Alabama Mortgage Deed Overview

Alabama is one of a shrinking number of states that still uses a mortgage deed rather than a deed of trust to secure real property loans. When a borrower signs an Alabama mortgage deed, they convey a lien interest in the property to the lender as security for the debt while retaining title and possession. The lender does not take actual title; they hold a secured interest that can only be enforced through the courts.

Mortgage deeds in Alabama are recorded at the county probate court, not a county recorder or register of deeds. Alabama's 67 probate judges serve dual roles as court officials and recording officers for real property instruments. Recording fees start around $13 for the first page. Alabama has no state-level real estate transfer tax, so there is no documentary stamp or mortgage tax charged on the instrument. Notarization by an Alabama notary public is required; no witnesses are needed beyond the notary.

$13

Recording fee

None

Transfer tax

Required

Notarization

0

Witnesses required

Alabama Requirements

Alabama's recording requirements are governed primarily by Title 35 of the Alabama Code. A mortgage deed must be signed by the mortgagor, acknowledged before a notary public, and delivered to the county probate court in the county where the property is located. Because Alabama follows a judicial foreclosure model, a properly executed and recorded mortgage is the foundation of any enforcement action, making document accuracy critical from the outset.

Alabama Specific Note

If the mortgaged property is the borrower's homestead, Alabama law requires the mortgagor's spouse to also sign the mortgage deed, even if the spouse is not on the title. Skipping this signature can make the mortgage unenforceable against the homestead interest. Alabama has no state transfer tax on mortgage deeds, but per-page recording fees apply. Confirm current fees with the probate court before filing.

Document Requirements

- Notarization: Must be notarized by an Alabama notary public or authorized notary

- Witnesses: Alabama requires 0 additional witness(es)

- Legal Description: Complete legal description as it appears on the current deed of record

- Parcel Number: Assessor's parcel number or tax ID

- Return Address: Mailing address for returning the recorded document

- Formatting: Standard formatting with adequate margins, black ink, minimum 10-point font

How to File in Alabama

Alabama routes all real property recording through the probate court rather than a separate recorder's office. The process is straightforward but requires careful attention to the homestead spousal signature rule before notarization.

Prepare the Document

Complete all required fields including the full legal description from the current deed of record, the mortgagor and mortgagee names and addresses, and the amount of the secured obligation. If the property is the mortgagor's homestead, identify all spouses who must also sign.

Get the Document Notarized

All signing parties must appear before an Alabama notary public with government-issued photo ID. The notary must apply their official seal and include their commission expiration date. No witnesses beyond the notary are required under Alabama law.

File With the County Probate Court

Bring the original notarized mortgage deed to the probate court in the Alabama county where the property is situated. The probate judge's office handles real property recording. Some counties accept mail-in recording and a handful offer e-recording through approved vendors.

Pay Recording Fees

Alabama charges a per-page recording fee starting around $13 for the first page. There is no state transfer tax on mortgages. Bring payment in the form accepted by your county; cash, check, and money order are commonly accepted, but credit card acceptance varies by office.

Retain the Stamped Original

The probate court will return the recorded document with a stamp showing the book and page number of the official record. Store this original in a secure location. When the loan is paid off, the lender must file a satisfaction of mortgage with the same probate court to release the lien from the record.

Alabama Fees & Costs

Typical costs for filing in Alabama. Actual fees may vary by county.

| Fee / Tax | Amount |

|---|---|

| Recording Fee | $13 |

| Transfer Tax | None |

| Notarization | $5 - $25 per signature |

| Certified Copy | $1 - $10 per page |

| Attorney Review (optional) | $150 - $500 |

Alabama Tax Implications

Alabama does not levy a state real estate transfer tax, which sets it apart from many southern states. When a mortgage deed is recorded, no documentary stamp tax or mortgage excise tax is charged on the instrument. This is a meaningful cost difference compared to states like Florida, which charges significant documentary stamp taxes on both deeds and mortgage notes.

Alabama does impose property taxes administered at the county level by each county's revenue commissioner or tax assessor. Property is assessed at a percentage of market value that varies by property class; residential homestead property is assessed at 10% of market value, while non-homestead residential property is assessed at 10% as well, and commercial and industrial property at 20%. Mortgaged property remains taxable throughout the loan term, and lenders typically collect escrow for taxes as part of the monthly payment.

Borrowers who pay off a mortgage should request and record a satisfaction of mortgage promptly. An unreleased mortgage on the public record can complicate a future sale or refinance. If a lender fails to file the release within 60 days of payoff, Alabama law provides remedies including a statutory penalty against the lender.

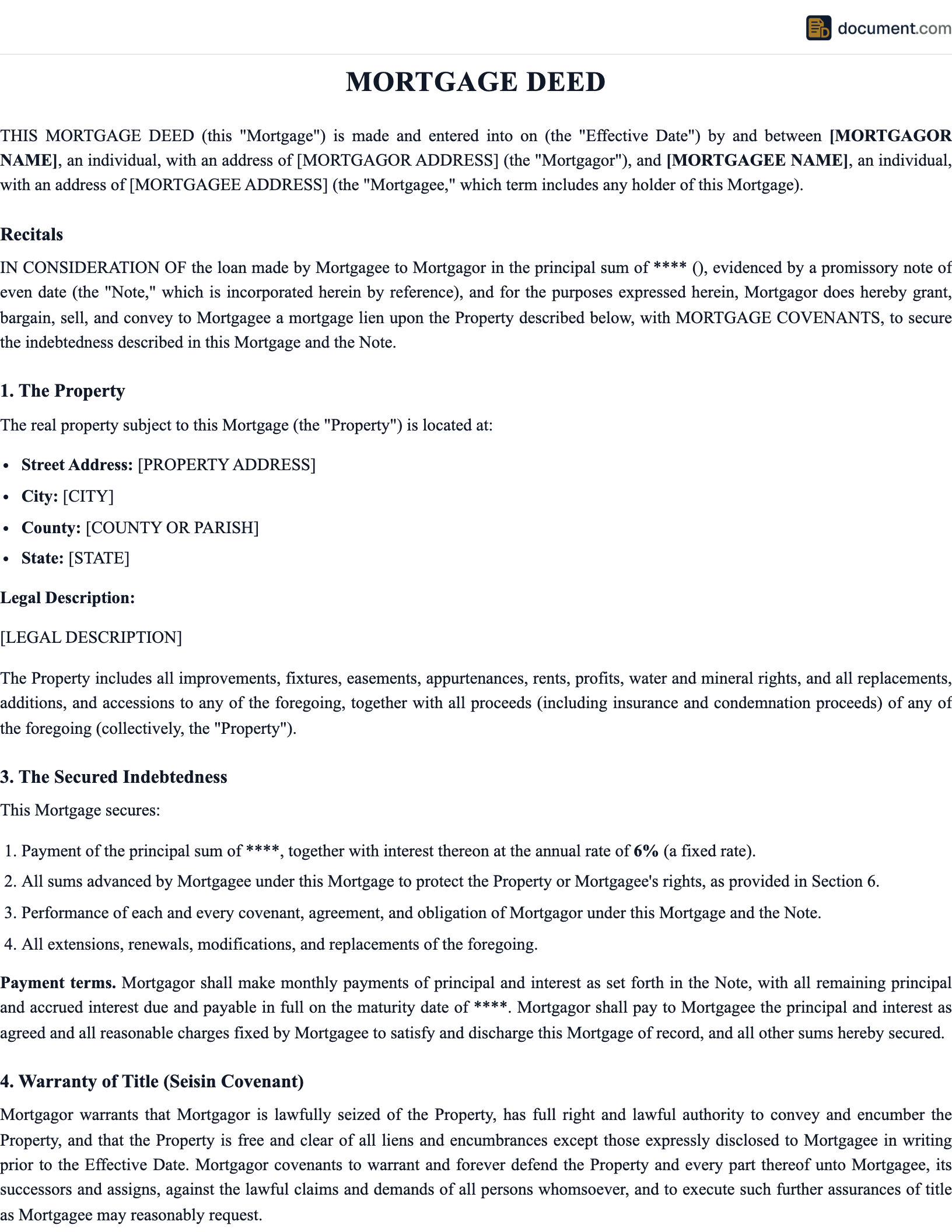

Sample Alabama Mortgage Deed

Preview of our Alabama-specific template. Your document will include all fields required for recording in any Alabama county.

MORTGAGE DEED

STATE OF ALABAMA

Legal Document

PARTY INFORMATION

Name: [Full Legal Name]

Address: [Alabama Address]

County: [County]

PROPERTY DESCRIPTION

County: [County] State: Alabama

Legal Description: [Per Recorded Plat]

Parcel No.: [APN]

Alabama Mortgage Deed FAQ

Common questions about filing in Alabama, including requirements, fees, and tax implications.

Official Alabama Resources

Official state resources for verifying requirements and finding your local recording office.

Important Considerations for Alabama Mortgage Deeds

Alabama's judicial foreclosure requirement is the single biggest practical difference between an Alabama mortgage and a deed of trust used in many other states. Because lenders must go to court to foreclose, the process routinely takes a year or longer from the first missed payment to a completed sale. This affects how lenders price Alabama mortgages and what workout options they may offer a borrower in default.

The homestead spousal signature rule catches many borrowers and even some title professionals by surprise. If the mortgaged property is the borrower's principal residence, the borrower's spouse must sign the mortgage regardless of whether they are on the deed or the loan. This requirement comes from Alabama's homestead protection statutes and is not waivable by contract. Missing this signature gives the non-signing spouse grounds to challenge the mortgage in court.

Alabama also provides borrowers a one-year statutory right of redemption after a mortgage foreclosure sale. During that year, the borrower can reclaim the property by paying the foreclosure sale price plus interest and costs. This redemption right is a significant consumer protection, but it also creates uncertainty for buyers at foreclosure sales, which is why investors in Alabama foreclosure properties frequently factor redemption risk into their bids.

Working with an Alabama Real Estate Attorney

The homestead signature rule and the judicial foreclosure framework make Alabama mortgage transactions more legally sensitive than many borrowers expect. An Alabama real estate attorney can confirm whether the homestead requirement applies, review the legal description against the probate court record, and advise on any title issues before recording. Many Alabama attorneys offer fixed-fee residential mortgage document review.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Important Considerations

Alabama's judicial foreclosure requirement is the single biggest practical difference between an Alabama mortgage and a deed of trust used in many other states. Because lenders must go to court to foreclose, the process routinely takes a year or longer from the first missed payment to a completed sale. This affects how lenders price Alabama mortgages and what workout options they may offer a borrower in default.

The homestead spousal signature rule catches many borrowers and even some title professionals by surprise. If the mortgaged property is the borrower's principal residence, the borrower's spouse must sign the mortgage regardless of whether they are on the deed or the loan. This requirement comes from Alabama's homestead protection statutes and is not waivable by contract.

Alabama provides borrowers a one-year statutory right of redemption after a mortgage foreclosure sale. During that year, the borrower can reclaim the property by paying the foreclosure sale price plus interest and costs. Buyers at foreclosure sales factor this redemption risk into their bids, which is one reason Alabama foreclosure auction prices often run lower than comparable sales prices.

When a loan is paid off, the lender is obligated to record a satisfaction of mortgage with the county probate court within 60 days. Keep the stamped original recorded mortgage deed in your personal files alongside the satisfaction when it arrives. The probate court index is your authoritative reference if questions ever arise about the lien's current status. are also recommended as a backup.

Professional Recommendation

While our templates are designed to be comprehensive and legally compliant, we recommend having your completed document reviewed by a licensed attorney before recording, especially for high-value transactions or complex situations. Many attorneys offer flat-fee document review services that provide peace of mind at a reasonable cost.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Create your Alabama Mortgage Deed in under 5 minutes.

Answer a few questions and download a Alabama-compliant document, ready for the state agency.