North Dakota Mortgage Deed Overview

North Dakota is a judicial foreclosure state that uses mortgage deeds as the standard lien instrument for real property lending. Mortgage deeds are recorded with the Register of Deeds in each of the state's 53 counties. If a borrower defaults, the lender must file a district court action to foreclose, obtain a judgment, and then proceed to a sheriff's sale. One of North Dakota's most distinctive features is the post-sale redemption period: residential borrowers typically have 60 days after the foreclosure sale to redeem, while agricultural landowners may have considerably longer, reflecting the state's historical policy of protecting farm operators from rapid loss of agricultural property.

North Dakota imposes no mortgage recording tax and no real property transfer tax, making recording costs among the lowest in the country. Base recording fees start around $10. The state has no income tax at all, which eliminates several tax complications that arise in other states. Agricultural land lending is a significant segment of North Dakota's real estate market, and lenders and borrowers working in that sector need to be aware of extended redemption rights and corporate ownership restrictions that apply specifically to agricultural property. Abstract-and-opinion title practice is still common in rural North Dakota counties, so title evidence may come in the form of a title opinion rather than a title insurance policy.

$10

Recording fee

None

Transfer tax

Required

Notarization

0

Witnesses required

North Dakota Requirements

North Dakota's recording requirements are set out in NDCC Chapter 47-19. Instruments affecting title to real property must be acknowledged before a notary public in the form specified by statute, and the acknowledgment must correctly identify the type of party (individual, corporate officer, trustee, etc.) who is signing. The county Register of Deeds maintains a grantor-grantee index. In rural counties, abstract-and-opinion title work remains common, where a licensed attorney reviews the abstract of title and issues an opinion letter rather than providing title insurance. Lenders from other states should confirm which form of title evidence will satisfy their requirements before closing.

North Dakota: Redemption Rights and Agricultural Land Rules

North Dakota has meaningful post-sale redemption rights that lenders need to account for in their collateral analysis. For residential property, the redemption period is 60 days after the foreclosure sale. For agricultural land, redemption periods are longer, giving farm operators additional time to reclaim property. Additionally, North Dakota restricts corporate ownership of agricultural land under its Alien Ownership Act. Any transaction involving agricultural land should be reviewed by a North Dakota attorney familiar with both real estate and agricultural law.

Document Requirements

- Notarization: Must be notarized by a North Dakota notary public or authorized notary

- Witnesses: North Dakota requires 0 additional witness(es)

- Legal Description: Complete legal description as it appears on the current deed of record

- Parcel Number: Assessor's parcel number or tax ID

- Return Address: Mailing address for returning the recorded document

- Formatting: Standard formatting with adequate margins, black ink, minimum 10-point font

How to File in North Dakota

The recording process in North Dakota is straightforward, and costs are low compared to most states. The steps below reflect standard practice, though rural counties may have specific submission procedures or limited hours.

Draft the Mortgage Deed

Include the full legal names and addresses of all parties, the complete legal description exactly matching the existing deed, the parcel identification number, the loan amount and relevant mortgage covenants, and a properly formatted acknowledgment block. For agricultural land transactions, flag whether the property is farmland, as additional rules may apply to the lender's collateral analysis.

Execute Before a Notary

The mortgagor signs in the presence of a commissioned North Dakota notary public. The notary must use the acknowledgment form prescribed by NDCC 47-19-02. Bring valid government-issued photo ID. No witnesses beyond the notary are required. Out-of-state acknowledgments are acceptable if they follow the Uniform Recognition of Acknowledgments Act.

Submit to the County Register of Deeds

Bring or mail the original notarized mortgage deed to the Register of Deeds office in the county where the property is located. Call ahead in rural counties, as hours may be limited. Some North Dakota counties accept e-recording through approved platforms, which can save a trip and reduce processing time.

Pay the Recording Fee

North Dakota charges roughly $10 for the first page and a per-page charge for subsequent pages. There is no mortgage recording tax and no real property transfer tax in North Dakota. Pay by check, money order, or cash depending on the county office's accepted methods.

Retain the Recorded Document

The Register of Deeds stamps the document with recording information and returns it. The lender typically holds the recorded mortgage deed as evidence of the lien during the loan term. When the debt is fully paid, the lender must execute and file a satisfaction of mortgage. Borrowers should follow up to confirm the satisfaction is recorded, as an unreleased mortgage can cloud the title for future sales or refinances.

North Dakota Fees & Costs

Typical costs for filing in North Dakota. Actual fees may vary by county.

| Fee / Tax | Amount |

|---|---|

| Recording Fee | $10 |

| Transfer Tax | None |

| Notarization | $5 - $25 per signature |

| Certified Copy | $1 - $10 per page |

| Attorney Review (optional) | $150 - $500 |

North Dakota Tax Implications

North Dakota's tax environment is unusually favorable for real property transactions. The state imposes no real property transfer tax and no mortgage recording tax. North Dakota also has no state income tax, eliminating the state-level income tax consequences that borrowers in other states must navigate when dealing with cancellation of debt income, mortgage interest deductions, or capital gains from foreclosure sales. From a pure tax cost standpoint, North Dakota mortgage transactions carry very little state-level tax friction.

Property taxes in North Dakota are administered at the county level. Agricultural land is valued differently than residential or commercial property, with farmland assessed based on its productive capacity rather than market value in some contexts. This distinction matters for lenders evaluating agricultural collateral, since the assessed value used for tax purposes may diverge significantly from the market value of the land. Recording a mortgage deed does not itself trigger reassessment in North Dakota.

For federal tax purposes, mortgage interest on a North Dakota property is deductible for taxpayers who itemize, subject to the standard federal limits. Borrowers who experience cancellation of debt income through foreclosure, short sale, or loan modification may have federal reporting obligations, but North Dakota's lack of a state income tax means there is no separate state tax calculation to perform on that income. This is a meaningful simplification compared to states like California or New York where cancellation of debt income triggers both federal and state tax obligations.

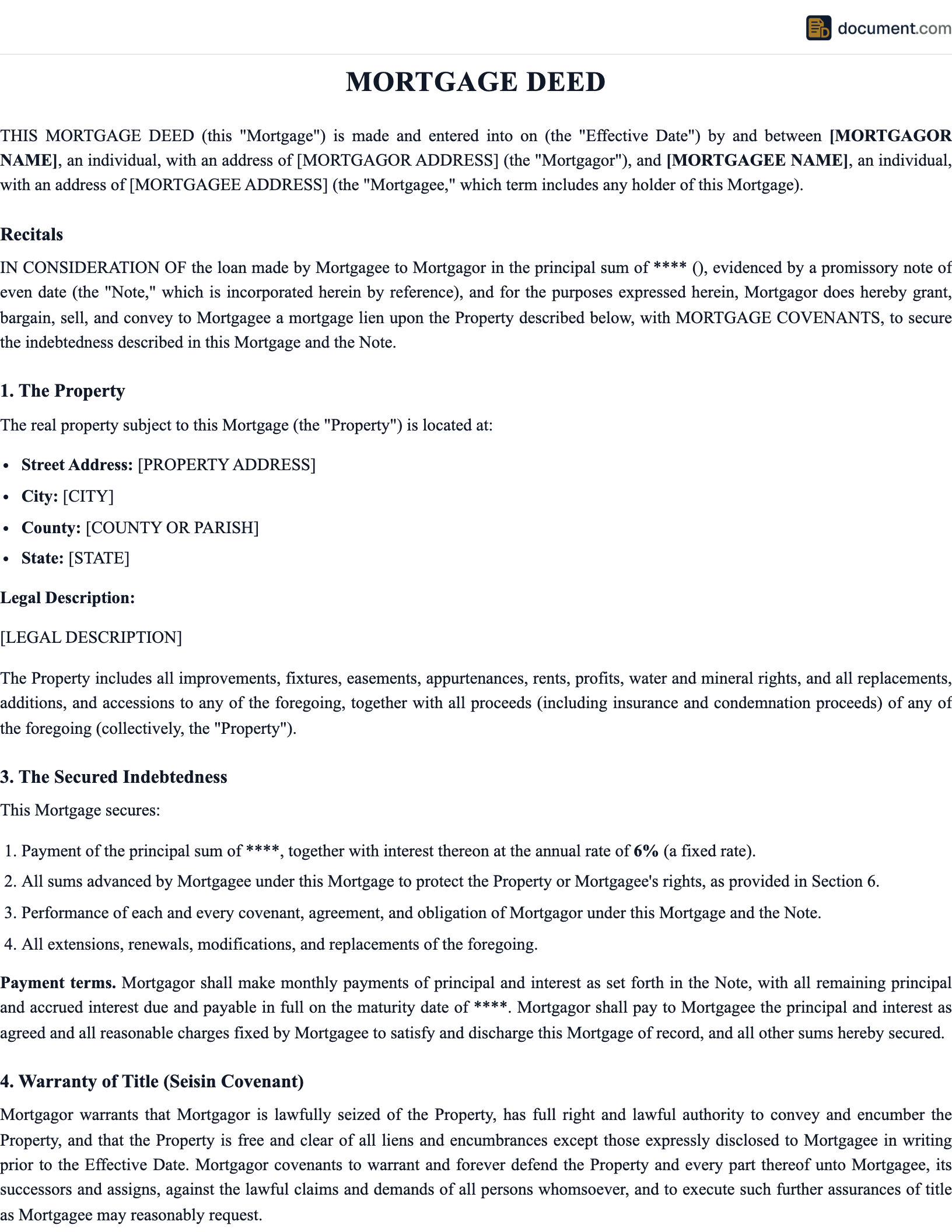

Sample North Dakota Mortgage Deed

Preview of our North Dakota-specific template. Your document will include all fields required for recording in any North Dakota county.

MORTGAGE DEED

STATE OF NORTH DAKOTA

Legal Document

PARTY INFORMATION

Name: [Full Legal Name]

Address: [North Dakota Address]

County: [County]

PROPERTY DESCRIPTION

County: [County] State: North Dakota

Legal Description: [Per Recorded Plat]

Parcel No.: [APN]

North Dakota Mortgage Deed FAQ

Common questions about filing in North Dakota, including requirements, fees, and tax implications.

Official North Dakota Resources

Official state resources for verifying requirements and finding your local recording office.

Important Considerations

Redemption rights in North Dakota are a practical reality that lenders underwriting North Dakota mortgages need to account for. After a judicial foreclosure sale, a residential borrower has 60 days to redeem the property by paying the sale price plus costs and interest. For agricultural land, the redemption period can be substantially longer. This means that even after a foreclosure sale is completed, lenders cannot take possession or convey the property with confidence until the redemption period expires. Build this timeline into your enforcement planning.

Agricultural land transactions in North Dakota carry unique legal considerations beyond the redemption period. North Dakota's Alien Ownership Law restricts certain corporate entities from acquiring agricultural land, which can affect who is eligible to be a lender or buyer in a foreclosure context. Lenders taking mortgages on North Dakota farmland should review whether their institutional structure creates any ownership restriction issues. Borrowers using agricultural land as mortgage collateral should also understand how the extended redemption period interacts with any farm loan programs they may be using.

Title evidence in rural North Dakota often takes the form of an abstract of title with an attorney opinion rather than a title insurance policy. If you are an out-of-state lender accustomed to receiving a title insurance commitment, confirm early in the process whether your loan requirements will accept an abstract-and-opinion alternative. Some North Dakota lenders and attorneys can arrange title insurance through national title companies, but it may take more lead time in smaller counties than in urban markets.

Consult a North Dakota Real Estate Attorney for Agricultural Transactions

North Dakota real property law has several features that are not intuitive for practitioners from other states, particularly around agricultural land redemption rights, corporate ownership restrictions, and abstract-and-opinion title practice. For any transaction involving agricultural land or seller financing in North Dakota, working with a licensed North Dakota real estate attorney is strongly recommended. The upfront cost of legal review is modest compared to the complications that can arise from an improperly structured mortgage on farmland.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Important Considerations

Redemption rights in North Dakota are a practical reality that lenders underwriting North Dakota mortgages need to account for. After a judicial foreclosure sale, a residential borrower has 60 days to redeem the property by paying the sale price plus costs and interest. For agricultural land, the redemption period can be substantially longer. This means that even after a foreclosure sale is completed, lenders cannot take possession or convey the property with confidence until the redemption period expires. Build this timeline into your enforcement planning.

Agricultural land transactions in North Dakota carry unique legal considerations beyond the redemption period. North Dakota's Alien Ownership Law restricts certain corporate entities from acquiring agricultural land, which can affect who is eligible to be a lender or buyer in a foreclosure context. Lenders taking mortgages on North Dakota farmland should review whether their institutional structure creates any ownership restriction issues. Borrowers using agricultural land as mortgage collateral should also understand how the extended redemption period interacts with any farm loan programs they may be using.

Title evidence in rural North Dakota often takes the form of an abstract of title with an attorney opinion rather than a title insurance policy. If you are an out-of-state lender accustomed to receiving a title insurance commitment, confirm early in the process whether your loan requirements will accept an abstract-and-opinion alternative. Some North Dakota lenders and attorneys can arrange title insurance through national title companies, but it may take more lead time in smaller counties than in urban markets.

Consult a North Dakota Real Estate Attorney for Agricultural Transactions

North Dakota real property law has several features that are not intuitive for practitioners from other states, particularly around agricultural land redemption rights, corporate ownership restrictions, and abstract-and-opinion title practice. For any transaction involving agricultural land or seller financing in North Dakota, working with a licensed North Dakota real estate attorney is strongly recommended. The upfront cost of legal review is modest compared to the complications that can arise from an improperly structured mortgage on farmland.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Create your North Dakota Mortgage Deed in under 5 minutes.

Answer a few questions and download a North Dakota-compliant document, ready for the state agency.