to 40 percent, and grocery 20 to 25 percent.

Operating Income & Operating Margin

Gross profit minus operating expenses. Also called EBIT (earnings before interest and taxes). Measures whether the core business model is profitable before financing decisions and taxes enter the picture. Operating margin is operating income divided by revenue.

EBITDA

Earnings before interest, taxes, depreciation, and amortization. Often used by lenders and acquirers as a proxy for cash-generating capacity because it strips out non-cash expenses. EBITDA is not a GAAP measure and should be reconciled to net income whenever it is presented externally.

Net Income & Net Margin

The very bottom of the P&L — what is left for owners after every cost, every expense, all interest, and all taxes. Net margin is net income divided by revenue. It is the most commonly cited overall profitability number and the one that flows into retained earnings on the balance sheet.

GAAP and Accounting Standards

Generally Accepted Accounting Principles (GAAP) are the rules and conventions issued by the Financial Accounting Standards Board (FASB) that govern how U.S. financial statements are prepared. Public companies are required by SEC rules to follow GAAP, and most banks, sophisticated investors, and acquirers expect GAAP-compliant statements from any business they are evaluating. The most important GAAP principles affecting the P&L are the revenue recognition standard (ASC 606), the matching principle, accrual accounting, and the materiality and consistency principles.

Under ASC 606, revenue is recognized when the performance obligations of a contract are satisfied — not necessarily when cash is received. For example, a software company that sells an annual subscription on January 1 must recognize one-twelfth of the revenue each month rather than recording the entire amount as revenue in January. The matching principle requires expenses to be recorded in the same period as the revenue they helped generate, which is why accrual-basis accounting (and accounts payable, prepaid expenses, and deferred revenue) exists.

Small businesses are not legally required to follow GAAP for internal management reporting, and many sole proprietors use cash-basis accounting for simplicity. However, the moment the P&L will be shared with a bank, an investor, or an acquirer, GAAP compliance becomes important — and the cost of converting messy cash-basis books to GAAP late in a diligence process is much higher than maintaining GAAP-aligned books from the start.

Sample Profit and Loss Statement

Below is a condensed example of a multi-step profit and loss statement for a fictional small business covering a full fiscal year. Use it as a reference for the structure, ordering, and level of detail your own statement should include.

RIVERSIDE OUTFITTERS, LLC

Profit and Loss Statement

For the Year Ended December 31, 2025

Frequently Asked Questions

Answers to common questions about profit and loss statements, accounting standards, and how P&Ls are used by lenders, investors, and the IRS.

Official Resources

For authoritative information on income statement preparation, accounting standards, and small business financial reporting, consult these official and industry resources.

SBA - Manage Your Finances

Small Business Administration guide to financial statements and bookkeeping

IRS - Schedule C (Form 1040)

Profit or loss from business for sole proprietors — instructions and form

FASB - Accounting Standards

Financial Accounting Standards Board — official source of U.S. GAAP

AICPA - Resources

American Institute of CPAs — professional accounting standards and guidance

SEC EDGAR - Filings

Search public company income statements and 10-K filings for benchmarks

SCORE - Financial Statements

Free SCORE templates and mentoring for small business financial reporting

IRS Publication 334

Tax Guide for Small Business — income, expenses, and accounting methods

BLS - Industry Statistics

Bureau of Labor Statistics data for benchmarking labor cost as a percentage of revenue

Create your Profit and Loss Statement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.