Alabama Rent-to-Own Agreement Overview

Alabama does not have a dedicated rent-to-own or lease-purchase statute. Instead, these transactions are governed by a combination of general contract law, the Alabama Uniform Residential Landlord and Tenant Act (AURLTA, Ala. Code Title 35, Chapter 9A) for the lease portion, and Alabama real property law for the option-to-purchase component. Because there is no specific regulatory framework, the terms of the agreement itself are critically important in Alabama rent-to-own deals.

Alabama's approach to rent-to-own is essentially a "freedom of contract" model. Courts enforce the terms as written, provided they do not violate public policy or constitute unconscionable bargains. This means both parties have significant flexibility in structuring the deal — but it also means that a poorly drafted agreement offers little statutory protection for either side. The caveat emptor tradition remains strong in Alabama real estate, making thorough due diligence and clear documentation especially important.

It is worth noting that the AURLTA has not been adopted in all Alabama counties. In counties that have not adopted the Act, common law principles govern the landlord-tenant relationship during the lease period. The tenant-buyer should verify whether the county where the property is located has adopted the AURLTA, as this affects habitability standards, security deposit rules, and eviction procedures.

No

Specific RTO Statute

1-5%

Option Fee Range

Optional

Rent Credits

Recommended

Recording Option

Alabama Rent-to-Own Laws & Regulations

Alabama regulates rent-to-own real estate transactions through several overlapping bodies of law rather than a single comprehensive statute. Understanding which laws apply is essential for structuring an enforceable agreement.

- AURLTA (Ala. Code § 35-9A-101 et seq.): Governs the landlord-tenant relationship during the lease period in counties that have adopted the Act. Requires landlords to maintain habitable premises, limits security deposits to one month's rent, mandates a 60-day deposit return period, and establishes notice requirements for entry (two days) and eviction (7 days for non-payment).

- Alabama Statute of Frauds (Ala. Code § 8-9-2): Requires contracts for the sale of real property to be in writing. A rent-to-own agreement, because it contemplates a future real estate transfer, must be documented in a signed written instrument to be enforceable in Alabama courts.

- Recording Statutes (Ala. Code § 35-4-50 et seq.): Alabama is a "race-notice" recording state. An unrecorded option to purchase can be defeated by a subsequent bona fide purchaser who records first. Recording with the county probate office is strongly recommended to protect the tenant-buyer's interest.

- Federal Lead Paint Disclosure (42 U.S.C. § 4852d): For properties built before 1978, the seller must provide the tenant-buyer with a lead-based paint disclosure form and the EPA pamphlet "Protect Your Family From Lead in Your Home." This applies regardless of whether Alabama state law requires other property disclosures.

- Caveat Emptor: Alabama follows the caveat emptor doctrine in residential real estate sales. The seller has no general duty to disclose property defects, though actively concealing known defects constitutes fraud. Tenant-buyers should conduct thorough inspections before committing to the option fee.

AURLTA Adoption Varies by County

Not all Alabama counties have adopted the AURLTA. In non-AURLTA counties, the landlord-tenant relationship during your rent-to-own lease is governed by older common law rules, which generally provide less protection for tenants. Jefferson County (Birmingham), Madison County (Huntsville), and Mobile County have adopted the Act. Verify your county's status before entering into any rent-to-own agreement.

How Rent-to-Own Works in Alabama

Alabama rent-to-own transactions follow a straightforward process, but the lack of a specific statute means that each step must be carefully documented. Here is how a typical Alabama rent-to-own deal progresses from initial negotiation to closing.

Property Inspection and Due Diligence

Because Alabama follows caveat emptor, the tenant-buyer should hire a licensed inspector, review the title history, and verify there are no outstanding liens or encumbrances on the property before signing any agreement

Negotiate and Execute the Agreement

Both parties agree on the purchase price, option fee amount, monthly rent, rent credit percentage, option period length, maintenance responsibilities, and default remedies. The agreement must be in writing per the Alabama Statute of Frauds

Pay Option Fee and Record the Agreement

The tenant-buyer pays the non-refundable option consideration and records a memorandum of option with the Alabama county probate office. Recording fees in Alabama are typically $15-25 for the first page

Lease Period — Build Equity Through Rent Credits

During the 1-3 year lease term, the tenant pays monthly rent with a portion credited toward the purchase price. The tenant-buyer uses this time to improve credit, save for a down payment, and prepare for mortgage qualification

Exercise the Option and Close

The tenant-buyer notifies the seller in writing of intent to exercise the purchase option, secures mortgage financing, and proceeds through a standard Alabama real estate closing. The option fee and accumulated rent credits are applied to the purchase price

Key Alabama Rent-to-Own Agreement Terms

Because Alabama relies on general contract law rather than a specific rent-to-own statute, every material term must be explicitly addressed in the written agreement. Ambiguity works against the drafter in Alabama courts.

| Term | Alabama Details |

|---|---|

| Option Fee | Typically 1-5% of purchase price. Non-refundable but credited at closing. No statutory regulation — amount is purely negotiable between the parties |

| Purchase Price | Locked at signing or tied to an appraisal formula. In growing Alabama markets (Huntsville, Birmingham), locking the price protects the buyer from appreciation |

| Option Period | Usually 1-3 years in Alabama. Must include a specific expiration date. The option is not automatically extended under Alabama law |

| Monthly Rent | No rent control in Alabama. Rent is typically above market rate to accommodate the rent credit component |

| Rent Credits | Not required by Alabama law. When included, typically 10-25% of monthly rent. Specify whether credits are forfeited upon default or only upon voluntary non-exercise |

| Security Deposit | In AURLTA counties, limited to one month's rent. Must be returned within 60 days of lease termination. Separate from the option fee |

| Maintenance | Contractually determined. Many Alabama rent-to-own agreements shift routine maintenance to the tenant-buyer while the owner handles structural and major system repairs |

| Default & Forfeiture | Must specify consequences of non-payment, lease violations, and failure to exercise. Alabama courts enforce forfeiture provisions unless they are unconscionable |

Alabama Consumer Protections for Tenant-Buyers

Alabama provides relatively limited statutory protections for tenant-buyers compared to states with dedicated rent-to-own legislation. However, several legal doctrines and federal laws apply.

Unconscionability Defense

Alabama courts can refuse to enforce a rent-to-own agreement — or specific provisions — if they are found to be unconscionable at the time of contracting. This includes grossly one-sided terms, excessive option fees with no reasonable chance of mortgage qualification, or forfeiture clauses that result in unjust enrichment of the seller.

Fraud and Misrepresentation

While caveat emptor applies broadly in Alabama, the seller cannot actively conceal known material defects or make fraudulent representations about the property's condition, title status, or the terms of the agreement. Alabama's fraud statute (Ala. Code § 6-5-101) provides a cause of action for damages resulting from intentional misrepresentation.

Federal Fair Housing Act

Rent-to-own transactions in Alabama are subject to the Federal Fair Housing Act (42 U.S.C. § 3601 et seq.), which prohibits discrimination based on race, color, national origin, religion, sex, familial status, and disability. Alabama has additional state fair housing protections. Discriminatory terms in rent-to-own agreements are void and actionable.

Alabama Attorney General Consumer Protection

The Alabama Attorney General's office has authority to investigate and pursue action against deceptive trade practices under the Alabama Deceptive Trade Practices Act (Ala. Code § 8-19-1 et seq.). Predatory rent-to-own schemes that use deceptive advertising, hidden fees, or misleading terms about the likelihood of homeownership may violate this Act.

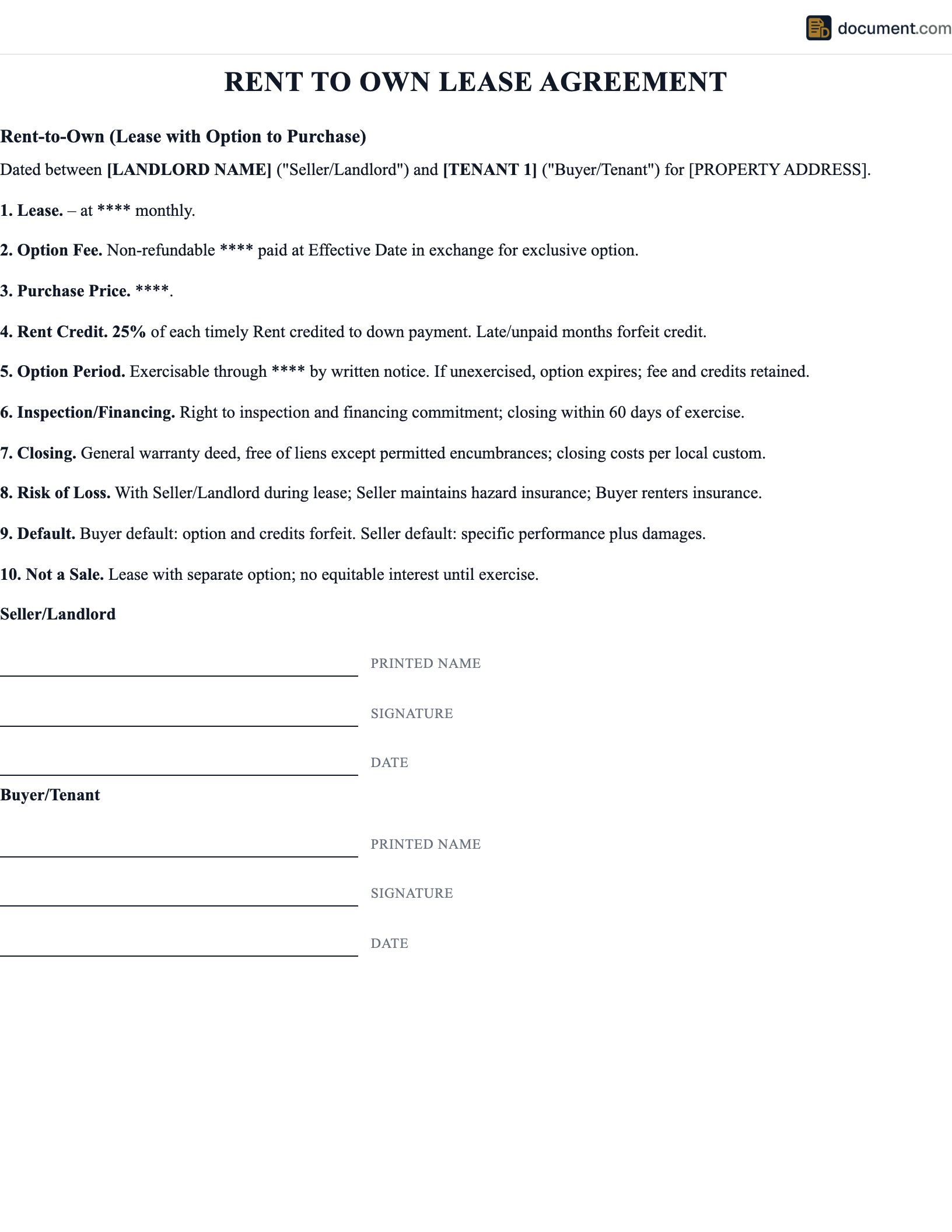

Sample Alabama Rent-to-Own Agreement

Below is a preview of our Alabama-specific rent-to-own agreement. The customized document addresses AURLTA compliance, recording provisions, and Alabama contract law requirements.

STATE OF ALABAMA

RESIDENTIAL LEASE WITH OPTION TO PURCHASE

Governed by Alabama Contract Law & AURLTA

PROPERTY OWNER / OPTIONOR:

Name: [Owner Name]

Address: [Alabama Address]

TENANT-BUYER / OPTIONEE:

Name: [Tenant Name]

Address: [Current Address]

PROPERTY & TERMS

Property: [Alabama Property Address]

County: [County] AURLTA Applies: [Yes/No]

Option Fee: $[Amount] Purchase Price: $[Amount]

Monthly Rent: $[Amount] Rent Credit: [%]%

Alabama Rent-to-Own FAQ

Common questions about rent-to-own agreements in Alabama, including AURLTA applicability, recording requirements, and caveat emptor considerations.

Official Alabama Resources

Government and legal resources for Alabama rent-to-own transactions.

Alabama Attorney General — Consumer Protection

File complaints about deceptive rent-to-own practices

Alabama Real Estate Commission

State regulatory body for real estate transactions

Legal Services Alabama

Free legal assistance for low-income Alabama residents

HUD — Alabama Housing Resources

Federal housing assistance, counseling, and complaint filing

Create your Alabama Rent To Own Lease Agreement in under 5 minutes.

Answer a few questions and download a Alabama-compliant document, ready for the state agency.