What Are Nonprofit Corporate Bylaws?

Nonprofit corporate bylaws are the internal operating manual of a tax-exempt corporation. While the articles of incorporation are the short public charter filed with the Secretary of State to create the organization as a legal entity, the bylaws are the longer internal document that defines how the nonprofit will actually govern itself on a day-to-day basis. Bylaws set out the composition of the board of directors, the rules for electing directors and officers, the procedures for holding meetings, the quorum and voting requirements, the structure of committees, the rules for handling conflicts of interest, the policies for indemnifying directors against personal liability, and the procedure for amending the bylaws themselves.

For nonprofits seeking recognition as a 501(c)(3) public charity or private foundation, bylaws are especially important because the IRS reviews them as part of the Form 1023 application. The IRS looks for specific provisions: a purpose clause limited to exempt activities under section 501(c)(3); a dissolution clause requiring assets to be distributed only to other exempt organizations or governments upon dissolution; a prohibition on private inurement; a limit on political campaign activity and substantial lobbying; and a conflict of interest policy consistent with the IRS sample in Appendix A of the Form 1023 instructions. Bylaws that are missing any of these required provisions can cause delays or denials of tax-exempt status.

State law also regulates nonprofit bylaws through state nonprofit corporation acts. Most states have adopted some version of the Revised Model Nonprofit Corporation Act (RMNCA), but California, New York, and a handful of other states have distinct statutory frameworks with unique requirements. State law governs issues such as the minimum number of directors (usually 1 or 3), the required officer positions, the rules for member voting rights (if the nonprofit has members), the notice requirements for meetings, the rules for board composition and independence, and the procedures for dissolution and asset distribution.

Most 501(c)(3) public charities in the United States operate as non-member (board-only) organizations, in which the board of directors is self-perpetuating: the board elects its own successors, and there are no voting members. This structure is simpler to govern and avoids the complexity of managing member rights, annual member meetings, and member votes. Member-based nonprofits — which are more common among professional associations, trade groups, clubs, and some religious organizations — have a more complex governance structure in which members elect the directors and may have other voting rights. The bylaws should clearly state which structure the organization has chosen.

Our attorney-reviewed nonprofit bylaws templates include every provision required by the IRS for 501(c)(3) recognition, as well as the state-specific requirements of your state of incorporation. The templates include optional provisions (such as audit committees, executive committees, and advisory boards) that you can activate or remove depending on the size and complexity of your organization. Whether you are forming a new nonprofit and preparing to file Form 1023, or updating the bylaws of an existing organization to meet current governance best practices, our templates provide the legal framework you need.

Mission Alignment

Anchor the organization's governance to its charitable purpose and exempt activities

IRS Compliance

Meet every 501(c)(3) requirement for Form 1023 approval and ongoing exempt status

Board Accountability

Establish clear roles, voting rules, and conflict-of-interest procedures for the board

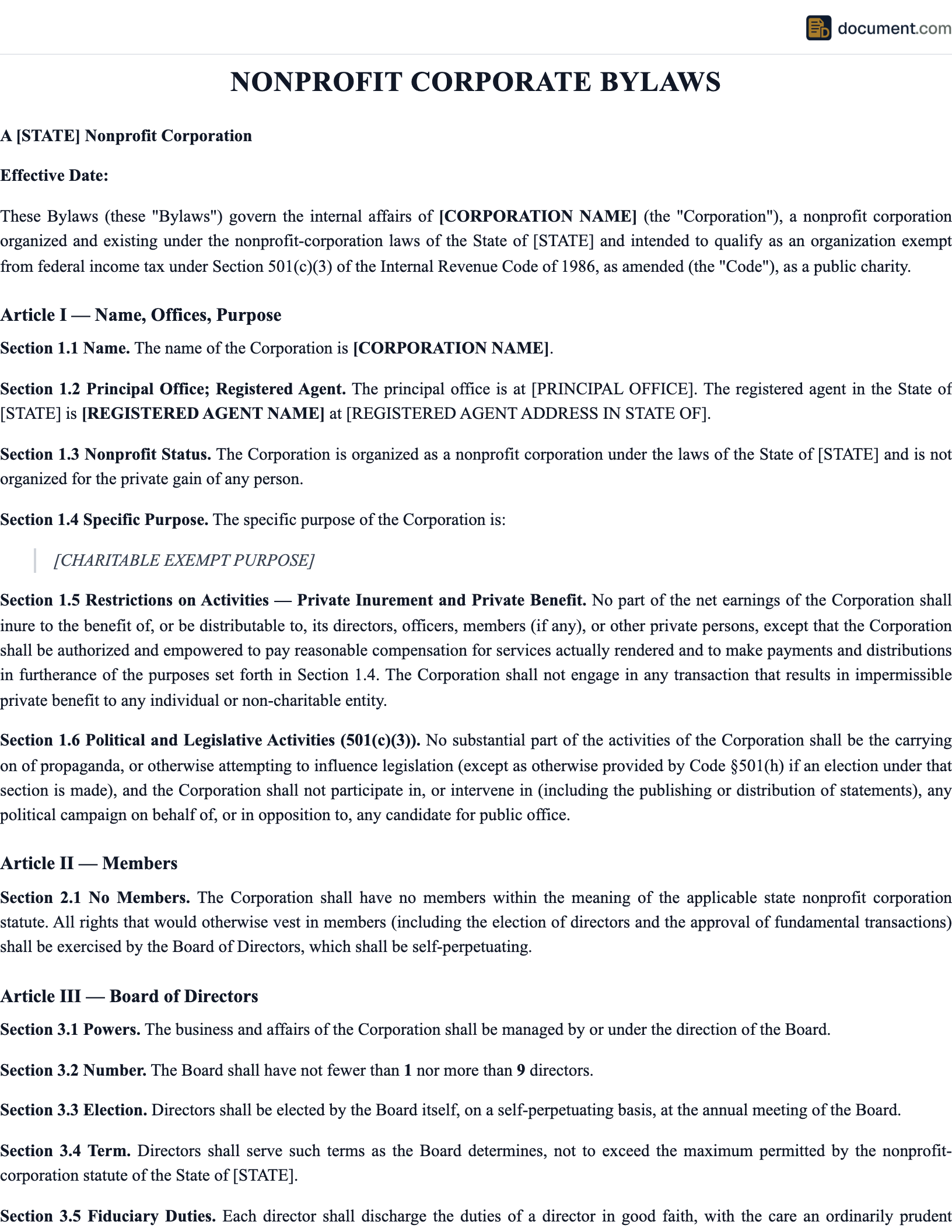

Nonprofit Bylaws Form Preview

Below is a visual preview showing the structure of a set of IRS-compliant 501(c)(3) bylaws. Your completed document will be fully formatted with all required articles, exhibits, and the conflict of interest policy as an attached exhibit.

Bylaws of

[Nonprofit Name], a nonprofit corporation

Article I: Name, Purpose, and Offices

Article II: Membership

Article III: Board of Directors

Article IV: Officers

Article V: Committees

Article VI: Conflict of Interest Policy

Adoption & Certification

Secretary Signature

Date Adopted

Key Sections of Nonprofit Bylaws

A complete set of 501(c)(3) bylaws contains a standard set of articles that the IRS and state regulators expect. Each section plays a specific role in establishing governance, compliance, and accountability. Below is an overview of the nine core sections included in our template.

Name and Purpose

States the nonprofit's legal name and its tax-exempt charitable, religious, educational, or scientific purpose

Membership Structure

Defines whether the nonprofit has voting members, their rights, dues, and eligibility requirements

Board of Directors

Board composition, terms, election process, meetings, quorum, and removal procedures

Officers

Required officers (president, secretary, treasurer), duties, election, and succession

Committees

Standing and ad-hoc committees including executive, finance, audit, and nominating committees

Conflicts of Interest

IRS-required conflict of interest policy covering disclosure, recusal, and enforcement

Financial Management

Fiscal year, financial reporting, annual audit, and treasurer's responsibilities

Indemnification

Protection for directors and officers against personal liability for good-faith actions

Amendment and Dissolution

Procedures for amending bylaws and distributing assets upon dissolution to another 501(c)(3)

Member vs Non-Member Nonprofit

One of the first decisions in drafting nonprofit bylaws is whether the organization will have voting members or operate as a board-only (non-member) nonprofit. This decision fundamentally shapes the rest of the bylaws.

"We want the simplest possible governance structure for our public charity."

Choose a non-member (board-only) nonprofit. The board of directors is self-perpetuating — directors elect their own successors — and there are no voting members. This is the structure used by most U.S. public charities because it is simpler to govern and easier to maintain compliance.

"Our community will be deeply involved and should vote on key matters."

Choose a member-based nonprofit. Members typically elect the directors, vote on amendments to the articles and bylaws, and may have other rights defined in the bylaws. This is common for professional associations, trade groups, membership clubs, and some religious congregations.

"We want dues-paying supporters but not formal voting members."

Choose a non-member nonprofit with a supporters program. You can have dues-paying supporters, friends, or patrons who receive benefits (e.g., newsletters, events) without having legal voting rights under the bylaws. This preserves simple governance while still engaging the community.

Nonprofit Bylaws vs Articles of Incorporation

New nonprofits often confuse bylaws with articles of incorporation. Both documents are necessary, but they serve different functions.

| Feature | Bylaws | Articles of Incorporation |

|---|---|---|

| Filed with state | No | Yes |

| Public document | Typically no | Yes |

| Creates legal entity | No | Yes |

| Governs day-to-day operations | Yes | No |

| Amendment difficulty | Easier (internal vote) | Harder (state filing) |

| Length | 10 - 30 pages | 1 - 3 pages |

| Required for Form 1023 | Yes (attached) | Yes (attached) |

How to Draft and Adopt Nonprofit Bylaws

Adopting bylaws is typically the first major action of a newly formed nonprofit board. Follow these steps to draft, review, and formally adopt a set of bylaws that will support Form 1023 approval.

File Articles of Incorporation First

Bylaws reference the articles, so file the articles of incorporation with the Secretary of State before drafting bylaws. Make sure the articles include the required IRS purpose and dissolution clauses.

Choose Member or Non-Member Structure

Decide whether the nonprofit will have voting members. This decision drives most of the rest of the bylaws. Most 501(c)(3) public charities choose the board-only structure.

Set Board Size and Composition

Decide the minimum and maximum number of directors. The IRS recommends at least 3 unrelated directors for 501(c)(3) organizations. Most states require a minimum of 1 or 3.

Draft Each Required Article

Using our template, fill in each required article: name and purpose, membership, board, officers, committees, conflict of interest, indemnification, financial management, and amendment/dissolution.

Attach the Conflict of Interest Policy

Include the IRS sample conflict of interest policy (from Form 1023 Appendix A) as an exhibit. Every director must sign an annual disclosure form under the policy.

Hold the Organizational Meeting

Convene the initial board of directors (named in the articles or elected by the incorporator) and hold the organizational meeting. The board formally adopts the bylaws by resolution.

Sign and File Internally

The secretary signs and dates the bylaws. Keep the original in the corporate minute book along with the articles, organizational minutes, and other foundational documents.

Submit with Form 1023

Attach a copy of the signed bylaws to Form 1023 (or Form 1023-EZ if eligible) when applying for 501(c)(3) recognition with the IRS. The IRS will review the bylaws for required provisions.

IRS 501(c)(3) Requirements

To qualify for federal tax-exempt status under section 501(c)(3), a nonprofit's organizing documents (articles of incorporation and bylaws) must meet the "organizational test" set forth in IRS regulations. This means the documents must limit the organization's purposes to exempt activities and must not expressly empower it to engage in non-exempt activities (except as an insubstantial part of its operations).

The Organizational Test

Under Treas. Reg. §1.501(c)(3)-1(b), an organization is organized exclusively for an exempt purpose only if its articles of incorporation: (1) limit the purposes to one or more exempt purposes; (2) do not expressly empower the organization to engage in activities that are not in furtherance of exempt purposes (other than insubstantial lobbying); (3) contain a dissolution clause; and (4) contain provisions prohibiting private inurement. Bylaws should be consistent with and supplement these articles provisions.

Required IRS Provisions

- Exempt Purpose Clause: The purpose statement must limit the organization to one or more exempt purposes: charitable, religious, educational, scientific, literary, testing for public safety, fostering amateur sports competition, or preventing cruelty to children or animals.

- Dissolution Clause: Upon dissolution, all assets must be distributed to another 501(c)(3) organization, the federal government, or a state or local government for a public purpose. This clause prevents private distribution of assets accumulated through tax-exempt status.

- Private Inurement Prohibition: No part of the net earnings of the organization may inure to the benefit of any private individual or shareholder. Reasonable compensation for services is permitted.

- Political Activity Prohibition: The organization cannot participate in political campaigns for or against any candidate for public office. Even an endorsement can jeopardize exempt status.

- Lobbying Limitation: Lobbying activities (attempting to influence legislation) must be no more than an insubstantial part of the organization's activities, unless the organization has made a 501(h) election.

- Conflict of Interest Policy: Though not strictly required by the Code, the IRS recommends and expects a written conflict of interest policy. Form 1023 asks whether the organization has adopted one.

Conflict of Interest Policy

Every 501(c)(3) nonprofit should adopt a written conflict of interest policy. The IRS sample policy in Appendix A of the Form 1023 instructions has become the de facto standard and is incorporated (with minor adjustments) into our bylaws template.

Why Conflicts of Interest Matter

Conflicts of interest are one of the most common reasons nonprofits lose their tax-exempt status or face penalties under the intermediate sanctions rules of section 4958. When directors, officers, or key employees engage in transactions that personally benefit them at the expense of the organization, the IRS may treat those transactions as excess benefit transactions and impose penalty taxes on the recipients and on the organization managers who approved them.

Required Policy Elements

Annual Disclosure

All directors and officers must sign a written annual disclosure statement listing all financial interests that could create a conflict

Duty to Disclose

Directors must disclose any actual or possible conflict when a relevant matter arises, before any discussion or vote

Recusal from Vote

Conflicted directors must leave the meeting during discussion and vote on the conflicted matter

Independent Review

The remaining board members (or a committee) must determine whether the transaction is in the organization's best interest

Documentation

Minutes must document the conflict, the discussion, and the vote, including the names of directors who recused themselves

Violations

The policy should describe the consequences of violations, which may include removal from the board

Board Governance Best Practices

The IRS governance checklist on Form 990 asks about practices that go beyond the legal minimum. Incorporating these best practices into bylaws signals to the IRS, state regulators, donors, and grantmakers that the nonprofit is well-governed.

- Majority Independent Directors: The majority of the board should be independent — not related by blood, marriage, or business to other directors or employees, and not compensated by the organization except for reasonable director expenses.

- Staggered Terms: Stagger director terms so that only one-third of the board turns over each year. This preserves institutional knowledge and board continuity.

- Term Limits: Consider term limits (e.g., two consecutive three-year terms) to ensure board renewal while allowing dedicated directors time to contribute meaningfully.

- Whistleblower Policy: Adopt a whistleblower policy protecting employees and volunteers who report financial misconduct or policy violations from retaliation.

- Document Retention Policy: Adopt a document retention and destruction policy that satisfies IRS recordkeeping requirements and Sarbanes-Oxley whistleblower protections.

- Executive Compensation Review: The board (or a committee of independent directors) should review and approve the executive director's compensation annually using comparable salary data, and document the process.

- Form 990 Review: The full board should review the organization's Form 990 before it is filed with the IRS. Form 990 itself asks whether this review occurred.

State Legal Requirements for Nonprofit Bylaws

In addition to IRS requirements, nonprofit bylaws must comply with the nonprofit corporation statute of the state of incorporation. These statutes vary significantly, particularly regarding minimum board size, required officers, member rights, and meeting procedures.

Common State Variations

- Minimum Directors: Most states require at least 1 director, but California requires at least 1 and recommends 3, New York requires at least 3, and Tennessee requires at least 3. The IRS recommends 3 for all 501(c)(3) organizations.

- Required Officers: Most states require a president (or chair), secretary, and treasurer at a minimum. Some states allow one person to hold multiple offices, while others (like California) prohibit the same person from serving as both president and secretary or treasurer.

- California Nonprofit Integrity Act: California imposes additional requirements on nonprofits with annual gross revenue over $2 million, including an audit committee and an independent audit. Bylaws should reference compliance with the Act.

- New York Nonprofit Revitalization Act: New York imposes specific requirements on nonprofit governance, including conflict of interest policies, whistleblower policies (for organizations with 20+ employees), and audit requirements for organizations with $1 million or more in revenue.

- Meeting Notice Requirements: State law typically sets minimum notice periods for board meetings (often 2 to 10 days) and annual member meetings (often 10 to 60 days). Bylaws can require longer notice but not shorter.

Sample Nonprofit Bylaws

Below is a condensed preview of our 501(c)(3) nonprofit bylaws template. Your completed bylaws will be fully customized for your state, organizational structure, and specific governance preferences.

BYLAWS OF [NONPROFIT NAME]

A Nonprofit Corporation

ARTICLE I: NAME AND PURPOSE

Section 1.1. Name. The name of this corporation is[Nonprofit Name](the "Corporation").

Section 1.2. Purpose. The Corporation is organized exclusively for charitable, educational, and scientific purposes within the meaning of section 501(c)(3) of the Internal Revenue Code, including: [Specific charitable purposes].

ARTICLE II: MEMBERSHIP

The Corporation shall have no members. All rights that would otherwise vest in members shall vest in the Board of Directors.

ARTICLE III: BOARD OF DIRECTORS

Section 3.1. Number and Qualifications. The Board shall consist of not fewer than [5] nor more than [15] directors.

Section 3.2. Term. Each director shall serve a term of[three] years, with terms staggered so that approximately one-third of the directors are elected each year.

Section 3.3. Meetings. The Board shall hold an annual meeting and at least[quarterly] regular meetings.

Section 3.4. Quorum. A majority of directors then in office shall constitute a quorum for the transaction of business.

ARTICLE IV: OFFICERS

The officers of the Corporation shall be a President, Vice President, Secretary, and Treasurer, each elected annually by the Board.

ARTICLE V: CONFLICTS OF INTEREST

The Corporation shall adopt and enforce a written Conflict of Interest Policy consistent with the IRS sample policy in Appendix A of the Form 1023 Instructions, which is attached to these bylaws as Exhibit A.

ARTICLE VI: INDEMNIFICATION

To the fullest extent permitted by [State] law, the Corporation shall indemnify any director, officer, employee, or agent against expenses, judgments, fines, and settlements incurred in connection with any action brought against them by reason of their service to the Corporation...

ARTICLE VII: DISSOLUTION

Upon dissolution of the Corporation, assets shall be distributed for one or more exempt purposes within the meaning of section 501(c)(3) of the Internal Revenue Code, or shall be distributed to the federal government or to a state or local government for a public purpose...

ARTICLE VIII: AMENDMENT

These Bylaws may be amended by a two-thirds vote of the directors then in office, provided that written notice of the proposed amendment is given to each director at least [30] days before the meeting.

Frequently Asked Questions

Answers to the most common questions about nonprofit bylaws, 501(c)(3) governance requirements, and board operations.

Official Resources

Government and recognized sector resources for nonprofit governance, 501(c)(3) compliance, and board best practices.

IRS - Form 1023 Application

Application for recognition of 501(c)(3) tax-exempt status

IRS - Form 1023 Instructions

Includes the sample conflict of interest policy in Appendix A

IRS - Governance and 501(c)(3) Organizations

IRS guidance on governance practices for tax-exempt nonprofits

National Council of Nonprofits - Governance

Governance resources, sample policies, and best practices

BoardSource

Leading authority on nonprofit board governance and leadership

California AG - Charities

California Attorney General registry and nonprofit compliance

New York Charities Bureau

New York charities registration and reporting

Candid (formerly Foundation Center)

Nonprofit data, fundraising research, and organizational guidance

Create your Nonprofit Corporate Bylaws in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.