Illinois Mortgage Deed Overview

Illinois is a judicial foreclosure state governed by the Illinois Mortgage Foreclosure Law (735 ILCS 5/Art. XV), one of the more detailed statutory foreclosure frameworks in the Midwest. Mortgage deeds are recorded at the County Recorder of Deeds in the county where the property sits, and the difference between filing in Cook County and filing downstate is substantial. Cook County operates at much higher volume, has slightly different formatting requirements, and charges higher fees than most other counties.

Illinois imposes no mortgage tax, but there is a real estate transfer tax of $0.50 per $500 of consideration on conveyances of ownership. Mortgage deeds create a security interest rather than a transfer of ownership, so the transfer tax generally does not apply to the mortgage itself. Recording fees in Cook County typically exceed those in other Illinois counties by a meaningful margin. All mortgage deeds must be notarized before recording, and no additional witnesses are required.

$50

Recording fee

$0.50 per $500

Transfer tax

Required

Notarization

0

Witnesses required

Illinois Requirements

Illinois recording requirements are uniform at the state level, but Cook County has its own operational quirks that practitioners learn to navigate. Documents must meet Illinois statutory requirements for content and must be notarized. Cook County has specific margin, font, and first-page formatting rules that can result in rejection if the document does not conform. Calling the Cook County Recorder's office or checking their website for current standards before filing is advisable for any Cook County filing.

Illinois Specific Note

Cook County has notably higher recording fees than the rest of Illinois and processes documents through a high-volume office. If your property is in Chicago or a Cook County suburb, confirm the current fee schedule at cookcountyil.gov before submitting. The Illinois Mortgage Foreclosure Law also requires specific notice provisions in residential mortgage deeds; a residential mortgage that omits required statutory language may limit enforcement options later.

Document Requirements

- Notarization: Must be notarized by an Illinois notary public or authorized notary

- Witnesses: Illinois requires 0 additional witness(es)

- Legal Description: Complete legal description as it appears on the current deed of record

- Parcel Number: Assessor's parcel number or tax ID

- Return Address: Mailing address for returning the recorded document

- Formatting: Standard formatting with adequate margins, black ink, minimum 10-point font

How to File in Illinois

The process differs meaningfully between Cook County and the rest of Illinois. The steps below apply to both, with Cook County-specific notes where relevant.

Prepare the Mortgage Deed

Include the full legal names and addresses of all parties, the complete legal description from the county deed records, the PIN (parcel identification number), the loan amount, and any statutory covenants required by the Illinois Mortgage Foreclosure Law for residential properties. Make sure the first-page header conforms to Cook County formatting standards if the property is in Cook County.

Obtain Notarized Signatures

All required signatories must appear before a licensed Illinois notary public. No additional witnesses are required. Illinois allows remote online notarization under the Illinois Electronic Notarization Act for signers who cannot appear in person, provided they use an Illinois-authorized notary and platform.

Submit to the County Recorder of Deeds

Take or send the notarized mortgage deed to the County Recorder of Deeds in the county where the property sits. Cook County accepts e-recording through approved submitters; most title companies and real estate attorneys file electronically. Downstate counties vary in their e-recording capabilities, so call ahead.

Pay Recording Fees

Fees in Cook County start at approximately $50 for the first page with additional per-page charges. Downstate counties are generally in the $30 to $50 range for a standard mortgage. The Illinois real estate transfer tax does not apply to mortgage deeds, only to conveyances of ownership.

Retain Recorded Copies for All Parties

The recorder returns the document stamped with the book, page, and document number. Keep the recorded original or a certified copy in a safe place. Provide the lender with a copy and retain a copy for your own records. The recording information is the permanent identifier for the mortgage in county records.

Illinois Fees & Costs

Typical costs for filing in Illinois. Actual fees may vary by county.

| Fee / Tax | Amount |

|---|---|

| Recording Fee | $50 |

| Transfer Tax | $0.50 per $500 |

| Notarization | $5 - $25 per signature |

| Certified Copy | $1 - $10 per page |

| Attorney Review (optional) | $150 - $500 |

Illinois Tax Implications

Illinois does not impose a mortgage recording tax, which is a meaningful distinction from states like New York or Tennessee where the tax can be substantial. The Illinois Real Estate Transfer Tax of $0.50 per $500 of consideration applies to deeds that transfer ownership of real property, not to mortgage deeds that create a security interest. Borrowers recording a mortgage in Illinois do not pay transfer tax on the mortgage itself, though they would pay it if the underlying property were being conveyed at the same time.

Chicago imposes its own municipal transfer tax in addition to the state rate, and buyers in the city pay a combined rate of $7.50 per $1,000 of consideration (state plus city). This applies to property sales, not to mortgage recordings, but it is relevant context for buyers purchasing Chicago property simultaneously. Evanston and some other Cook County municipalities also impose local transfer taxes, so confirm local rates when buying or selling within Cook County.

Illinois property taxes are among the higher ones in the country, particularly in Cook County. Property is assessed at one-third of its estimated fair market value, though actual effective rates vary significantly by township and municipality. Foreclosure does not change a property's assessed value mid-year, but a sale can result in reassessment in subsequent tax years. Homeowners who qualify for the homeowner exemption should confirm that exemption status is not disrupted by any change in ownership.

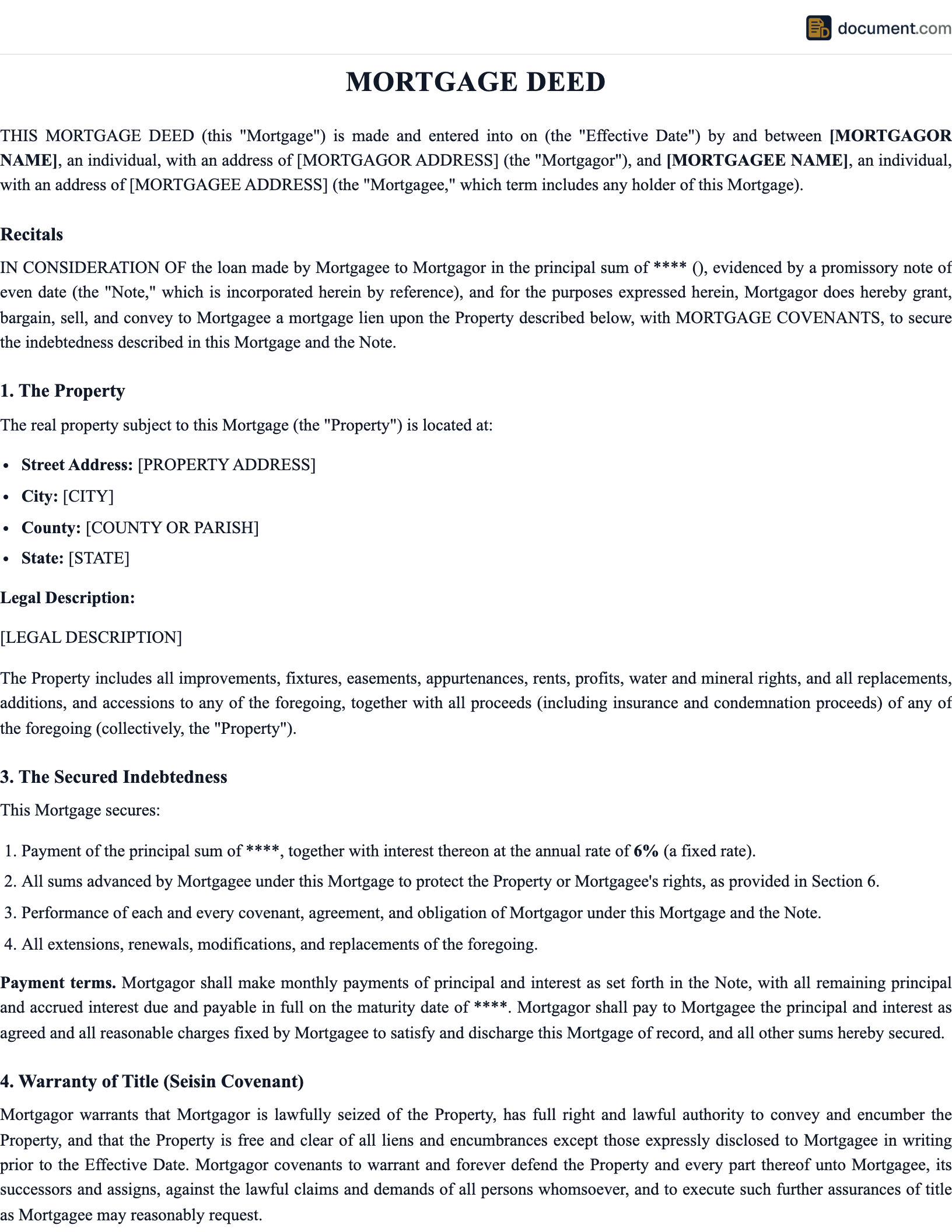

Sample Illinois Mortgage Deed

Preview of our Illinois-specific template. Your document will include all fields required for recording in any Illinois county.

MORTGAGE DEED

STATE OF ILLINOIS

Legal Document

PARTY INFORMATION

Name: [Full Legal Name]

Address: [Illinois Address]

County: [County]

PROPERTY DESCRIPTION

County: [County] State: Illinois

Legal Description: [Per Recorded Plat]

Parcel No.: [APN]

Illinois Mortgage Deed FAQ

Common questions about filing in Illinois, including requirements, fees, and tax implications.

Official Illinois Resources

Official state resources for verifying requirements and finding your local recording office.

Important Considerations

Cook County deserves specific attention because it is functionally a different operating environment from the rest of Illinois for real estate purposes. Recording fees are higher, processing is handled at higher volume, and the Illinois Mortgage Foreclosure Law's court system in Cook County has historically experienced longer timelines than downstate courts. If your property is in Cook County, verify current filing requirements directly with the Recorder's office rather than relying on general Illinois guidance.

Illinois residential mortgage deeds should reference or include the statutory covenants set out in the Illinois Mortgage Foreclosure Law to preserve all standard lender remedies. A residential mortgage that omits required disclosure language may limit the remedies available to the lender in foreclosure. For commercial mortgages, different rules apply and the parties have more flexibility to customize the mortgage terms.

The Illinois Mortgage Foreclosure Law also gives borrowers important rights during foreclosure, including a grace period and the right to reinstate the loan before judgment by paying the arrears rather than the full balance. Lenders who want to preserve the right to a deficiency judgment after foreclosure must follow specific statutory procedures. Understanding these rights and obligations before executing a mortgage deed helps both parties set realistic expectations.

Working With an Illinois Real Estate Attorney

Illinois real estate transactions, particularly in the Chicago area, typically involve attorneys on both sides of the transaction. The Illinois State Bar Association has a lawyer referral service that can connect you with a real estate attorney familiar with Cook County or downstate practice. For residential mortgages, many attorneys offer flat-fee review services that are well worth the cost given the Illinois Mortgage Foreclosure Law's requirements.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Important Considerations

Before proceeding with your document, there are several important factors to consider. Each real estate transaction is unique, and understanding the specific requirements and implications of your situation will help ensure a smooth and legally compliant process.

Real estate laws and regulations are subject to change, and local requirements may differ from state-level rules. It is always advisable to verify current requirements with your local recording office before submitting any documents for recording.

If your transaction involves complex circumstances such as multiple parties, commercial properties, trusts, estates, or interstate elements, consulting with a licensed real estate attorney is strongly recommended. An attorney can provide guidance specific to your situation and help you avoid potential legal issues.

Keep copies of all documents related to your real estate transaction in a safe place. Recorded documents become part of the public record, but having your own copies ensures you can reference the terms and conditions at any time. Digital copies stored securely are also recommended as a backup.

Professional Recommendation

While our templates are designed to be comprehensive and legally compliant, we recommend having your completed document reviewed by a licensed attorney before recording, especially for high-value transactions or complex situations. Many attorneys offer flat-fee document review services that provide peace of mind at a reasonable cost.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Create your Illinois Mortgage Deed in under 5 minutes.

Answer a few questions and download a Illinois-compliant document, ready for the state agency.