What Is a Gift Letter for a Mortgage?

A mortgage gift letter is a signed statement from a person providing money to a homebuyer that confirms the funds are a true gift and will not be repaid. It is one of the most common — and most misunderstood — documents in the mortgage process. When a borrower receives money from a parent, grandparent, or other approved donor to help with a down payment or closing costs, the lender must verify that the funds are not a loan. Disguising a loan as a gift would inflate the borrower's effective debt load and violate federal underwriting standards.

Gift letters are required by Fannie Mae, Freddie Mac, the Federal Housing Administration (FHA), the Department of Veterans Affairs (VA), and the U.S. Department of Agriculture (USDA) for any portion of a borrower's funds that come from a third party. Each loan program has its own rules about who can give a gift, how much can be gifted, and what documentation is required, but every program agrees on one core principle: the funds must truly be a gift with no expectation of repayment.

In recent years, gift funds have become increasingly important as home prices have outpaced wage growth and saving a 20% down payment has become difficult for many first-time buyers. According to the National Association of Realtors, roughly 22% of first-time homebuyers receive financial help from family or friends to assemble their down payment. For those buyers, a properly drafted gift letter is the difference between a smooth closing and a last-minute underwriting denial.

A gift letter alone is rarely enough — lenders also require documentation showing that the donor had the funds available and that the funds were actually transferred to the borrower or to escrow. This process, called "sourcing and seasoning," ensures the underwriter can trace the money from the donor's account to the closing table. Borrowers who plan to use gift funds should start the documentation process early — ideally weeks before applying for the mortgage — so the gift can be properly verified without delaying the loan.

Our attorney-reviewed gift letter templates include all of the language required by major loan programs, identify the donor and recipient, state the amount and source of the funds, explicitly confirm that the gift is not a loan, and provide signature blocks for both parties. Whether you are buying a home with an FHA, VA, conventional, or USDA loan, our templates give you a clean, lender-ready document that will satisfy any underwriter.

Lender-Ready

Meets Fannie, Freddie, FHA, VA, and USDA requirements

Underwriter Approved

Includes the exact language underwriters look for

Family Friendly

Perfect for parents helping first-time homebuyers

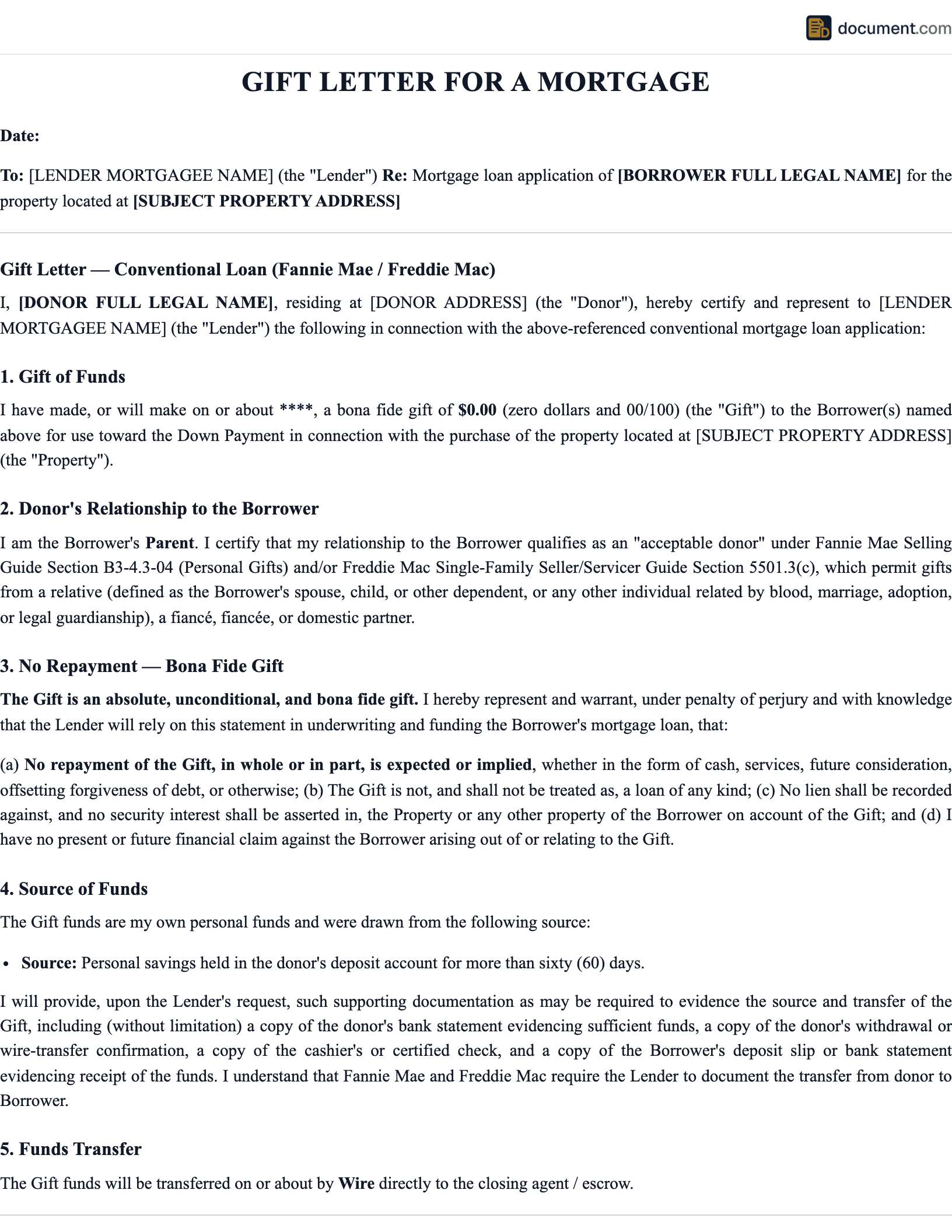

Form Preview

Our gift letter is a single-page document with all of the elements lenders require.

MORTGAGE GIFT LETTER

Date: _______________

Donor Name & Address: _____________________

Recipient Name: _____________________________

Relationship: _______________________________

Gift Amount: $_______________________________

Source of Funds: ____________________________

Property Address: ___________________________

Donor Signature: ____________________________

Recipient Signature: ________________________

Types of Mortgage Gift Letters

Different loan programs have different gift fund rules. Here are the most common types of gift letters used in residential mortgage transactions.

Conventional vs FHA vs VA Gift Rules

Each major loan program has its own gift fund rules. The table below summarizes the most important differences.

| Feature | Conventional | FHA | VA |

|---|---|---|---|

| Allowed Donors | Family only | Family, employer, friend, charity, government | Any non-interested party |

| Down Payment Coverage | Up to 100% (primary) | Up to 100% | Up to 100% |

| Donor Bank Statement | Required | Required | Required |

| Investment Property | Not allowed | Not eligible | Not eligible |

| Repayment Allowed | No | No | No |

How to Write a Mortgage Gift Letter

Follow these steps to create a lender-ready gift letter that will satisfy any underwriter.

Confirm the Loan Program

Check with your lender to confirm whether your loan is conventional, FHA, VA, USDA, or jumbo, and ask if they have a preferred gift letter format.

Identify the Donor and Recipient

Use full legal names and current addresses for both parties. The donor and the borrower's relationship must be stated clearly.

State the Gift Amount

Write the gift amount in numbers and words. If the gift covers both down payment and closing costs, you can use one letter or separate letters.

Identify the Source of Funds

Briefly describe where the funds are coming from (savings account, checking account, money market, brokerage).

Identify the Property

Include the address of the property being purchased so the underwriter can match the gift to the loan file.

Include the No-Repayment Statement

State unambiguously that the funds are a gift with no expectation of repayment, no side agreement, and no future obligation.

Sign and Date

Both the donor and the borrower should sign and date the letter. Submit the letter and supporting bank documentation to the lender as early as possible.

Key Components of a Gift Letter

Every well-drafted mortgage gift letter contains the same core elements that underwriters look for.

- Donor Information: Full name, address, phone, and relationship to the borrower

- Recipient Information: Full name and current address of the borrower

- Gift Amount: Exact amount in numbers and words

- Source of Funds: The donor's account from which the gift will be drawn

- Property Address: Full street address of the home being purchased

- No Repayment Statement: Clear, unambiguous language confirming the funds are a true gift

- Donor Signature: Handwritten signature with printed name and date

- Borrower Signature: Handwritten signature with printed name and date

Sourcing the Gift Funds

"Sourcing" means proving where the gift money came from, and "seasoning" means showing that the funds have been in the donor's account long enough to be considered legitimate. Lenders use these terms to describe the documentation chain that connects the donor's account to the closing table.

Avoid Large Unusual Deposits

Underwriters are trained to flag any large unusual deposit in the donor's or the borrower's bank account that does not appear to come from a documented source. To avoid delays, the donor should let the gift funds "season" in their account for at least 60 days before transferring, and the borrower should not deposit any large unexplained sums into their own account in the months leading up to closing.

- Donor Bank Statement: Most recent 30-60 days showing the gift amount available.

- Transfer Evidence: Wire confirmation, canceled check, or bank-to-bank transfer record.

- Borrower Deposit Receipt: Statement showing the funds entering the borrower's account.

- Direct-to-Escrow Wire: Some lenders prefer the gift to be wired directly to the closing agent.

Gift Tax Considerations

Federal gift tax law affects donors, not recipients. The IRS allows individuals to give up to a certain amount per recipient per year (the "annual exclusion") without any tax consequences. Beyond that amount, the donor may need to file Form 709 but typically does not owe any actual tax thanks to the lifetime exemption, which is currently in the multi-million dollar range.

- Annual Exclusion: $18,000 per recipient per donor (2024-2025). A married couple can together give $36,000 to one recipient.

- Lifetime Exemption: Gifts above the annual exclusion are reported on Form 709 and applied to the donor's lifetime exemption (over $13 million).

- Recipient Treatment: Recipients never pay income tax on a gift, regardless of the amount.

- State Gift Taxes: Connecticut is the only state that imposes a separate state gift tax. All other states follow federal rules.

Sample Mortgage Gift Letter

Below is a condensed preview of our mortgage gift letter template. Your finished document will be customized for your loan program, donor, and property.

MORTGAGE GIFT LETTER

Date: [Date]

To: [Lender Name]

RE: Gift of Funds for the Purchase of [Property Address]

I, [Donor Full Name], residing at [Donor Address], hereby certify that I am giving a gift of $[Amount] ([Amount in Words]) to [Borrower Name], who is my [Relationship].

SOURCE OF FUNDS

The gift funds are being drawn from my account at [Bank Name], account number ending in [Last 4]. I am attaching a recent bank statement showing the funds available.

NO REPAYMENT

I certify that this is a true gift and there is no obligation, expressed or implied, to repay these funds at any time, in any form, in cash or by future services. There is no loan agreement or side arrangement of any kind.

CERTIFICATION

I understand that this gift letter will be relied upon by the lender in underwriting the borrower's mortgage and that any false statement may be considered mortgage fraud.

Donor Signature:

Borrower Signature:

Frequently Asked Questions

Common questions about mortgage gift letters, loan program rules, sourcing of funds, and tax implications.

Official Resources

Authoritative resources from federal mortgage agencies and the IRS for borrowers using gift funds.

Fannie Mae - Selling Guide

Conventional loan underwriting standards including gift fund rules

Freddie Mac - Selling Guide

Conventional loan documentation requirements for gift funds

HUD - FHA Loan Handbook

Official FHA mortgage program rules including allowable donors

VA - Home Loan Program

Department of Veterans Affairs home loan rules

USDA - Single Family Housing

Rural Development home loan program

IRS - Gift Tax FAQ

Federal gift tax rules and the annual exclusion

CFPB - Owning a Home

Consumer Financial Protection Bureau homebuyer toolkit

NAR - Research and Statistics

National Association of Realtors data on first-time buyers and gift funds

Create your Gift Letter for a Mortgage in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.