Florida Rent-to-Own Agreement Overview

Florida does not have a specific rent-to-own statute for real property. While the state has the Florida Rent-to-Own Act (Fla. Stat. § 559.9231 et seq.), that statute governs personal property only. Real property rent-to-own transactions are governed by the Florida Residential Landlord and Tenant Act (Fla. Stat. Chapter 83, Part II) for the lease component, general contract law for the purchase option, and the Johnson v. Davis disclosure standard established by the Florida Supreme Court for property conditions.

Florida's booming housing market — with rapidly appreciating prices in metro areas like Miami, Orlando, Tampa, and Jacksonville — makes rent-to-own especially attractive for buyers who need time to build a down payment. However, Florida's unique considerations including hurricane risk, volatile property insurance, homestead exemption implications, sinkhole exposure, and prevalent HOA/COA restrictions require specialized agreement provisions not found in standard templates.

Florida is an equitable distribution state. The Florida Constitution provides one of the strongest homestead protections in the country (Art. X, § 4), which provides both property tax benefits and creditor protection. However, the homestead exemption transfers to the new owner at closing, and the property tax assessment may increase significantly when ownership changes due to the Save Our Homes cap reset.

No

Specific RTO Statute

2-5%

Option Fee Range

Case Law

Disclosure Standard

Race-Notice

Recording System

Florida Rent-to-Own Laws & Regulations

Florida regulates rent-to-own real estate transactions through its comprehensive landlord-tenant statute, case law disclosure standards, and real property recording system.

- Residential Landlord and Tenant Act (Fla. Stat. Ch. 83, Part II): Governs the lease component. No statutory security deposit cap, but strict handling rules apply (escrow, notice, return within 15-30 days). Requires 3-day notice for non-payment and 7-day notice for lease violations. Landlord must maintain habitable premises.

- Johnson v. Davis Disclosure Standard: Florida courts require sellers to disclose known material facts that affect the property's value and are not readily observable. This includes sinkholes, water intrusion, structural defects, Chinese drywall, and environmental contamination. No statutory disclosure form exists — the duty arises from case law.

- Recording Statutes (Fla. Stat. § 695.11): Florida is a race-notice recording state. Record with the county clerk of court (67 counties). Recording fees vary but are typically $10 for the first page and $8.50 for each additional page, plus a documentary stamp tax surcharge for documents that transfer an interest in real property.

- Judicial Foreclosure (Fla. Stat. Ch. 702): Florida requires judicial foreclosure through the circuit court. The process typically takes 6-12 months and includes a lis pendens filing. The tenant-buyer's recorded option may be junior to the seller's existing mortgage.

- Homestead Exemption (Fla. Const. Art. X, § 4): Provides up to $50,000 in property tax exemption for primary residences. The Save Our Homes cap limits annual assessment increases to 3%. The cap resets upon change of ownership, which can significantly increase the tax bill for the new owner.

Florida Property Insurance Crisis

Florida's property insurance market has been in crisis, with many carriers leaving the state and premiums increasing dramatically — especially in coastal areas and flood zones. Before entering a rent-to-own agreement, verify that the property is insurable at a reasonable cost. Some coastal properties may only be insurable through Citizens Property Insurance (the state's insurer of last resort) at elevated rates. The agreement should address insurance requirements, who maintains coverage, and what happens if coverage becomes unavailable or unaffordable during the option period.

How Rent-to-Own Works in Florida

Florida rent-to-own transactions require attention to hurricane risk, insurance availability, homestead implications, and HOA/COA restrictions in addition to standard lease-purchase considerations.

Property Inspection, Insurance Check, and HOA Review

Hire a licensed Florida home inspector (check for Chinese drywall, sinkhole risk, wind damage, roof condition). Verify property insurability and cost. If in an HOA/COA, review all governing documents for rental restrictions before committing

Negotiate and Execute the Agreement

Agree on purchase price, option fee, rent, rent credits, option period, maintenance (including hurricane preparation), insurance requirements, and default remedies. Address the Save Our Homes property tax cap reset at closing

Pay Option Fee and Record with County Clerk

Pay the option fee and record a memorandum of option with the clerk of court in the county where the property is located. Florida has 67 counties. Documentary stamp tax may apply to the recording

Lease Period — Build Equity Through Rent Credits

During the 1-3 year lease, pay rent with credits toward the purchase price. Explore Florida Housing Finance Corporation first-time buyer programs, including the Florida Assist and HLP programs for down payment assistance

Exercise the Option and Close

Notify the seller in writing, secure mortgage financing, and close through a Florida title company. Apply for homestead exemption with the county property appraiser. Documentary stamp tax and intangible tax apply at closing

Key Florida Rent-to-Own Agreement Terms

Florida rent-to-own agreements must address the state's unique considerations including hurricane risk, insurance challenges, homestead implications, and HOA/COA restrictions.

| Term | Florida Details |

|---|---|

| Option Fee | Typically 2-5% of purchase price. Non-refundable but credited at closing. No statutory cap in Florida |

| Purchase Price | Locked at signing or by appraisal at exercise. Factor in the Save Our Homes cap reset for property tax budgeting |

| Option Period | Usually 1-3 years. Must include specific expiration date and written exercise notice requirements |

| Monthly Rent | No rent control in Florida (state law preempts local rent control under Fla. Stat. § 166.043). Lock rent for the full term |

| Rent Credits | Not required by Florida law. When included, typically 10-25% of rent. Specify forfeiture conditions |

| Security Deposit | No statutory cap. Must be held in separate account (escrow or interest-bearing). Return 15-30 days per Fla. Stat. § 83.49 |

| Insurance | Address hurricane/windstorm, flood (if in FEMA zone), and liability insurance. Specify who maintains coverage and minimum amounts |

| Default & Forfeiture | 3-day notice for non-payment, 7-day notice for violations. Address hurricane/casualty events and HOA compliance defaults separately |

Florida Consumer Protections for Tenant-Buyers

While Florida's property disclosure requirements are less statutory than many states, several laws and programs provide meaningful protections for rent-to-own tenant-buyers.

Johnson v. Davis Disclosure Standard

Florida's landmark case established that sellers must disclose known material facts that affect the property's value and are not readily observable. This includes sinkholes, water intrusion, structural defects, Chinese drywall, and environmental contamination. While Florida doesn't require a statutory form, the duty to disclose is enforceable in court. Failure to disclose can result in rescission and damages.

Florida Deceptive and Unfair Trade Practices Act (Fla. Stat. § 501.201)

FDUTPA prohibits unfair or deceptive acts in trade or commerce. Predatory rent-to-own schemes that use misleading advertising, hidden fees, or deceptive representations may violate this Act. The Florida Attorney General enforces the statute. Consumers can bring private actions for actual damages and attorney fees.

Florida Housing Finance Corporation (FHFC)

FHFC offers first-time homebuyer programs including the Florida Assist (up to $10,000 in down payment assistance), the Homebuyer Loan Program (HLP) with below-market rates, and the Salute Our Soldiers Military Loan Program. Tenant-buyers should explore these programs during the lease period to prepare for mortgage qualification.

Sinkhole Protection (Fla. Stat. § 627.7073)

Florida law requires insurance companies to offer sinkhole coverage as an option. In known sinkhole-prone areas (particularly central Florida), this coverage is essential. The seller must disclose known sinkhole activity or testing. Rent-to-own buyers in sinkhole-prone areas should insist on a geological assessment before committing to the option fee.

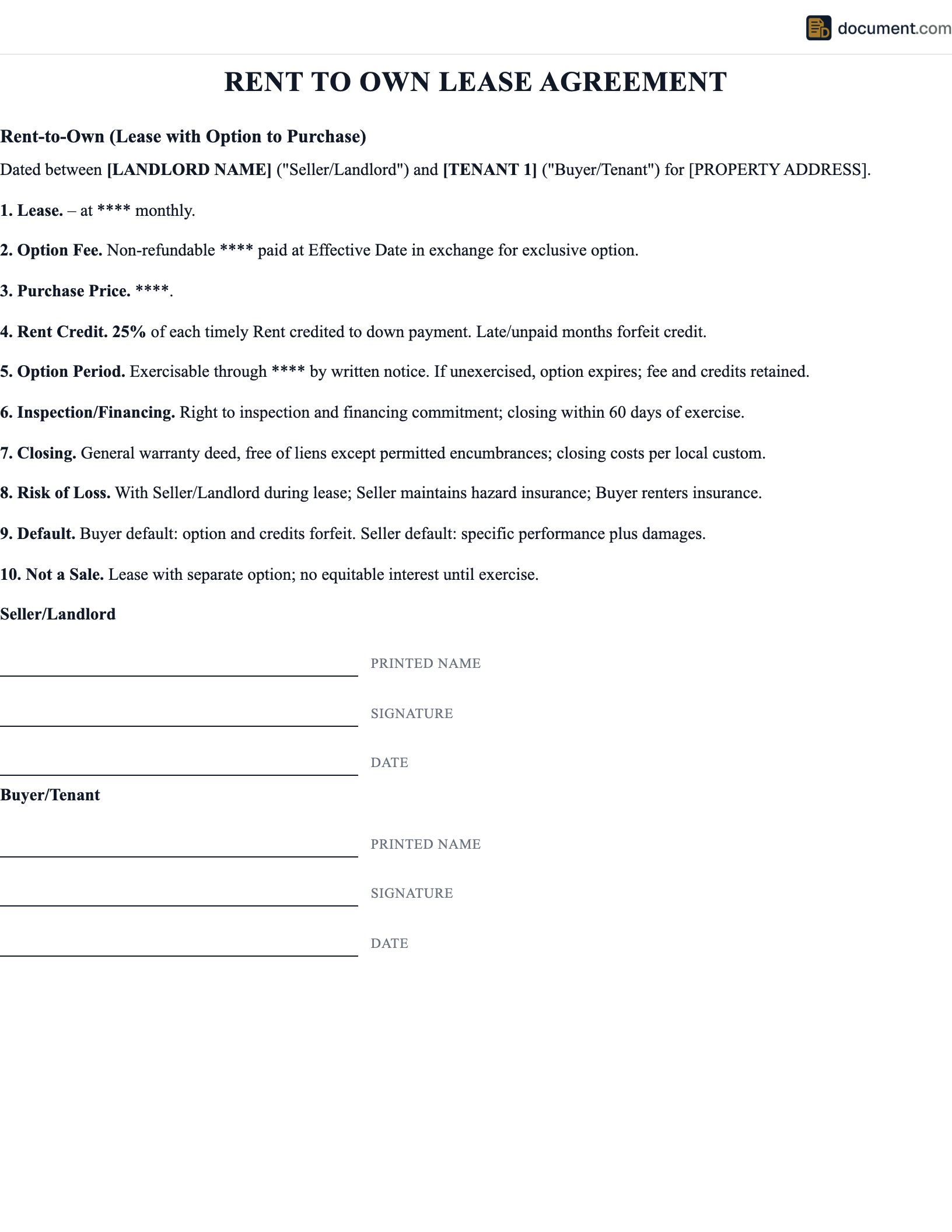

Sample Florida Rent-to-Own Agreement

Below is a preview of our Florida-specific rent-to-own agreement. The customized document addresses hurricane provisions, insurance requirements, homestead implications, and HOA/COA compliance.

STATE OF FLORIDA

RESIDENTIAL LEASE WITH OPTION TO PURCHASE

Governed by Fla. Stat. Ch. 83 & Florida Contract Law

PROPERTY OWNER / OPTIONOR:

Name: [Owner Name]

Address: [Florida Address]

TENANT-BUYER / OPTIONEE:

Name: [Tenant Name]

Address: [Current Address]

PROPERTY & TERMS

Property: [Florida Property Address]

County: [County] HOA/COA: [Yes/No]

Option Fee: $[Amount] Purchase Price: $[Amount]

Monthly Rent: $[Amount] Rent Credit: [%]%

Florida Rent-to-Own FAQ

Common questions about rent-to-own agreements in Florida, including homestead exemption, hurricane provisions, HOA restrictions, and insurance considerations.

Official Florida Resources

Government and legal resources for Florida rent-to-own transactions.

Florida Attorney General — Consumer Protection

File complaints about deceptive rent-to-own practices

Florida Department of Business and Professional Regulation — Real Estate

Real estate licensing, regulation, and consumer resources

Florida Housing Finance Corporation

First-time homebuyer programs and down payment assistance

HUD — Florida Housing Resources

Federal housing assistance, counseling, and complaint filing

Create your Florida Rent To Own Lease Agreement in under 5 minutes.

Answer a few questions and download a Florida-compliant document, ready for the state agency.