What Is a Merger Agreement?

A merger agreement is the definitive contract that governs the combination of two companies into a single entity. When two businesses merge, one company (the target) ceases to exist, and its assets, liabilities, contracts, permits, and employees transfer to the other company (the surviving entity) by operation of law. The merger agreement sets the terms of that combination: what the target's shareholders receive, what conditions must be met before closing, what each party promises about its business, and what happens if the deal falls apart.

Mergers are one of the most complex transactions in corporate law. Even a small-company merger involves corporate governance approvals (board resolutions and shareholder votes), regulatory compliance (antitrust filings, industry-specific approvals), financial due diligence, legal due diligence, tax structuring, employment considerations, and contract assignment issues. The merger agreement is the document that ties all of these threads together into a binding transaction.

The merger process typically follows a sequence: letter of intent, due diligence, negotiation and execution of the definitive merger agreement, satisfaction of closing conditions (including regulatory approvals and shareholder votes), and closing. Between signing and closing, the target operates under interim operating covenants that restrict significant business changes. The period between signing and closing can range from a few weeks for simple private company mergers to several months for transactions requiring regulatory review.

Our templates are designed for private company mergers where two closely held businesses combine operations. For public company mergers subject to SEC proxy rules and tender offer regulations, retain specialized M&A counsel.

Full Combination

Assets, liabilities, contracts, and employees transfer by operation of law

Closing Conditions

Regulatory approvals, shareholder votes, and accuracy of representations protect both sides

Post-Closing Protection

Indemnification, escrow holdbacks, and purchase price adjustments allocate post-closing risk

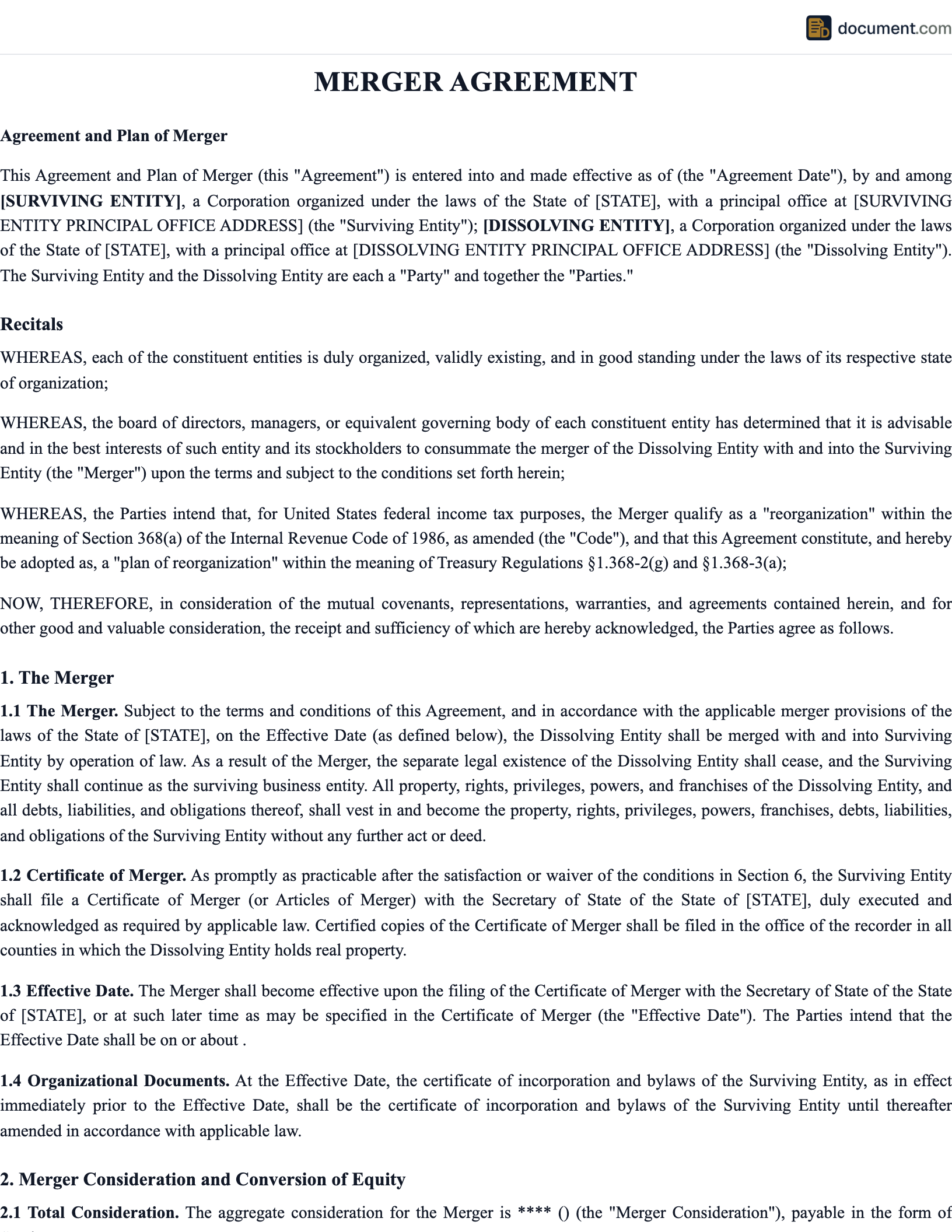

Merger Agreement Form Preview

Preview of the core sections in our merger agreement template.

Agreement and Plan of Merger

Private Company Merger

Section 1: Parties

Section 2: Merger Consideration

Cash Consideration: $4,200,000

Escrow Holdback: 10% held for 18 months

Working Capital Adjustment: Dollar-for-dollar above/below target

Section 3: Surviving Entity

Types of Mergers

Mergers come in several structural variations, each with different legal, tax, and practical implications.

Forward Merger

The target company merges into the acquiring company, and the target ceases to exist. The acquiring company is the surviving entity and takes on all of the target's assets, liabilities, contracts, and employees by operation of law. This is the simplest merger structure and is commonly used when the buyer wants to absorb the target's operations entirely. The target's shareholders receive the merger consideration (cash, stock, or a combination) in exchange for their shares.

Reverse Merger

The acquiring company merges into the target company, and the acquiring company ceases to exist. The target is the surviving entity. Reverse mergers are used when the target holds valuable contracts, licenses, permits, or regulatory approvals that would be difficult to transfer or reassign. By keeping the target as the surviving entity, those assets remain undisturbed. Reverse mergers are also used by private companies seeking to go public by merging into a publicly listed shell company, although regulatory scrutiny of this practice has increased.

Triangular Merger

The buyer forms a subsidiary, and the subsidiary merges with the target. In a forward triangular merger, the target merges into the subsidiary and the subsidiary survives. In a reverse triangular merger, the subsidiary merges into the target and the target survives as a wholly owned subsidiary of the buyer. Triangular mergers are popular because they insulate the buyer's parent company from the target's liabilities, preserve the target's contracts (in a reverse triangular merger), and can qualify for tax-free reorganization treatment under IRC Section 368(a)(2)(D) or (E).

How to Create a Merger Agreement: 8 Steps

Building a merger agreement requires working through the deal's structure, economics, conditions, and risk allocation in a logical sequence.

Choose the Merger Structure

Decide whether this will be a forward merger, reverse merger, or triangular merger. The structure affects which entity survives, how liabilities transfer, the tax treatment, and whether third-party consents are required for contract assignments. Consult with tax counsel before committing to a structure because the difference between a taxable and tax-free merger can be worth millions in shareholder-level taxes.

Define the Merger Consideration

Specify what the target's shareholders will receive: cash, stock of the surviving or parent company, promissory notes, contingent consideration (earnouts), or a combination. Set the exchange ratio for stock deals. Address fractional shares. For deals with earnouts, define the performance metrics, measurement period, accounting methodology, and dispute resolution for earnout calculations.

Draft Representations and Warranties

Each party makes factual statements about its business that the other party relies on. The target's representations typically cover corporate standing, capitalization, financial statements, material contracts, litigation, tax compliance, employee matters, environmental issues, IP, and regulatory compliance. Qualify representations with disclosure schedules that list known exceptions. Negotiate materiality qualifiers and the material adverse effect definition carefully.

Set Closing Conditions

List the conditions that must be satisfied before either party is obligated to close: shareholder approval, regulatory clearances (Hart-Scott-Rodino filing for deals above the reporting threshold), accuracy of representations (subject to the MAE qualifier), compliance with pre-closing covenants, absence of legal proceedings blocking the merger, receipt of third-party consents, and delivery of closing documents.

Negotiate Pre-Closing Covenants

Between signing and closing, the target must operate its business in the ordinary course. Define what the target can and cannot do without the buyer's consent: no new debt, no material contracts, no changes to employee compensation, no acquisitions, no dividends, no amendments to organizational documents. The buyer agrees to use reasonable best efforts to obtain regulatory approvals and not to take actions that would jeopardize the closing.

Address Employee Matters

Specify how employees will be treated after closing: will they receive comparable compensation and benefits for a defined period? How will outstanding equity awards be handled? Will there be a severance program for employees who are terminated within a specified period after closing? Address WARN Act compliance if layoffs are anticipated. Identify key employees who must sign retention or employment agreements as a condition to closing.

Build the Indemnification Framework

After closing, the buyer needs a remedy if the target's representations turn out to be false or if pre-closing liabilities surface. Structure the indemnification with a survival period for representations (typically 12 to 24 months, longer for fundamental representations), a deductible or basket (the buyer absorbs the first dollar amount of losses), a cap on the seller's indemnification liability (often 10% to 20% of the purchase price), and an escrow holdback to fund indemnification claims.

Include Termination and Breakup Provisions

Specify the circumstances under which either party can terminate the agreement before closing: mutual consent, failure to close by the outside date, material breach of representations or covenants, failure to obtain shareholder or regulatory approval. Address breakup fees payable by the target if its board changes its recommendation or accepts a superior proposal, and reverse breakup fees payable by the buyer if it fails to close due to financing or regulatory failure.

Key Components

A comprehensive merger agreement covers all of these elements.

| Component | Description |

|---|---|

| The Merger | Structure, surviving entity, and effective time of the merger |

| Merger Consideration | Cash, stock, notes, earnouts, and the exchange mechanism |

| Closing Mechanics | Closing date, location, deliverables, and funds flow |

| Representations and Warranties | Factual statements about each party's business and legal standing |

| Pre-Closing Covenants | Ordinary course obligations and restrictions between signing and closing |

| Closing Conditions | Conditions precedent to each party's obligation to close |

| Employee Matters | Compensation continuity, equity treatment, severance, and WARN compliance |

| Tax Matters | Tax treatment of the merger, pre-closing tax returns, and tax indemnification |

| Indemnification | Survival periods, baskets, caps, escrow, and claims procedures |

| Termination | Termination rights, outside date, breakup fees, and reverse breakup fees |

| Non-Competition | Post-closing restrictions on the selling shareholders |

| Disclosure Schedules | Exceptions to representations organized by section |

| Governing Law | Choice of law and dispute resolution (typically Delaware for corporate mergers) |

Legal Requirements and Considerations

Mergers involve corporate, tax, antitrust, employment, and sometimes securities law considerations. These are the key regulatory requirements.

Shareholder Approval Requirements

State corporate statutes typically require the boards of both companies to approve the merger agreement and the shareholders of the target company to approve it by at least a majority vote (some states and organizational documents require a supermajority). In a short-form merger (where the parent owns 90% or more of the subsidiary), shareholder approval of the subsidiary's minority shareholders may be unnecessary under most state statutes. Delaware General Corporation Law Section 251 governs the merger approval process for Delaware corporations and is the most commonly referenced statute.

Antitrust and HSR Filing

The Hart-Scott-Rodino Antitrust Improvements Act requires parties to certain mergers and acquisitions to file notification with the FTC and DOJ and observe a waiting period (typically 30 days) before closing. HSR filing is required when the transaction meets certain size-of- transaction and size-of-person thresholds, which are adjusted annually. For transactions reported in 2024, the size-of-transaction threshold is approximately $111.4 million. Failure to file when required can result in penalties of over $50,000 per day.

Appraisal Rights

In most states, shareholders who dissent from a merger have appraisal rights: the right to have a court determine the "fair value" of their shares and receive cash payment instead of the merger consideration. Appraisal rights are significant in private company mergers where minority shareholders may believe the merger consideration undervalues the company. Delaware's appraisal statute (DGCL 262) has generated extensive case law on valuation methodology. The merger agreement should address appraisal rights, including how dissenting shares will be treated and the buyer's right to terminate if too many shareholders seek appraisal.

Tax Considerations

- Taxable vs Tax-Free: A merger can be structured as a taxable transaction (target shareholders recognize gain) or as a tax-free reorganization under IRC Section 368 (target shareholders defer gain by receiving buyer stock).

- Section 338(h)(10): In certain stock acquisitions, the parties can elect to treat the transaction as an asset sale for tax purposes, giving the buyer a stepped-up basis in the target's assets.

- Pre-Closing Tax Returns: The merger agreement should allocate responsibility for filing pre-closing tax returns, cooperating in tax audits, and indemnifying for pre-closing tax liabilities.

Sample Merger Agreement

Condensed preview of our merger agreement template.

AGREEMENT AND PLAN OF MERGER

[Company A] and [Company B]

This Agreement and Plan of Merger is entered into between[Acquiring Company] and[Target Company].

1. THE MERGER

At the Effective Time, Target shall merge with and into Acquiror, with Acquiror continuing as the surviving entity. The separate corporate existence of Target shall cease.

2. MERGER CONSIDERATION

Each outstanding share of Target common stock shall be converted into the right to receive[$] in cash, subject to the escrow holdback and working capital adjustment described herein.

3. CLOSING CONDITIONS

The obligations of the parties to consummate the Merger are subject to the satisfaction of the conditions set forth in Article VII, including shareholder approval, regulatory clearance, and the accuracy of representations.

4. INDEMNIFICATION

The Sellers shall indemnify Acquiror for losses arising from breaches of representations, warranties, and covenants, subject to the basket, cap, and survival limitations set forth in Article IX.

Frequently Asked Questions

Common questions about merger agreements, closing conditions, and deal structure.

Official Resources

Authoritative sources on merger law, antitrust, and corporate governance.

Delaware General Corporation Law

DGCL merger statutes (Sections 251-264) governing corporate mergers and consolidations

FTC Premerger Program

Hart-Scott-Rodino filing requirements, thresholds, and premerger notification guidance

DOJ Antitrust Division

Department of Justice merger review guidelines and enforcement actions

SEC Corporate Finance

SEC guidance on proxy statements, tender offers, and going-private transactions

IRS Corporate Tax

Tax guidance on reorganizations, Section 368, and Section 338 elections

ABA M&A Committee

American Bar Association resources on mergers and acquisitions practice

Create your Merger Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.