What Is a Deed in Lieu of Foreclosure?

A deed in lieu of foreclosure is a real estate transaction in which a homeowner voluntarily transfers ownership of their property to the mortgage lender in exchange for release from some or all of the outstanding mortgage obligation. Rather than the lender pursuing a formal foreclosure — which involves court proceedings, public auctions, and significant legal costs — the borrower simply deeds the property back to the lender through a negotiated agreement. The phrase "in lieu of" means "instead of," because the deed transfer replaces the formal foreclosure process entirely.

The concept is straightforward in principle but carries substantial legal, financial, and tax consequences that borrowers must understand before proceeding. When a borrower falls behind on mortgage payments and cannot sell the property for enough to cover the outstanding loan balance, a deed in lieu may offer a way out that is faster, less expensive, and less damaging to the borrower's credit than a full foreclosure. For the lender, accepting a deed in lieu eliminates the cost and uncertainty of foreclosure litigation, avoids potential property vandalism during a prolonged process, and provides a quicker path to recovering the collateral.

However, a deed in lieu is not a unilateral decision. The lender must agree to accept the property and the terms of the release. Most lenders will require the borrower to demonstrate genuine financial hardship, show that the property has been listed for sale without success, and confirm that no junior liens or encumbrances exist on the property (or that they will be resolved). The agreement should always specify whether the lender waives its right to pursue a deficiency judgment — the difference between the property's fair market value and the outstanding loan balance — because without a written waiver, the borrower may still owe that difference.

A deed in lieu is distinct from a foreclosure, a short sale, a loan modification, and a forbearance agreement. Each of these alternatives addresses mortgage default differently, and the right choice depends on the borrower's financial situation, the property's market value relative to the loan balance, the lender's policies, and the laws of the state where the property is located. Understanding these distinctions is essential before committing to any course of action.

Avoid Foreclosure

Voluntarily resolve mortgage default without court proceedings or public auction

Less Credit Damage

Typically less damaging to your credit than a completed foreclosure proceeding

Faster Resolution

Resolve in two to six months versus six to eighteen months for foreclosure

Deed in Lieu of Foreclosure by State

State laws differ on deficiency judgments, tax treatment, and mandatory disclosures for deeds in lieu of foreclosure. Choose your state below for a template that matches local statutes and recording requirements.

How a Deed in Lieu Works

The deed in lieu process involves a negotiated transfer of property from the borrower to the lender. Unlike a foreclosure, which is an adversarial legal proceeding initiated by the lender, a deed in lieu is a cooperative transaction where both parties agree to the terms. Understanding the mechanics of this process helps borrowers prepare for what to expect and negotiate effectively.

At its core, the borrower executes a new deed — typically a special warranty deed or grant deed depending on the state — conveying the property to the lender. The lender records the deed with the county recorder's office, takes ownership of the property, and releases the mortgage lien. If the agreement includes a deficiency waiver, the lender also releases the borrower from personal liability for any remaining balance. The entire transaction is documented in a deed in lieu agreement that spells out the rights and obligations of both parties.

Borrower Contacts Loss Mitigation

The borrower contacts the lender's loss mitigation department to discuss alternatives to foreclosure. The borrower explains their financial hardship and expresses interest in a deed in lieu. The lender may require the borrower to first apply for a loan modification or list the property for sale before considering a deed in lieu.

Documentation and Property Evaluation

The lender requests financial hardship documentation (income statements, bank statements, hardship letter) and orders a property appraisal or broker price opinion (BPO) to determine the current market value. The lender also conducts a title search to identify any junior liens, tax liens, mechanic's liens, or other encumbrances on the property.

Negotiation of Terms

If the lender agrees in principle, both parties negotiate the terms of the deed in lieu agreement. Critical terms include whether the lender will waive the deficiency balance, the move-out timeline, whether cash-for-keys relocation assistance will be provided, the condition in which the borrower must leave the property, and any representations or warranties the borrower must make about the property's condition.

Execution and Recording

The borrower signs the deed transferring the property to the lender, along with the deed in lieu agreement. The deed is notarized and recorded with the county recorder's office. The lender records a satisfaction or release of the mortgage. The borrower vacates the property by the agreed-upon date, and the lender takes possession.

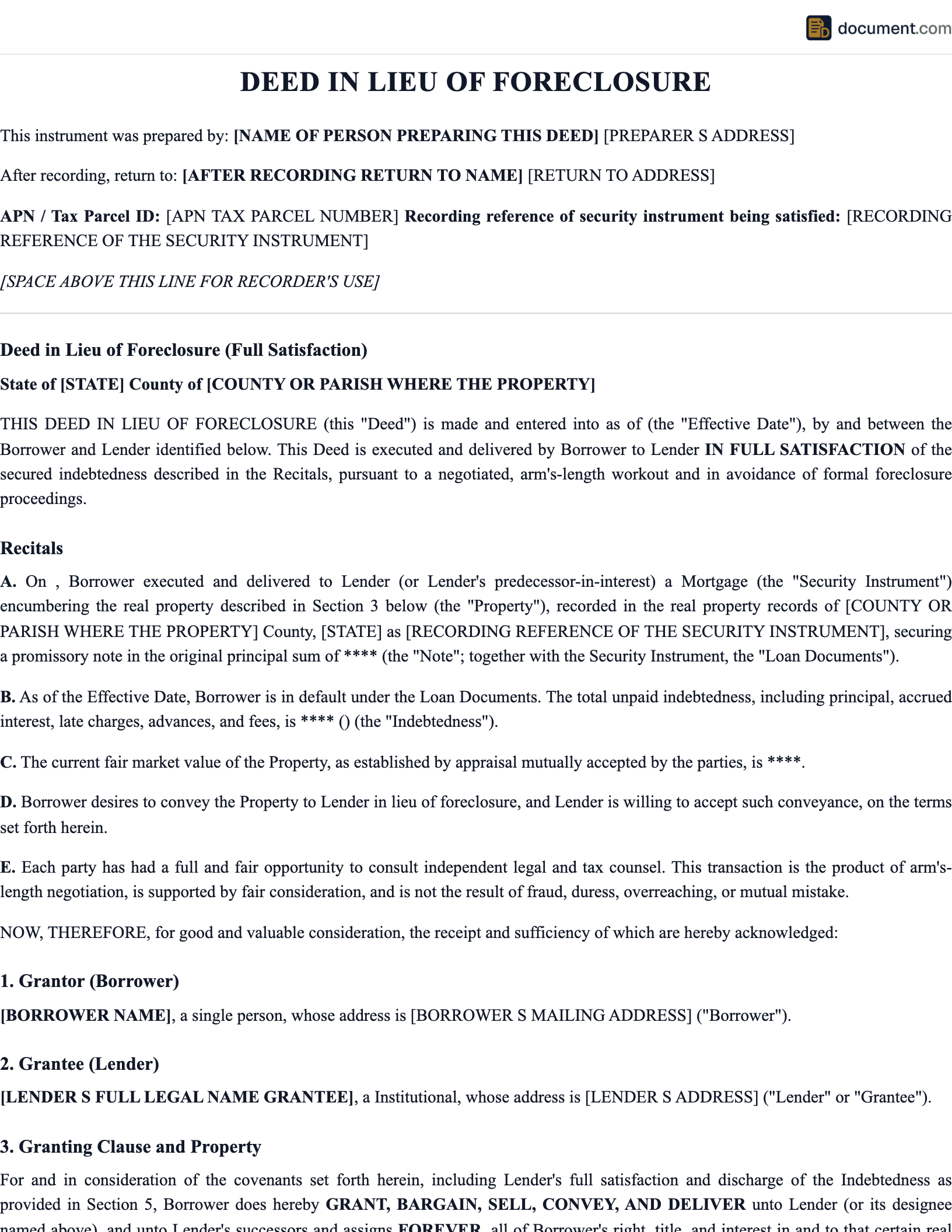

Deed in Lieu Form Preview

Below is a visual preview of the sections and fields included in a deed in lieu of foreclosure agreement. This mockup illustrates the structure and level of detail our templates provide. Your completed document will be fully formatted, professionally styled, and customized for your state's recording requirements.

Deed in Lieu of Foreclosure

Agreement and Conveyance

Section 1: Grantor (Borrower)

Section 2: Grantee (Lender)

Section 3: Property Information

Section 4: Financial Terms

Section 5: Execution & Notarization

Grantor (Borrower) Signature

Notary Public

Deed in Lieu vs Foreclosure vs Short Sale

Homeowners facing mortgage default have several options, and understanding the differences between them is critical for making the right decision. Each option carries different consequences for your credit, your tax obligations, your timeline, and your ability to obtain future financing. The comparison below highlights the key distinctions.

Deed in Lieu vs Foreclosure

Deed in Lieu

- - Voluntary transfer by borrower

- - No court proceedings or public auction

- - Takes 2-6 months to complete

- - Credit score drop of 85-160 points

- - New conventional loan eligible in ~4 years

- - Less public record visibility

- - Borrower may negotiate relocation assistance

Foreclosure

- - Involuntary action by lender

- - Court proceedings (judicial) or trustee sale (non-judicial)

- - Takes 6-18+ months depending on state

- - Credit score drop of 100-160+ points

- - New conventional loan eligible in ~7 years

- - Public record of foreclosure filing and auction

- - No relocation assistance

Key takeaway: A deed in lieu is generally the better option when both parties can agree on terms, because it is faster, less expensive, less adversarial, and typically results in less credit damage than a completed foreclosure.

Deed in Lieu vs Short Sale

Deed in Lieu

- - Property transfers directly to lender

- - No third-party buyer needed

- - Simpler process with fewer parties

- - Lender acquires an REO property to manage

- - Typically faster (2-6 months)

- - Lender may offer cash-for-keys

Short Sale

- - Property sold to third-party buyer

- - Requires finding a qualified buyer

- - More complex with buyer, agent, lender approval

- - Lender receives cash (no REO management)

- - Usually longer (3-12 months)

- - May have slightly less credit impact

Key takeaway: Many lenders prefer a short sale because they receive cash rather than a property they must maintain and resell. However, if the property cannot be sold on the open market within a reasonable time, a deed in lieu may be the more practical option.

Deed in Lieu vs Loan Modification

Deed in Lieu

- - Borrower gives up the property

- - Ends the mortgage obligation

- - Negative credit impact

- - Last-resort option

Loan Modification

- - Borrower keeps the property

- - Restructures mortgage terms (rate, term, balance)

- - Less credit impact if approved

- - First option to explore

Key takeaway: A loan modification should always be explored first because it allows you to keep your home. A deed in lieu is appropriate only when you have determined that keeping the property is no longer financially viable.

When to Consider a Deed in Lieu

A deed in lieu of foreclosure is not the right solution for every homeowner facing mortgage default. It is most appropriate in specific circumstances where the borrower has exhausted other options and the property cannot be retained or sold. Understanding when a deed in lieu makes sense — and when it does not — is critical for making an informed decision.

Underwater Mortgage

When you owe more on your mortgage than the property is currently worth and the negative equity is substantial enough that selling the property on the open market would still leave a significant balance due at closing.

Unable to Sell

When the property has been listed for sale for an extended period (typically 90+ days) without attracting a viable buyer, and the local market conditions suggest a sale is unlikely in the near term.

Genuine Financial Hardship

When you have experienced a qualifying financial hardship — job loss, significant income reduction, medical emergency, divorce, military deployment, or death of a co-borrower — that makes continued mortgage payments impossible.

Faster Credit Recovery

When minimizing the long-term credit impact is important to you. A deed in lieu typically allows you to qualify for new financing several years sooner than a completed foreclosure, which can be critical if you plan to purchase another home in the future.

Important:Before pursuing a deed in lieu, explore all alternatives with your lender — including loan modification, forbearance, repayment plans, and partial claim programs (for FHA loans). A deed in lieu should be a last resort after you have determined that keeping the property is no longer viable and a traditional sale or short sale is not feasible.

What Lenders Require for a Deed in Lieu

Lenders impose specific conditions that borrowers must meet before they will consider accepting a deed in lieu. These requirements protect the lender from fraud, ensure the borrower has a genuine hardship, and confirm that the property is worth acquiring. Understanding these requirements upfront will help you prepare a stronger application and increase the likelihood of approval.

- Demonstrated Financial Hardship: The borrower must provide documentation proving a genuine financial hardship — including a detailed hardship letter, recent pay stubs or proof of income (or lack thereof), bank statements, tax returns, and a complete financial statement showing monthly income versus expenses. Strategic default (choosing not to pay when you can afford to) typically disqualifies a borrower from a deed in lieu.

- Market Listing Attempt: Most lenders require the borrower to list the property for sale on the open market for a minimum period (typically 90 to 120 days) before they will consider a deed in lieu. This ensures that a traditional sale is not possible, which is the lender's preferred outcome because it results in a cash payoff rather than the lender taking ownership of a property.

- Clear Title (No Junior Liens): The property must be free of junior liens, second mortgages, HELOC liens, tax liens, mechanic's liens, judgment liens, and other encumbrances. If junior liens exist, they must be resolved or released before the lender will accept the deed, because the lender does not want to acquire a property subject to other creditors' claims.

- Property Condition: The property must be in reasonably marketable condition. Lenders will order an appraisal or broker price opinion to assess the property's value and condition. Significant damage, deferred maintenance, environmental hazards, or code violations may cause the lender to reject the deed in lieu.

- Voluntary and Arm's-Length Transaction: The lender will require the borrower to certify that the deed in lieu is being executed voluntarily, without duress or coercion, and that the borrower understands they are giving up ownership of the property. This protects the lender from future claims that the transfer was involuntary.

- Occupancy Status: Lenders may require the property to be owner-occupied rather than an investment or rental property. Some loan programs (particularly government-backed loans) have stricter eligibility requirements for deed in lieu transactions on non-owner-occupied properties.

Credit Impact of a Deed in Lieu

A deed in lieu of foreclosure will negatively affect your credit, but the damage is typically less severe than a completed foreclosure and the recovery period is shorter. Understanding the specific credit consequences — and how they compare to other forms of mortgage default — helps you make an informed decision and plan your financial recovery.

| Factor | Deed in Lieu | Foreclosure |

|---|---|---|

| Credit Score Drop | 85-160 points | 100-160+ points |

| Credit Report Duration | 7 years | 7 years |

| Conventional Loan Wait | 4 years | 7 years |

| FHA Loan Wait | 3 years (extenuating) | 3 years (extenuating) |

| VA Loan Wait | 2 years | 2 years |

| USDA Loan Wait | 3 years | 3 years |

Recovery tip: After a deed in lieu, you can begin rebuilding your credit immediately by maintaining on-time payments on all remaining obligations, keeping credit card balances low, and avoiding new derogatory marks. Many borrowers see significant credit score improvement within 18 to 24 months of a deed in lieu, particularly if the mortgage was their only delinquent account.

Tax Implications of a Deed in Lieu

The tax consequences of a deed in lieu are among the most complex and frequently misunderstood aspects of the transaction. When a lender forgives mortgage debt, the IRS may treat the forgiven amount as taxable income. Additionally, the property transfer itself may trigger capital gains tax depending on the property's basis and fair market value. Understanding these implications before executing a deed in lieu is essential.

Cancellation of Debt Income (1099-C)

When the lender forgives the difference between the outstanding loan balance and the property's fair market value, they issue IRS Form 1099-C reporting the forgiven amount as cancellation of debt income. For example, if you owe $300,000 and the property is appraised at $250,000, the lender may report $50,000 in cancelled debt. Without an applicable exclusion, this $50,000 would be added to your taxable income for the year.

Mortgage Forgiveness Debt Relief Act

This federal law allows qualifying homeowners to exclude forgiven mortgage debt from taxable income on their principal residence. The debt must have been used to buy, build, or substantially improve your main home, and the home must secure the debt. This exclusion has been extended multiple times and is subject to specific caps and eligibility requirements. Consult a tax professional to confirm whether the exclusion applies in your situation and for your tax year.

Insolvency Exclusion (IRC Section 108)

If you were insolvent at the time of debt cancellation — meaning your total liabilities exceeded the fair market value of your total assets — you may exclude the forgiven debt from income up to the amount of your insolvency. For example, if your liabilities exceeded your assets by $40,000 and $50,000 in debt was forgiven, you could exclude $40,000 and would owe tax on only $10,000. This exclusion requires filing IRS Form 982 with your tax return.

Capital Gains Tax Considerations

The property transfer in a deed in lieu is treated as a sale for tax purposes. If the property's fair market value exceeds your adjusted basis (original purchase price plus improvements minus depreciation), you may owe capital gains tax on the difference. For a primary residence, you may be able to exclude up to $250,000 in gains ($500,000 for married filing jointly) under IRC Section 121 if you lived in the home for at least two of the five years preceding the transfer.

Critical advice: Consult a tax professional before executing a deed in lieu. The tax consequences can be significant, and the interaction between cancellation of debt income, capital gains, and available exclusions is complex. A qualified CPA or tax attorney can help you understand your specific liability and plan accordingly.

Deficiency Judgment Risk

One of the most critical issues in any deed in lieu transaction is whether the lender will pursue a deficiency judgment against the borrower. A deficiency is the difference between the outstanding mortgage balance and the property's fair market value. If the property is worth less than what you owe — which is typically the case when a borrower seeks a deed in lieu — the lender may have the legal right to pursue you for that difference.

Whether a lender can pursue a deficiency depends on state law and the terms of the deed in lieu agreement. Some states are "non-recourse" states that prohibit deficiency judgments on purchase-money mortgages (loans used to buy the property), while other states allow lenders to pursue deficiency judgments in any situation unless the agreement specifically waives that right. Even in states that allow deficiency judgments, many lenders choose to waive the deficiency as part of the deed in lieu negotiation because the cost of pursuing a judgment against a financially distressed borrower often exceeds the recovery.

Always Negotiate a Written Deficiency Waiver

Never execute a deed in lieu without a clear, written statement from the lender waiving their right to pursue a deficiency judgment. Without this waiver, the lender could accept your property and still sue you for the remaining balance. The waiver should be explicit, unconditional, and included in the deed in lieu agreement itself.

Check Your State's Deficiency Laws

State laws vary significantly on deficiency judgments. Some states (such as California for purchase-money mortgages and Alaska) prohibit deficiency judgments after a deed in lieu. Other states (such as Florida and New York) allow them unless waived. Understanding your state's law gives you leverage in negotiations and helps you assess the risk.

Watch for Reservation of Rights Language

Some deed in lieu agreements include language where the lender "reserves the right" to pursue a deficiency. This means the lender has not waived anything. Have an attorney review the agreement before signing to ensure you understand whether the deficiency is truly being waived or merely deferred.

Cash-for-Keys Programs

Many lenders offer cash-for-keys arrangements as part of a deed in lieu transaction. Under these programs, the lender provides the borrower with a cash payment — typically ranging from $1,500 to $10,000 or more — in exchange for the borrower vacating the property by an agreed-upon date and leaving it in good, broom-clean condition. Cash-for-keys benefits both parties: the borrower receives financial assistance for relocation, and the lender avoids the risk of property damage or a protracted eviction.

The specific amount of relocation assistance varies by lender, loan type, and program. Some government-sponsored programs (such as those through Fannie Mae and Freddie Mac) have established cash-for-keys guidelines with set payment amounts. Private lenders have more discretion and may negotiate the amount based on the borrower's cooperation, the property's condition, and the local market. The cash-for-keys payment is typically conditioned on the borrower leaving the property in acceptable condition, with all personal belongings removed, all utilities connected (or properly winterized), and no intentional damage.

Negotiation tip:Always ask about cash-for-keys during your deed in lieu negotiation. Even if the lender does not mention it, they may be willing to offer relocation assistance to incentivize your cooperation. Frame it as a mutual benefit — you get help with moving costs, and they get an orderly, timely transition with the property in good condition.

How to Negotiate a Deed in Lieu

Negotiating a deed in lieu requires preparation, documentation, and an understanding of what the lender needs to approve the transaction. The process is not as simple as calling your lender and offering to hand back the keys — there is a formal application and review process that mirrors, in many ways, the process of applying for the original mortgage. Here is a step-by-step approach to negotiating effectively.

Contact Loss Mitigation Early

Do not wait until you are months behind on payments or until the lender files a foreclosure action. Contact your lender's loss mitigation department as soon as you know you cannot maintain your mortgage payments. Early contact demonstrates good faith and gives you more time and leverage to negotiate favorable terms. Ask specifically about all available alternatives, including loan modification, forbearance, repayment plans, and deed in lieu options.

Prepare Your Hardship Package

Assemble a complete documentation package before approaching the lender. This should include: a detailed hardship letter explaining why you can no longer afford the mortgage; two to three months of bank statements; recent pay stubs or proof of income (or proof of unemployment); your most recent two years of tax returns; a personal financial statement listing all assets, liabilities, income, and expenses; documentation of the hardship event (job termination letter, medical bills, divorce decree, etc.); and evidence that you attempted to sell the property (listing agreement, marketing history, showing feedback).

Negotiate the Critical Terms

Focus your negotiation on the terms that matter most. The deficiency waiver is the single most important term — insist on a full waiver in writing. Negotiate the move-out timeline to give yourself adequate time to find new housing (30 to 90 days is typical). Ask about cash-for-keys relocation assistance. Clarify how the lender will report the transaction to credit bureaus (some lenders will report it as "settled" rather than "foreclosed," which may be slightly more favorable). Have an attorney review the final agreement before signing.

What Lenders Evaluate in a Deed in Lieu Request

Lenders apply a specific set of criteria when evaluating whether to accept a deed in lieu of foreclosure. Understanding these factors helps you present a stronger case and anticipate potential obstacles. The lender's analysis essentially asks: "Is accepting this property voluntarily a better financial outcome for us than pursuing foreclosure?"

Hardship Documentation

The lender must be convinced that the borrower's financial hardship is genuine and not a strategic default. Comprehensive documentation of income loss, medical events, divorce, or other qualifying hardships is essential for approval.

Property Condition

The lender evaluates whether the property is in marketable condition. Well-maintained properties are more likely to be accepted because the lender can resell them quickly. Properties with significant damage, deferred maintenance, or environmental issues may be rejected.

Market Value Analysis

The lender orders a property appraisal or broker price opinion to determine current market value. They compare this to the outstanding loan balance, estimated foreclosure costs, and the likely recovery from a foreclosure sale to determine which option produces a better financial outcome.

Title Clearance

A clean title is essential. The lender conducts a title search to identify all liens and encumbrances. Properties with multiple liens, unresolved judgments, or title defects are unlikely candidates for a deed in lieu because the lender would acquire the property subject to those issues.

Sample Deed in Lieu of Foreclosure

Below is a condensed preview of our deed in lieu of foreclosure template. This sample shows the structure, language, and sections included in our attorney-reviewed documents. Your completed document will be fully customized for your state's recording and execution requirements.

DEED IN LIEU OF FORECLOSURE

Agreement and Conveyance

This Deed in Lieu of Foreclosure Agreement ("Agreement") is entered into as of [Date], by and between [Borrower Name]("Grantor/Borrower") and [Lender Name]("Grantee/Lender").

RECITALS

WHEREAS, Grantor is the owner of real property located at [Property Address], more particularly described in Exhibit A attached hereto; and WHEREAS, the Property is encumbered by a Deed of Trust/Mortgage dated [Date], recorded in [Recording Info], securing a promissory note in the original amount of $[Amount]; and WHEREAS, Grantor is in default under the terms of said Deed of Trust/Mortgage...

1. CONVEYANCE

Grantor hereby conveys, transfers, and delivers to Grantee all of Grantor's right, title, and interest in and to the Property, including all improvements, fixtures, and appurtenances, by execution and delivery of a [Grant/Special Warranty] Deed in the form attached hereto as Exhibit B...

2. RELEASE OF OBLIGATION

Upon recording of the Deed, Grantee hereby releases Grantor from all obligations under the Note and Deed of Trust/Mortgage identified in the Recitals, including any and all deficiency that may exist between the outstanding balance and the fair market value of the Property. Grantee waives any right to pursue a deficiency judgment against Grantor...

3. REPRESENTATIONS AND WARRANTIES

Grantor represents and warrants that: (a) this conveyance is made voluntarily and without duress or coercion; (b) Grantor has been advised to seek independent legal counsel; (c) there are no liens, encumbrances, or claims against the Property other than the Deed of Trust/Mortgage described herein; (d) the Property is in substantially the same condition as when last inspected by Grantee...

4. VACATING THE PROPERTY

Grantor shall vacate the Property no later than [Number] days after the execution of this Agreement, leaving the Property in broom-clean condition with all personal property removed and all keys, garage door openers, and access devices surrendered to Grantee...

5. RELOCATION ASSISTANCE

Grantee shall pay Grantor the sum of $[Amount]as relocation assistance, payable upon Grantor's satisfactory vacating of the Property in accordance with Section 4...

Frequently Asked Questions

Find answers to common questions about deeds in lieu of foreclosure, including credit impact, tax consequences, lender requirements, and how the process compares to other foreclosure alternatives.

Official Resources

For additional information on foreclosure alternatives, housing counseling, and homeowner assistance programs, consult these official and reputable resources.

HUD - Avoiding Foreclosure

U.S. Department of Housing and Urban Development foreclosure prevention resources

CFPB - Help for Homeowners

Consumer Financial Protection Bureau guide to mortgage relief and foreclosure prevention

HUD - Housing Counseling

Find a HUD-approved housing counselor near you for free foreclosure prevention assistance

Fannie Mae - Homeowner Help

Fannie Mae foreclosure alternatives including deed in lieu and short sale programs

Freddie Mac - Foreclosure Prevention

Freddie Mac resources for borrowers exploring foreclosure alternatives

IRS - Foreclosure & Debt Cancellation

IRS guidance on tax implications of foreclosure and cancelled mortgage debt

Nolo - Foreclosure Alternatives

Free legal encyclopedia covering deed in lieu, short sale, and other options

VA - Home Loan Resources

Department of Veterans Affairs assistance for veterans facing mortgage default

Create your Deed in Lieu of Foreclosure in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.