What Is a Health Insurance Verification Form?

A health insurance verification form is a comprehensive document that healthcare providers use to confirm and record a patient's insurance coverage details before delivering medical services. The form functions as the provider's primary reference for understanding a patient's benefit structure, enabling accurate billing, proper claim submission, and transparent patient communication about expected costs. In an industry where claim denial rates average 5-10% and administrative costs consume nearly a third of healthcare spending, thorough insurance verification at the front end of the patient encounter is one of the most effective strategies for reducing revenue leakage and preventing billing disputes.

The verification process requires the provider's staff to contact the insurance carrier and systematically confirm multiple layers of coverage information. Beyond basic eligibility (whether the patient has an active policy), the verification must capture the specific benefit design that determines the patient's financial responsibility: what type of plan the patient has (HMO, PPO, EPO, POS, high-deductible), whether the provider is in or out of network, what co-payments apply to different service types, whether the deductible has been met, what coinsurance percentages apply after the deductible, whether the patient is approaching or has reached their out-of-pocket maximum, and whether the planned service requires pre-authorization from the carrier.

The Affordable Care Act and the subsequent No Surprises Act have added new dimensions to the verification process. Providers must now comply with price transparency requirements, provide good faith cost estimates to uninsured and self-pay patients, and navigate complex rules about balance billing for emergency and certain non-emergency services. These regulatory developments make thorough, documented insurance verification more important than ever — not only for revenue cycle management but for legal compliance and patient protection.

Coverage Confirmation

Verifies active coverage, plan type, and network status before treatment.

Cost Transparency

Enables accurate patient cost estimates based on verified benefit details.

Pre-Authorization

Identifies services requiring carrier approval before treatment proceeds.

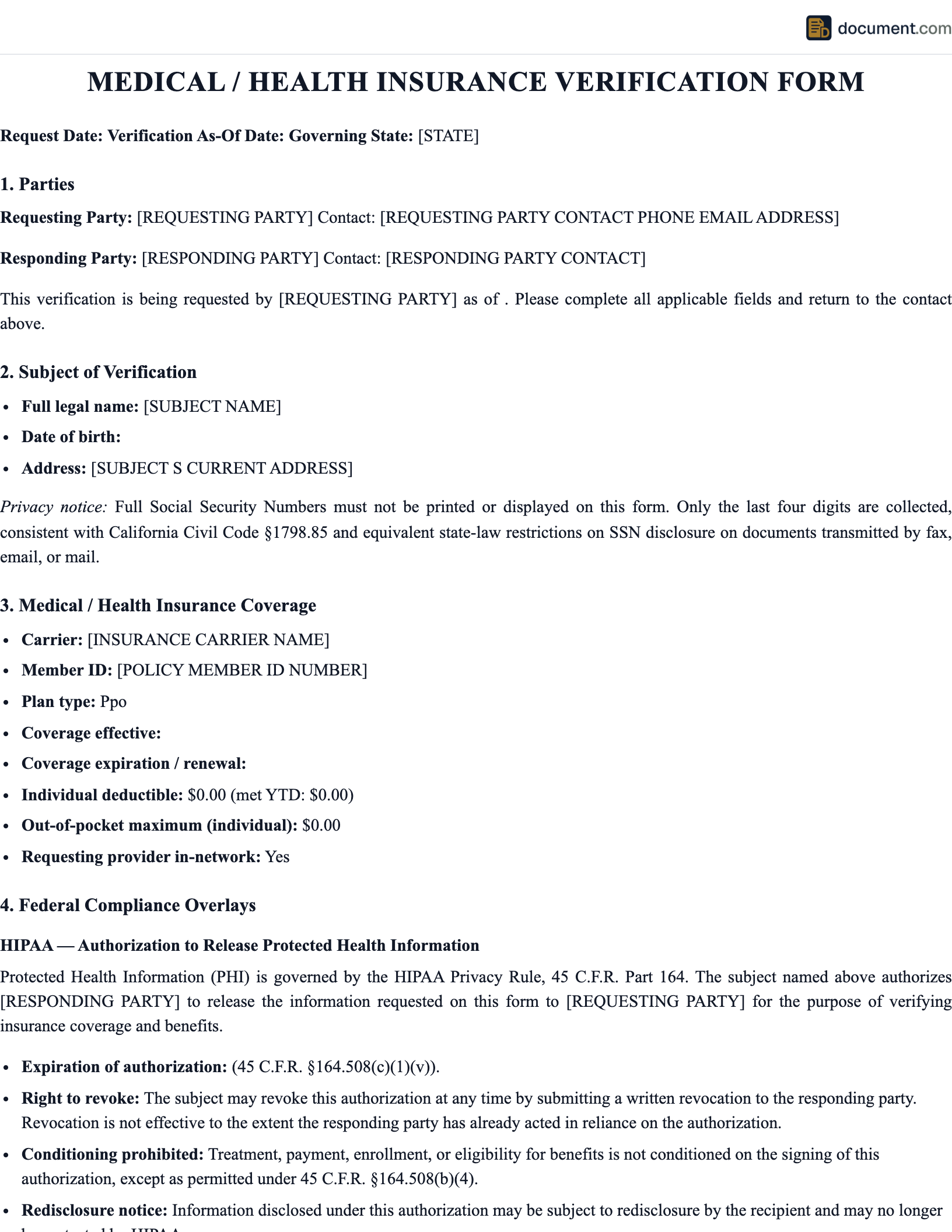

Health Insurance Verification Form Preview

Health Insurance Verification

Patient Coverage Confirmation

1. PATIENT / SUBSCRIBER INFORMATION

Patient: Member ID: Group #:

2. PLAN DETAILS

Carrier: Plan Type: Effective:

3. BENEFIT SUMMARY

Deductible: $ Met YTD: $ OOP Max: $

VERIFIED BY

CARRIER REP / REF #

Key Components

A complete health insurance verification form should capture these critical benefit elements to ensure accurate billing and patient cost communication:

| Component | Purpose | Key Details |

|---|---|---|

| Subscriber Information | Identifies the policy holder | Subscriber name, member ID, group number, DOB, relationship to patient |

| Plan Identification | Classifies the coverage type | Carrier name, plan name, plan type (HMO/PPO/EPO/POS), effective and term dates |

| Deductible Status | Calculates remaining patient responsibility | Individual/family deductible, amount met YTD, in-network vs out-of-network |

| Co-payments | Fixed patient costs per service type | PCP visit, specialist, urgent care, ER, prescription tiers |

| Coinsurance | Percentage-based cost sharing | In-network percentage, out-of-network percentage, service-specific rates |

| Out-of-Pocket Maximum | Caps patient annual spending | Individual/family OOP max, amount accumulated YTD, what counts toward max |

| Pre-Authorization | Identifies approval requirements | Services requiring prior auth, submission process, phone/fax numbers, turnaround |

How to Verify Health Insurance

Collect Insurance Card and Patient Demographics

Obtain copies of the front and back of the patient's insurance card, noting the carrier name, plan name, member ID, group number, and the provider services phone number. Record the subscriber's name, date of birth, and relationship to the patient. If the patient reports having secondary insurance, collect that information as well for coordination of benefits processing.

Contact the Carrier or Access the Provider Portal

Call the provider services number or log into the carrier's online provider portal using the practice's NPI number and credentials. Automated phone systems and online portals can provide basic eligibility confirmation, but complex verifications — particularly those involving benefit details for specific planned procedures — often require speaking with a carrier representative. Record the representative's name and the call reference number.

Verify Eligibility and Plan Type

Confirm the patient's eligibility status (active, terminated, on COBRA), the plan type (HMO, PPO, EPO, POS, HDHP), the plan's effective date and termination date (if applicable), and whether your practice is in-network for the patient's plan. For HMO plans, confirm whether the patient has designated your provider as their PCP or whether a referral from their PCP is required.

Record Deductible and Out-of-Pocket Details

Document the individual and family deductible amounts, how much has been met year-to-date, and which services the deductible applies to (many plans exempt preventive services). Record the out-of-pocket maximum, the amount accumulated year-to-date, and what expenses count toward the maximum. Note whether the plan year follows the calendar year or a different anniversary date.

Document Co-payments, Coinsurance, and Limitations

Record co-payment amounts for each service type relevant to your practice: primary care visits, specialist visits, urgent care, emergency room, diagnostic imaging, laboratory services, and prescription drug tiers. Document coinsurance percentages for both in-network and out-of-network services. Note any visit limits, annual or lifetime benefit caps, and services excluded from coverage.

Check Pre-Authorization Requirements

Determine which of the planned services require pre-authorization from the carrier. Record the pre-authorization phone and fax numbers, the information required for submission (diagnosis codes, clinical notes, supporting documentation), and the expected turnaround time for authorization decisions. For hospital admissions, determine whether inpatient notification is required within a specified timeframe and whether concurrent review will apply during the stay.

Insurance Plan Types

Understanding the patient's plan type is essential for accurate verification because each plan type has different rules about provider networks, referral requirements, and out-of-network benefits. The plan type directly affects what the patient pays and what the provider can bill.

Health Maintenance Organization (HMO) plans require patients to choose a primary care physician (PCP) who coordinates all care and provides referrals to specialists. HMO plans generally do not cover out-of-network services except in emergencies. Preferred Provider Organization (PPO) plans allow patients to see any provider without a referral but offer lower costs for in-network providers and higher costs for out-of-network providers. Exclusive Provider Organization (EPO) plans function like PPOs in that no referral is needed, but like HMOs in that they provide no out-of-network coverage except for emergencies. Point of Service (POS) plans combine HMO and PPO features — patients need a PCP and referrals like an HMO, but can go out of network at higher cost like a PPO. High-Deductible Health Plans (HDHPs) have lower premiums but higher deductibles and are typically paired with Health Savings Accounts (HSAs) or Health Reimbursement Arrangements (HRAs).

No Surprises Act Compliance

The federal No Surprises Act, effective January 2022, requires providers to give uninsured and self-pay patients a good faith estimate of expected charges before scheduled services. For insured patients, the Act protects against surprise balance billing for emergency services, non-emergency services at in-network facilities by out-of-network providers, and air ambulance services. Providers must verify insurance and network status as part of their No Surprises Act compliance workflow, and must provide proper notice and consent forms when out-of-network balance billing is permitted.

Frequently Asked Questions

Official Resources

Authoritative resources for health insurance verification, compliance, and healthcare revenue cycle management.

Centers for Medicare & Medicaid Services

Federal agency overseeing Medicare, Medicaid, CHIP, and marketplace insurance programs with provider enrollment and billing resources.

HealthCare.gov

Federal health insurance marketplace with consumer resources on plan types, coverage requirements, and enrollment periods.

CMS - No Surprises Act

Federal guidance on the No Surprises Act including provider requirements, good faith estimates, and dispute resolution processes.

America's Health Insurance Plans (AHIP)

National trade association for health insurance carriers with resources on plan design, consumer protection, and industry standards.

HHS - HIPAA Information

Department of Health and Human Services HIPAA guidance on patient privacy protections applicable to insurance verification processes.

AMA - CPT Code Resources

American Medical Association resources on CPT procedure coding essential for insurance verification and pre-authorization submissions.

Create Your Health Insurance Verification Form

Streamline patient insurance verification with a comprehensive form covering plan details, benefits, deductibles, and pre-authorization requirements.

Create DocumentNo account required. Free to create and preview.