Nevada Mortgage Deed Overview

Nevada is a deed of trust state, and while mortgage deeds are legally valid instruments, institutional lenders in Nevada almost exclusively use deeds of trust to take advantage of the state's non-judicial foreclosure process under NRS Chapter 107. A mortgage deed still creates a valid lien on real property and is the right tool in many private lending and seller-financed transactions. After the 2008 housing crisis hit Nevada harder than almost any other state, the legislature enacted sweeping foreclosure reforms including a mandatory Foreclosure Mediation Program for owner-occupied homes that significantly changed the dynamic between lenders and distressed borrowers.

Nevada has no state income tax, which affects how real estate investors think about holding and financing property here. The state does impose a Real Property Transfer Tax on conveyances, and Clark County adds a school district surcharge, but these taxes apply to property transfers rather than mortgage recording specifically. Both spouses must typically sign and acknowledge any mortgage encumbering community property, which is an important execution requirement to get right before recording.

$15

Recording fee

$1.95 per $500

Transfer tax

Required

Notarization

0

Witnesses required

Nevada Requirements

Nevada's county recorder offices have standardized recording requirements under state law, but Clark County and Washoe County handle dramatically higher document volumes and have invested more heavily in e-recording infrastructure. For transactions in the Las Vegas metro or Reno-Sparks area, e-recording through an approved vendor is the most efficient route. For rural Nevada counties, confirm whether in-person or mail submission is required before making plans.

Nevada Specific Note

Nevada is a community property state, and both spouses must acknowledge any mortgage or deed of trust encumbering community property. A lender who records without both spouses' signatures risks having the non-signing spouse's interest be unencumbered. Nevada reformed its foreclosure laws significantly after 2008; the Foreclosure Mediation Program applies to owner-occupied residential properties and cannot be waived by the borrower at loan origination. Confirm current recording fees and any applicable Real Property Transfer Tax with the specific county recorder before closing.

Document Requirements

- Notarization: Must be notarized by a Nevada notary public or authorized notary

- Witnesses: Nevada requires 0 additional witness(es)

- Legal Description: Complete legal description as it appears on the current deed of record

- Parcel Number: Assessor's parcel number or tax ID

- Return Address: Mailing address for returning the recorded document

- Formatting: Standard formatting with adequate margins, black ink, minimum 10-point font

How to File in Nevada

Nevada mortgage deeds are recorded at the county recorder in the county where the property sits. In Clark and Washoe counties, e-recording is the standard; in smaller counties, confirm procedures before submitting. Here is the process from execution to recording.

Complete All Document Fields

Fill in the borrower and lender names, the complete legal description from the current county recorder index, the loan amount and maturity, and all required covenants. In Nevada, the document should also include the assessor's parcel number and the lender's address for the purposes of the county record.

Obtain Notarial Acknowledgment From Both Spouses if Applicable

All grantors must sign before a Nevada notary public with valid identification. Because Nevada is a community property state, both spouses must acknowledge the instrument if the mortgaged property is community property. The notary completes the acknowledgment block and affixes their official stamp and commission expiration.

Submit to the County Recorder

In Clark County, use the Simplifile or similar e-recording platform unless your escrow company files on your behalf. In Washoe County, e-recording is also available. For rural Nevada counties, contact the recorder's office to confirm their current submission methods, fees, and hours before making the trip.

Pay the Recording Fee

Nevada county recorders charge a per-page fee, typically starting around $15 for the first page. Clark County adds a modest additional charge. There is no mortgage recording tax in Nevada. Any applicable Real Property Transfer Tax is calculated on the deed of conveyance rather than the mortgage instrument.

Retain the Stamped Recorded Copy

Once recorded, the document receives a recorder's stamp with book and instrument number establishing the priority date. Keep the original in a secure location. If the Foreclosure Mediation Program applies to this loan, make sure the borrower is aware of their right to request mediation in the event of default, which must be exercised within the notice period.

Nevada Fees & Costs

Typical costs for filing in Nevada. Actual fees may vary by county.

| Fee / Tax | Amount |

|---|---|

| Recording Fee | $15 |

| Transfer Tax | $1.95 per $500 |

| Notarization | $5 - $25 per signature |

| Certified Copy | $1 - $10 per page |

| Attorney Review (optional) | $150 - $500 |

Nevada Tax Implications

Nevada's biggest tax advantage for real estate investors is the absence of a state income tax. When property appreciates and is eventually sold, gains are subject only to federal capital gains tax and not to any state-level income tax. This makes Nevada attractive for long-term real estate holds and for investors rolling proceeds between properties. The mortgage itself does not trigger a tax event at origination or payoff.

Nevada does impose a Real Property Transfer Tax (RPTT) when real property changes hands by deed. The base rate is $1.95 per $500 of value statewide, and Clark County imposes an additional school district tax on top of that. The RPTT is typically the seller's obligation on a sale, and in a refinance there is no transfer of ownership so no RPTT is due. However, when property is being placed into or transferred out of a trust or LLC as part of a financing arrangement, confirm with a Nevada attorney whether that transfer triggers RPTT liability.

Nevada property taxes are capped at 3% annual increases for homeowners who have the property as their primary residence under the state's partial abatement program. Investment properties do not benefit from the cap to the same degree. Lenders financing Nevada investment properties typically require property tax impounds given the higher assessed values in Clark and Washoe counties, where property tax bills on commercial and multi-family assets can be substantial.

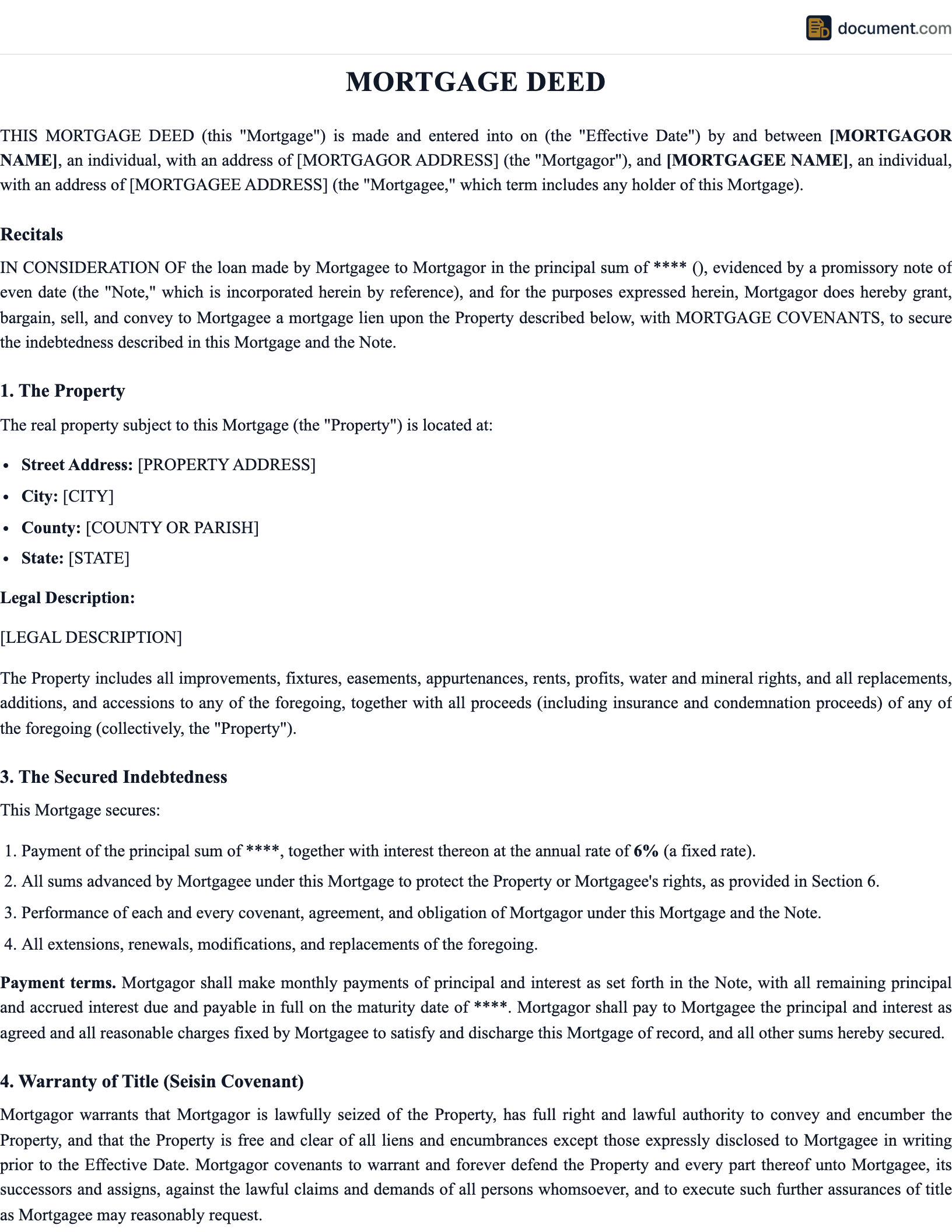

Sample Nevada Mortgage Deed

Preview of our Nevada-specific template. Your document will include all fields required for recording in any Nevada county.

MORTGAGE DEED

STATE OF NEVADA

Legal Document

PARTY INFORMATION

Name: [Full Legal Name]

Address: [Nevada Address]

County: [County]

PROPERTY DESCRIPTION

County: [County] State: Nevada

Legal Description: [Per Recorded Plat]

Parcel No.: [APN]

Nevada Mortgage Deed FAQ

Common questions about filing in Nevada, including requirements, fees, and tax implications.

Official Nevada Resources

Official state resources for verifying requirements and finding your local recording office.

Important Considerations

Nevada's post-2008 foreclosure reforms created lasting procedural obligations that lenders must follow even today. The Foreclosure Mediation Program is not optional for owner-occupied residential properties: if a borrower elects mediation after receiving a notice of default, the lender must participate and produce specified documents demonstrating authority to modify or resolve the loan. Lenders who fail to comply in good faith risk sanctions that can halt the foreclosure entirely. These requirements should be factored into any Nevada residential lending program from a compliance standpoint.

The community property rule in Nevada requires careful attention to signing requirements. If one spouse holds title to a property acquired during the marriage, the other spouse may still hold a community property interest. A lender who records a mortgage signed only by the title-holding spouse may find that the non-signing spouse's interest is unencumbered, which creates a serious problem in foreclosure. Title companies in Nevada typically require both spousal signatures in the commitment and will not insure around a missing spouse signature.

Nevada's real estate market, particularly in Las Vegas and Henderson, sees significant investor activity and short-term rental investment. Mortgage documents for investment properties should address intended use, short-term rental compliance with local ordinances, and any HOA restrictions, particularly in planned communities where rental restrictions may be enforceable. Some Nevada HOAs have occupancy restrictions that could affect a lender's ability to market and sell the property in a foreclosure scenario.

Nevada Attorney Note

Nevada real estate attorneys in Las Vegas and Reno are well-versed in the post-2008 statutory changes. For institutional lenders with Nevada portfolios, having counsel review your standard mortgage documents against NRS Chapter 107 and the Foreclosure Mediation Program requirements is worthwhile. For private lenders and seller-financed deals, even a brief consultation before closing can prevent issues that are expensive to correct after recording.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Important Considerations

Nevada's post-2008 foreclosure reforms created lasting procedural obligations that lenders must follow even today. The Foreclosure Mediation Program is not optional for owner-occupied residential properties: if a borrower elects mediation after receiving a notice of default, the lender must participate and produce specified documents demonstrating authority to modify or resolve the loan. Lenders who fail to comply in good faith risk sanctions that can halt the foreclosure entirely.

The community property rule in Nevada requires careful attention to signing requirements. If one spouse holds title to a property acquired during the marriage, the other spouse may still hold a community property interest. A lender who records a mortgage signed only by the title-holding spouse may find that the non-signing spouse's interest is unencumbered. Title companies in Nevada typically require both spousal signatures and will not insure around a missing spouse signature.

Nevada's real estate market, particularly in Las Vegas and Henderson, sees significant investor activity and short-term rental investment. Mortgage documents for investment properties should address intended use, short-term rental compliance with local ordinances, and any HOA restrictions, particularly in planned communities where rental restrictions may be enforceable. Keep the stamped recorded original in a secure location after recording is confirmed.

Nevada Attorney Note

Nevada real estate attorneys in Las Vegas and Reno are well-versed in the post-2008 statutory changes. For institutional lenders with Nevada portfolios, having counsel review your standard mortgage documents against NRS Chapter 107 and the Foreclosure Mediation Program requirements is worthwhile. For private lenders and seller-financed deals, even a brief consultation before closing can prevent issues that are expensive to correct after recording.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Create your Nevada Mortgage Deed in under 5 minutes.

Answer a few questions and download a Nevada-compliant document, ready for the state agency.