Pennsylvania Mortgage Deed Overview

Pennsylvania is a mortgage state that requires judicial foreclosure. When a borrower defaults, the lender must file a complaint in the county Court of Common Pleas, work through the required pre-suit notice process, and obtain a judgment before any sheriff's sale can occur. Before filing, Pennsylvania law mandates that lenders send specific statutory notices under the Loan Interest and Protection Law (Act 6) and, for certain loans, the Homeowner Emergency Mortgage Assistance Program notice (Act 91). Missing these notice requirements can derail a foreclosure action.

Pennsylvania mortgage deeds are recorded with the Recorder of Deeds in the county where the property sits. Recording fees vary by county and are not set by a uniform state schedule, so the amount due depends on which of Pennsylvania's 67 counties holds the property. Philadelphia County has additional local requirements and taxes that apply to certain real property transactions. Properties subject to agricultural conservation easements, which are common in Chester, Lancaster, and other rural counties, carry deed restrictions that affect what a lender can do with encumbered farmland.

$25

Recording fee

2% (1%+1%)

Transfer tax

Required

Notarization

0

Witnesses required

Pennsylvania Requirements

Pennsylvania mortgage deeds must be notarized and meet the formatting requirements of the Recorder of Deeds in the applicable county. Documents should include the complete legal description as it appears in the current deed of record, the parcel identification number (PIN) assigned by the county assessment office, and a return address for the recorded document. Pennsylvania does not require additional witnesses for mortgage instruments beyond the notary.

Pennsylvania Specific Note

Pennsylvania imposes a realty transfer tax of 2% (split between state and local) on real property ownership transfers, but mortgage instruments are generally exempt because they do not convey ownership. Recording fees vary by county and are not set by a uniform state schedule; confirm the exact fee with the Recorder of Deeds in the property's county before submitting. Philadelphia County imposes additional local taxes and requirements that do not apply elsewhere in the state. For properties in agricultural preservation programs, confirm with the county agricultural land preservation board before recording a mortgage.

Document Requirements

- Notarization: Must be notarized by a Pennsylvania notary public or authorized notary

- Witnesses: Pennsylvania requires 0 additional witness(es)

- Legal Description: Complete legal description as it appears on the current deed of record

- Parcel Number: Assessor's parcel number or tax ID

- Return Address: Mailing address for returning the recorded document

- Formatting: Standard formatting with adequate margins, black ink, minimum 10-point font

How to File in Pennsylvania

Recording in Pennsylvania is done at the county Recorder of Deeds office in the county where the property is located. Fees and processing times vary by county, so contact the specific office before submitting.

Prepare the Document

Complete the mortgage deed with full legal names of all parties, the complete legal description as it appears in the existing deed of record, the county parcel identification number, the loan amount being secured, and a return address. For properties in agricultural preservation programs, confirm with the preservation board before proceeding.

Notarize Before a Pennsylvania Notary

The mortgagor must sign before a notary public commissioned in Pennsylvania. Bring valid government-issued photo ID. Pennsylvania permits remote online notarization under the Pennsylvania Revised Uniform Law on Notarial Acts, so electronic notarization through an approved platform is an option for parties who cannot appear in person.

Submit to the Recorder of Deeds

File the executed and notarized mortgage deed with the Recorder of Deeds in the county where the property is located. Many Pennsylvania county offices accept e-recording. For Philadelphia County, contact the Philadelphia Recorder of Deeds directly about local submission requirements, which differ from other counties.

Pay the Recording Fee

Recording fees in Pennsylvania vary by county and are not set by a uniform state schedule. Call the specific Recorder of Deeds office to get the current fee before submitting. Mortgage instruments generally are not subject to the Pennsylvania realty transfer tax, which applies to ownership transfers rather than loan security documents.

Receive and Retain the Recorded Document

After recording, the Recorder of Deeds stamps the document with the recording book and page number or instrument number and returns it to the address listed on the document. Keep the recorded mortgage deed with the loan file. When the loan is satisfied, a mortgage satisfaction piece must be recorded to release the lien from the property records.

Pennsylvania Fees & Costs

Typical costs for filing in Pennsylvania. Actual fees may vary by county.

| Fee / Tax | Amount |

|---|---|

| Recording Fee | $25 |

| Transfer Tax | 2% (1%+1%) |

| Notarization | $5 - $25 per signature |

| Certified Copy | $1 - $10 per page |

| Attorney Review (optional) | $150 - $500 |

Pennsylvania Tax Implications

Pennsylvania imposes a realty transfer tax of 2% on real property conveyances, split between the state (1%) and the local taxing authority (1%). However, mortgage instruments are generally not conveyances of ownership and are not subject to the realty transfer tax. Recording a mortgage deed does not trigger a transfer tax obligation for borrowers. Philadelphia imposes an additional local realty transfer tax of 3.278% on ownership conveyances, but again this applies to deeds rather than mortgage documents.

Mortgage interest paid on a qualifying Pennsylvania residence may be deductible on federal income taxes for taxpayers who itemize. Pennsylvania does not allow a deduction for mortgage interest on Pennsylvania personal income tax returns, which is an important distinction for Pennsylvania homeowners comparing state and federal tax treatment. The lack of a state mortgage interest deduction is offset somewhat by Pennsylvania's relatively low flat income tax rate.

Pennsylvania property taxes are assessed and collected at the local level by county, municipality, and school district. The Commonwealth does not impose a statewide property tax. Reassessment practices vary widely: some counties reassess regularly while others maintain outdated base-year assessments that can result in effective tax rates far below or above market. Borrowers should verify the current assessed value and confirm that the property taxes shown on the loan documents reflect actual obligations.

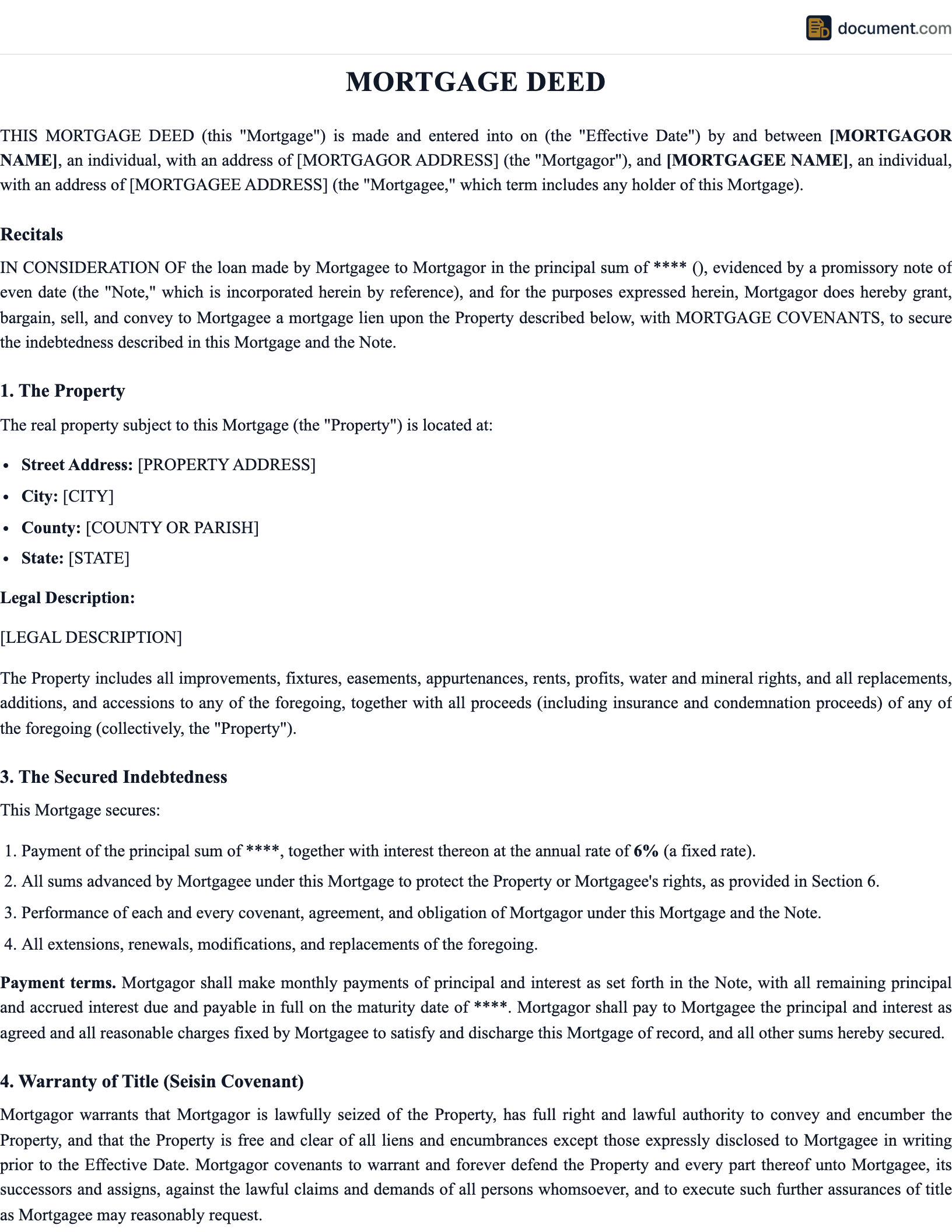

Sample Pennsylvania Mortgage Deed

Preview of our Pennsylvania-specific template. Your document will include all fields required for recording in any Pennsylvania county.

MORTGAGE DEED

STATE OF PENNSYLVANIA

Legal Document

PARTY INFORMATION

Name: [Full Legal Name]

Address: [Pennsylvania Address]

County: [County]

PROPERTY DESCRIPTION

County: [County] State: Pennsylvania

Legal Description: [Per Recorded Plat]

Parcel No.: [APN]

Pennsylvania Mortgage Deed FAQ

Common questions about filing in Pennsylvania, including requirements, fees, and tax implications.

Official Pennsylvania Resources

Official state resources for verifying requirements and finding your local recording office.

Important Considerations

Pennsylvania's pre-foreclosure notice requirements are among the more borrower-protective in the country. Before a lender can file a foreclosure complaint on a residential mortgage, it must send Act 6 and Act 91 notices that give the borrower specific information about the default, the amount needed to cure, and the right to apply for emergency assistance through the Pennsylvania Housing Finance Agency's Homeowner Equity Recovery Opportunity program. Lenders who skip or improperly serve these notices face dismissal of their foreclosure actions.

Philadelphia County operates differently from the rest of Pennsylvania in several respects. The Philadelphia court system has its own mortgage foreclosure procedures, and the city imposes local taxes on real property transactions that do not apply elsewhere. Borrowers and lenders with Philadelphia properties should work with counsel familiar with city-specific requirements, not just statewide Pennsylvania practice.

Properties enrolled in Pennsylvania's agricultural conservation easement program are a category that deserves special attention. The easements are perpetual deed restrictions that limit development and non-agricultural use. A lender foreclosing on preserved farmland acquires the property subject to the easement, and the county preservation board generally has rights that complicate any non-agricultural disposition. Lenders should obtain and review the specific easement deed before accepting preserved farmland as collateral.

Pennsylvania Practice Note

Pennsylvania real estate attorneys play an active role in residential closings in many parts of the state, particularly in eastern Pennsylvania. If you are uncertain whether a property is subject to an agricultural easement, a Philadelphia local tax, or prior liens that require careful clearance, consulting with a Pennsylvania real estate attorney before closing and recording is the prudent course.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Important Considerations

Pennsylvania's pre-foreclosure notice requirements are among the more borrower-protective in the country. Before a lender can file a foreclosure complaint on a residential mortgage, it must send Act 6 and Act 91 notices that give the borrower specific information about the default, the amount needed to cure, and the right to apply for emergency assistance through the Pennsylvania Housing Finance Agency's Homeowner Equity Recovery Opportunity program. Lenders who skip or improperly serve these notices face dismissal of their foreclosure actions.

Philadelphia County operates differently from the rest of Pennsylvania in several respects. The Philadelphia court system has its own mortgage foreclosure procedures, and the city imposes local taxes on real property transactions that do not apply elsewhere. Borrowers and lenders with Philadelphia properties should work with counsel familiar with city-specific requirements, not just statewide Pennsylvania practice.

Properties enrolled in Pennsylvania's agricultural conservation easement program are a category that deserves special attention. The easements are perpetual deed restrictions that limit development and non-agricultural use. A lender foreclosing on preserved farmland acquires the property subject to the easement, and the county preservation board generally has rights that complicate any non-agricultural disposition. Lenders should obtain and review the specific easement deed before accepting preserved farmland as collateral.

Pennsylvania Practice Note

Pennsylvania real estate attorneys play an active role in residential closings in many parts of the state, particularly in eastern Pennsylvania. If you are uncertain whether a property is subject to an agricultural easement, a Philadelphia local tax, or prior liens that require careful clearance, consulting with a Pennsylvania real estate attorney before closing and recording is the prudent course.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Create your Pennsylvania Mortgage Deed in under 5 minutes.

Answer a few questions and download a Pennsylvania-compliant document, ready for the state agency.