Connecticut Rent-to-Own Agreement Overview

Connecticut does not have a specific rent-to-own statute for real property. These transactions are governed by the Connecticut Landlord-Tenant Act (Conn. Gen. Stat. § 47a-1 et seq.) for the lease component, general contract law for the purchase option, and the Residential Property Condition Disclosure Act (Conn. Gen. Stat. § 20-327b) for property disclosures. Connecticut is notable for its strict security deposit escrow requirements, judicial foreclosure system, and attorney-closing mandate for real estate transactions.

Connecticut's housing market — with a high median home price particularly in Fairfield County (the Gold Coast) and the greater Hartford area — makes rent-to-own an attractive pathway for buyers who need time to build savings for a down payment. The state's older housing stock (many homes built before 1978) raises lead paint and environmental contamination concerns that must be addressed in the agreement.

Connecticut is an equitable distribution state for marital property. While not a community property state, spousal interests should still be addressed in the agreement if either party is married. The state's requirement for attorney involvement at closing provides an additional layer of legal protection for both parties.

No

Specific RTO Statute

2-5%

Option Fee Range

§ 20-327b

Disclosure Required

Race-Notice

Recording System

Connecticut Rent-to-Own Laws & Regulations

Connecticut regulates rent-to-own real estate transactions through several overlapping bodies of law, with particularly strong protections for tenants and property buyers.

- Landlord-Tenant Act (Conn. Gen. Stat. § 47a-1 et seq.): Governs the lease component. Caps security deposits at two months' rent (one month for tenants 62+). Deposits must be held in escrow and earn interest. Return within 30 days. Requires landlords to maintain habitable premises. Strict eviction procedures with judicial oversight.

- Property Condition Disclosure (Conn. Gen. Stat. § 20-327b): Requires a comprehensive disclosure covering 40+ categories. Seller can opt to credit $300 instead, but buyers should insist on full disclosure. Covers structural, environmental, flood, and neighborhood conditions.

- Recording Statutes (Conn. Gen. Stat. § 47-10): Connecticut is a race-notice recording state. Record with the town clerk in the municipality where the property is located. Connecticut uses towns (not counties) for real property recording — there are 169 towns.

- Judicial Foreclosure (Conn. Gen. Stat. § 49-17): Connecticut is a strict judicial foreclosure state. Foreclosures must go through court and typically take 6-12+ months. Connecticut also has "strict foreclosure" where the court sets a "law day" for redemption — a process unique to Connecticut.

- Attorney-Closing Requirement: Connecticut requires that a licensed attorney conduct real estate closings. When the purchase option is exercised, both the buyer and seller should have their own attorney for the closing process.

Connecticut Records by Town, Not County

Connecticut uses a town-based recording system, not a county-based one. There are 169 towns in Connecticut, and each town clerk maintains separate land records. When recording your rent-to-own option agreement, you must file with the town clerk in the specific town where the property is located. Filing in the wrong town provides no constructive notice. Recording fees vary by town but are typically $60 for the first four pages and $5 per additional page, plus a town clerk fee.

How Rent-to-Own Works in Connecticut

Connecticut rent-to-own transactions require attention to the state's strict security deposit rules, comprehensive disclosure requirements, town-based recording system, and attorney-closing mandate.

Property Inspection and Disclosure Review

Hire a licensed Connecticut home inspector. Review the Residential Property Condition Disclosure Report (insist on the full report, not the $300 credit). For pre-1978 homes, ensure lead paint testing is conducted. Check for environmental issues common in older Connecticut properties

Negotiate and Execute the Agreement

Agree on purchase price, option fee, rent, rent credits, option period, and maintenance responsibilities. Consider having a Connecticut real estate attorney review the agreement before signing. Ensure security deposit is clearly separated from option fee

Pay Option Fee and Record with Town Clerk

Pay the option fee and record a memorandum of option with the town clerk in the specific Connecticut town where the property is located. Verify the correct town before recording — Connecticut has 169 towns

Lease Period — Build Equity Through Rent Credits

During the 1-3 year lease, pay rent with a portion credited toward the purchase price. Explore CHFA (Connecticut Housing Finance Authority) first-time buyer programs and down payment assistance

Exercise the Option and Close Through Attorney

Notify the seller in writing, secure mortgage financing, and close through a Connecticut-licensed attorney. The option fee and rent credits are applied to the purchase price. The state conveyance tax (0.75%+) applies at closing

Key Connecticut Rent-to-Own Agreement Terms

Connecticut's strict tenant protection laws and attorney-closing requirement demand that the agreement be comprehensive and precisely drafted.

| Term | Connecticut Details |

|---|---|

| Option Fee | Typically 2-5% of purchase price. Non-refundable but credited at closing. Not subject to security deposit escrow rules |

| Purchase Price | Set at signing or determined at exercise. Connecticut conveyance tax (0.75%+) applies at closing |

| Option Period | Usually 1-3 years. Must include specific expiration date and exercise notice requirements |

| Monthly Rent | No statewide rent control in Connecticut, though some municipalities may have local protections. Lock rent for the full term |

| Rent Credits | Not required by Connecticut law. When included, typically 10-25% of rent. Specify forfeiture conditions clearly |

| Security Deposit | Capped at 2 months' rent (1 month for 62+). Must be held in escrow with interest. Return within 30 days. Separate from option fee |

| Maintenance | Landlord must maintain habitable premises per Conn. Gen. Stat. § 47a-7. Address older-home issues: lead paint abatement, heating systems, foundation |

| Default & Forfeiture | Connecticut requires judicial eviction. 3-day notice for non-payment, 15-day notice for lease violations. Address option fee and rent credit treatment |

Connecticut Consumer Protections for Tenant-Buyers

Connecticut provides strong consumer protections through its tenant protection laws, property disclosure requirements, and consumer fraud statutes.

Residential Property Condition Disclosure (§ 20-327b)

Connecticut requires comprehensive property disclosures covering 40+ categories including structural condition, environmental hazards (lead, radon, asbestos, underground tanks), flood zones, and neighborhood issues. Failure to disclose known material defects can result in rescission and damages. In a rent-to-own transaction, insist on the full disclosure rather than accepting the $300 credit option.

Connecticut Unfair Trade Practices Act (Conn. Gen. Stat. § 42-110a et seq.)

CUTPA prohibits unfair or deceptive acts in trade or commerce. It is one of the broadest consumer protection statutes in the country. Predatory rent-to-own schemes that use misleading advertising, hidden fees, or deceptive terms may violate CUTPA. Consumers can seek actual damages, punitive damages, and attorney fees. The Connecticut Attorney General and the Department of Consumer Protection can also pursue enforcement.

Connecticut Housing Finance Authority (CHFA)

CHFA offers first-time homebuyer programs including below-market-rate mortgages, down payment assistance (up to $20,000 in some programs), and the Teacher and Nurse Mortgage Assistance programs. Tenant-buyers should explore CHFA programs during the lease period. CHFA also provides homebuyer education courses that satisfy lender requirements.

Security Deposit Escrow and Interest (§ 47a-21)

Connecticut's strict security deposit rules protect tenant-buyers by requiring deposits to be held in escrow at a Connecticut bank and earn interest. Failure to comply entitles the tenant to double damages. These protections apply to the security deposit portion of the rent-to-own arrangement, providing an additional layer of financial protection.

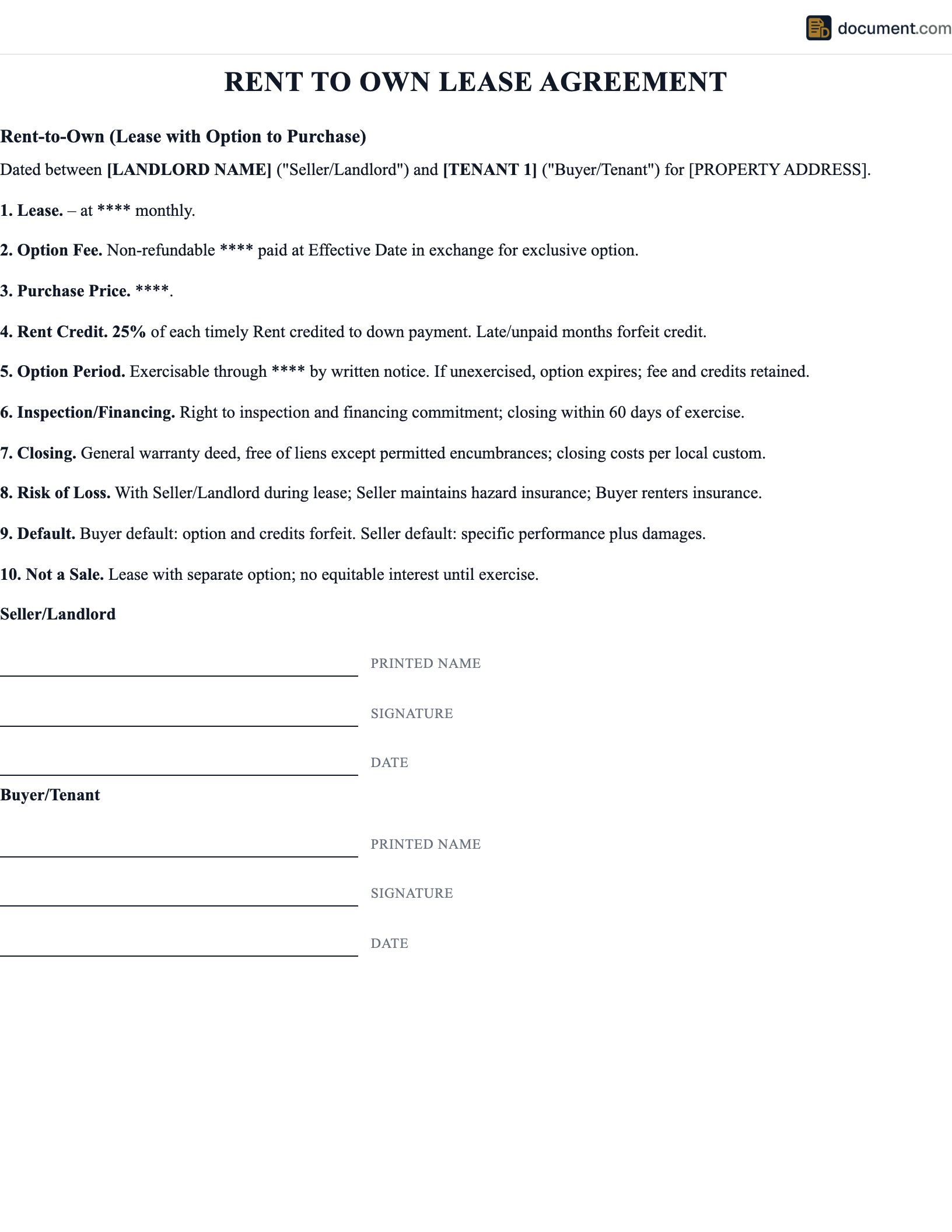

Sample Connecticut Rent-to-Own Agreement

Below is a preview of our Connecticut-specific rent-to-own agreement. The customized document addresses security deposit escrow requirements, property disclosure obligations, and town-based recording provisions.

STATE OF CONNECTICUT

RESIDENTIAL LEASE WITH OPTION TO PURCHASE

Governed by Conn. Gen. Stat. Title 47a & Connecticut Contract Law

PROPERTY OWNER / OPTIONOR:

Name: [Owner Name]

Address: [Connecticut Address]

TENANT-BUYER / OPTIONEE:

Name: [Tenant Name]

Address: [Current Address]

PROPERTY & TERMS

Property: [Connecticut Property Address]

Town: [Town] Disclosure: [Full/Credit]

Option Fee: $[Amount] Purchase Price: $[Amount]

Monthly Rent: $[Amount] Rent Credit: [%]%

Connecticut Rent-to-Own FAQ

Common questions about rent-to-own agreements in Connecticut, including security deposit escrow, property disclosures, judicial foreclosure, and attorney-closing requirements.

Official Connecticut Resources

Government and legal resources for Connecticut rent-to-own transactions.

Connecticut Department of Consumer Protection

File complaints about deceptive rent-to-own practices

Connecticut Attorney General

Consumer protection enforcement and legal guidance

Connecticut Housing Finance Authority (CHFA)

First-time homebuyer programs and down payment assistance

HUD — Connecticut Housing Resources

Federal housing assistance, counseling, and complaint filing

Create your Connecticut Rent To Own Lease Agreement in under 5 minutes.

Answer a few questions and download a Connecticut-compliant document, ready for the state agency.