What Is a Gift Affidavit?

A gift affidavit is a sworn written statement, signed in front of a notary public, in which the donor and donee of property formally declare that the transfer is a true gift made for no consideration. The affidavit identifies the donor, the donee, the family relationship between them (if any), and the property being given, and it creates a legal record that supports state sales tax exemptions, DMV title transfers, federal gift tax reporting, and capital gains basis tracking. By far the most common use of the gift affidavit is to transfer a vehicle from one family member to another without paying state sales or use tax.

The donor is the person giving the property. The doneeis the person receiving it. Consideration is the legal term for anything of value exchanged for the property — money, the assumption of a loan, services rendered, or other property. A true gift is a transfer for no consideration: the donor parts with the property freely, expecting nothing in return except possibly nominal love and affection. The affidavit specifically requires the parties to swear that no consideration was exchanged, which exposes them to perjury liability and prevents abuse of the family-relationship sales tax exemption.

Most states publish their own gift affidavit forms for vehicle transfers — for example, Texas Comptroller Form 14-317 (Affidavit of Motor Vehicle Gift Transfer), Pennsylvania DOT Form MV-13 (Affidavit of Gift), Maryland MVA Form VR-103 (Gift Certification), Virginia DMV Form SUT3 (Purchaser's Statement of Tax Exemption), and California DMV Form REG 256 (Statement of Facts). Our templates incorporate the language and structure of these state forms while remaining flexible enough to document gifts of real estate, jewelry, household goods, and other personal property.

The federal gift tax angle is also important. Although the donor (not the donee) is technically responsible for federal gift tax, most family gifts fall well below the annual exclusion amount ($19,000 per donee in 2025) and create no actual tax liability or filing obligation. Larger gifts must be reported on IRS Form 709, but no tax is owed unless the donor has used up the lifetime exemption (currently $13.99 million per individual). The gift affidavit serves as the contemporaneous record of the transfer for both the donor and the donee.

Whether you are a parent gifting a college graduate their first car, a spouse transferring jointly-owned property to their partner, a grandparent passing down a cherished family heirloom, or an adult child receiving an inherited vehicle from a parent, our state-specific gift affidavit templates include the donor and donee disclosures, no-consideration recitals, family-relationship attestations, and notarization language every state DMV and county clerk accepts.

DMV Title Transfer

Transfer a vehicle to a family member without state sales tax

Tax Documentation

Support state exemptions and federal Form 709 reporting

Family Transfers

Memorialize gifts between spouses, parents, children, and siblings

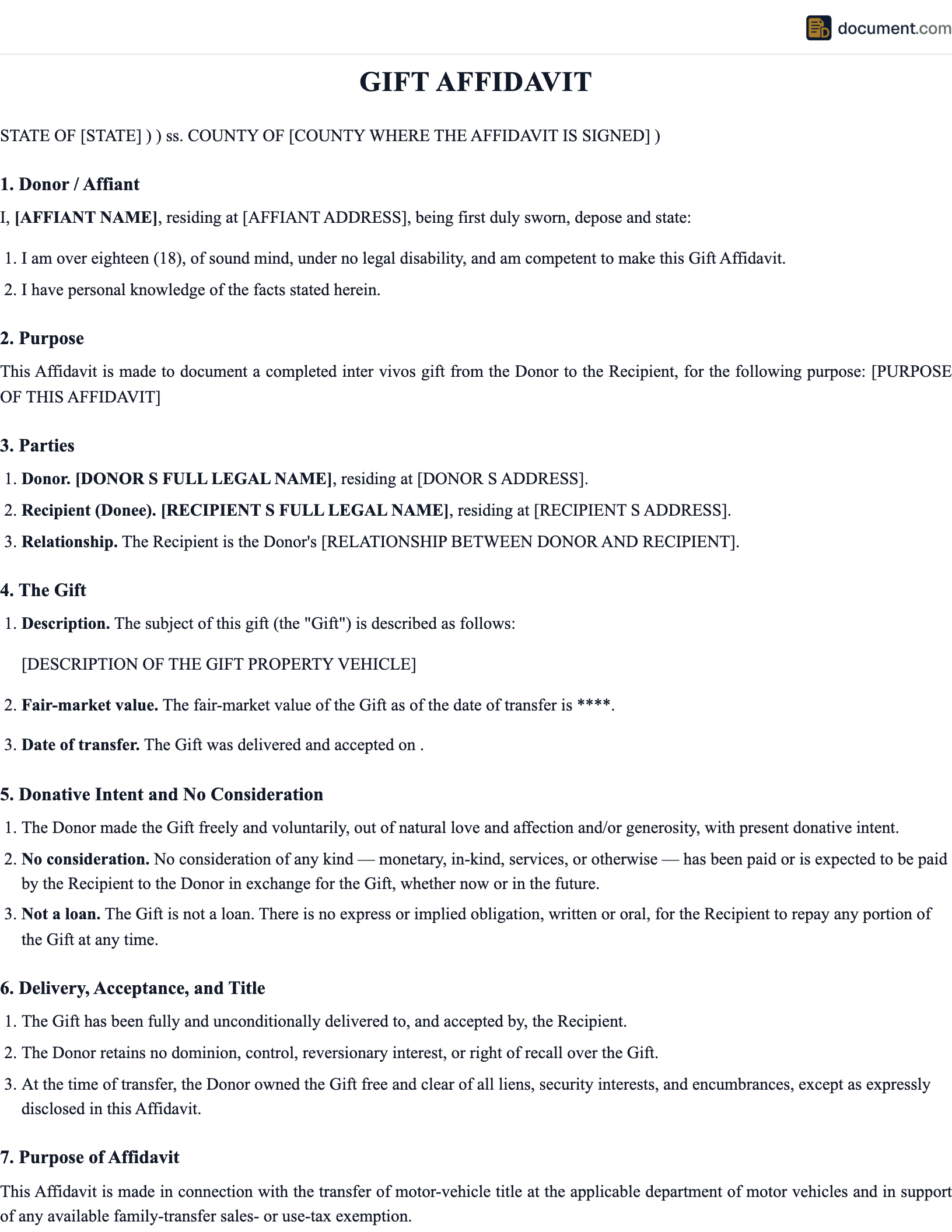

Gift Affidavit Form Preview

Below is a preview of a complete vehicle gift affidavit. Your final document will be customized for the specific donor, donee, family relationship, and property being gifted.

Gift Affidavit

Affidavit of Motor Vehicle Gift Transfer

Section 1: Donor (Person Giving the Gift)

Section 2: Donee (Person Receiving the Gift)

Section 3: Property Being Gifted

Section 4: Sworn Declarations

1. The transfer of the vehicle described above is a true gift.

2. No consideration of any kind has been exchanged.

3. The donor and donee are parent and child as defined by Texas Tax Code Section 152.025.

4. The gift qualifies for exemption from Texas motor vehicle sales and use tax.

5. There is no outstanding lien against the vehicle, or the lien has been satisfied as of the date of this affidavit.

Section 5: Signatures and Notarization

Donor Signature

Donee Signature

Notary Public

When to Use a Gift Affidavit

The gift affidavit is the right tool whenever a donor and donee need to formally document a no-consideration transfer of property — most often a vehicle, but sometimes real estate, jewelry, household goods, or financial accounts.

Gifting a vehicle to a family member

Parent to child, spouse to spouse, sibling to sibling, or grandparent to grandchild. The gift affidavit is required by state DMVs to qualify for the family-relationship sales tax exemption and to complete the title transfer.

Transferring real estate as a gift

When a parent deeds a home to a child, the gift affidavit accompanies the deed to memorialize that no consideration was paid, support the family transfer tax exemption, and establish the donee's basis for capital gains purposes.

Documenting a large gift for IRS purposes

Gifts above the federal annual exclusion ($19,000 per donee in 2025) must be reported on IRS Form 709. The gift affidavit creates a contemporaneous record of the transfer, the parties, and the value.

Transferring an inherited vehicle to a beneficiary

When a vehicle passes from a deceased parent to an adult child by intestacy or under a will, the gift affidavit (combined with a small estate affidavit or letters testamentary) can support a tax-free DMV title transfer in most states.

Wedding or graduation gifts of significant value

Newlyweds receiving a car from parents, college graduates receiving a vehicle as a graduation gift, or family members receiving heirlooms can use the affidavit to document the transfer for both tax and insurance purposes.

Charitable contributions of vehicles

Although charities provide their own donation forms, some states still require a gift affidavit to support the tax-exempt title transfer to the charity at the DMV.

Wrong tool when: any consideration is being exchanged (use a bill of sale instead), the parties are not actually related and the state exemption requires a family relationship, or the property is real estate that requires a recorded deed (use a quitclaim or warranty deed; the gift affidavit supports but does not replace the deed).

Gift Affidavit vs Other Documents

The gift affidavit overlaps with several closely related documents. Each addresses a different need.

Gift Affidavit vs Bill of Sale

Gift Affidavit

- - No consideration exchanged

- - Used for family transfers

- - Qualifies for sales tax exemption

- - Sworn under oath

Bill of Sale

- - Documents an actual sale

- - Shows the purchase price

- - Used to calculate sales tax

- - Contractual, not sworn

Gift Affidavit vs Gift Letter for Mortgage

Gift Affidavit

- - Used for property transfers (cars, real estate, goods)

- - Sworn before a notary

- - Submitted to DMV or recorder

- - Establishes tax exemption

Gift Letter for Mortgage

- - Used for cash gifts toward a down payment

- - Signed by donor; no notary in most cases

- - Submitted to mortgage lender

- - Documents that the cash is a true gift

Gift Affidavit vs Quitclaim Deed

Gift Affidavit

- - Sworn statement about the gift

- - Supports the deed

- - Establishes tax exemption

- - Does not transfer title by itself

Quitclaim Deed

- - Operative transfer instrument

- - Recorded in deed records

- - Actually moves title to the donee

- - Often paired with a gift affidavit

How to Create a Gift Affidavit

Preparing a state-compliant gift affidavit takes about ten minutes if you have the necessary information ready. Follow these eight steps.

Confirm the Family Relationship Qualifies

Look up your state's gift exemption statute (Texas Tax Code Section 152.025, California R&T Code Section 6285, Pennsylvania Title 75 Section 1101, etc.) and confirm that the donor and donee fall within the qualifying relationships. Most states allow spouse, parent/child, grandparent/grandchild, and sibling. Some allow in-laws and step-relations; some do not. If the relationship doesn't qualify, sales tax will apply.

Gather Property Information

For a vehicle: year, make, model, VIN, current odometer reading, and fair market value (use the most recent NADA or Kelley Blue Book value, or your state's assessed value). For real estate: legal description, address, APN, and fair market value (recent appraisal or county assessment). For other property: a clear description and a defensible value.

Verify No Consideration Is Being Exchanged

Confirm that the donee will not pay anything for the property, will not assume any loan against it, will not perform services in exchange, and is not trading other property. If any consideration exists, the transfer is a sale and a bill of sale (not a gift affidavit) is the right document.

Check for Liens

If there is a loan against the vehicle or real estate, the lien must typically be satisfied (or the lender must consent) before the property can be gifted. The gift affidavit usually requires the donor to swear that no outstanding lien exists, so the loan must be paid off first.

Use the Right State Form

Most states publish their own gift affidavit form for vehicles (Texas 14-317, Pennsylvania MV-13, Maryland VR-103, Virginia SUT3, California REG 256). For real estate and other property, a generic gift affidavit usually works. Use the state form whenever one exists.

Both Parties Sign Before a Notary

Both the donor and the donee typically sign the affidavit in front of a notary public. Bring valid government-issued photo ID for both signers. Some states allow signing at the DMV counter in front of a DMV employee instead of a notary.

Submit to the DMV (or Recorder)

For a vehicle gift, take the signed and notarized affidavit, the signed-over title, the application for title and registration, proof of insurance, and the title transfer fee to the DMV. For a real estate gift, attach the affidavit to the deed and submit both to the county recorder.

Consider Federal Gift Tax Reporting

If the value of gifts to a single donee in a single year exceeds $19,000 (2025 annual exclusion), the donor must file IRS Form 709 by April 15 of the following year. No tax is owed unless the lifetime exemption ($13.99 million per individual in 2025) has been exhausted, but the filing is mandatory. Keep a copy of the gift affidavit with your tax records.

Key Components of a Gift Affidavit

Every state-compliant gift affidavit contains the same essential elements.

Donor Identification

Full legal name, address, driver's license number, and contact information.

Donee Identification

Full legal name, address, driver's license number, and date of birth.

Family Relationship

Specific qualifying relationship (spouse, parent, child, sibling, grandparent, grandchild).

Property Description

For a vehicle: year, make, model, VIN, mileage. For other property: complete description.

Fair Market Value

Defensible valuation from KBB, NADA, recent appraisal, or county assessment.

No-Consideration Recital

Sworn statement that no money, services, or other value was exchanged.

Lien Disclosure

Statement that no outstanding lien exists or that the lien has been satisfied.

Notarization

Both donor and donee signatures, with notarial certificate, seal, and commission expiration.

Federal Gift Tax Rules

Understanding the federal gift tax framework prevents surprises and ensures the gift affidavit is properly supported by IRS reporting.

The Annual Gift Tax Exclusion

Under IRC Section 2503(b), each donor may give up to the annual exclusion amount to each donee each year without any gift tax filing or liability. The exclusion is adjusted periodically for inflation: $17,000 in 2023, $18,000 in 2024, and $19,000 in 2025. A married couple may elect to split gifts and combine their exclusions for a total of $38,000 per donee per year. Most family vehicle gifts, routine cash gifts, and ordinary holiday gifts fall well below the exclusion.

When Form 709 Is Required

IRS Form 709 (United States Gift (and Generation-Skipping Transfer) Tax Return) must be filed by the donor whenever total gifts to any single donee in a calendar year exceed the annual exclusion. The form is due April 15 of the following year (or October 15 with an extension). Filing the form does not necessarily mean tax is owed — most filers simply use up a small portion of their lifetime exemption and pay nothing. The form is the IRS's record of the gift for purposes of estate tax reconciliation.

Lifetime Exemption

Under IRC Section 2010, each individual has a lifetime exemption from federal estate and gift tax. The exemption is currently $13.99 million per individual ($27.98 million per married couple) in 2025, but it is scheduled to revert to approximately $7 million per individual on January 1, 2026 unless Congress acts. Gifts above the annual exclusion use up the lifetime exemption dollar-for-dollar. Until the lifetime exemption is exhausted, no actual gift tax is owed even on very large gifts — only the filing requirement.

Donee's Basis

When property is gifted, the donee generally takes the donor's basis (the donor's original cost) for purposes of calculating capital gains if the donee later sells the property. This is called "carryover basis" and it differs from the "stepped-up basis" rule that applies when property passes at death. For a vehicle gift, the carryover basis usually doesn't matter because vehicles depreciate. For real estate gifts, however, carryover basis can have significant tax consequences when the donee eventually sells, because the donee inherits the donor's low purchase price and pays capital gains on the full appreciation.

Sample Gift Affidavit

Below is a condensed preview of our gift affidavit template. Your final document will use the specific state form (Texas 14-317, Pennsylvania MV-13, etc.) where available, or this generic version for property types and states without a dedicated form.

GIFT AFFIDAVIT

Sworn Declaration of Gift Transfer

STATE OF [State] COUNTY OF [County]

We, the undersigned Donor and Donee, being first duly sworn upon oath under penalty of perjury, depose and state:

1. PARTIES

Donor: [Donor Name], residing at [Address].

Donee: [Donee Name], residing at [Address].

2. RELATIONSHIP

The Donor and Donee are [Relationship], which qualifies as an immediate family relationship under [Statute Cite].

3. PROPERTY

[For a vehicle: year, make, model, VIN, mileage. For other property: complete description.]

Fair Market Value: [$Value] based on [Source].

4. NO CONSIDERATION

The transfer of the property described above is a true and complete gift. No money, services, assumption of debt, or other consideration of any kind has been or will be exchanged between the Donor and the Donee.

5. NO LIENS

To the best of the Donor's knowledge, there are no outstanding liens, encumbrances, or claims against the property.

6. EXEMPTION

The Donor and Donee request that this transfer be treated as exempt from state sales or use tax under the family-relationship exemption applicable in the State of [State].

7. TRUTHFULNESS

The statements above are true and correct. We understand that knowingly false statements may subject us to criminal penalties for perjury, civil tax liability, and additional state penalties.

Subscribed and sworn to before me by both Donor and Donee on [Date].

Frequently Asked Questions

Common questions about vehicle gifts, IRS gift tax, family exemptions, and DMV requirements.

Official Resources

Authoritative sources for state DMV gift forms, federal gift tax reporting, and family transfer rules.

IRS - Gift Tax FAQs

Internal Revenue Service official guidance on federal gift tax and Form 709

IRS Form 709 - Gift Tax Return

Annual federal gift tax return required for gifts above the exclusion

Texas Form 14-317 - Motor Vehicle Gift Transfer

Official Texas Comptroller affidavit for family vehicle gifts

Pennsylvania DOT - Gifting a Vehicle

PennDOT MV-13 affidavit and gift transfer instructions

Virginia DMV - Buying or Selling a Vehicle

Virginia DMV forms and procedures including SUT3 gift exemption

California DMV - Forms

California DMV form library including REG 256 statement of facts

Kelley Blue Book

Industry-standard vehicle valuation source for gift affidavits

CFPB - Mortgage Resources

Consumer Financial Protection Bureau guidance on gifts toward home purchases

Create your Gift Affidavit in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.