South Carolina Mortgage Deed Overview

South Carolina is a judicial foreclosure state with a distinctive court structure. Rather than routing foreclosure cases through the general civil docket, South Carolina directs them to the Master-in-Equity, a specialized judicial officer appointed in each county to handle real property matters. This means that when a borrower defaults on a South Carolina mortgage, the lender files before the Master rather than a circuit court judge, and the Master presides over the foreclosure proceeding from initial hearing through judicial sale.

Mortgage deeds are recorded with the Register of Deeds in the county where the property is located. South Carolina imposes a deed stamp tax on ownership conveyances, but mortgage instruments are generally not ownership transfers and typically are not subject to that fee. Recording fees are modest, starting around $10 for a first page. South Carolina allows deficiency judgments within two years of a foreclosure sale, giving lenders the ability to pursue borrowers for any remaining loan balance after the property is sold. The state also provides a $50,000 homestead property tax exemption for qualifying residents age 65 and older, permanently disabled, or legally blind.

$10

Recording fee

$1.85 per $500

Transfer tax

Required

Notarization

0

Witnesses required

South Carolina Requirements

South Carolina mortgage deeds must be acknowledged before a notary public and submitted to the Register of Deeds in the county where the property is located. Documents should include the complete legal description, the names and addresses of all parties, the parcel identification number, the loan amount being secured, and a return address. No additional witnesses are required beyond the notary for mortgage instruments. South Carolina has 46 counties, so confirming the correct Register of Deeds office before submission is essential.

South Carolina Specific Note

South Carolina's deed recording fee of $1.85 per $500 applies to deeds that convey ownership, not to mortgage instruments. Recording a mortgage deed does not trigger the deed stamp fee. However, confirm with the county Register of Deeds that no other local fees apply. South Carolina allows deficiency judgments against borrowers after foreclosure, and lenders have two years from the date of the foreclosure sale to bring that action. Borrowers who qualify for the $50,000 homestead property tax exemption should confirm enrollment with the county auditor, as the exemption is not automatic.

Document Requirements

- Notarization: Must be notarized by a South Carolina notary public or authorized notary

- Witnesses: South Carolina requires 0 additional witness(es)

- Legal Description: Complete legal description as it appears on the current deed of record

- Parcel Number: Assessor's parcel number or tax ID

- Return Address: Mailing address for returning the recorded document

- Formatting: Standard formatting with adequate margins, black ink, minimum 10-point font

How to File in South Carolina

Recording a mortgage deed in South Carolina follows the standard county Register of Deeds process. South Carolina closings frequently involve attorneys who handle both the closing and the recording submission, particularly for residential transactions.

Prepare the Document

Complete all required fields: the full legal names and addresses of the mortgagor and mortgagee, the complete legal description of the property as it appears in the county records, the county TMS (Tax Map Number) or parcel identification number, the amount of the loan being secured, and a return mailing address for the recorded instrument.

Notarize the Document

The mortgagor must sign before a South Carolina notary public, with valid government-issued photo ID. South Carolina does not require witnesses beyond the notary for mortgage instruments. Remote online notarization is permitted under South Carolina law for parties who cannot appear in person at closing.

Submit to the Register of Deeds

File the executed and notarized mortgage deed with the Register of Deeds in the county where the property is located. South Carolina has 46 counties, so confirm the correct county office before submitting. Many South Carolina counties accept e-recording, which is standard practice for institutional lenders and closing attorneys.

Pay the Recording Fee

Recording fees in South Carolina start at approximately $10 and are charged per page. The South Carolina deed stamp tax of $1.85 per $500 applies to ownership transfers recorded on deeds, not to mortgage instruments, so this fee generally does not apply when recording a mortgage. Confirm the current per-page recording fee with the specific county Register of Deeds.

Retain the Recorded Document

After recording, the Register of Deeds assigns an instrument number and returns the document to the address provided. Keep the recorded mortgage deed with the loan file. When the loan is satisfied, a mortgage satisfaction or release must be recorded with the same Register of Deeds to release the lien from the county's real property records.

South Carolina Fees & Costs

Typical costs for filing in South Carolina. Actual fees may vary by county.

| Fee / Tax | Amount |

|---|---|

| Recording Fee | $10 |

| Transfer Tax | $1.85 per $500 |

| Notarization | $5 - $25 per signature |

| Certified Copy | $1 - $10 per page |

| Attorney Review (optional) | $150 - $500 |

South Carolina Tax Implications

South Carolina imposes a deed recording fee, commonly called the deed stamp tax, of $1.85 per $500 of the consideration on real property ownership transfers. This tax applies when a deed conveying title is recorded. Mortgage instruments are generally not subject to this fee because they create a security interest rather than transferring title. Recording fees for mortgage documents are modest and charged per page by the county Register of Deeds.

South Carolina residents who are 65 or older, permanently disabled, or legally blind may qualify for the state's homestead property tax exemption, which reduces the assessed value of a primary residence by up to $50,000. This exemption lowers annual property tax bills but does not protect the property from mortgage foreclosure. Borrowers who believe they qualify should apply with the county auditor, as the exemption requires an application and is not automatically granted.

South Carolina allows deficiency judgments after foreclosure, and lenders have a two-year window from the date of the foreclosure sale to pursue the remaining loan balance. The deficiency amount may be reduced if the court determines the fair market value of the property at the time of sale exceeded the sale price, but this is not automatic and typically requires a hearing. Borrowers anticipating difficulty should contact a South Carolina attorney or HUD-approved housing counselor early to understand all available options before a foreclosure sale occurs.

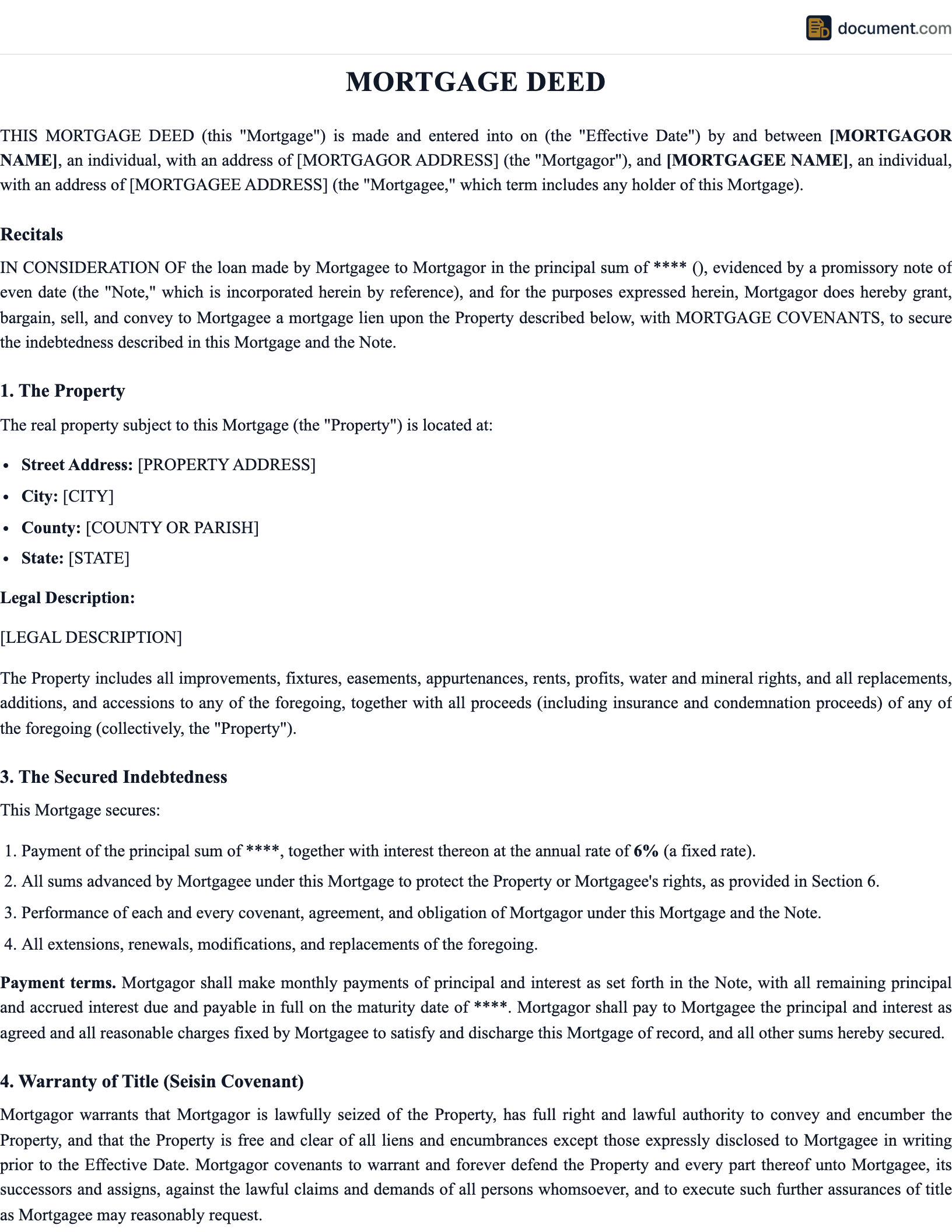

Sample South Carolina Mortgage Deed

Preview of our South Carolina-specific template. Your document will include all fields required for recording in any South Carolina county.

MORTGAGE DEED

STATE OF SOUTH CAROLINA

Legal Document

PARTY INFORMATION

Name: [Full Legal Name]

Address: [South Carolina Address]

County: [County]

PROPERTY DESCRIPTION

County: [County] State: South Carolina

Legal Description: [Per Recorded Plat]

Parcel No.: [APN]

South Carolina Mortgage Deed FAQ

Common questions about filing in South Carolina, including requirements, fees, and tax implications.

Official South Carolina Resources

Official state resources for verifying requirements and finding your local recording office.

Important Considerations

The Master-in-Equity system is South Carolina's most distinctive feature in mortgage law. If you default on a South Carolina mortgage, your foreclosure case will go before the county Master-in-Equity rather than a regular circuit court judge. The Master is a specialist in real property disputes and typically runs a more streamlined docket than a general civil court, which tends to make uncontested foreclosures somewhat more predictable in timing.

South Carolina's two-year deficiency judgment window is a material risk for borrowers who lose property in foreclosure. If the foreclosure sale does not cover the full loan balance, the lender can sue for the deficiency for up to two years after the sale date. Borrowers negotiating a short sale, deed in lieu, or loan modification should attempt to obtain a written waiver of deficiency rights from the lender as part of any settlement, since South Carolina law does not automatically extinguish the deficiency claim after a judicial sale.

The homestead property tax exemption in South Carolina is a meaningful benefit for qualifying residents, reducing the assessed value of a primary residence by up to $50,000. The exemption requires an application with the county auditor and is available to residents who are 65 or older, permanently and totally disabled, or legally blind. Mortgage lenders cannot prevent a borrower from claiming this exemption, and it does not affect the enforceability of the mortgage.

South Carolina Practice Note

Attorney involvement in South Carolina real estate closings is common and in some cases customary, particularly in the Charleston, Greenville, and Columbia markets. South Carolina attorneys who are licensed as title agents can handle both the closing and the title insurance commitment. Given the deficiency judgment exposure and the Master-in-Equity foreclosure process, having an attorney review the mortgage deed and loan terms before signing is a practical step for any South Carolina borrower.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Important Considerations

The Master-in-Equity system is South Carolina's most distinctive feature in mortgage law. If you default on a South Carolina mortgage, your foreclosure case will go before the county Master-in-Equity rather than a regular circuit court judge. The Master is a specialist in real property disputes and typically runs a more streamlined docket than a general civil court, which tends to make uncontested foreclosures somewhat more predictable in timing.

South Carolina's two-year deficiency judgment window is a material risk for borrowers who lose property in foreclosure. If the foreclosure sale does not cover the full loan balance, the lender can sue for the deficiency for up to two years after the sale date. Borrowers negotiating a short sale, deed in lieu, or loan modification should attempt to obtain a written waiver of deficiency rights from the lender as part of any settlement, since South Carolina law does not automatically extinguish the deficiency claim after a judicial sale.

The homestead property tax exemption in South Carolina is a meaningful benefit for qualifying residents, reducing the assessed value of a primary residence by up to $50,000. The exemption requires an application with the county auditor and is available to residents who are 65 or older, permanently and totally disabled, or legally blind. Mortgage lenders cannot prevent a borrower from claiming this exemption, and it does not affect the enforceability of the mortgage.

South Carolina Practice Note

Attorney involvement in South Carolina real estate closings is common and in some cases customary, particularly in the Charleston, Greenville, and Columbia markets. South Carolina attorneys who are licensed as title agents can handle both the closing and the title insurance commitment. Given the deficiency judgment exposure and the Master-in-Equity foreclosure process, having an attorney review the mortgage deed and loan terms before signing is a practical step for any South Carolina borrower.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Create your South Carolina Mortgage Deed in under 5 minutes.

Answer a few questions and download a South Carolina-compliant document, ready for the state agency.